Last updated: May 24, 2026

Quick Answer: A first lien HELOC replaces your traditional mortgage entirely, giving you a revolving line of credit secured by your home as the primary — or "first" — lien. Real estate investors choose it over a standard mortgage because it offers flexible access to equity, interest-only payment options during the draw period, and the ability to pay down principal aggressively when cash flow allows — without the rigid structure of a 30-year fixed loan.

Key Takeaways

- A first lien HELOC sits in the first lien position on your property, meaning it replaces your mortgage rather than sitting behind it like a second mortgage.

- Investors use it to access equity on demand, fund deals faster, and reduce interest costs by sweeping income directly into the account.

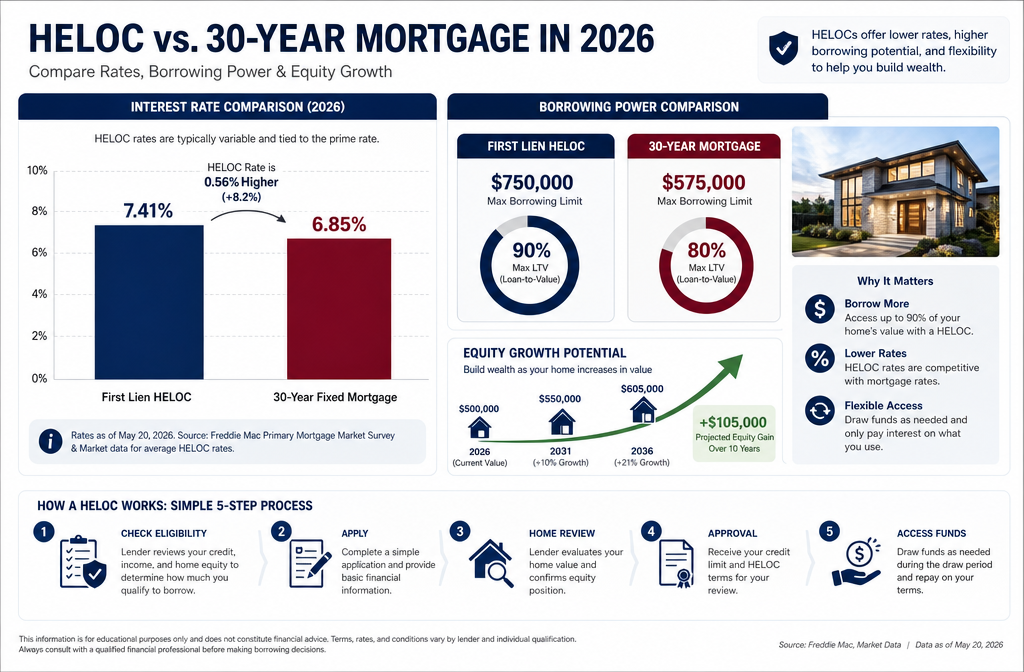

- Current first lien HELOC rates in 2026 hover around 7.41% (variable), which is competitive with many conventional mortgage products depending on your credit profile.

- You typically need a credit score of 680 or higher to qualify, though some lenders prefer 720+.

- The draw period (usually 10 years) allows interest-only HELOC payments, which keeps monthly obligations low while you deploy capital.

- Not every bank offers a first lien HELOC — you'll need to shop specialty lenders and credit unions.

- This strategy works particularly well for house flippers, rental property investors, and self-employed borrowers who need flexible, reusable credit.

- The biggest risk is the variable rate structure — if rates spike, your payment can climb fast.

- Closing costs are generally lower than a traditional mortgage, often ranging from 2% to 5% of the credit limit.

- The all-in-one HELOC mortgage strategy (also called an all-in-one mortgage) takes this concept further by linking your checking account directly to the HELOC balance.

What Exactly Is a First Lien HELOC and How Does It Work?

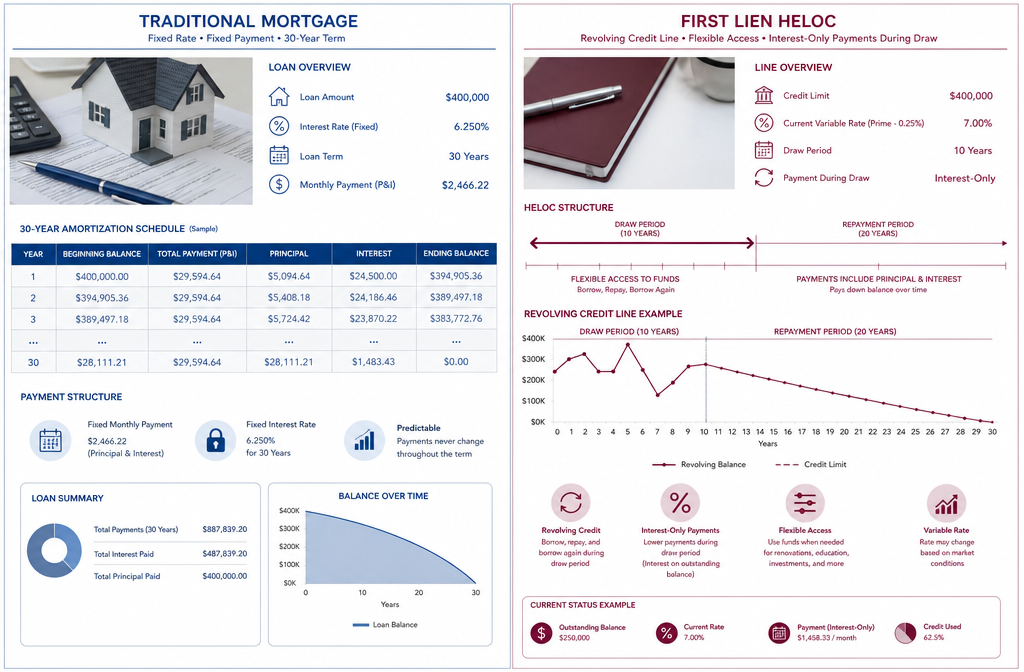

A first lien HELOC is a home equity line of credit that holds the primary lien position on your property — meaning it's the first debt paid if the home is sold or foreclosed. Unlike a standard HELOC, which sits behind your existing mortgage as a second lien, this product replaces your mortgage entirely.

Here's the basic mechanics of how a HELOC works in first lien position:

- You borrow against your home's equity up to a set credit limit (typically 80–90% of the home's appraised value, minus any existing debt).

- The draw period (usually 10 years) lets you borrow, repay, and re-borrow as needed — like a credit card secured by real estate.

- During the draw period, most lenders allow interest-only HELOC payments, which keeps your minimum payment low.

- After the draw period ends, the loan enters a repayment phase (usually 10–20 years), during which you pay both principal and interest.

- Your income can be deposited directly into the HELOC account, reducing the daily balance and cutting the interest you owe — this is the core of the all-in-one HELOC mortgage strategy.

Think of it like this: a traditional mortgage is a one-way street. You borrow, you pay it down, and that's it. A first lien HELOC is a two-way street. You can pull money out, push money in, and repeat the cycle throughout the draw period.

Home equity meaning in this context: The equity in your home is the difference between what it's worth and what you owe. A first lien HELOC lets you treat that equity like a checking account — liquid, accessible, and working for you instead of sitting idle.

First Lien HELOC: Why Investors Choose It Over a Mortgage

This is the core of the conversation — and honestly, the real estate finance world has been gatekeeping this strategy for too long.

The short answer: Investors choose a first lien HELOC over a traditional mortgage because it gives them control, flexibility, and speed that a fixed 30-year loan simply can't match.

Here's the breakdown of why the first lien HELOC strategy is getting serious traction in 2026:

1. Flexibility That a Mortgage Can't Touch

A conventional mortgage locks you into a fixed payment schedule. Miss a payment, and you're in trouble. Pay extra, and the bank keeps the savings in the form of reduced loan term — but you can't pull that money back out easily.

A first lien HELOC flips that dynamic. Pay extra when you have cash flow. Pull funds back out when a deal shows up. The money stays accessible.

2. Interest-Only Payments During the Draw Period

During the draw period, you're only required to pay interest on what you've borrowed. For investors managing multiple properties, this dramatically improves monthly cash flow. That extra cash can go toward down payments on new acquisitions, property repairs, or reserves.

3. The All-In-One Mortgage Strategy

The all-in-one HELOC mortgage (sometimes called an all-in-one mortgage) is the most aggressive version of this approach. Every dollar of income you deposit reduces your outstanding balance — and since HELOC interest is calculated daily on the average balance, your interest costs drop in real time. You're essentially using your paycheck to fight your mortgage balance every single day.

This is a fresh strategy that's gaining real momentum among high-income professionals and self-employed borrowers who have irregular but substantial income.

4. Reusable Credit for Deal Flow

For active investors, the ability to draw, repay, and draw again is extraordinary. Instead of applying for a new mortgage every time a deal comes up, you already have a credit line ready to deploy. That speed can mean the difference between closing a deal and losing it.

5. HELOC vs Mortgage 2026: The Rate Picture

With current mortgage rates in 2026 sitting around 6.11% for a 30-year fixed, and first lien HELOC rates 2026 hovering near 7.41% (variable), the rate gap is real — but many investors find the flexibility worth the premium. And if rates drop, your variable HELOC rate drops with them.

How Is a First Lien HELOC Different From a Traditional Mortgage?

The difference between a HELOC vs mortgage comes down to structure, flexibility, and how interest is calculated.

| Feature | First Lien HELOC | Traditional Mortgage |

|---|---|---|

| Lien position | First | First |

| Payment type | Interest-only (draw period) | Principal + interest |

| Rate type | Variable | Fixed or variable |

| Access to funds | Revolving (reusable) | One-time disbursement |

| Extra payments | Reduce balance immediately | Reduce loan term |

| Funds reusable | Yes | No |

| Typical rate (2026) | ~7.41% (variable) | ~6.11% (30-yr fixed) |

| Closing costs | Lower (2–5%) | Higher (2–6%+) |

HELOC vs second mortgage: Don't confuse a first lien HELOC with a second mortgage or a standard HELOC. A second mortgage (or traditional HELOC) sits behind your primary mortgage in lien position — meaning in a foreclosure, your primary lender gets paid first. A first lien HELOC eliminates that hierarchy by replacing the mortgage entirely.

HELoan vs HELOC: A HELoan (home equity loan) gives you a lump sum at a fixed rate. A HELOC gives you a revolving credit line at a variable rate. For investors who need ongoing access to capital, the HELOC wins on flexibility. For those who want predictable payments, the HELoan has its place.

What Are the Pros and Cons of Using a First Lien HELOC for Real Estate Investing?

The honest answer: The first lien HELOC is an extraordinary tool for the right investor — and the wrong tool for someone who needs payment predictability above all else.

✅ Pros

- Flexible capital access — draw funds when deals appear, repay when cash flow allows

- Interest-only payments keep monthly obligations low during the draw period

- Daily interest calculation means every dollar deposited saves you money immediately

- Reusable credit line eliminates the need to refinance for every new deal

- Lower closing costs than a traditional mortgage in most cases

- Rate drops benefit you — when the Fed cuts rates, your HELOC rate follows

❌ Cons

- Variable rate risk — if rates climb, so does your payment (this is the biggest first lien HELOC con)

- Discipline required — treating your HELOC like a piggy bank can destroy your equity fast

- Limited lender availability — not every bank offers first lien HELOC products

- Repayment phase shock — when the draw period ends, payments can jump significantly

- Not ideal for long-term rate certainty — if you want a locked-in payment for 30 years, this isn't it

So based take: The first lien HELOC pros and cons really come down to your income consistency and financial discipline. High earners with strong cash flow who can sweep income into the account regularly? This strategy is built for them. Investors who need a fixed payment to sleep at night? Stick with a conventional mortgage.

For a deeper look at how smart investors use equity to scale, check out our guide on HELOC on investment property strategies.

How Much Can I Borrow With a First Lien HELOC Compared to a Traditional Mortgage?

Most first lien HELOC lenders will let you borrow up to 80–90% of your home's appraised value, minus any existing liens. In practice, the maximum credit limit depends on your equity, credit profile, and the lender's guidelines.

Example:

- Home value: $500,000

- Maximum LTV (85%): $425,000

- Existing mortgage balance: $0 (first lien HELOC replaces it)

- Available credit line: up to $425,000

Compare that to a conventional mortgage, where you'd typically borrow a fixed amount at closing and have no ability to re-draw without refinancing.

Key constraints:

- Most lenders cap the combined loan-to-value (CLTV) at 80–90%

- Some lenders limit first lien HELOCs to owner-occupied primary residences

- Investment property first lien HELOCs are less common and may carry stricter LTV limits (often 70–75%)

What Credit Score Do I Need to Qualify for a First Lien HELOC?

Most lenders require a minimum credit score of 680 to qualify for a first lien HELOC, but the best rates typically go to borrowers at 720 or above.

Qualification criteria typically include:

- Credit score: 680 minimum (720+ for best rates)

- Debt-to-income ratio (DTI): Generally 43% or lower

- Home equity: At least 10–20% equity remaining after the credit line is established

- Income verification: W-2, tax returns, or bank statements (self-employed borrowers may need 24 months of returns)

- Property type: Owner-occupied primary residences are easiest to qualify; investment properties face tighter standards

Edge case: Self-employed borrowers with strong equity but inconsistent reported income often find the first lien HELOC easier to qualify for than a conventional mortgage — especially if they use bank statement programs offered by some specialty lenders.

Which Banks or Lenders Offer the Best First Lien HELOC Rates?

First lien HELOCs are not offered by every major bank — this is one of the most gatekept products in residential lending. You'll need to shop beyond the big-name institutions.

Where to look:

- Credit unions — Many credit unions offer first lien HELOC products with competitive rates and lower fees

- Regional banks — Smaller community banks sometimes offer these products where national banks don't

- Specialty mortgage lenders — Companies like Figure, CMG Financial (which popularized the all-in-one mortgage), and similar fintech lenders

- Mortgage brokers — A broker can shop multiple lenders simultaneously; see our breakdown of mortgage broker vs. direct lender options for investors

Current first lien HELOC rates 2026: Variable rates are currently tracking around 7.41%, tied to the prime rate plus a margin. The exact margin varies by lender and borrower profile.

Pro tip: Always compare the annual percentage rate (APR), not just the headline rate. Some lenders charge annual fees, draw fees, or inactivity fees that can erode the rate advantage.

For a curated list of vetted options, our best HELOC lenders for investment property guide breaks down the top picks for 2026.

Can I Use a First Lien HELOC for Rental Property Investments?

Yes — but with important caveats. A first lien HELOC on a rental property is less common than on a primary residence, and lenders apply stricter standards.

How it works for rental investors:

- You can use a first lien HELOC on your primary residence to fund rental property purchases (the HELOC stays on your home, the rental is purchased separately)

- Some lenders offer first lien HELOCs directly on investment properties, but LTV limits are tighter (often 70–75%) and rates are higher

- The revolving credit line is ideal for funding renovations, down payments on new rentals, or bridging gaps between deals

Real-world use case: An investor owns a primary home worth $600,000 with no mortgage. They open a first lien HELOC for $480,000 (80% LTV). They draw $150,000 to buy a rental property in cash, then repay the HELOC with rental income over 18 months. When the next deal appears, the credit is available again — no new loan application required.

This is the first lien HELOC for investors strategy in action. Let it cook before you see results — the compounding effect of reusing the same credit line across multiple deals is where the real wealth builds.

For more on scaling a rental portfolio, our apartment investing numbers guide is worth your time.

What Are the Typical Closing Costs for a First Lien HELOC?

Closing costs for a first lien HELOC are generally lower than a traditional mortgage, typically ranging from 2% to 5% of the credit limit — though some lenders advertise low or no closing cost options (usually by rolling fees into the rate).

Common fees to expect:

- Appraisal fee: $300–$700 (sometimes waived by lenders)

- Title search and insurance: $500–$1,500

- Origination fee: 0–1% of the credit limit

- Recording fees: $50–$200 depending on the state

- Annual fee: Some lenders charge $50–$100/year to maintain the line

Comparison: A traditional $400,000 mortgage might carry $8,000–$16,000 in closing costs. A first lien HELOC for the same amount might run $4,000–$10,000 — a meaningful difference, especially for investors who prioritize capital efficiency.

Watch out for: Prepayment penalties or early closure fees. Some lenders charge a fee if you close the HELOC within 2–3 years of opening it.

What Mistakes Do Real Estate Investors Make When Choosing a First Lien HELOC?

The most common mistake is treating the first lien HELOC like free money. It's not — it's debt secured by your home, and the variable rate can bite hard if you're not prepared.

Top mistakes to avoid:

- Not stress-testing the variable rate — Run your numbers assuming rates climb 2–3% above current levels. Can you still make the payment?

- Ignoring the repayment phase — When the draw period ends, your payment jumps to include principal. Many investors are caught off guard.

- Overextending the credit line — Drawing the maximum available and leaving no buffer is a recipe for trouble if income dips.

- Not shopping lenders — The first lien HELOC market is thin. Rates and terms vary significantly between lenders. One call to a mortgage broker can save thousands.

- Confusing it with a second mortgage — A HELOC vs second mortgage comparison matters legally and financially. Make sure you understand the lien position before signing.

- Skipping the income sweep strategy — If you're not depositing income into the HELOC account regularly, you're leaving the biggest benefit of the product on the table.

- Using it on a property with declining value — If your home's value drops, your available credit can be frozen or reduced by the lender.

Is a First Lien HELOC a Good Strategy for House Flipping?

For house flipping, the first lien HELOC can be an impeccable funding tool — but it works best when used on your primary residence to fund flip purchases, not as the primary lien on the flip property itself.

Why it works for flippers:

- Speed — You can draw funds within days instead of waiting weeks for a new loan to close

- Reusability — Complete one flip, repay the HELOC, and immediately fund the next deal

- Interest-only payments during the draw period keep holding costs low while the flip is in progress

- No prepayment penalty on most HELOCs — pay it off the moment the flip sells

Where it gets tricky:

- Flips are short-term by nature, so the variable rate risk is manageable

- If a flip takes longer than expected, the interest costs can stack up

- Lenders may scrutinize heavy draws and repayments if they appear speculative

For investors who want to understand the full financial picture before their first flip or rental purchase, our how to analyze a rental property checklist gives you the numbers framework to make confident decisions.

How Quickly Can I Access Funds With a First Lien HELOC?

Once the HELOC is established, you can typically access funds within 1–3 business days via wire transfer, check, or a linked debit card — depending on the lender.

The timeline to get the HELOC set up is the longer part:

- Application to approval: 2–4 weeks on average

- Appraisal and underwriting: 1–3 weeks

- Closing and funding: 3–5 business days after closing

Total time from application to first draw: roughly 3–6 weeks. That's still faster than many conventional mortgage processes, and once the line is open, the speed advantage is significant.

Tip: Open the HELOC before you need it. Many investors establish the credit line when their equity is strong and the market is calm — then have it ready to deploy when a deal shows up. That's the real first lien HELOC strategy: preparation before opportunity.

What Happens If I Can't Make Payments on a First Lien HELOC?

Missing payments on a first lien HELOC carries serious consequences because the lender holds the primary lien on your property.

Here's what happens, step by step:

- 30 days late — Late fee assessed, negative mark on your credit report

- 60–90 days late — Lender may freeze your ability to draw additional funds

- 90+ days late — Account may be sent to collections; lender begins default proceedings

- Foreclosure — Because this is a first lien, the lender has the right to foreclose on your home to recover the debt. This is the same risk as defaulting on a traditional mortgage.

Important distinction: Unlike a second mortgage lender, a first lien HELOC lender doesn't have to wait behind anyone else. They can move to foreclose directly.

If you're struggling:

- Contact your lender immediately — many offer hardship programs or temporary payment modifications

- Consider converting the HELOC balance to a fixed-rate loan if your lender offers that option

- Consult a HUD-approved housing counselor before the situation escalates

The variable rate structure of a first lien HELOC means payment shock is a real risk if rates climb. Always maintain a cash reserve equal to at least 3–6 months of HELOC payments. That's not optional — it's the baseline for responsible use of this product.

FAQ: First Lien HELOC

Q: What is a first lien HELOC in simple terms?

A: It's a home equity line of credit that replaces your mortgage as the primary debt on your property. You borrow against your home's equity, repay it, and borrow again — like a reusable credit line secured by your home.

Q: Is a first lien HELOC the same as an all-in-one mortgage?

A: They're closely related. An all-in-one mortgage is a specific product that combines a first lien HELOC with a checking account, so your income automatically reduces your balance daily. Not all first lien HELOCs have this feature, but the concept is the same.

Q: What are current first lien HELOC rates in 2026?

A: Variable rates are currently tracking around 7.41%, tied to the prime rate plus a lender margin. Your exact rate depends on your credit score, equity, and lender.

Q: Can I get a first lien HELOC on an investment property?

A: Some lenders offer it, but it's less common. Most investors use a first lien HELOC on their primary residence to fund investment property purchases separately.

Q: How is a first lien HELOC different from a second mortgage?

A: A second mortgage sits behind your primary mortgage in lien position. A first lien HELOC replaces the mortgage entirely and holds the primary lien position — meaning the lender is first in line if the property is sold or foreclosed.

Q: What credit score do I need for a first lien HELOC?

A: Most lenders require a minimum of 680, but 720 or higher gets you the best rates and terms.

Q: Are interest-only payments available on a first lien HELOC?

A: Yes. During the draw period (typically 10 years), most lenders allow interest-only HELOC payments. After the draw period, you enter the repayment phase and must pay both principal and interest.

Q: What's the biggest risk of a first lien HELOC?

A: The variable rate. If interest rates rise significantly, your monthly payment increases — and since this is the first lien on your home, defaulting puts your property at risk of foreclosure.

Q: How does a first lien HELOC compare to a HELoan?

A: A HELoan gives you a lump sum at a fixed rate. A HELOC gives you a revolving credit line at a variable rate. Investors who need ongoing, flexible access to capital generally prefer the HELOC. Those who want payment certainty lean toward the HELoan.

Q: Can I use a first lien HELOC to buy a house outright?

A: Not directly — a first lien HELOC is secured by a property you already own. You'd draw from the HELOC on your existing property to purchase a new one in cash or as a down payment.

Q: What happens to my HELOC if my home value drops?

A: The lender can freeze or reduce your available credit line if your home's value declines significantly. This is called a credit line suspension and is within the lender's rights under most HELOC agreements.

Q: Is the interest on a first lien HELOC tax deductible?

A: Interest may be deductible if the funds are used to buy, build, or substantially improve the home securing the loan. If you use the funds for investment purposes, different rules may apply. Consult a tax professional for your specific situation.

Conclusion: Is the First Lien HELOC Right for You?

The first lien HELOC isn't a secret anymore — but it's still being gatekept by lenders who'd rather sell you a 30-year fixed and call it a day. For the right investor, this product is an extraordinary tool that turns idle home equity into a reusable capital engine.

Here's how to think about it:

- ✅ Choose a first lien HELOC if you have strong equity, consistent income, financial discipline, and an active deal pipeline that benefits from fast, reusable capital.

- ❌ Stick with a traditional mortgage if you need payment predictability, are buying your first home with limited equity, or aren't comfortable with variable rate exposure.

The all-in-one HELOC mortgage strategy, the interest-only draw period, and the ability to fund multiple deals from a single credit line make this one of the most impeccable financing tools available to serious investors in 2026. Let it cook before you see results — the compounding effect of sweeping income into a HELOC and redeploying equity across multiple deals takes time to build, but the payoff is real.

Your next steps:

- Pull your home's current value and calculate your available equity

- Check your credit score — aim for 720+ before applying

- Shop at least 3 lenders (credit unions, regional banks, and a mortgage broker)

- Run your numbers with a stress test at rates 2–3% above current levels

- Consult a tax professional about the interest deductibility for your use case

For more on building a real estate investment strategy around flexible financing, explore our real estate financing guide and our breakdown of how the economy shapes real estate prices and demand in 2026.

The information is out here. Use it.

{kind=link}