Last updated: April 23, 2026

Quick Answer: The best HELOC lenders for investment property in 2026 include Kiavi, LendingOne, Lima One Capital, RCN Capital, and New Silver — lenders that specialize in non-owner-occupied financing where traditional banks typically won’t go. Expect rates between 9%–13%, LTVs up to 75%, and qualification requirements focused more on the deal’s numbers than your personal credit score.

Key Takeaways

- 🏠 Investment property HELOCs are harder to get than primary residence HELOCs — most traditional banks won’t offer them, so specialized lenders fill the gap.

- 💰 Rates typically run 2%–4% higher than primary residence HELOC rates, landing between 9%–13% in 2026.

- 📋 Hard money lenders and private lenders are often the most accessible route for investors pulling equity from rental or investment properties.

- 🔑 LTV limits are stricter — most lenders cap at 65%–75% combined loan-to-value (CLTV) on investment properties.

- 📊 Bad credit isn’t always a dealbreaker — some lenders, including Do Hard Money and Groundfloor, work with borrowers down to a 500 credit score or lower.

- 🏙️ State-specific lenders matter — availability and terms vary significantly across TX, FL, GA, IL, NY, NJ, CA, CO, and other states.

- 🔄 Hard money loans and HELOCs serve different purposes — HELOCs are revolving credit lines; hard money loans are short-term bridge financing.

- ⚡ DSCR loans are a strong alternative if you need longer-term financing based on rental income rather than personal income.

What Is a HELOC on an Investment Property — and How Does It Work?

A HELOC (Home Equity Line of Credit) on an investment property lets you borrow against the equity you’ve built in a rental or non-owner-occupied property. Think of it like a credit card secured by your property — you draw what you need, pay interest only on what you use, and replenish the line as you repay.

The catch? Lenders treat investment property HELOCs very differently from primary residence HELOCs. The risk profile is higher in their eyes, so the requirements are tighter and the rates are steeper.

Here’s how the structure typically works:

- Draw period: 5–10 years (you borrow and repay as needed)

- Repayment period: 10–20 years (you pay down the principal)

- Rate type: Usually variable, tied to the prime rate or SOFR

- Max CLTV: 65%–75% on investment properties (vs. 85%–90% on primary residences)

Example: You own a rental property worth $400,000 with a $200,000 mortgage balance. Your equity is $200,000. At a 70% CLTV cap, the lender allows a total of $280,000 in debt — meaning you could access up to $80,000 through a HELOC.

Common mistake: Many investors assume their primary residence HELOC lender will extend the same product on their rental property. Most won’t. You’ll need a lender that specifically underwrites investment property lines of credit — or a hard money lender offering similar equity-based products.

Best HELOC Lenders for Investment Property: Rates, Requirements, and Top Picks in 2026

This is where we stop gatekeeping the real intel. The lenders below are the ones actually doing business with real estate investors in 2026 — not the ones with the flashiest websites who quietly decline investment property applications.

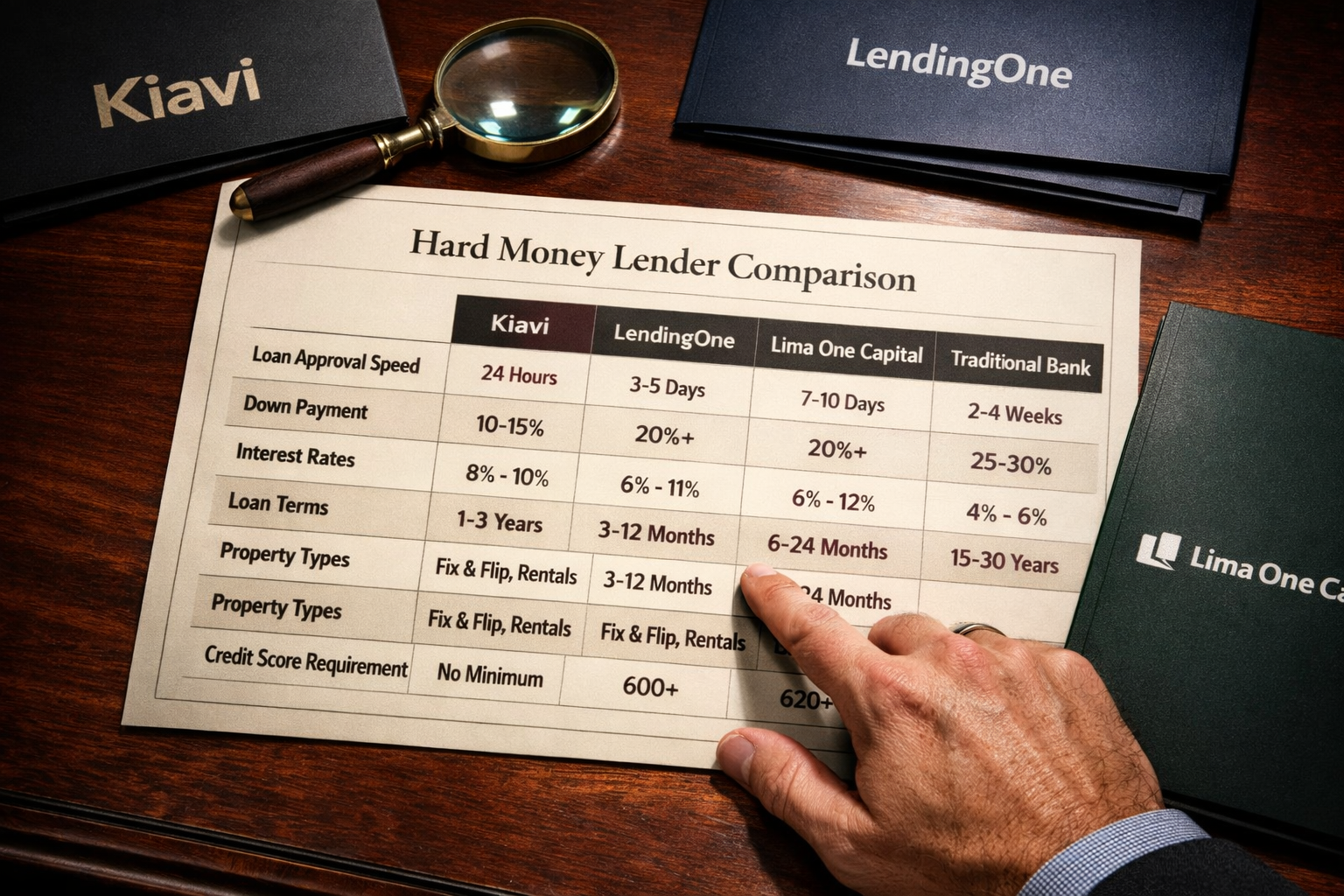

🏆 Top Lenders at a Glance

| Lender | Best For | Min. Credit Score | Max LTV | Rates (Est.) | States |

|---|---|---|---|---|---|

| Kiavi | Fix & flip, BRRRR investors | 640 | 75% | 9.5%–12.5% | 32+ states |

| LendingOne | Rental portfolios, bridge loans | 620 | 75% | 9%–12% | Nationwide |

| Lima One Capital | Fix & flip + construction | 600 | 75% | 9.99%–13% | Nationwide |

| RCN Capital | Multi-family, bridge | 620 | 75% | 9.5%–12% | Nationwide |

| New Silver | Fast closings, tech-forward | 650 | 70% | 10%–13% | 40+ states |

| Do Hard Money | Bad credit investors | 500+ | 70% | 11%–14% | Nationwide |

| Groundfloor | Short-term, crowdfunded | No min. | 70% | 10%–14% | Nationwide |

| CoreVest Finance | Large rental portfolios | 680 | 75% | 8.5%–11% | Nationwide |

| Anchor Loans | Fix & flip, experienced investors | 600 | 75% | 9%–12% | CA, AZ, WA, OR, CO, TX, FL |

| Builders Capital | Ground-up construction | 620 | 75% | 10%–13.5% | Select states |

Kiavi (Formerly LendingHome)

Kiavi is one of the most well-known names in investment property lending, and the Kiavi reviews from active investors are consistently solid. They offer bridge loans, fix and flip loans, and rental property loans — and their tech-driven platform means faster approvals than most traditional lenders. Kiavi operates in 32+ states and is a go-to for investors doing volume.

Best for: BRRRR investors, fix and flip operators, and rental property buyers who want speed and reliability.

LendingOne

LendingOne specializes in non-owner-occupied properties and offers bridge loans, fix and flip financing, and rental property loans. Their hard money bridge loans are particularly popular with investors who need to move fast on acquisitions. They’re one of the few lenders with a dedicated rental portfolio product.

Best for: Investors building a rental portfolio who need flexible, scalable financing.

Lima One Capital

Lima One Capital covers the full spectrum — fix and flip, hard money lender construction loans, rental loans, and multi-family. Their rates sit slightly higher, but they’re willing to work with credit scores as low as 600 and have a strong track record with newer investors.

Best for: Investors who need a one-stop lender for multiple project types.

RCN Capital

RCN Capital is a direct private lender offering hard money fix and flip loans, bridge loans, and long-term rental financing. They’re particularly strong in the multi-family space and work with investors across the country. Solid option for hard money lenders in states like NJ, NY, and CT.

New Silver

New Silver uses AI-driven underwriting to close loans faster than almost anyone else in the space — sometimes in as little as 5 days. Their hard money interest rates run slightly higher, but the speed is worth it for time-sensitive deals.

Do Hard Money

Do Hard Money is one of the few lenders openly marketing to investors with bad credit. If you’re searching for hard money loans for bad credit or a 500 credit score hard money lender, they’re worth a serious look. They focus on the deal, not your credit history.

Groundfloor

Groundfloor operates on a crowdfunding model, connecting real estate investors with individual lenders. No minimum credit score requirement makes them a standout for hard money loans no credit check situations. Rates vary based on deal quality.

CoreVest Finance

CoreVest is built for the serious portfolio investor. Their rental portfolio loans and blanket loan products are extraordinary for investors with 5+ properties who want to consolidate financing. Rates are among the most competitive in the private lending space.

Hard Money Loan Requirements: What Lenders Actually Evaluate

Hard money lenders evaluate deals differently than banks. Your W-2 income and debt-to-income ratio matter far less. What matters most is the asset — the property itself.

Here’s what lenders look at:

- Property value and condition — Is the collateral worth the loan?

- Loan-to-Value (LTV) — How much are you borrowing vs. the property’s current value?

- After-Repair Value (ARV) — For fix and flip loans, what will the property be worth after renovation?

- Exit strategy — How will you repay the loan? (Sale, refinance, rental income?)

- Experience — First-time investors may face higher rates or lower LTV limits.

- Credit score — Less critical than with banks, but most lenders still check it.

- Reserves — Do you have cash to cover carrying costs if the deal takes longer?

So based: The deal is the application. A great property in a strong market can get you funded even if your personal finances aren’t perfect. That’s the whole point of asset-based lending.

LTV vs. ARV Explained: The Numbers That Drive Hard Money Deals

LTV (Loan-to-Value) is the ratio of your loan to the property’s current value. ARV (After-Repair Value) is the projected value after renovations are complete.

Most hard money lenders use both:

- LTV: Typically 65%–75% of the current as-is value

- ARV: Typically 65%–70% of the projected post-renovation value

Example:

- Property purchase price: $150,000

- Estimated repair costs: $50,000

- ARV (projected value after repairs): $280,000

- 70% of ARV = $196,000 (maximum loan amount based on ARV)

- Lender may fund up to $196,000 to cover purchase + repairs

This is why hard money fix and flip loans can cover both acquisition and renovation costs — as long as the ARV math works.

Decision rule: If your ARV-based loan covers your purchase price and rehab budget with room to spare, you’ve got a fundable deal. If the numbers are tight, expect the lender to pull back on the loan amount or require more skin in the game.

Hard Money Interest Rates, Points, and Fees: What to Expect in 2026

Hard money lender rates are higher than conventional loans — full stop. But the tradeoff is speed, flexibility, and access to deals that banks won’t touch.

Typical hard money interest rates in 2026:

- Short-term bridge/fix & flip: 9.5%–13%

- Construction loans: 10%–14%

- Rental/DSCR bridge: 9%–12%

- Bad credit loans: 12%–15%+

Points and fees breakdown:

| Fee Type | Typical Range |

|---|---|

| Origination points | 1–3 points (1 point = 1% of loan) |

| Underwriting fee | $500–$1,500 |

| Appraisal fee | $400–$800 |

| Processing fee | $300–$800 |

| Draw inspection fee (construction) | $150–$300 per draw |

| Prepayment penalty | Varies (some lenders waive it) |

Quick math: On a $200,000 hard money loan at 2 points, you’re paying $4,000 upfront in origination fees plus your interest rate. Factor this into your deal analysis before you commit.

If you want to understand how current rate environments affect your financing costs, our breakdown of current mortgage rates and what buyers need to know gives solid context on where rates are heading.

Hard Money Lenders by State: Where to Find Funding Near You

Finding the right lender often comes down to geography. Some lenders are national; others specialize in specific markets. Here’s a state-by-state breakdown of where the major players operate:

Texas (TX)

Hard money lenders in Dallas, hard money lenders Houston, hard money lenders Austin, and fort worth hard money lenders are all well-served by Kiavi, LendingOne, and RCN Capital. Texas is one of the most active fix and flip markets in the country, and competition among lenders keeps rates relatively competitive.

Florida (FL)

Hard money lenders Tampa and the broader Florida market are covered by Lima One Capital, CoreVest, and Kiavi. Florida’s short-term rental market makes it a hotspot for BRRRR investors. Check out our Airbnb vs. Vacasa property management comparison if you’re considering short-term rental strategy after funding.

Georgia (GA)

Hard money lenders Georgia are well-represented by Lima One Capital (headquartered in Atlanta), RCN Capital, and LendingOne. Atlanta’s investor-friendly market makes Georgia one of the stronger fix and flip states.

Illinois (IL)

Hard money lenders Chicago face a more complex regulatory environment, but national lenders like Kiavi and RCN Capital are active. Chicago’s multi-family market is strong for experienced investors.

New York & New Jersey (NY/NJ)

Hard money lenders NY and hard money lenders NJ operate in one of the tightest lending environments in the country. RCN Capital and LendingOne are both active here. Expect stricter requirements and slightly higher rates due to longer foreclosure timelines.

Other Key Markets

| City/State | Active Lenders |

|---|---|

| Hard money lenders Phoenix | Kiavi, LendingOne, Anchor Loans |

| Hard money lenders Denver | Kiavi, RCN Capital, New Silver |

| Hard money lenders Boston | RCN Capital, LendingOne |

| Hard money lenders San Antonio | Kiavi, LendingOne |

| Hard money lenders NJ | RCN Capital, LendingOne, New Silver |

Hard Money Loans for Bad Credit: Real Options That Actually Work

Bad credit doesn’t automatically disqualify you from investment property financing. This is one of the most gatekept facts in real estate lending — and we’re putting it out there plainly.

Options for investors with credit challenges:

- Do Hard Money — Works with scores as low as 500. Focuses almost entirely on the deal, not the borrower’s credit profile.

- Groundfloor — No stated minimum credit score. Crowdfunded model means individual investors evaluate your deal.

- Lima One Capital — Accepts scores as low as 600 with strong deal fundamentals.

- New Silver — AI-driven underwriting that weighs deal quality heavily alongside credit.

Hard money loans no credit check are rare but exist in the private lending space — typically through individual private investors or small regional lenders who rely entirely on collateral.

Edge case: If you have bad credit but significant equity in an existing property, a cross-collateralization strategy (using one property to secure a loan on another) can sometimes get deals funded that would otherwise be declined.

For investors with credit challenges who want to understand all their financing options, our DSCR loan requirements guide covers another strong alternative that’s less credit-dependent than conventional financing.

Fix and Flip Loans vs. Hard Money Bridge Loans vs. DSCR Loans: Which One Do You Need?

These three products get confused constantly. Here’s the clean breakdown:

Hard Money Fix and Flip Loans

- Purpose: Short-term financing to purchase and renovate a property for resale

- Term: 6–18 months

- Repayment: Interest-only during the loan term, balloon payment at end

- Best for: Flipping houses with hard money — buy, renovate, sell, repeat

Hard Money Bridge Loans

- Purpose: Short-term financing to “bridge” the gap between buying a new property and selling or refinancing an existing one

- Term: 3–24 months

- Best for: Investors who need to move fast on an acquisition before their current property sells

DSCR Loans (Debt Service Coverage Ratio)

- Purpose: Long-term rental property financing based on the property’s income, not your personal income

- Term: 15–30 years

- Best for: Buy-and-hold investors who want permanent financing on rental properties

Choose fix and flip loans if: You’re renovating and selling within 12 months.

Choose bridge loans if: You need temporary financing while transitioning between properties.

Choose DSCR loans if: You’re holding a rental long-term and want to refinance out of hard money.

For a deeper look at how to evaluate different investment property types before choosing your financing, our guide to the 4 essential property types for investments is impeccable reading.

How to Refinance Out of a Hard Money Loan

Hard money loans are designed to be temporary. The goal is always to refinance out into cheaper, longer-term financing once the property is stabilized. Here’s the standard playbook:

Step 1: Stabilize the property

Complete renovations, get the property rented (if it’s a rental), and establish a rental income history (typically 6–12 months for most DSCR lenders).

Step 2: Get an updated appraisal

Your post-renovation value is what lenders use to size the refinance loan. A higher appraised value means more equity and better loan terms.

Step 3: Choose your refinance product

- DSCR loan — Best for rentals; qualifies based on rent income, not your W-2

- Conventional investment loan — Requires stronger personal credit and income documentation

- Portfolio loan — Good for investors with multiple properties

Step 4: Pay off the hard money loan

Use the refinance proceeds to pay off the hard money lender. Your hard money refinance is complete.

Step 5: Let it cook before you see results

Seasoning requirements matter. Most lenders want to see 3–12 months of ownership before they’ll refinance. Plan your timeline accordingly.

Common mistake: Investors rush the refinance before the property is fully stabilized or before they’ve hit the seasoning requirement. This forces them to extend the hard money loan (at significant cost) or sell prematurely.

If you want to understand the broader financing landscape, our real estate investment financing hub covers the full spectrum of options available to investors in 2026.

Hard Money Construction Loans and Land Loans: What Investors Need to Know

Hard money lender construction loans and hard money land loans are specialized products that carry more risk — and therefore more cost — than standard fix and flip financing.

Construction loan structure:

- Funds are released in draws as construction milestones are completed

- Lender sends an inspector to verify progress before each draw

- Rates typically run 1%–2% higher than standard hard money rates

- Terms: 12–24 months

Land loans:

- Hardest category to finance with hard money

- Most lenders cap LTV at 50%–60% on raw land

- Rates can hit 13%–16% depending on the project

- Builders Capital is one of the few national lenders actively doing ground-up construction and land loans for investors

Key requirement: For construction loans, lenders want to see detailed project plans, contractor bids, and a realistic timeline. The more documentation you bring, the better your terms.

How to Become a Hard Money Lender: The Other Side of the Table

Knowing how to become a hard money lender is the logical next step for investors who’ve built capital and want to generate passive returns. Here’s the honest overview:

Option 1: Lend privately to investors you know

The simplest entry point. You fund deals directly, secured by a deed of trust or mortgage on the property. Returns typically run 8%–12%.

Option 2: Invest through a hard money fund

Companies like Groundfloor allow you to invest in individual loans starting at $10. You earn interest without managing the lending process yourself.

Option 3: Start a private lending company

This requires licensing in most states, legal structure (typically an LLC or LP), and significant capital. You’ll also need a loan servicer and legal counsel.

Requirements to be aware of:

- State lending licenses (varies by state — some require a mortgage broker license)

- Securities laws if you’re pooling investor capital

- Proper loan documentation (promissory notes, deeds of trust)

- Title insurance and property insurance requirements

For investors interested in the full spectrum of real estate investment strategies, our beginner’s blueprint for real estate investing is a fresh starting point.

FAQ: Best HELOC Lenders for Investment Property

Q: Can I get a HELOC on an investment property?

Yes, but not through most traditional banks. Specialized lenders — including hard money lenders and private lenders — offer equity-based lines of credit on non-owner-occupied properties. Expect higher rates and stricter LTV limits than a primary residence HELOC.

Q: What credit score do I need for an investment property HELOC?

Most specialized lenders require a minimum of 600–640. Some, like Do Hard Money and Groundfloor, work with scores as low as 500 or have no stated minimum. The deal quality often matters more than the credit score.

Q: What is the maximum LTV for an investment property HELOC?

Most lenders cap combined loan-to-value (CLTV) at 65%–75% on investment properties. This is lower than the 85%–90% CLTV available on primary residences.

Q: What are typical hard money interest rates in 2026?

Hard money lender rates in 2026 range from approximately 9%–14%, depending on the loan type, borrower experience, property condition, and lender. Fix and flip loans typically run 9.5%–12.5%; construction loans and bad credit loans run higher.

Q: What’s the difference between a HELOC and a hard money loan?

A HELOC is a revolving line of credit secured by property equity, typically with a 10–20 year repayment period. A hard money loan is a short-term, interest-only loan (6–24 months) used for acquisitions and renovations. They serve different purposes in an investor’s toolkit.

Q: Are hard money loans available for bad credit?

Yes. Do Hard Money, Groundfloor, and Lima One Capital all work with borrowers who have challenged credit. Asset-based lenders focus primarily on the property’s value and the investor’s exit strategy.

Q: How fast can hard money lenders close?

Most hard money lenders close in 5–15 business days. New Silver and Kiavi are among the fastest, sometimes closing in under a week on straightforward deals.

Q: What states have the most hard money lender options?

Texas, Florida, California, Georgia, and New York have the highest concentration of active hard money lenders. National lenders like Kiavi, LendingOne, and RCN Capital cover most U.S. states.

Q: Can I use a hard money loan for a rental property?

Yes, but it’s typically a bridge strategy. You’d use hard money to acquire and stabilize the property, then refinance into a DSCR loan or conventional investment loan for long-term hold.

Q: What is a DSCR loan and how does it compare to hard money?

A DSCR loan qualifies based on the property’s rental income covering its debt payments (typically a 1.0–1.25 DSCR ratio). It’s a long-term product (15–30 years) vs. hard money’s short-term structure. DSCR loans have lower rates but take longer to close.

Q: What are points on a hard money loan?

One point equals 1% of the loan amount, paid upfront at closing. Most hard money lenders charge 1–3 points as an origination fee. On a $200,000 loan, 2 points = $4,000 in upfront fees.

Q: How do I refinance out of a hard money loan?

Complete your renovation, stabilize the property (get it rented if applicable), wait for any seasoning requirements to pass, then apply for a DSCR loan or conventional investment loan. Use the refinance proceeds to pay off the hard money lender.

Conclusion: Your Next Move as a Savvy Investor

The best HELOC lenders for investment property in 2026 aren’t hiding — they’re just not the ones advertising on every billboard. Kiavi, LendingOne, Lima One Capital, RCN Capital, and Do Hard Money are doing real business with real investors right now, and the terms are more accessible than most people realize.

Here’s your action plan:

- Know your numbers first — Calculate your current LTV and ARV before approaching any lender. Lenders respect investors who walk in prepared.

- Match the lender to the deal — Fix and flip? Go Kiavi or Lima One. Bad credit? Start with Do Hard Money or Groundfloor. Portfolio rental? CoreVest is extraordinary for that.

- Plan your exit before you enter — Know whether you’re selling, refinancing into a DSCR loan, or holding long-term. Your exit strategy affects which hard money product you should use.

- Compare at least 3 lenders — Hard money lender rates and terms vary more than you’d expect. Getting multiple quotes is not optional.

- Factor in all costs — Points, fees, interest, draw inspection costs. Run the full deal analysis before committing.

Real estate investing rewards the prepared. The lenders on this list are fresh options that can move your deals forward — but the due diligence is on you. Let it cook before you see results, and make sure the foundation is solid before you scale.

For more investor resources, explore our investment property news hub and stay current on what’s moving markets in 2026.

References

- Consumer Financial Protection Bureau (CFPB). (2023). Home Equity Lines of Credit (HELOCs). https://www.consumerfinance.gov/

- Federal Reserve. (2024). Survey of Consumer Finances. https://www.federalreserve.gov/

- Kiavi. (2024). Investment Property Loan Products. https://www.kiavi.com/

- LendingOne. (2024). Real Estate Investment Loans. https://www.lendingone.com/

- Lima One Capital. (2024). Fix and Flip and Rental Loan Products. https://www.limaone.com/

- RCN Capital. (2024). Hard Money Lending Programs. https://www.rcncapital.com/

- Groundfloor. (2024). Real Estate Debt Investing Platform. https://www.groundfloor.us/

- CoreVest Finance. (2024). Rental Portfolio Loans. https://www.corevestfinance.com/

- National Association of Realtors. (2024). Investment and Vacation Home Buyers Survey. https://www.nar.realtor/

- Mortgage Bankers Association. (2024). Commercial/Multifamily Lending Data. https://www.mba.org/

Have questions about investment property financing? Reach us at news@realestaterankiq.com or visit realestaterankiq.com for more expert-backed real estate content.

Tags: HELOC investment property, hard money lenders, fix and flip loans, hard money interest rates, Kiavi reviews, LendingOne, Lima One Capital, DSCR loans, investment property financing, hard money loans bad credit, real estate investor loans, bridge loans

{kind=link}