Last updated: May 24, 2026

Quick Answer: The best home buying company will typically pay between 70% and 85% of your home's fair market value — sometimes less. In exchange, you get speed, certainty, and zero repair headaches. That trade-off makes sense for some sellers and is a terrible deal for others. This guide breaks down exactly what these companies pay, what they charge, and the red flags that should send you straight back to the open market.

Key Takeaways

- Home buying companies (iBuyers, "we buy houses" investors, and cash offer platforms) typically pay 70%–85% of market value, depending on the company type and your local market.

- iBuyers like Opendoor and Offerpad charge service fees that can run 5%–8%, which eats further into your net proceeds.

- The speed benefit is real — many sellers close in 7–14 days vs. 30–60+ days on the traditional market.

- Investors who flip homes (the "we buy houses" crowd) often offer the lowest prices but the fewest conditions.

- In 2025, investors purchased roughly 33–34% of all U.S. home sales, signaling just how active the cash buyer market remains heading into 2026.

- Sellers in foreclosure, divorce, or inherited property situations often benefit most from cash offer companies.

- High-equity homeowners in competitive markets should almost always list traditionally — the gap in net proceeds is too large to ignore.

- You can negotiate with home buying companies. Their first offer is rarely their best.

- Legitimacy matters: always verify licensing, check reviews, and get multiple offers before signing anything.

- Walking away from a lowball offer is not just acceptable — sometimes it's the smartest financial move you'll make.

Best Home Buying Company: What They Pay and When to Walk Away — The Full Picture

The best home buying company for your situation depends entirely on what you're optimizing for: speed, certainty, or maximum dollars. These are rarely the same thing.

Home buying companies operate in a few distinct categories, and each one has a different pricing model:

The Three Types of Home Buying Companies

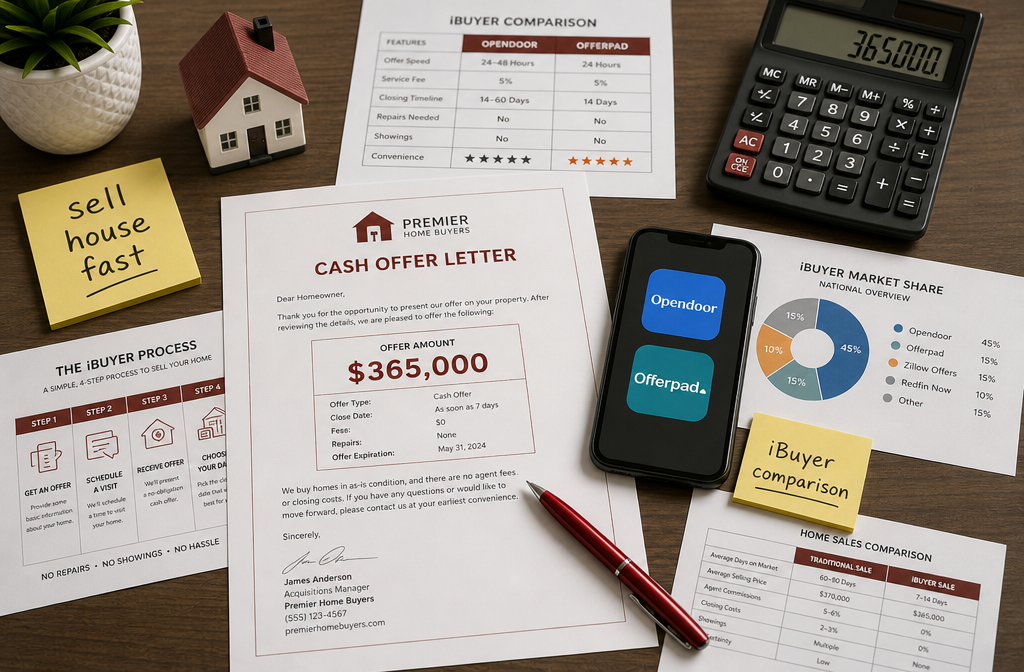

1. iBuyers (Opendoor, Offerpad)

These are tech-powered platforms that make instant cash offers online. They buy homes in decent condition in specific markets, charge a service fee, then resell the property. In the iBuyer comparison for 2026, Opendoor and Offerpad remain the two dominant players after Zillow Offers and Redfin Now exited the market.

- Opendoor operates in 50+ U.S. markets and typically offers 70%–80% of fair market value after fees.

- Offerpad focuses on slightly fewer markets but often includes a free local move as a perk.

- Both charge service fees in the 5%–8% range, on top of the discount already baked into the offer price.

2. "We Buy Houses" Investor Companies

These are local and national cash-for-homes companies — think We Buy Ugly Houses (HomeVestors), MarketPro Homebuyers, and hundreds of regional operators. They buy as-is, close fast, and typically offer the lowest prices of any category. Expect offers in the 60%–75% of ARV (after-repair value) range.

3. Cash Offer Marketplaces

Platforms like HomeLight's Simple Sale or Clever Offers connect sellers with multiple cash buyers simultaneously. These can produce more competitive offers since buyers compete, but the process takes slightly longer than a direct iBuyer offer.

💡 Decision rule: If your home is in great condition and in a hot market, iBuyers will offer more than "we buy houses" investors. If your home needs significant work, go straight to the investor buyer market — iBuyers will either decline or discount heavily for repairs.

For sellers weighing all their options in 2026, our home sellers pricing strategies guide is a solid companion read.

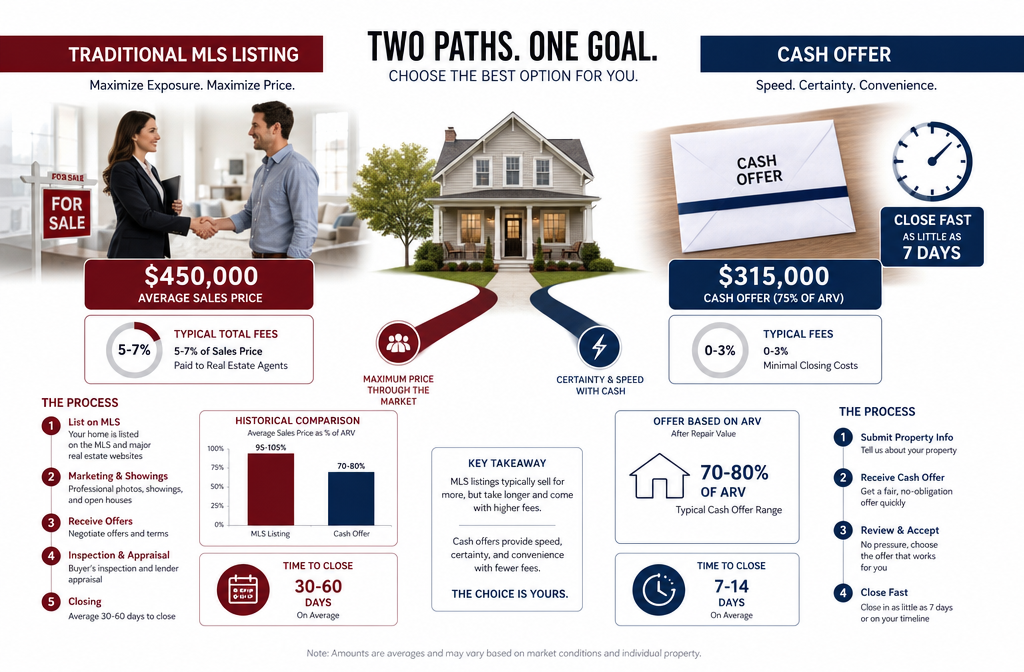

How Much Will a Home Buying Company Pay Compared to Listing Traditionally?

The honest answer: expect to leave money on the table — the question is how much.

On the traditional market, a well-priced home in a competitive area can sell at or above asking price. Cash offer companies don't compete with that. Here's a realistic comparison:

| Sale Method | Typical Net Proceeds (% of Market Value) | Timeline |

|---|---|---|

| Traditional MLS listing | 90%–97% (after agent fees) | 30–90 days |

| iBuyer (Opendoor/Offerpad) | 75%–85% (after service fees) | 7–21 days |

| "We Buy Houses" investor | 60%–75% of ARV | 7–14 days |

| Cash offer marketplace | 78%–88% | 14–30 days |

On a $400,000 home, the difference between a traditional sale and an iBuyer offer could easily be $30,000–$60,000. That's real money. For some sellers, the speed and simplicity are worth it. For others, that gap is a hard no.

Common mistake: Sellers compare the gross offer price from a cash buyer to their asking price — not their actual net after commissions, repairs, and carrying costs on a traditional sale. Run the full math before deciding.

If you're still on the fence about whether to sell or hold, check out our breakdown on whether to sell, stay, or rent it out in 2026.

How Fast Can You Get Cash for Your House?

Speed is where cash offer companies genuinely shine. Most can close in 7–14 days from the time you accept an offer. Some "we buy houses" investors can close in as few as 3–5 days if the title is clean.

Compare that to the traditional route: listing prep, showings, offer negotiations, inspection contingencies, appraisal delays, and lender underwriting can stretch a sale to 60–90 days easily.

The sell home fast 2026 timeline typically looks like this:

- Submit your home details online or by phone (same day)

- Receive a preliminary cash offer (24–48 hours for iBuyers; sometimes same day for investors)

- Home walkthrough or inspection (3–7 days)

- Revised final offer (if applicable)

- Accept offer and choose closing date (often flexible within 7–30 days)

- Close and receive funds

One thing worth knowing: iBuyers like Opendoor often allow you to pick your closing date within a window, which is genuinely useful if you're coordinating a move or a purchase of another home.

What Fees Do Home Buying Companies Charge?

This is where the iBuyer comparison gets interesting — and where sellers often get surprised.

iBuyer fees in 2026:

- Service fee: 5%–8% of the sale price

- Repair credits: iBuyers conduct their own inspection and deduct estimated repair costs from the final offer — this can add another 1%–3% reduction

- Closing costs: typically covered by the seller (1%–3%)

"We buy houses" investor fees:

- Most advertise zero fees or commissions — and that's technically true. But their profit margin is built into the lowball offer price, not a separate line item.

- Closing costs are often covered by the investor, which is a genuine perk.

Cash offer marketplace fees:

- Some platforms charge nothing to the seller (they earn from the buyer side)

- Others charge a small referral or platform fee (1%–2%)

Bottom line: With iBuyers, you're paying a visible service fee plus an invisible discount on your home's value. With investor buyers, you're paying one large invisible discount. Neither is free — the cost is just packaged differently.

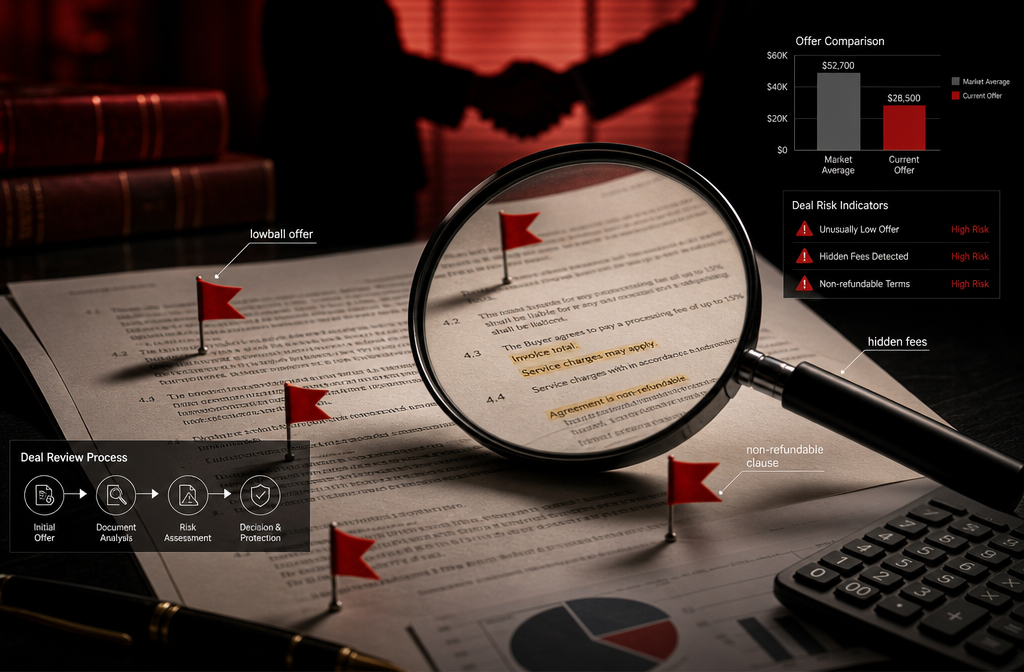

Red Flags to Watch Out for With Home Buying Companies

Not every company calling itself the best as-is home buyer deserves that title. The space has legitimate players and outright predatory ones.

🚩 Red flags that should make you pause:

- Pressure to sign quickly — Any company rushing you to sign before you've had time to think or get a second opinion is a problem. Extraordinary deals don't expire in 24 hours.

- No physical address or verifiable business presence — Legitimate cash for homes companies have a real office, a real team, and a verifiable track record.

- Verbal offers only — Every offer must be in writing. No exceptions.

- Excessive earnest money requests from the seller — That's not how this works. You're the one receiving money.

- Sketchy contract language — Clauses that allow the buyer to reduce the price at closing, assign the contract to a third party without your consent, or extend the closing indefinitely are major red flags.

- No reviews, no references — Check Google, BBB, and Trustpilot. A company with zero reviews or a pattern of complaints about bait-and-switch pricing is one to avoid.

- Lowball offer with no explanation — A legitimate company will show you how they arrived at their number. If they can't explain the math, walk.

The gatekeeping in this industry is real — the best cash for homes companies are transparent about their process. The bad ones are counting on sellers being too stressed or too rushed to ask questions.

Is a Home Buying Company Good for People in Foreclosure?

Yes — and this is one of the clearest use cases for cash offer companies. If you're facing foreclosure, time is the enemy, and a cash buyer can close before the bank takes the property.

How it works in a foreclosure situation:

- A cash buyer can close in 7–14 days, which may be fast enough to stop the foreclosure process

- The sale pays off the mortgage balance, which eliminates the foreclosure from proceeding

- You avoid the long-term credit damage of a completed foreclosure (a short sale or cash sale still hits your credit, but far less severely)

- Any equity above the mortgage payoff goes to you — even if the offer is below market value

Important caveat: If you have significant equity, even a discounted cash offer may net you more than a foreclosure would. Run the numbers with a HUD-approved housing counselor before deciding.

Edge case: If the home is underwater (you owe more than it's worth), a cash buyer won't solve the problem alone — you'd need lender approval for a short sale, which takes longer and involves more parties.

Who Shouldn't Use a Home Buying Company?

Cash offer companies are not the right move for everyone. Here's who should almost certainly skip them:

- Homeowners with significant equity in a competitive market — If your home is move-in ready and in a market with low inventory, a traditional listing will almost always net you more. The gap in proceeds can be $40,000–$100,000+.

- Sellers who have time — If you're not in a rush, there's no reason to accept a discount. Let it cook before you see results — a properly priced and marketed home in a decent market will sell.

- Homes with unique features or luxury finishes — iBuyers use algorithms to price homes. Unique properties (custom architecture, high-end finishes, unusual lot sizes) are often undervalued by automated models.

- Sellers in high-appreciation markets — If your market is trending up, waiting even 30–60 days for a traditional sale could net you more than the "instant" cash offer.

- People who haven't gotten multiple offers — Never accept the first cash offer you receive without at least two or three comparisons.

If your home isn't selling on the traditional market and you're wondering why, our 5 questions to ask your broker when your home won't sell is worth a read before you pivot to a cash buyer.

Common Mistakes People Make When Selling to Cash Home Buyers

The investor cash offers 2026 market is active and competitive — but sellers still make the same avoidable mistakes.

Mistake 1: Accepting the first offer

The first offer from any cash buyer is rarely their best. It's a starting point. Treat it like one.

Mistake 2: Not getting a comparative market analysis (CMA) first

If you don't know what your home is worth, you can't evaluate whether an offer is fair. Get a free CMA from a local agent before you talk to any cash buyer. It costs you nothing and gives you a baseline.

Mistake 3: Ignoring the net proceeds

Sellers fixate on the offer price and forget to subtract fees, repair credits, and closing costs. A $350,000 offer with 7% in fees and $15,000 in repair credits nets you $310,500 — which may be less than a $340,000 traditional sale after a 5% commission.

Mistake 4: Not reading the contract

Cash buyer contracts are not standard real estate purchase agreements. They often contain clauses that favor the buyer heavily. Have a real estate attorney review any contract before you sign.

Mistake 5: Assuming "as-is" means no inspection

Most iBuyers and many investor buyers conduct their own inspection and adjust the offer afterward. "As-is" means you don't have to make repairs — it doesn't mean they won't price them in.

What Happens If the Home Buying Company Lowballs My Offer?

A lowball offer from a cash buyer is so based — it's just business. Don't take it personally, and don't walk away without pushing back first.

What to do when the offer is too low:

- Counter in writing — Come back with a specific number and a brief explanation (comparable sales, recent improvements, your timeline flexibility).

- Request their pricing breakdown — Ask how they calculated the offer. Legitimate companies will show you their ARV estimate, repair deductions, and margin. If they won't, that tells you something.

- Get competing offers — Use the low offer as leverage. If you have a higher offer from another buyer, present it. Cash buyers will often improve their number rather than lose the deal.

- Walk away if the gap is too large — If their best offer is still 20%+ below market value and you have time and equity, the traditional market is your friend.

Can you negotiate with a home buying company? Yes — and this is one of the most gatekept pieces of information in the seller space. iBuyers like Opendoor and Offerpad do have some flexibility, especially on closing timelines, repair credits, and occasionally on price. Investor buyers often have more room to move than they let on.

The key is knowing your number before you sit down at the table. Our home sellers pricing strategies guide will help you get there.

How Do I Know If a Home Buying Company Is Legitimate?

The best home buying company will pass every one of these checks without hesitation. If a company balks at any of them, that's your answer.

Legitimacy checklist:

- ✅ Verifiable business registration — Check your state's Secretary of State website to confirm the company is a registered entity.

- ✅ Physical address — Not just a P.O. box or a virtual office.

- ✅ Proven track record — How many homes have they bought in your area? Ask for references from recent sellers.

- ✅ BBB accreditation or rating — Not perfect, but a pattern of unresolved complaints is a clear warning.

- ✅ Google and Trustpilot reviews — Look for volume and recency. Ten reviews from 2019 don't tell you much about 2026.

- ✅ Written offer, not verbal — Always in writing, always with a clear expiration date.

- ✅ No upfront fees — Legitimate cash buyers never charge sellers upfront fees to receive an offer.

- ✅ Proof of funds — Ask to see a bank statement or letter confirming they have the cash to close. Any serious buyer will provide this.

For national iBuyers like Opendoor and Offerpad, legitimacy isn't the concern — their business models and track records are well-documented. The risk is higher with smaller, local "we buy houses" operators, especially those who cold-call or send unsolicited mailers.

What Repairs Do Home Buying Companies Typically Require?

The short answer: most cash buyers won't require you to make any repairs before closing. That's part of the appeal.

But here's what actually happens:

- iBuyers (Opendoor, Offerpad) conduct a home assessment after you accept a preliminary offer. They identify needed repairs and either deduct the estimated cost from your final offer or ask you to make specific repairs before closing. Common deductions include HVAC issues, roof damage, foundation concerns, and outdated electrical panels.

- "We buy houses" investors typically buy completely as-is — no repairs, no cleaning, sometimes not even emptying the house. Their low offer price already accounts for the work they'll need to do.

- Cash offer marketplaces vary by the individual buyer matched to your property.

Fresh take: The "no repairs needed" pitch is real, but it's not free. Every dollar of deferred maintenance gets priced into the offer — usually at a higher cost than if you'd fixed it yourself. A $500 plumbing repair that you handle before listing might only reduce a traditional buyer's offer by $500. An iBuyer might deduct $2,000 for the same issue.

If you're thinking about which improvements actually move the needle on value, our best home renovations for ROI guide breaks it down clearly.

How to Find the Best Home Buying Companies in Your Area

Finding the best home buying company locally requires more than a Google search. Here's an impeccable process for vetting your options:

Step 1: Start with national iBuyers

Check if Opendoor or Offerpad operate in your market. Both have online tools that give you a preliminary offer in minutes. Use these as your baseline — they're the most transparent about their pricing model.

Step 2: Search for local investor buyers

Search "[your city] we buy houses" or "[your city] cash home buyers." You'll find a mix of legitimate operators and opportunists. Apply the legitimacy checklist above to each one.

Step 3: Use a cash offer marketplace

Platforms like HomeLight's Simple Sale or Clever Offers submit your property to multiple cash buyers simultaneously. This is one of the fastest ways to generate competing offers without doing the legwork yourself.

Step 4: Get a CMA from a local agent

Before you accept anything, know your market value. A local agent will give you a free CMA and can often tell you which cash buyers in your area are reputable.

Step 5: Compare net proceeds, not offer prices

Build a simple spreadsheet. For each offer, subtract fees, repair credits, and estimated closing costs. Compare that number to your projected net from a traditional sale (price minus 5–6% commission, minus any prep costs, minus carrying costs for 45–60 days).

For a broader look at the best platforms to explore when buying or selling, our best home buying sites in the U.S. for 2026 is a solid resource.

FAQ: Best Home Buying Company Questions Answered

Q: What is the best home buying company overall in 2026?

A: For most sellers, Opendoor offers the most transparent process and the widest market coverage among iBuyers. For sellers who need the absolute fastest close and don't mind a lower offer, a local "we buy houses" investor may be faster. The best home buying company is the one that fits your specific timeline and financial situation.

Q: Do cash home buying companies negotiate?

A: Yes. Most cash buyers — including iBuyers — have some flexibility on price, closing timeline, and repair credits. Always counter before accepting or walking away.

Q: How much below market value do cash buyers offer?

A: Typically 15%–30% below market value, depending on the company type, your market, and your home's condition. iBuyers tend to offer closer to market value (minus fees), while traditional investor buyers offer the steepest discounts.

Q: Are there any home buying companies that pay full market value?

A: Rarely. Some cash offer marketplaces in highly competitive markets can get close to 90%–95% of market value, but that's the exception. If full market value is your goal, a traditional listing is almost always the better path.

Q: How long does it take to close with a cash home buying company?

A: Most cash buyers can close in 7–21 days. Some investor buyers close in as few as 3–5 days if the title is clean and both parties are motivated.

Q: Is Opendoor or Offerpad better in 2026?

A: Both are legitimate, but Opendoor has broader market coverage and a longer operating history. Offerpad sometimes offers perks like free local moves. Get offers from both if they operate in your market and compare the net proceeds.

Q: What happens if I change my mind after accepting a cash offer?

A: Read your contract carefully. Most cash buyer agreements have a cancellation window, but penalties or forfeited deposits may apply depending on how far into the process you are.

Q: Can I sell to a cash buyer if I have a mortgage?

A: Yes. The mortgage is paid off at closing from the sale proceeds, just like any other home sale.

Q: Are "we buy houses" companies a scam?

A: Not inherently — many are legitimate businesses. But the space has bad actors. Use the legitimacy checklist in this article and never sign anything without a review period.

Q: What is the investor share of home purchases in 2025?

A: Investors accounted for approximately 33–34% of all U.S. home purchases in 2025, reflecting continued strong demand from the cash buyer market heading into 2026.

Q: Should I use a real estate agent even if I'm selling to a cash buyer?

A: Having an agent review your offer costs nothing if they're representing you in a future purchase. Many sellers benefit from having an experienced eye on the contract terms, even in a cash sale.

Q: Can a cash offer fall through?

A: With true cash buyers (no financing contingency), it's rare — but it happens. Verify proof of funds before accepting any offer.

Conclusion: Know Your Number, Know Your Options

The best home buying company is not a universal answer — it's a contextual one. If you're in foreclosure, dealing with an inherited property, relocating on a tight timeline, or selling a home that needs serious work, a cash offer company can be an extraordinary solution. The speed and certainty are real, and sometimes that's worth more than the extra dollars a traditional sale might bring.

But if you have equity, time, and a home in decent condition, walking away from a lowball cash offer and listing traditionally is almost always the stronger financial play. The difference in net proceeds on a $400,000 home can easily exceed $50,000 — and that's not a gap to dismiss.

Your action steps:

- Get a CMA first — Know your home's market value before talking to any cash buyer.

- Request offers from at least 3 companies — Include at least one iBuyer (Opendoor or Offerpad if available in your market) and one local investor buyer.

- Run the net proceeds math — Compare every offer on what you actually walk away with, not the headline number.

- Verify legitimacy — Apply the checklist. No shortcuts.

- Negotiate — Always counter. The first offer is a starting point.

- Know when to walk — If the gap between a cash offer and a traditional sale is more than you're willing to trade for speed, list the home.

For more guidance on navigating the 2026 market as a seller, explore our spring home selling mistakes guide and our full home buyers and sellers market update.

The cash buyer market isn't going anywhere — investor share at 33–34% of purchases proves that. But so does the traditional market. Know your options, run your numbers, and make the move that actually serves your financial future.

{kind=link}