Let’s be real—navigating the 2026 housing market feels like trying to solve a Rubik’s cube blindfolded while riding a rollercoaster. Mortgage rates are doing their own thing, loan limits just got a fresh upgrade, and everyone’s asking the same question: “Should I buy now or wait?” If you’ve been gatekeeping your homeownership dreams because the market seemed too wild, it’s time to let it cook and dive into what’s actually happening with U.S home buyers and sellers financing & mortgages tips and market update right now.

As of early March 2026, the average 30-year fixed mortgage rate hovers around 6.0%—a number that might make you nostalgic for the ultra-low rates of 2020-2021, but is actually extraordinary compared to the 7%+ chaos we saw in 2022-2023.[1][3][6] Meanwhile, conforming loan limits jumped to $832,750 nationwide, and FHA ceilings climbed even higher, giving buyers more breathing room.[7][10] Whether you’re a first-timer stretching your budget or a seasoned investor eyeing your next flip, understanding these shifts is impeccable for making smart moves this spring.

This guide—written by licensed brokers with over 15 years of experience at Real Estate Rank IQ—breaks down everything you need to know about financing, mortgages, and the current market landscape. No fluff, just actionable intel to help you close deals, save thousands, and navigate 2026 like a pro.

Key Takeaways

- Mortgage rates are near three-year lows: 30-year fixed rates average around 6.0% in early March 2026, down from 7%+ peaks, making now a relatively favorable time to lock in financing.[1][3][6]

- Conforming loan limits increased significantly: The 2026 limit rose to $832,750 (up from $806,500), with high-cost ceilings at $1,249,125, expanding conventional loan access for buyers in pricier markets.[7][10]

- FHA limits also climbed: FHA loan floors start at $541,287, with high-cost ceilings matching conforming at $1,249,125, plus higher limits for multi-unit properties—ideal for house hackers and small investors.[4]

- Refinance activity is surging: Lower rates have triggered a noticeable uptick in purchase and refinance applications, signaling pent-up demand from buyers who paused during the rate spike.[9]

- Don’t wait for sub-4% rates: Experts agree that hoping for a return to ultra-low rates could mean missing out on inventory and appreciation; focus on payment affordability and refinance later if rates drop further.[1][2][9]

Understanding the 2026 Mortgage Rate Landscape: What U.S Home Buyers and Sellers Need to Know

Current Rates Are So Based—Here’s Why

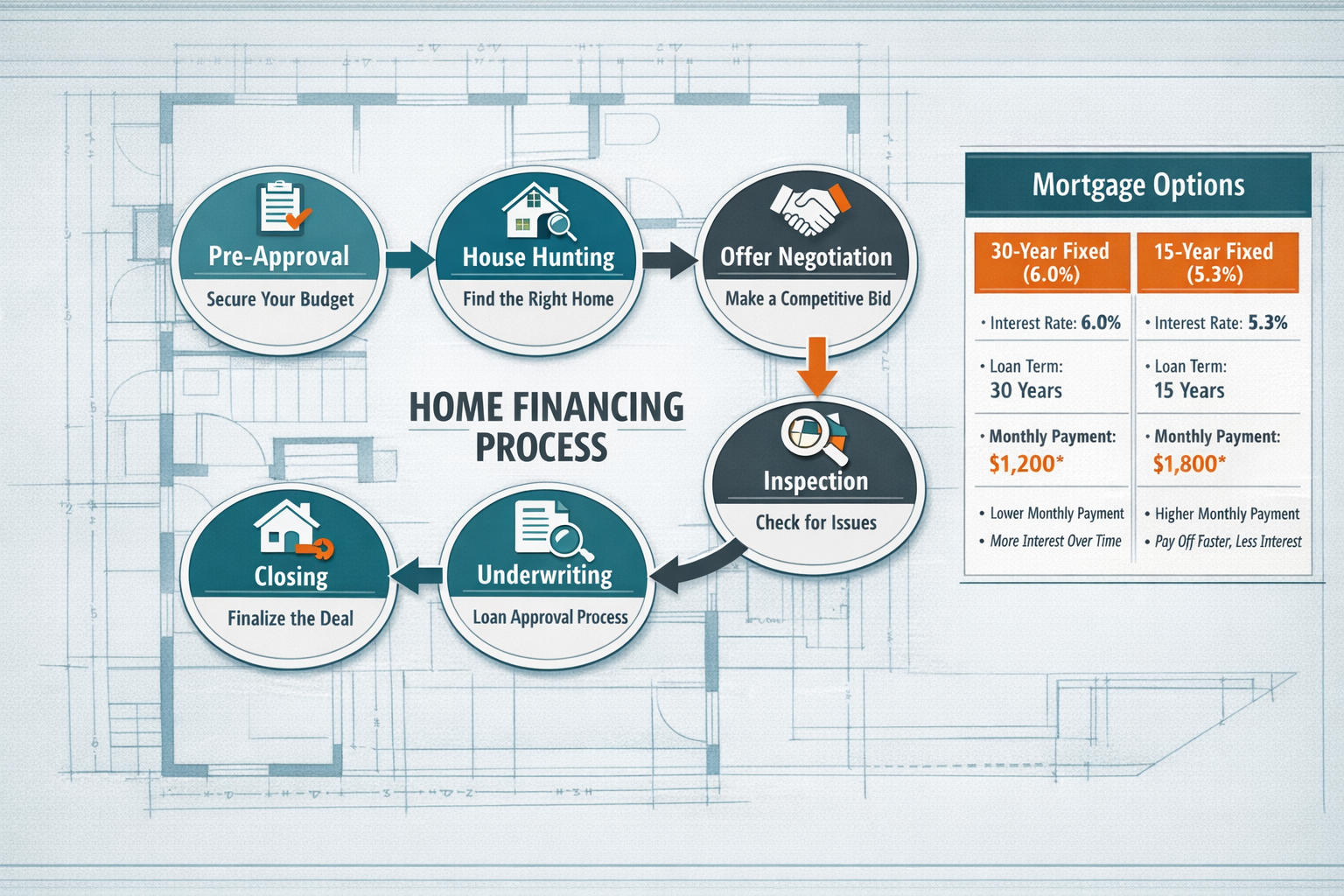

As of March 5, 2026, Fortune reported the average 30-year fixed conforming mortgage rate at 6.02%, while 15-year rates sit around 5.3-5.4%.[1][3] CBS and Zillow data from early March show similar figures—5.87% to 5.98%—confirming that rates have stabilized near a three-year low.[6] Bankrate’s analysis notes that 30-year rates averaged about 6.18% over the first two months of 2026 and have been trending down since late 2025, prompting a pickup in both purchase and refinance applications.[9]

Yes, these numbers are roughly double the pandemic-era lows of 2020-2021, but context matters. During 2022-2023, rates spiked above 7%, freezing many buyers and sellers in place. The current ~6% environment is what analysts describe as “good” or even “excellent” relative to that volatility.[1][2][3] Freddie Mac economists expect a “solid spring sales season” if rates remain near current levels, and NerdWallet’s March 2026 outlook predicts rates will drift modestly lower through spring rather than plunge.[9]

Bottom line: If you can afford the monthly payment at 6%, don’t delay solely hoping for a much lower rate. You can always refinance later if rates drop, but you can’t recapture lost time, appreciation, or inventory.

How the Federal Government’s MBS Purchases Are Lowering Rates

One reason rates have eased is the Federal Reserve’s ongoing management of its mortgage-backed securities (MBS) portfolio. In 2026, the government’s strategic $200 billion MBS purchase program has helped stabilize and lower mortgage rates by increasing demand for these securities, which directly influences the interest rates lenders offer to consumers.Learn more about how the Federal government’s $200B MBS purchase is lowering mortgage rates.

This intervention has been a game-changer for buyers and sellers alike, creating a more predictable rate environment and encouraging transaction activity after years of uncertainty.

What Rising Loan Limits Mean for Your Buying Power

The Federal Housing Finance Agency (FHFA) raised the 2026 conforming loan limit for one-unit properties to $832,750 nationwide, up from $806,500 in 2025—a roughly 3.26% increase reflecting average home price growth.[7][10] High-cost areas (like parts of California, New York, and Hawaii) can now access conforming loans up to $1,249,125 (150% of the baseline).[7][10] Only 32 counties saw no increase, meaning most buyers have slightly more room to borrow with conventional conforming loans before hitting jumbo territory.[7][10]

Why does this matter? Conforming loans typically offer better rates and terms than jumbo loans because they can be sold to Fannie Mae or Freddie Mac, reducing lender risk. If you were just over the 2025 limit and facing jumbo pricing, you might now qualify for a conforming loan with lower rates and smaller down payment requirements.

HUD also increased 2026 FHA forward mortgage loan limits, with the floor for single-unit homes at $541,287 and the high-cost ceiling at $1,249,125.[4] For multi-unit properties (ideal for house hacking), FHA limits now reach up to $2.40 million for four-unit properties in high-cost areas.[4] FHA also raised the HECM (reverse mortgage) maximum claim amount to $1,249,125, expanding access for senior homeowners looking to tap home equity.[4]

Pro tip: If you’re buying in a high-cost market, check your county’s specific loan limit on the FHFA or HUD website. You might be surprised at how much more you can borrow with favorable terms in 2026.

Smart Financing Strategies for U.S Home Buyers and Sellers in 2026

Choosing the Right Loan Type: Conventional vs. FHA vs. Adjustable

Conventional conforming loans are the gold standard for buyers with solid credit (typically 620+) and at least 3-5% down. With the new $832,750 limit, more buyers in mid-to-high-cost areas can access these loans without jumping to jumbo.[7][10] Conventional loans require private mortgage insurance (PMI) if you put down less than 20%, but PMI can be canceled once you hit 20% equity—unlike FHA’s mortgage insurance premium (MIP), which often lasts the life of the loan.

FHA loans remain a lifeline for first-time buyers and those with lower credit scores or smaller down payments (as low as 3.5% with a 580+ score). However, FHA loans come with both an upfront premium of 1.75% of the base loan amount and annual MIP between about 0.15% and 0.75%.[4] Most 30-year borrowers pay around 0.55% annually after the 2023 reduction, but higher-balance FHA loans (above roughly $500k in many areas) pay higher annual MIP—often 0.70-0.75%—increasing costs for buyers in expensive markets.[4]

Adjustable-rate mortgages (ARMs) are making a comeback in 2026. A 5/1 or 7/1 ARM typically offers a lower initial rate than a 30-year fixed, which can be attractive if you plan to sell or refinance within a few years. Just be sure you understand the rate caps and worst-case scenarios before committing.

For sellers: Understanding buyer financing options helps you evaluate offers more intelligently. An FHA or VA offer isn’t automatically weaker than conventional—especially if the buyer is well-qualified and the appraisal is solid. In fact, knowing how to negotiate seller concessions can help you close deals faster while keeping more cash in your pocket.

Pre-Approval Is Non-Negotiable: Fast-Track Your Path to Homeownership

In a market where inventory remains tight and competition can flare up quickly, a pre-approval letter is your golden ticket. Unlike pre-qualification (which is just a rough estimate), pre-approval means a lender has reviewed your credit, income, assets, and debts and committed to lending you a specific amount—subject to appraisal and final underwriting.

Getting pre-approved accomplishes three things:

- Clarifies your budget: You’ll know exactly how much house you can afford, preventing heartbreak from falling in love with a property out of reach.

- Strengthens your offer: Sellers and listing agents take pre-approved buyers seriously, especially in multiple-offer situations.

- Speeds up closing: Much of the underwriting legwork is already done, so you can close faster—a huge advantage in competitive markets.

Fast-track your path to homeownership with pre-approval and market trends by gathering your documents early: two years of tax returns, recent pay stubs, bank statements, and a list of debts. If you’re self-employed or have non-traditional income, work with a lender experienced in alternative documentation.

Down Payment Strategies: How Much Do You Really Need?

The old “20% down or bust” rule is a myth. In 2026, many buyers are putting down far less:

- Conventional loans: 3-5% down for qualified buyers (though PMI applies under 20%).

- FHA loans: 3.5% down with a 580+ credit score; 10% down for scores between 500-579.[4]

- VA loans: 0% down for eligible veterans and service members (no PMI, but a one-time funding fee applies).

- USDA loans: 0% down for rural and suburban properties in eligible areas.

That said, larger down payments offer advantages: lower monthly payments, better interest rates, stronger offers, and immediate equity. According to the National Association of Realtors’ 2025 Profile of Home Buyers and Sellers, the typical seller owned their home for a record 11 years and accumulated roughly $140,900 in wealth over the past five years alone.[5] This equity growth fuels repeat buyers’ ability to deploy big down payments or purchase all-cash, changing competitive dynamics for financed buyers.[5][8]

First-time buyers: Don’t let the equity gap discourage you. Explore down payment assistance programs (many states and cities offer grants or low-interest loans), and consider asking sellers to contribute toward closing costs. Learn how to get a home seller to pay closing costs upfront to reduce your out-of-pocket expenses.

Closing Costs and Compliance: What’s New in 2026

Compliance updates for 2026 adjusted multiple federal mortgage thresholds under Regulation Z (Truth in Lending), including HOEPA triggers, APR-to-APOR spreads, and points-and-fees caps for Qualified Mortgages, as well as the “higher-priced mortgage” appraisal threshold (increasing the dollar threshold for smaller-loan appraisal exemptions). Lenders must update disclosure and pricing systems accordingly, which can affect closing costs and how borderline loans are underwritten.

What this means for you: Closing costs—typically 2-5% of the loan amount—cover lender fees, title insurance, appraisal, escrow setup, and more. In 2026, some of these fees may shift slightly due to regulatory changes, so it’s crucial to review your Loan Estimate carefully and compare offers from multiple lenders.

Calculate closing costs in minutes using AI and real estate tech to budget accurately and avoid surprises at the closing table. Sellers, you’re not off the hook either—understand what you’ll pay and how to cut costs before listing.

Market Dynamics and Timing: Should You Buy Now or Wait?

The “Buy Now or Wait” Debate: Expert Insights

Bankrate’s March 2026 analysis frames the central question on every buyer’s mind: “Should I buy now or wait?”[9] With rates trending down but still well above pandemic lows, and home prices remaining firm, the answer depends on your personal situation—but the consensus among experts is clear: if you can afford the payment now, don’t wait.

Here’s why:

- Rates may not drop much further: NerdWallet’s March 2026 outlook expects rates to drift modestly lower through spring, not plunge back to sub-4% territory.[9] Waiting for a dramatic rate drop could mean missing out on inventory and appreciation.

- You can refinance later: If rates do fall significantly, you can refinance to a lower rate. But you can’t recapture lost equity or the opportunity to build wealth through homeownership.

- Inventory is improving but still tight: Spring 2026 housing market trends show lower rates and rising inventory signaling buyer opportunities, but competition remains in desirable neighborhoods.

- Prices are holding steady or rising: With limited supply and steady demand, home prices in most markets are not falling. Waiting could mean paying more later.

For sellers: The current rate environment is bringing buyers back to the table after a slow 2023-2024 period. If you’ve been holding off on listing, spring 2026 is shaping up to be an impeccable window. Check out these 9 signs your local housing market is heating up to time your listing for maximum impact.

Regional Market Variations: Where the Action Is

Not all markets are created equal in 2026. Luxury housing strength in 2026 shows top-tier markets outpacing mid-range amid rate volatility, while emerging Sun Belt markets are experiencing a data center boom driving real estate demand.

Key trends by region:

- High-cost coastal markets (California, New York, Boston): Benefiting most from increased conforming and FHA loan limits; buyer activity picking up as rates stabilize.

- Sun Belt cities (Phoenix, Austin, Nashville, Tampa): Strong job growth and migration continue to drive demand; inventory improving but still competitive.

- Midwest and Rust Belt (Cleveland, Detroit, Pittsburgh): Affordability remains a strength; first-time buyers finding opportunities with FHA and conventional low-down-payment loans.

- Rural and suburban areas: USDA loans and remote work flexibility making these markets attractive for buyers priced out of urban cores.

Understanding your local market is crucial. Analyze real estate markets by location with AI tools to get hyper-local insights on inventory, pricing trends, and days on market.

The Equity Advantage: How Long-Term Homeowners Are Winning

NAR’s 2025 Profile highlights a “tale of two markets”: older, equity-rich repeat buyers making large down payments or paying cash, while many younger or first-time buyers are constrained by high prices and debt.[5][8] The typical seller owned their home for a record 11 years, accumulating significant equity—roughly $140,900 in wealth over the past five years alone.[5]

This equity growth is extraordinary and fuels repeat buyers’ ability to dominate competitive markets. For first-timers, this means you’re often competing against buyers with deep pockets and no financing contingencies.

How to compete:

- Get pre-approved and include the letter with every offer.

- Offer earnest money that shows you’re serious (typically 1-3% of the purchase price).

- Be flexible on contingencies: If inspection and appraisal come back clean, consider waiving minor contingencies (but never waive inspection entirely).

- Write a personal letter: In some markets, a heartfelt letter to the seller can tip the scales in your favor.

- Work with an experienced agent: A skilled buyer’s agent knows how to structure competitive offers and negotiate effectively. Master negotiation power moves to save thousands on your next home.

Actionable Tips for Buyers and Sellers in 2026

For Buyers: Your Step-by-Step Game Plan

- Check your credit and clean it up: Aim for 620+ for conventional, 580+ for FHA. Dispute errors and pay down high-balance credit cards.

- Get pre-approved (not just pre-qualified): Shop at least three lenders to compare rates and fees.

- Determine your budget: Use the 28/36 rule (housing costs ≤28% of gross income; total debt ≤36%) as a guideline, but also consider your comfort level.

- Explore loan options: Compare conventional, FHA, VA, and USDA loans to find the best fit for your situation.

- Factor in all costs: Down payment, closing costs (2-5%), moving expenses, immediate repairs, and ongoing maintenance.

- Start house hunting strategically: Use the best home buying sites in the U.S. for 2026 to search efficiently, and work with a buyer’s agent who knows your target neighborhoods.

- Make strong, clean offers: Include pre-approval, earnest money, and realistic timelines. Avoid lowball offers in competitive markets.

- Don’t skip inspection: Even in a hot market, a professional inspection can save you from costly surprises. Negotiate repairs or credits based on findings.

- Lock your rate at the right time: Rates can fluctuate daily. Work with your lender to lock when rates dip, and consider a float-down option if rates continue to fall.

- Close with confidence: Review your Closing Disclosure carefully, bring certified funds, and celebrate your new home!

For Sellers: Maximize Your Sale in a Shifting Market

- Understand current market conditions: Review 2026 real estate trends to see how stable 6% rates are reshaping buyer and seller strategies.

- Price it right from day one: Overpricing triggers price cuts and lowball offers. Avoid these 7 pricing mistakes to attract serious buyers quickly.

- Prep your home like a pro: Follow the complete home sale checklist with AI tips and market insights to maximize appeal and ROI.

- Invest in high-ROI upgrades: Focus on curb appeal, fresh paint, and minor kitchen/bath updates. See these 7 high-ROI home renovation ideas before touching a wall.

- Market aggressively: Professional photos, virtual tours, and social media promotion are non-negotiable. Transform your marketing with virtual tours and aerial photos to stand out.

- Be strategic with concessions: Offering to pay closing costs or buy down the buyer’s rate can attract more offers. Master these 10 spring negotiation tactics for seller concessions to close deals faster.

- Vet offers carefully: Don’t just look at price—consider financing type, contingencies, earnest money, and closing timeline. A slightly lower all-cash offer might be safer than a higher financed offer with shaky pre-approval.

- Stay flexible and responsive: Answer questions quickly, accommodate showings, and be willing to negotiate in good faith.

Conclusion

The U.S home buyers and sellers financing & mortgages tips and market update for 2026 reveals a market in transition—one where rates have stabilized near three-year lows, loan limits have expanded to support more buyers, and inventory is gradually improving. Whether you’re a first-time buyer stretching to afford your dream home, a seasoned investor eyeing your next rental property, or a seller looking to capitalize on renewed buyer activity, the opportunities are fresh and the timing is impeccable.

Key action steps:

- Buyers: Get pre-approved, explore all loan options (conventional, FHA, VA, USDA), and don’t wait for rates to drop dramatically—focus on payment affordability and refinance later if needed.

- Sellers: Price competitively, prep your home strategically, and leverage seller concessions to attract serious offers in a market where buyers are coming back to the table.

- Everyone: Stay informed on local market trends, work with experienced professionals, and use technology (AI tools, virtual tours, online calculators) to make smarter, faster decisions.

The 2026 housing market isn’t perfect, but it’s far more favorable than the chaos of 2022-2023. Rates are so based right now compared to the 7%+ peaks, and with the right strategy, you can navigate financing and mortgages like a pro. Don’t let gatekeeping myths or fear hold you back—let it cook, do your homework, and make your move.

Real Estate Rank IQ is here to guide you every step of the way with expert-backed, actionable content from licensed brokers with over 15 years of experience. For more insights, visit realestaterankiq.com, subscribe to our YouTube channel @Realestaterankiq, or reach out at news@realestaterankiq.com.

References

[1] Current Mortgage Rates 03 05 2026 – https://fortune.com/article/current-mortgage-rates-03-05-2026/

[2] Mortgage Rates February 25 2026 – https://www.bankrate.com/mortgages/analysis/mortgage-rates-february-25-2026/

[3] Current Mortgage Rates 03 04 2026 – https://fortune.com/article/current-mortgage-rates-03-04-2026/

[4] Hud Announces 2026 Fha Amp Hecm Loan Limit Increases To Reflect Market Conditions – https://www.mortgageprocessor.org/mortgage-processor-news/2025/12/16/hud-announces-2026-fha-amp-hecm-loan-limit-increases-to-reflect-market-conditions

[5] Key Takeaways From Nars 2025 Profile Of Home Buyers And Sellers – https://virginiarealtors.org/2025/12/08/key-takeaways-from-nars-2025-profile-of-home-buyers-and-sellers/

[6] Todays Mortgage Interest Rates March 3 2026 – https://www.cbsnews.com/news/todays-mortgage-interest-rates-march-3-2026/

[7] Fhfa Announces Conforming Loan Limit Values For 2026 – https://www.mortgage-underwriters.org/mortgage-underwriting-news/2025/11/25/fhfa-announces-conforming-loan-limit-values-for-2026

[8] A Tale Of Two Markets What Nars 2025 Buyer Seller Profile Means For You – https://pfar.org/a-tale-of-two-markets-what-nars-2025-buyer-seller-profile-means-for-you/

[9] Mortgage Rates For Friday March 6 2026 – https://www.bankrate.com/mortgages/todays-rates/mortgage-rates-for-friday-march-6-2026/

[10] Fhfa Announces Conforming Loan Limit Values For 2026 – https://www.fhfa.gov/news/news-release/fhfa-announces-conforming-loan-limit-values-for-2026

{kind=link}