Buying your first home in 2026 feels like trying to solve a Rubik’s cube blindfolded—except the stakes are way higher and the cube costs several hundred thousand dollars. But here’s the extraordinary news: the market conditions are finally shifting in favor of first-time buyers after years of gatekeeping by institutional investors and sky-high rates. With mortgage rates dipping below 6% for the first time in years and new federal policies aimed at leveling the playing field, 2026 might just be your year to stop scrolling through Zillow at 2 AM and actually get those keys in hand.

The journey to homeownership doesn’t have to feel like navigating a maze designed by someone who clearly doesn’t want you to succeed. Armed with the right First-Time Home Buyers Tips and a clear understanding of today’s market dynamics, that dream of owning your own place becomes less fantasy and more achievable reality. Whether you’re tired of your landlord’s “we’ll fix it eventually” approach to maintenance or you’re ready to paint your walls literally any color besides beige, this comprehensive guide will walk you through everything you need to know.

Key Takeaways

- Mortgage rates have dropped below 6% for the first time in years (around 6.06% as of late February 2026), creating fresh opportunities for buyers who’ve been waiting on the sidelines

- Federal policies are shifting the landscape with executive orders restricting institutional investors from using government-backed financing, promoting sales to individual owner-occupants

- Builder incentives are extraordinary with 40% cutting prices by ~5% and two-thirds offering mortgage rate buydowns, making new construction particularly appealing

- Down payment assistance programs are expanding with states like California offering up to $150,000 through lottery-based programs for first-generation buyers

- Strategic timing matters as experts recommend starting your search now in early 2026 to beat rising spring competition before the market heats up

Essential First-Time Home Buyers Tips: Financial Preparation That Actually Works

Let’s talk money—because nothing kills a home buying dream faster than discovering your finances aren’t quite ready for prime time. The foundation of successful homeownership starts long before you ever step foot in an open house.

Get Your Credit Score in Impeccable Shape

Your credit score isn’t just a number—it’s literally the difference between getting approved for a mortgage at a competitive rate or getting laughed out of the lender’s office (okay, they’re too professional to laugh, but you get the point). Aim for a score of 740 or higher to qualify for the best rates available in 2026’s market.

Here’s what actually moves the needle:

- Pay down existing debt strategically, focusing on credit cards with high utilization rates first

- Never close old credit cards even if you don’t use them—that available credit helps your utilization ratio

- Set up automatic payments for everything to avoid those soul-crushing late payment dings

- Dispute any errors on your credit report immediately (you’d be surprised how common these are)

According to mortgage experts, even a 20-point difference in your credit score can impact your rate by 0.25-0.5%, which translates to thousands of dollars over the life of your loan [4].

Budget Beyond the Down Payment

Here’s where most first-time buyers mess up: they save religiously for that down payment, hit their target, and think they’re ready to roll. Wrong. Charles Goodwin of Kiavi emphasizes the importance of maintaining liquidity beyond just your down payment for unexpected costs like appraisal gaps and moving expenses [4].

Your complete financial checklist should include:

| Expense Category | Typical Cost | When You’ll Need It |

|---|---|---|

| Down Payment | 3-20% of purchase price | At closing |

| Closing Costs | 2-5% of purchase price | At closing |

| Home Inspection | $300-500 | During due diligence |

| Appraisal | $300-600 | During loan process |

| Moving Costs | $1,000-5,000 | Move-in day |

| Emergency Fund | 3-6 months expenses | Always |

| Immediate Repairs | $2,000-10,000 | First few months |

The math might seem daunting, but remember: with rates hovering around 6% and builder incentives at historic levels, the monthly payment picture looks significantly better than it did just a year ago [1].

Explore Down Payment Assistance Programs (They’re Not Just for Low-Income Buyers)

Plot twist: you might not need to save that entire down payment yourself. Down payment assistance (DPA) programs are experiencing a renaissance in 2026, with both federal and state governments recognizing that the first-time buyer share has hit a historic low of just 21%—down a staggering 50% since 2007 [1].

California’s Dream For All Shared Appreciation Loan program reopened registration from February 24 to March 16, 2026, offering up to $150,000 (or 20% of the purchase price) in down payment assistance for first-generation, first-time buyers through a lottery system [5]. That’s not a typo—$150,000 in assistance.

But California isn’t the only game in town. Here’s what’s fresh in 2026:

- FHA loans still require just 3.5% down with credit scores as low as 580

- VA loans offer 0% down for eligible veterans and service members

- USDA loans provide 0% down options for properties in eligible rural areas

- State-specific programs vary wildly but can include grants, forgivable loans, and tax credits

- Relocation incentives in communities across Kansas, Oklahoma, and other states offering $5,000-$6,000 cash for remote workers willing to relocate [2]

The key is to stack these programs where possible. Combine a state DPA program with a federal loan program, add in a relocation incentive if you’re flexible on location, and suddenly that down payment barrier doesn’t look quite so insurmountable.

For those exploring mortgage options specifically designed for younger buyers, understanding the full spectrum of available programs can make all the difference.

Avoid These Financial Landmines Before Closing

You’ve found your dream home, your offer was accepted, and you’re counting down the days until closing. This is not the time to finance that new car you’ve been eyeing or switch jobs for a better opportunity. Seriously.

On March 11, 2026, experts specifically advised first-time buyers to avoid new debt, large purchases, or job changes before the Fed meeting, as these moves can torpedo your mortgage approval even days before closing [7].

The “don’t you dare” list includes:

- Opening new credit cards (even if the store offers you 20% off)

- Making large purchases on credit

- Changing jobs or employment status

- Moving money between accounts without documentation

- Co-signing loans for friends or family

- Letting any bills go to collections

Lenders verify your financial situation right up until closing day. One wrong move and you could watch your dream home slip away faster than you can say “underwriting denial.”

Strategic First-Time Home Buyers Tips: Navigating Today’s Market Like a Pro

Financial preparation is crucial, but understanding how to actually navigate the 2026 market separates the dreamers from the homeowners. Let’s get tactical.

Timing Is Everything: Why Starting Your Search Now Is So Based

Here’s the thing about real estate markets—they move in predictable patterns, and right now, we’re in a sweet spot that won’t last forever. Real estate expert DiBugnara advises starting home searches now in early 2026 to beat rising competition, capitalize on low rates, and lock in prices before the spring market heats up [4].

The Spring 2026 housing market outlook shows lower rates and rising inventory creating genuine buyer opportunities—but these windows close fast.

Why early 2026 is your moment:

- Inventory typically increases in spring, giving you more options

- Sellers who list in winter/early spring are often more motivated

- Competition is lower before the traditional spring buying frenzy

- Rate locks can protect you if rates tick up during your search

- You have time to be selective rather than rushed

The data backs this up: builders are ramping up townhome construction to 18% of single-family starts (up from less than 10% a decade ago) specifically to create affordable entry points with buydowns for the first few years [1]. Translation? There’s actually inventory designed for first-time buyers, but it won’t last if you let it cook too long.

New Construction vs. Existing Homes: The 2026 Calculus

In previous years, new construction was often priced out of reach for first-time buyers. But 2026 has flipped the script in extraordinary ways. With 40% of builders cutting prices by approximately 5% and two-thirds providing mortgage rate buydowns, new construction deserves serious consideration [1].

New Construction Advantages in 2026:

✅ Aggressive incentives including rate buydowns (sometimes as low as 4% for the first few years)

✅ No immediate repairs needed—everything is brand new with warranties

✅ Energy efficiency means lower utility bills from day one

✅ Customization options to make the space truly yours

✅ Modern layouts designed for how people actually live today

Existing Home Advantages:

✅ Established neighborhoods with mature landscaping and character

✅ Known quantities regarding neighborhood dynamics and schools

✅ Potential for equity if you’re buying in an appreciating area

✅ Negotiation leverage especially on homes that have been on the market longer

✅ Location flexibility with more inventory in desirable established areas

Robert Dietz, NAHB Chief Economist, specifically highlights that builders are focusing on townhomes as affordable entry points—perfect for first-time buyers who want the benefits of ownership without the overwhelming maintenance of a large single-family home [1].

For those considering new construction, understanding the builder incentives and rate cuts driving the 2026 market can help you negotiate even better deals.

First-Time Home Buyers Tips for Gen Z

The Institutional Investor Factor: How Policy Changes Help You

Here’s some genuinely exciting news: the playing field is being leveled. On January 20, 2026, President Trump issued an executive order directing federal agencies like HUD, VA, USDA, and FHFA to issue guidance within 60 days to restrict large institutional investors from using government-backed financing for single-family home purchases [3][9].

What this means for you:

The executive order promotes sales to individual owner-occupants, including first-time buyers, by limiting the ability of deep-pocketed institutional investors to compete with you using government-backed loans. For years, these investors have been gatekeeping affordable inventory, but that advantage is being systematically dismantled [6].

This policy shift is already creating ripple effects:

- Less competition from all-cash institutional offers on entry-level homes

- More inventory staying available for individual buyers

- Better negotiating position without competing against investment firms

- Stabilized prices in markets previously dominated by investor purchases

While the full impact will take time to materialize, early 2026 represents a transitional period where these policies are being implemented—giving savvy first-time buyers a window of opportunity before everyone else catches on.

Location Strategy: Thinking Beyond the Obvious

Everyone wants to live in the hot neighborhood with the trendy coffee shops and impeccable walkability scores. But here’s a fresh take: some of the best value for first-time buyers exists in emerging areas that are just starting their upward trajectory.

Strategic location considerations for 2026:

🏘️ Emerging neighborhoods near established areas often offer 20-30% lower prices with similar appreciation potential

🏘️ Suburban townhome communities provide lower entry points with community amenities

🏘️ Secondary markets in the Midwest and South where buying is cheaper than renting in 57.7% of counties [10]

🏘️ Remote work flexibility opens up possibilities in lower-cost areas with relocation incentives [2]

🏘️ Transit-oriented development areas where infrastructure improvements are planned

Consider this: in Peoria County, Illinois, buying costs just 14.5% of wages versus 22.4% for renting a 3-bedroom home [10]. That’s a massive difference that frees up cash flow for building wealth.

Understanding how location multiplies home value through amenity proximity can help you identify neighborhoods poised for growth.

To Rent or Buy? The 2026 Math

Let’s address the elephant in the room: should you even buy, or is renting the smarter financial move? The answer depends entirely on your situation, timeline, and location.

When renting makes more sense:

- You plan to move within 3-5 years

- Your job situation is uncertain

- You’re in a high-cost coastal market where the rent-to-buy ratio is extreme

- You value flexibility and minimal responsibility over equity building

- You can invest the difference between rent and ownership costs effectively

When buying makes more sense:

- You plan to stay put for at least 5-7 years

- You’re in one of the 57.7% of U.S. counties where buying is cheaper long-term than renting [10]

- You want to build equity rather than pay someone else’s mortgage

- You value stability and the ability to customize your living space

- You’re ready for the responsibilities of homeownership

The data shows that in the Midwest and South particularly, buying beats renting for 3-bedroom homes when you factor in a 20% down payment and current rates around 6% [10]. But in Western U.S. counties, rent often takes a smaller share of wages, making the calculation more complex.

Check out our detailed analysis of spring home buying tips for the 2026 market to understand the timing and market dynamics specific to your situation.

Advanced First-Time Home Buyers Tips: Working with Professionals and Closing the Deal

You’ve got your finances dialed in and you understand the market dynamics. Now it’s time to assemble your team and actually get to the finish line.

Choosing the Right Real Estate Agent (It Matters More Than You Think)

Not all agents are created equal, and the wrong choice can cost you literally tens of thousands of dollars. You need someone who specializes in working with first-time buyers and actually understands the programs and strategies available in 2026.

What to look for in a buyer’s agent:

🔍 First-time buyer experience with verifiable references from recent clients

🔍 Knowledge of DPA programs and ability to connect you with lenders who specialize in them

🔍 Strong negotiation skills backed by data and market knowledge

🔍 Availability and communication style that matches your needs

🔍 Local market expertise with specific neighborhood knowledge

🔍 Professional network including inspectors, lenders, and contractors

Interview at least three agents before making your choice. Ask about their recent first-time buyer transactions, how they handle multiple offer situations, and what their communication cadence looks like. The right agent will educate you throughout the process rather than just pushing you to make offers.

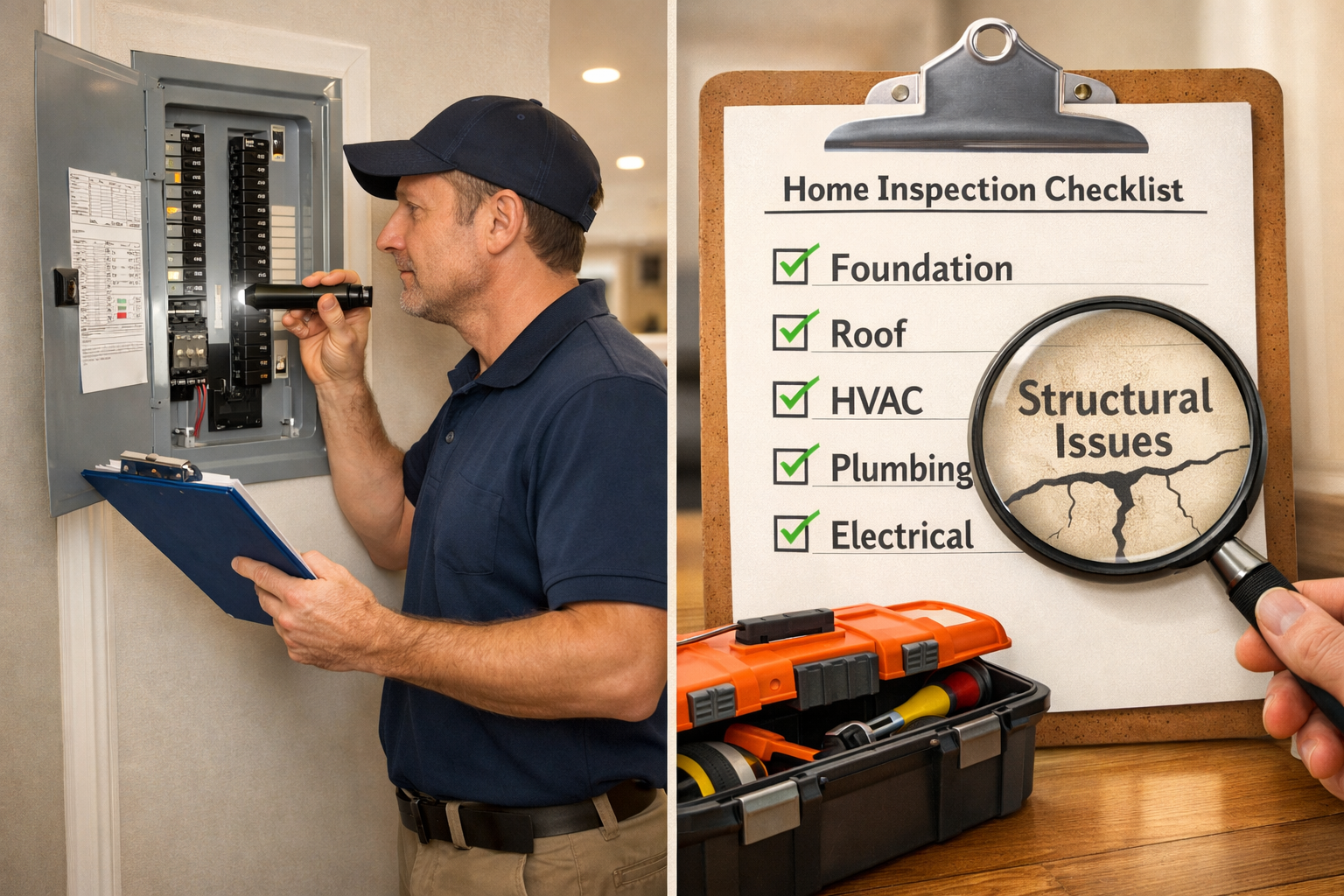

The Inspection Contingency: Your Safety Net

Never, ever, ever waive the inspection contingency unless you have extensive construction knowledge and are prepared to handle literally anything that comes up. This is your opportunity to discover if that charming 1920s bungalow has a foundation that’s slowly returning to the earth.

What a thorough inspection should cover:

- Structural integrity (foundation, framing, roof)

- Electrical systems and safety

- Plumbing and water heater condition

- HVAC system functionality and age

- Pest issues and wood rot

- Drainage and grading around the property

- Insulation and ventilation in attic/crawl spaces

Budget $300-500 for a standard inspection, and consider specialized inspections for issues like mold, radon, or septic systems if relevant. The few hundred dollars you spend here can save you from buying a money pit that drains your finances for years.

If the inspection reveals issues, you have leverage to negotiate repairs, credits, or even walk away if the problems are too extensive. This is not the time to let emotions override logic—if the bones of the house aren’t solid, move on to the next opportunity.

Making Competitive Offers Without Overextending

In competitive markets, the temptation to throw caution to the wind and offer way over asking price is real. But remember: you still have to live within your means after you get the keys.

Smart offer strategies for 2026:

💰 Get pre-approved (not just pre-qualified) to show sellers you’re a serious buyer

💰 Include an escalation clause that automatically increases your offer up to a maximum if competing offers come in

💰 Write a personal letter to the sellers explaining why you love their home (this actually works)

💰 Be flexible on closing dates to accommodate seller needs

💰 Consider asking for seller concessions toward closing costs rather than a lower price

💰 Understand appraisal gaps and have a plan for covering them if necessary

With current market conditions showing rising inventory and more balanced negotiations, buyers have more leverage than they’ve had in years. Don’t feel pressured to make decisions that don’t align with your financial boundaries.

For strategies on negotiating closing costs, including getting sellers to contribute, explore our comprehensive guide.

Understanding Closing Costs and Final Walkthroughs

You’re almost there—the finish line is in sight. But closing day involves a mountain of paperwork and final expenses that can catch first-time buyers off guard.

Typical closing costs include:

- Loan origination fees (0.5-1% of loan amount)

- Title insurance and title search

- Attorney fees (in states that require them)

- Property taxes (prorated)

- Homeowners insurance (first year premium)

- HOA fees (if applicable)

- Recording fees and transfer taxes

- Survey and appraisal fees

Expect closing costs to total 2-5% of the purchase price. Some of these can be negotiated with the seller or rolled into your loan, but you’ll need cash for others.

Final walkthrough checklist:

✅ All agreed-upon repairs have been completed

✅ Appliances and fixtures that were supposed to stay are still there

✅ No new damage has occurred since your last visit

✅ Utilities are functional (turn on faucets, test outlets)

✅ Garage door openers and keys are available

✅ The home is in “broom clean” condition

This is your last chance to ensure everything is as it should be before you sign on the dotted line. Don’t rush through it—take your time and document any issues immediately.

Post-Purchase: Setting Yourself Up for Long-Term Success

Congratulations—you did it! You’re officially a homeowner. But the journey doesn’t end at closing. Setting yourself up for long-term success means being proactive about maintenance and financial management.

First 90 days priorities:

🏠 Create a home maintenance fund separate from your emergency fund (aim for 1-2% of home value annually)

🏠 Document everything with photos and keep all receipts and warranties organized

🏠 Schedule regular maintenance for HVAC, gutters, and other systems

🏠 Meet your neighbors and learn about neighborhood dynamics

🏠 Review your homeowners insurance annually to ensure adequate coverage

🏠 Start planning for future improvements but don’t rush into major renovations

For guidance on home improvements that actually boost value, check out our ranked list of ROI projects—even though you just bought, thinking ahead prevents costly mistakes.

Remember that homeownership is a long-term wealth-building strategy. In markets where buying is cheaper than renting (which covers more than half of U.S. counties), you’re building equity with every payment while your renting friends are building their landlord’s equity [10].

Conclusion

Navigating the path to homeownership as a first-time buyer in 2026 requires equal parts financial preparation, market knowledge, and strategic thinking. But here’s the extraordinary truth: conditions are more favorable now than they’ve been in years. With mortgage rates below 6%, aggressive builder incentives, expanding down payment assistance programs, and federal policies leveling the playing field against institutional investors, your window of opportunity is wide open.

The First-Time Home Buyers Tips for Gen Z outlined in this guide provide a comprehensive roadmap from financial preparation through closing day and beyond. Focus on getting your credit score above 740, exploring the full range of DPA programs available, understanding the strategic advantages of timing your purchase in early 2026, and assembling a team of professionals who specialize in first-time buyer transactions.

Your action plan starting today:

- Check your credit score and create a plan to address any issues

- Calculate your complete budget including down payment, closing costs, and reserves

- Research DPA programs in your target area and determine eligibility

- Get pre-approved with a lender who understands first-time buyer programs

- Interview real estate agents who specialize in working with first-time buyers

- Start your home search now to beat the spring competition surge

The dream of homeownership isn’t just for people with trust funds or those who bought a decade ago when prices were lower. With the right preparation and strategy, 2026 can be the year you stop scrolling through listings and start building equity in your own home.

For more expert-backed guidance on navigating today’s real estate market, explore our comprehensive real estate education hub featuring market analysis, buying strategies, and financial education fundamentals.

References

[1] Could More First Time Buyers Make The Math Work In 2026 – https://www.nar.realtor/magazine/real-estate-news/could-more-first-time-buyers-make-the-math-work-in-2026

[2] Whats New In First Time Home Buyer Programs For 2025 – https://www.makemymove.com/articles/whats-new-in-first-time-home-buyer-programs-for-2025

[3] White House Focuses On Affordability Homeownership – https://www.nar.realtor/magazine/real-estate-news/white-house-focuses-on-affordability-homeownership

[4] Home Buyer Preparation 2026 – https://themortgagereports.com/125202/home-buyer-preparation-2026

[5] 2026 Homebuyer Assistance Programs – https://www.realtor.com/news/trends/2026-homebuyer-assistance-programs/

[6] Investor Housing Ban – https://winningwithwade.com/investor-housing-ban/

[7] Things Homebuyers Should Avoid Before The Fed March 2026 Meeting – https://www.cbsnews.com/news/things-homebuyers-should-avoid-before-the-fed-march-2026-meeting/

[9] Stopping Wall Street From Competing With Main Street Homebuyers – https://www.whitehouse.gov/presidential-actions/2026/01/stopping-wall-street-from-competing-with-main-street-homebuyers/

[10] Buying A Home This Spring 2026 – https://mortgagecenter.com/buying-a-home-this-spring-2026/

SEO Meta Title: First-Time Home Buyers Tips 2026: Expert Guide to Success

{kind=link}