Last updated: May 24, 2026

Quick Answer: Physician mortgage lenders offer specialized home loan programs that allow medical doctors, residents, and dentists to buy property with little to no down payment, no private mortgage insurance (PMI), and flexible debt-to-income calculations — even while carrying six-figure student loan debt. These programs exist because lenders view physicians as extraordinarily low credit risks, given their income trajectory and career stability.

Key Takeaways

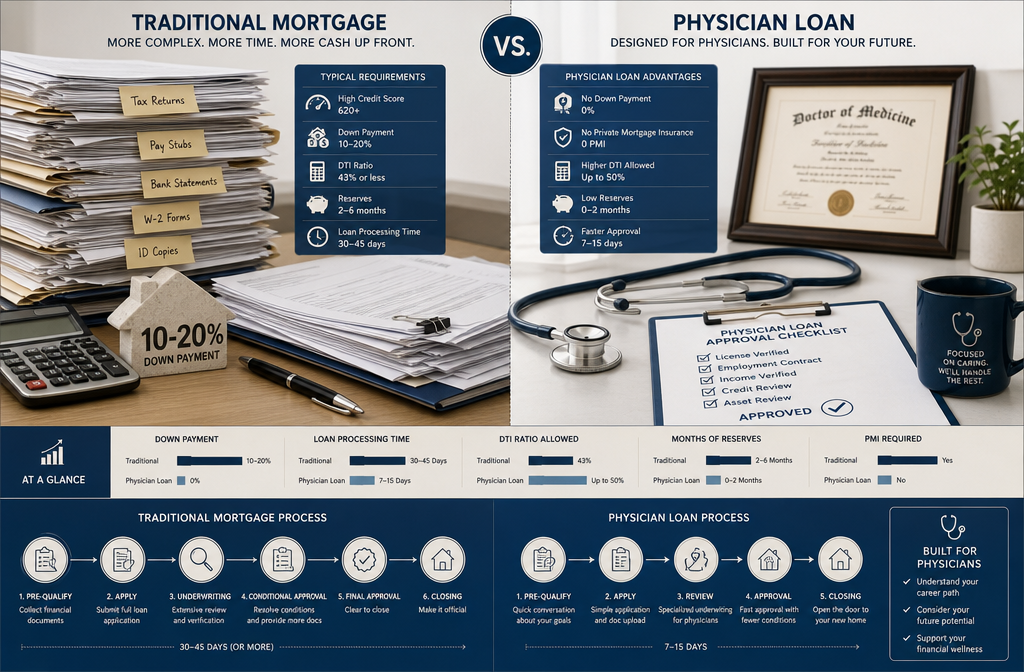

- No down payment required — most physician mortgage programs offer 0% to 5% down on loans up to $1 million or more

- No PMI — unlike conventional loans, physician home loans skip private mortgage insurance entirely, saving hundreds per month

- Student debt treated differently — lenders often exclude deferred medical school loans from your debt-to-income (DTI) ratio

- Residents qualify too — an employment contract is often enough to get approved, even before your first paycheck

- Credit score threshold — most physician mortgage lenders want a 700+ score, though some programs accept 680

- Not available in all states — program availability varies by lender and location; some top programs are region-specific

- Rates are competitive but not always the lowest — physician loan rates typically run slightly higher than conventional rates, but the no-PMI savings often offset the difference

- Board certification is NOT always required — most lenders qualify based on your MD, DO, DDS, DMD, or PharmD degree and employment status

- The loan is for primary residences only — most physician mortgage programs do not apply to investment properties or vacation homes

What Exactly Is a Physician Mortgage Loan and How Is It Different?

A physician mortgage loan is a specialized home financing product designed exclusively for licensed medical professionals. Unlike conventional mortgages, these loans are underwritten with the understanding that doctors have high earning potential but often start their careers with massive student debt and minimal savings — making them look terrible on paper but extraordinary in practice.

Here's what makes physician home loans genuinely different from standard mortgage products:

| Feature | Conventional Loan | Physician Mortgage |

|---|---|---|

| Down Payment | 3–20% | 0–5% |

| PMI Required | Yes (if <20% down) | No |

| Student Loan Treatment | Counted in full DTI | Often excluded or income-based |

| Employment Start Date | Must be employed now | Future contract accepted |

| Max Loan Amount | Conforming limits (~$766K) | Often $1M–$2M+ |

| Eligible Borrowers | General public | MD, DO, DDS, DMD, PharmD, and more |

The biggest structural difference is how these lenders treat student loan debt. A doctor finishing residency might owe $250,000 or more in medical school loans. On a conventional mortgage, that debt gets counted against you hard. Physician mortgage lenders either exclude deferred loans entirely or use a small income-based repayment figure — which can be the difference between qualifying for a $600,000 home and getting rejected outright.

This is the kind of intel that gets gatekept inside medical school financial aid offices. We're putting it out in the open.

Physician Mortgage Lenders: How Doctors Buy Property Early (The Full Picture)

Physician mortgage lenders make it possible for doctors to buy property years earlier than they could through conventional channels. The core logic is simple: a first-year attending physician earning $250,000+ annually is a near-zero default risk, even if they have $300,000 in student loans and $8,000 in savings.

The process works like this:

- You finish medical school or residency and receive an employment contract

- You apply with a physician mortgage lender — no need to wait for your first paycheck

- The lender evaluates your future income, not just your current bank balance

- Student loans in deferment are excluded or minimized in the DTI calculation

- You close with 0–5% down, no PMI, and move in before your first attending salary hits

This is why physician home loan lenders have become so popular with residents, fellows, and new attendings. The traditional mortgage system was built for W-2 employees with 20% saved up and no debt. That describes almost no doctor under 40.

For context on how this compares to other non-traditional financing options, check out our breakdown of mortgage broker vs. direct lender options for investors — because the channel you use to apply matters just as much as the loan type.

How Much House Can a Medical Resident or New Doctor Qualify For?

Medical residents can typically qualify for homes priced between $400,000 and $750,000, depending on their contract salary, credit score, and the specific physician mortgage lender. New attendings with confirmed employment contracts often qualify for $1 million or more.

The math behind qualification:

- Residency salary typically ranges from $55,000 to $80,000 annually (varies by specialty and program)

- Most physician mortgage lenders will use your signed employment contract as proof of future income, even if you haven't started yet

- DTI limits are generally more flexible — some lenders allow up to 45–50% DTI for physician borrowers

- Your loan amount ceiling is often $1 million to $1.5 million at 0% down, with higher amounts at 5–10% down

Choose this program if: You're a resident or fellow with a signed attending contract and want to buy before your income jumps. The lender will underwrite based on your future salary, not your current residency pay.

Common mistake: Applying based on residency income alone without submitting your employment contract. Always include the contract — it's the single document that unlocks the best terms.

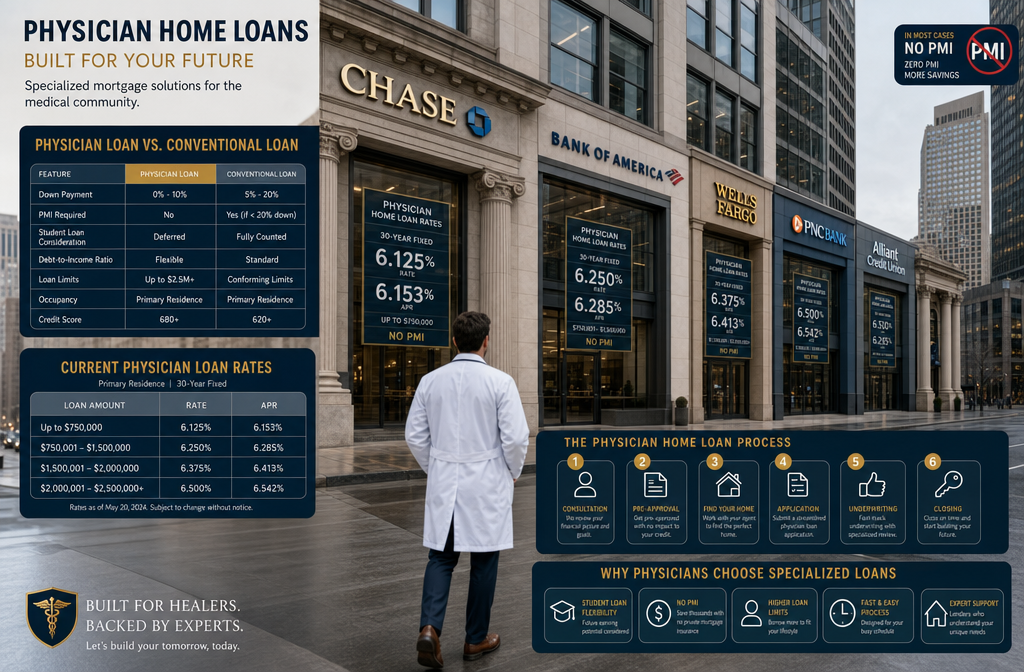

Which Banks Offer the Best Physician Mortgage Programs Right Now?

Several major banks and specialty lenders offer impeccable physician mortgage programs in 2026. The most consistently cited names include Truist Bank, Fifth Third Bank, Flagstar Bank, TD Bank, Huntington National Bank, and SunTrust (now merged with Truist). Specialty lenders like Laurel Road (a division of KeyBank) and First National Bank of Omaha also run well-regarded programs.

Here's what to look for when comparing best physician lenders 2026:

- Loan limits — does the program go up to $1M, $1.5M, or $2M+?

- Down payment tiers — 0%, 5%, or 10% options at different loan amounts

- Eligible specialties — some lenders include pharmacists, veterinarians, and nurse practitioners; others are MD/DO only

- Rate structure — fixed vs. adjustable, and how the rate compares to current conventional rates

- State availability — not every program is offered in every state

💡 Pro tip: Don't just call one bank. Physician mortgage lenders compete for this business. Get quotes from at least three lenders and compare the APR, not just the interest rate. The no-PMI benefit alone can save $200–$500 per month compared to a conventional loan with the same down payment.

For a broader look at current rate environments, our current mortgage rates guide for 2026 gives solid context on where rates are sitting right now.

Do You Need to Be Board Certified to Get a Physician Mortgage?

No — board certification is not required by most physician mortgage lenders. Qualification is typically based on your professional degree (MD, DO, DDS, DMD, PharmD, DPM) and your employment status or signed contract, not your board exam results.

Eligible degrees vary by lender but commonly include:

- MD (Medical Doctor)

- DO (Doctor of Osteopathic Medicine)

- DDS / DMD (Dental professionals — dental professional loans are widely available)

- PharmD (Pharmacist)

- DPM (Podiatrist)

- DVM / VMD (Veterinarian — fewer lenders, but programs exist)

- NP / PA — some lenders include nurse practitioners and physician assistants under expanded professional mortgage programs

The key qualifier is your degree and employment status. A resident who just matched into a program qualifies. A fellow with a signed attending contract qualifies. You don't need to be board-certified, fully licensed in your state, or even actively seeing patients yet.

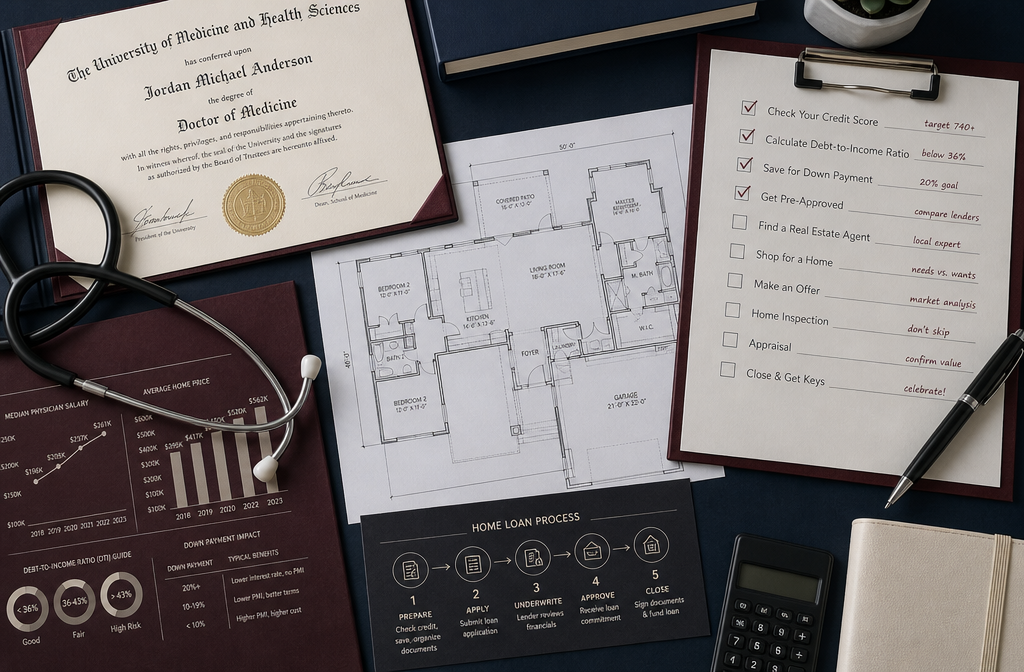

What Credit Score Do You Need for a Physician Home Loan?

Most physician mortgage lenders require a minimum credit score of 700, though some programs accept scores as low as 680. A score above 720 will get you the best available rates and the most flexible terms.

Credit score ranges and what to expect:

- 740+ — Best rates, highest loan limits, most program options

- 720–739 — Strong approval odds, competitive rates

- 700–719 — Approved at most lenders, slightly higher rates

- 680–699 — Limited options, may require larger down payment

- Below 680 — Most physician loan programs will decline; consider building credit before applying

Edge case: If your score dropped during residency due to high utilization or missed payments, some lenders will look at your payment history holistically. A letter of explanation and evidence of improved financial habits can help, but it's not guaranteed.

The fastest ways to move your score before applying:

- Pay down credit card balances below 30% utilization

- Dispute any errors on your credit report

- Avoid opening new credit accounts in the 6 months before applying

- Keep old accounts open — length of credit history matters

For a deeper look at how credit interacts with your overall financing strategy, our real estate financing fundamentals guide covers the full picture.

Are Physician Mortgages Worth It Compared to Traditional Mortgages?

For most doctors buying a primary residence in 2026, physician mortgages are worth it — especially if you have less than 20% for a down payment or carry significant student loan debt. The no-PMI benefit alone often makes the math work in your favor, even if the interest rate is slightly higher than a conventional loan.

Physician loan vs. conventional — a real comparison:

Assume a $700,000 home, 5% down ($35,000):

| Conventional Loan | Physician Mortgage | |

|---|---|---|

| Down Payment | $35,000 | $35,000 |

| PMI (monthly) | ~$350–$500/mo | $0 |

| Rate (estimate) | 6.5% | 6.75% |

| Monthly P&I | ~$4,200 | ~$4,320 |

| PMI added | +$400 | $0 |

| Effective monthly cost | ~$4,600 | ~$4,320 |

In this scenario, the physician mortgage saves roughly $280 per month despite having a slightly higher rate. Over five years, that's $16,800 back in your pocket.

When a conventional loan might win: If you have 20% or more to put down, a conventional loan will likely offer a lower rate with no PMI — making it the better choice. The physician loan shines brightest when your down payment is under 20%.

For a side-by-side look at how loan term length affects your long-term costs, our 15 vs. 30-year mortgage rates guide is worth a read before you commit to a structure.

Can You Use a Physician Mortgage If You Have Medical School Debt?

Yes — and this is actually one of the primary reasons physician mortgage programs exist. Medical school debt is treated very differently by physician home loan lenders compared to conventional underwriters.

Here's how lenders typically handle student loans:

- Deferred loans — many physician lenders exclude deferred student loans from the DTI calculation entirely

- Income-based repayment (IBR) — if you're on an IBR plan, lenders often use your actual monthly payment (which could be $0–$200) rather than a percentage of the loan balance

- Standard repayment — if you're actively repaying, the actual monthly payment is used

So based: A doctor with $300,000 in student loans on an IBR plan paying $150/month could qualify for a $900,000 home loan. That same borrower applying for a conventional mortgage might get rejected because the lender calculates a hypothetical $3,000/month student loan payment.

What doesn't change: You still need to demonstrate the ability to repay the mortgage itself. Your total debt load — including the new mortgage — still gets evaluated. The physician loan just gives you a much fairer starting point.

What Down Payment Do Doctors Need With a Physician Mortgage?

Most physician mortgage programs offer three down payment tiers based on loan size. The 0 down physician loan is available up to a certain loan limit, with small down payments required above that threshold.

Typical down payment structure for physician home loan lenders:

| Loan Amount | Down Payment Required |

|---|---|

| Up to $1,000,000 | 0% |

| $1,000,001 – $1,500,000 | 5% |

| $1,500,001 – $2,000,000 | 10% |

| Above $2,000,000 | 15–20% (varies by lender) |

The 0 down physician loan is genuinely extraordinary for new doctors who've spent a decade in school and training with minimal ability to save. You can close on a $900,000 home with essentially just closing costs out of pocket — typically 2–3% of the loan amount.

Closing costs to budget for:

- Origination fees: 0.5–1% of loan

- Title insurance: varies by state

- Appraisal: $500–$1,000

- Prepaid interest and escrow: 1–2 months of payments

- Attorney fees (in attorney states): $500–$1,500

Some physician mortgage lenders also allow seller concessions to cover closing costs — worth negotiating, especially in a buyer's market. Check our Spring 2026 housing market outlook to see where negotiating leverage currently sits.

Common Mistakes Doctors Make When Applying for a Home Loan

The biggest mistakes doctors make are applying too late, underestimating their buying power, and not shopping multiple physician mortgage lenders. Let it cook before you see results — rushing into the first offer you get is how you leave money on the table.

Top mistakes to avoid:

Not submitting your employment contract — This is the document that lets lenders underwrite your future income. Without it, you're stuck qualifying on residency pay alone.

Opening new credit accounts before closing — A new car loan or credit card in the 60 days before closing can tank your approval or change your rate.

Assuming all physician lenders are the same — Program terms vary significantly. One lender might cap the 0% down option at $750,000; another goes to $1.25 million.

Ignoring the rate vs. PMI trade-off — Some doctors chase the lowest rate without realizing that a slightly higher rate with no PMI is cheaper overall.

Forgetting about reserves — Some lenders require 2–6 months of mortgage payments in savings even after closing. Know this requirement before you drain your account on the down payment.

Applying before your contract is signed — Pre-approval is possible, but full approval typically requires a signed offer letter or employment contract.

Not asking about dental professional loans specifically — Dentists sometimes assume physician programs don't apply to them. Many do — ask explicitly.

How Soon After Medical School Can You Get Approved for a Mortgage?

You can get approved for a physician mortgage immediately after medical school if you have a signed residency or employment contract. Most physician mortgage lenders will accept a start date up to 90 days in the future — some go up to 180 days.

The timeline looks like this:

- Match Day (March) → Apply for pre-approval with your match results and anticipated contract

- Signed residency contract (April–May) → Submit for full approval

- Residency start (June–July) → Close on your home around the same time you start

This is the fresh start most residents dream about — moving into your own place at the same time you start your career. No more renting a studio apartment near the hospital. The physician loan makes that timing possible in a way conventional mortgages simply don't.

Important: You don't need to have received a single paycheck yet. The signed contract is enough for most physician home loan lenders to proceed.

Are Physician Mortgages Available in All 50 States?

Physician mortgage programs are NOT available in all 50 states through every lender. Coverage varies significantly by institution. That said, most major physician mortgage lenders operate in 30–45 states, and the gap is closing.

States with the most robust physician loan availability tend to be high-population states with large medical school systems: California, Texas, New York, Florida, Illinois, Ohio, Pennsylvania, and Massachusetts.

States with more limited options: Wyoming, Montana, Vermont, and other lower-population states may have fewer physician mortgage lenders operating locally, though national online lenders often fill the gap.

How to find coverage in your state:

- Search "[lender name] physician loan [your state]" to confirm availability

- Use physician loan comparison tools (several reputable ones exist through medical association websites)

- Work with a mortgage broker who specializes in physician loans — they can access multiple programs across lenders simultaneously

Speaking of brokers, our guide on mortgage broker vs. direct lender breaks down exactly when using a broker saves you more — and physician loans are one of those cases where a specialized broker earns their keep.

What Interest Rates Do Physician Mortgage Lenders Typically Offer?

Physician mortgage loan rates in 2026 typically run 0.125% to 0.5% higher than conventional 30-year fixed rates for the same borrower profile. With conventional 30-year rates currently in the mid-to-high 6% range, physician loan rates are generally sitting between 6.5% and 7.25% depending on loan size, down payment, and credit score.

Doctor loan rates 2026 — what moves them:

- Credit score — 740+ gets the best pricing; below 700 adds meaningful rate premium

- Down payment — 0% down typically carries a higher rate than 5% or 10% down

- Loan size — jumbo physician loans (above $1M) often carry slightly higher rates

- Fixed vs. ARM — a 5/1 or 7/1 ARM can offer rates 0.5–1% lower than 30-year fixed, which some residents use strategically if they plan to move after training

Physician loan vs. DSCR loan rates: Worth noting for doctors who are also thinking about real estate investing — DSCR loans (used for investment properties) operate on completely different underwriting logic and typically carry higher rates than physician mortgages. If you're considering adding rental properties to your portfolio, our best DSCR loan lenders guide covers that lane separately.

The no-PMI physician loan advantage is most powerful in the current rate environment. When PMI costs $300–$600/month and the rate premium is only 0.25%, the math almost always favors the physician program.

Frequently Asked Questions

Q: Can a dentist get a physician mortgage?

Yes. Most physician mortgage lenders include DDS and DMD degree holders. Dental professional loans are a well-established subset of professional mortgage programs. Some lenders market them separately; always ask specifically.

Q: Can I use a physician mortgage to buy a rental property or investment property?

No. Physician mortgage programs are designed for primary residences only. If you want to buy investment properties, look at DSCR loans or conventional investment property financing instead.

Q: Does my specialty matter for physician loan approval?

Generally, no. Whether you're in family medicine or neurosurgery, most physician mortgage lenders qualify based on your degree and employment status, not your specialty. Higher-earning specialties may help with loan amount qualification.

Q: Can I use a physician mortgage more than once?

Yes — as long as the property you're buying is your primary residence. If you move cities for a new position, you can use a physician loan again for your next primary home.

Q: What happens if my employment contract falls through before closing?

This is a real risk. If your job falls through before closing, the loan will likely not proceed. Some lenders build in contingencies; discuss this scenario with your loan officer before applying.

Q: Is there a maximum income limit for physician mortgages?

No. There is no income ceiling. These are high-earner mortgage programs designed specifically for professionals with strong income trajectories.

Q: Can pharmacists and veterinarians qualify for physician loans?

Yes, at select lenders. PharmD holders qualify at many major physician mortgage lenders. DVM/VMD holders have fewer options but programs do exist — search specifically for "veterinarian mortgage programs."

Q: Do physician loans require an appraisal?

Yes. All physician mortgage loans require a property appraisal, just like conventional loans. The appraisal protects both you and the lender.

Q: Can I refinance out of a physician loan later?

Absolutely. Many doctors use a physician loan to get into a home early, then refinance into a conventional loan once they've built equity and have a stronger financial profile. This is a common and smart strategy.

Q: Are no-PMI physician loans actually no PMI forever?

Yes — physician mortgage programs that offer no PMI don't require it at any point during the loan. It's not deferred; it's eliminated entirely from the loan structure.

Q: What if I'm self-employed as a physician (private practice)?

Self-employed physicians face more documentation requirements. You'll typically need two years of tax returns, a profit-and-loss statement, and possibly a CPA letter. Some lenders have specific programs for self-employed doctors; others are more restrictive.

Q: How is a physician mortgage different from an FHA loan?

FHA loans require PMI (called MIP), have lower loan limits, and are available to any qualified borrower. Physician mortgages require no PMI, have much higher loan limits, and are restricted to medical professionals. For most doctors, the physician loan is the superior choice.

Conclusion: The Playbook for Doctors Buying Property Early

Physician mortgage lenders exist because the traditional mortgage system was never built for the doctor's career arc. You spend a decade in school and training, accumulate six figures in debt, and then step into one of the highest-earning careers in the country — all before you've had a chance to save a meaningful down payment.

The no PMI physician loan, the 0 down physician loan, and the flexible student debt treatment aren't loopholes. They're the system working correctly for a specific type of borrower.

Your action plan:

- Check your credit score — aim for 720+ before applying

- Gather your employment contract — this is your most powerful document

- Get quotes from at least 3 physician mortgage lenders — compare APR, not just rate

- Calculate the PMI savings — run the numbers against a conventional loan with the same down payment

- Understand your DTI — know how your student loans will be treated before you apply

- Work with a broker who specializes in physician loans — they know which programs are available in your state and which lenders are most competitive right now

The gate keeping around physician mortgage programs stops here. This is fresh information that every medical professional deserves to have before they sign a lease for another year. The tools exist. The programs are real. Now you know how to use them.

For more on navigating the broader financing landscape as a high-income professional, explore our real estate financing hub and our mortgage options overview — both built with the same no-gatekeeping approach.

{kind=link}