Last updated: May 24, 2026

Quick Answer: Non-QM mortgage lenders are financial institutions and non-bank home loan lenders that offer mortgages outside the standard "Qualified Mortgage" rules set by the Consumer Financial Protection Bureau (CFPB). They exist specifically for borrowers who can't document income the traditional way — think self-employed entrepreneurs, real estate investors, and high-earning professionals with complex finances. If a conventional lender has turned you down, a non-QM lender may be your most viable path to financing.

Key Takeaways

- Non-QM stands for "Non-Qualified Mortgage" — loans that don't meet the CFPB's standard underwriting rules but are still legal and widely used.

- Non-QM mortgage lenders accept alternative income documentation like bank statements, asset depletion, and rental income (DSCR).

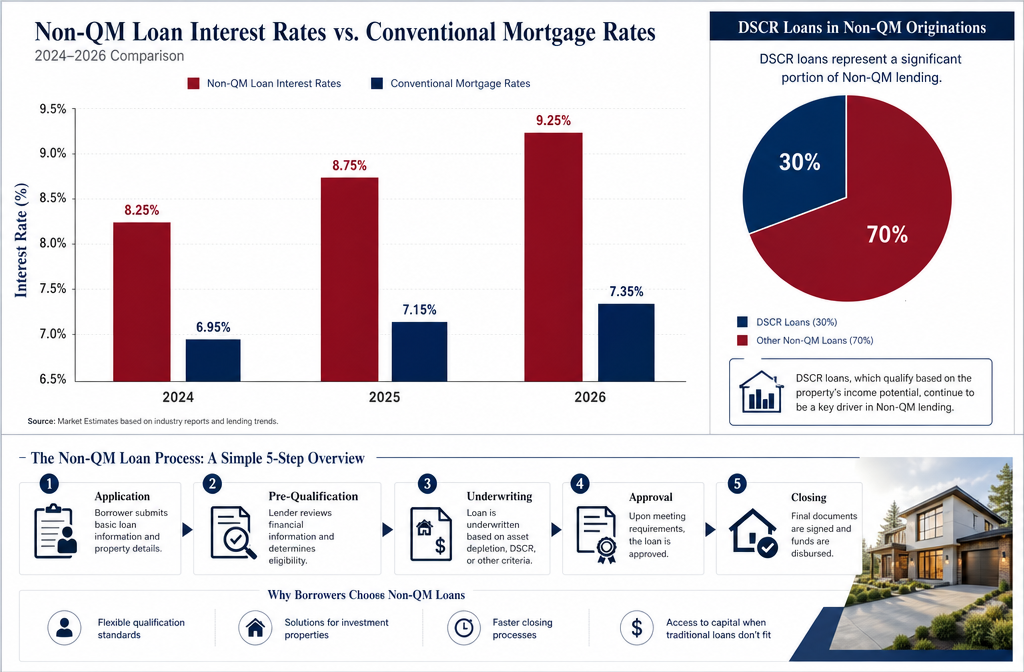

- As of 2026, non-QM loans represent an estimated 15% of total mortgage originations in the U.S., reflecting serious growth in this lending segment.

- Interest rates for non-QM loans typically run 1% to 3% higher than conventional mortgage rates, depending on borrower risk profile.

- DSCR loans (Debt Service Coverage Ratio) account for roughly 30% of all non-QM originations — making them the most popular product in this category.

- Real estate investors, self-employed borrowers, and recent credit-event survivors are the primary users of non-QM loans.

- Top non-QM lenders in 2026 include Angel Oak Lending, Griffin Funding, and several other non-bank mortgage providers.

- Credit score minimums vary by lender but typically start around 620, with some programs accepting scores as low as 580.

- AI-driven non-QM underwriting is changing the speed and accuracy of loan approvals in 2026.

- Non-QM loans carry real risks — higher rates, larger down payments, and less consumer protection than conventional loans.

What Exactly Is a Non-QM Mortgage Loan?

A Non-QM mortgage loan is any home loan that doesn't meet the federal "Qualified Mortgage" standards established by the CFPB under the Dodd-Frank Act. That doesn't mean these loans are predatory or sketchy — it simply means they operate outside the standard underwriting box.

Qualified Mortgages (QM) require lenders to verify a borrower's ability to repay using specific criteria: W-2 income, tax returns, a debt-to-income ratio (DTI) below 43%, and no risky loan features like interest-only payments or balloon payments. Non-QM loans drop one or more of those requirements to serve borrowers whose financial lives don't fit that mold.

Here's what makes a loan "non-QM" in practice:

- It may allow DTI ratios above 43%

- It may use bank statements instead of tax returns to verify income

- It may include interest-only payment periods

- It may use asset depletion or rental income as the primary qualifying factor

- It may allow financing shortly after a bankruptcy or foreclosure

Non-QM is not subprime. That's a distinction worth making. These loans are underwritten with real scrutiny — just different scrutiny. Lenders still assess creditworthiness; they just use a broader set of tools to do it. The non-QM lending growth in 2026 is a direct response to how many Americans now earn income in ways that don't show up cleanly on a tax return.

Non-QM Mortgage Lenders: Who They Are and When to Use One

Non-QM mortgage lenders are specialized non-bank mortgage providers — and sometimes credit unions or portfolio lenders — that have built their entire lending infrastructure around borrowers who fall outside conventional guidelines. Understanding who they are and when to use one is the whole game.

Who Non-QM Lenders Are

Unlike traditional banks that sell their loans to Fannie Mae or Freddie Mac (which require QM compliance), non-QM lenders typically hold loans in their own portfolio or sell them to private investors. That flexibility is what allows them to write loans with alternative documentation.

The major players in the non-QM space as of 2026 include:

| Lender | Specialty | Notable Products |

|---|---|---|

| Angel Oak Lending | Pioneer in non-QM, broad product menu | Bank statement loans, DSCR, investor cash flow |

| Griffin Funding | Self-employed and investor focus | Bank statement, asset depletion, DSCR |

| Acra Lending | Credit-event and jumbo non-QM | Recent bankruptcy, foreign national loans |

| Citadel Servicing | High-DTI and complex income | Interest-only, stated income programs |

| A&D Mortgage | Investor-heavy product line | DSCR, fix-and-flip, multi-family |

These are non-bank home loan lenders — meaning they don't take deposits like a traditional bank. They're funded through private capital, warehouse lines of credit, and mortgage-backed securities sold to institutional investors.

When to Use a Non-QM Lender

Use a non-QM lender when:

- You're self-employed and your tax returns show less income than you actually earn (after write-offs)

- You're a real estate investor qualifying based on property cash flow rather than personal income

- You recently had a bankruptcy, foreclosure, or short sale and can't wait years for conventional eligibility

- Your income is irregular — commissions, freelance payments, or foreign-sourced income

- You need a jumbo loan and your financial profile doesn't fit agency guidelines

- Your DTI is above 43% but your assets and payment history are strong

For a deeper look at how lender types compare, check out our guide on Mortgage Broker vs Direct Lender: Which Saves Investors More? — it breaks down the structural differences that affect your rate and approval odds.

How Are Non-QM Mortgages Different From Traditional Mortgages?

The core difference is the underwriting standard. Traditional mortgages follow agency guidelines set by Fannie Mae, Freddie Mac, FHA, or VA. Non-QM mortgages follow the lender's own internal guidelines, which can be far more flexible.

Side-by-side comparison:

| Feature | Conventional/QM | Non-QM |

|---|---|---|

| Income verification | W-2, tax returns | Bank statements, DSCR, assets |

| Max DTI | 43–50% (with exceptions) | Up to 55%+ depending on lender |

| Credit score minimum | 620–640 typical | 580–620 typical |

| Down payment | 3–20% | 10–30% |

| Interest rate | Market rate (e.g., 6–7% in 2026) | Typically 1–3% higher |

| Loan features | Standard amortization | May allow interest-only, balloon |

| Government backing | Yes (FHA, VA, Fannie/Freddie) | No — portfolio or private |

| Post-bankruptcy wait | 2–7 years | As little as 1 day (some programs) |

The trade-off is straightforward: more flexibility costs more money. Non-QM borrowers pay for access through higher rates and larger down payment requirements. For many borrowers, that's still the right call — especially when the alternative is no loan at all.

For context on where conventional rates sit right now, see our Current Mortgage Rates February 2026 coverage — it gives you a solid baseline for comparing non-QM premiums.

How Much Higher Are Interest Rates for Non-QM Loans?

Non-QM mortgage rates in May 2026 typically run 1% to 3% above comparable conventional rates, depending on the loan type, borrower credit profile, and down payment size. With 30-year conventional rates hovering around 6.5–7% in 2026, non-QM borrowers should expect rates in the 7.5–10% range for most products.

Rate ranges by non-QM product type (estimates, May 2026):

- Bank statement loans: 7.5% – 9.0%

- DSCR loans: 7.25% – 8.75%

- Asset depletion loans: 7.75% – 9.5%

- Interest-only non-QM: 8.0% – 10%+

- Recent credit event programs: 8.5% – 11%

Several factors push your rate higher within those ranges:

- Lower credit score

- Higher LTV (lower down payment)

- Recent credit events (bankruptcy, foreclosure)

- Higher DTI ratio

- Shorter loan term history with the lender

The good news: non-QM rates have become more competitive as the market has grown. AI-driven non-QM underwriting is one reason for this — lenders using machine learning to assess risk more accurately are able to price loans more precisely rather than applying blanket rate premiums to every non-standard borrower.

Who Typically Qualifies for a Non-QM Mortgage?

Non-QM loans are built for borrowers whose income, credit history, or financial structure doesn't fit conventional guidelines — not for borrowers who simply couldn't qualify anywhere. There's a difference, and lenders know it.

Primary borrower profiles that use non-QM:

1. Self-employed borrowers

Entrepreneurs, freelancers, and business owners who write off significant expenses on their taxes often show low taxable income — even when their actual cash flow is strong. Bank statement loans solve this by using 12–24 months of deposits instead of tax returns.

2. Real estate investors

Investors who own multiple properties often have complex income pictures. DSCR loans let them qualify based on whether the rental property generates enough income to cover the mortgage payment — personal income becomes secondary. For a full breakdown of this product, see our Best DSCR Loan Lenders for Investment Properties 2026 guide.

3. High-net-worth individuals with low income

Some wealthy borrowers have massive assets but little W-2 income. Asset depletion loans calculate a monthly "income" figure by dividing total assets over the loan term, allowing qualification without a traditional income stream.

4. Recent credit event borrowers

People who experienced bankruptcy, foreclosure, or short sales during economic downturns may qualify for non-QM loans much sooner than conventional programs allow.

5. Foreign nationals

Non-U.S. citizens purchasing property in the U.S. often lack the credit history required for agency loans. Several non-QM lenders have dedicated foreign national programs.

6. Gig economy workers

Uber drivers, content creators, and consultants with irregular income streams can use bank statements or 1099 income to qualify.

What Credit Score Do You Need for a Non-QM Loan?

Most non-QM mortgage lenders require a minimum credit score of 620, though some programs accept scores as low as 580 — and a handful of niche products have no minimum at all (with significant compensating factors required). The higher your score, the better your rate and terms.

General credit score tiers for non-QM:

- 740+: Best available rates, lowest down payment requirements

- 700–739: Competitive rates, standard non-QM terms

- 660–699: Slightly elevated rates, may need larger down payment

- 620–659: Higher rates, stricter LTV requirements (expect 25–30% down)

- 580–619: Limited programs available, expect premium pricing

- Below 580: Very few options; typically requires significant assets or equity

Common mistake: Borrowers assume a low credit score automatically means no options. That's not accurate. Non-QM lenders look at the full picture — credit score is one factor, not the only one. A borrower with a 610 score, 35% down payment, and 18 months of strong bank statement deposits will get approved at many non-QM lenders. Let it cook before you see results — meaning, if you're actively repairing credit, even 6–12 months of improvement can meaningfully change your non-QM rate.

Are Non-QM Mortgages Good for Self-Employed People?

So based — yes, non-QM mortgages are one of the best financing tools available for self-employed borrowers. The bank statement loan product was essentially built for this exact situation.

Here's the problem self-employed borrowers face with conventional loans: the IRS rewards business owners for writing off expenses. The more you write off, the lower your taxable income. But conventional lenders use taxable income to qualify you. So a business owner grossing $200,000 per year who writes off $120,000 in legitimate expenses shows only $80,000 in qualifying income on their tax return — which may not be enough to get the loan they need.

How bank statement loans solve this:

- Lender collects 12 or 24 months of personal or business bank statements

- They calculate average monthly deposits

- They apply an expense ratio (typically 50% for business accounts, 100% for personal)

- The result becomes your qualifying income

Example:

- 24-month business bank statement average: $25,000/month in deposits

- Lender applies 50% expense ratio

- Qualifying income: $12,500/month ($150,000/year)

- This is often significantly higher than what shows on a tax return

Self-employed mortgage lenders like Angel Oak Lending and Griffin Funding have refined this process considerably. Griffin Funding, for instance, accepts as little as one year of self-employment history for bank statement loans — which is fresh news for newer business owners who previously had to wait two years to qualify anywhere.

For broader mortgage education, our Real Estate Financing Guide: Mortgages, Credit & Down Payments 2026 covers the full financing landscape in plain language.

What Kinds of Income Documentation Do Non-QM Lenders Accept?

Non-QM lenders accept a wide range of alternative documentation that conventional lenders won't touch. This is the core value proposition of the entire non-QM category.

Documentation types accepted by most non-QM lenders:

| Documentation Type | Best For | How It Works |

|---|---|---|

| Bank statements (12–24 months) | Self-employed, freelancers | Deposits averaged to calculate income |

| DSCR (no income docs needed) | Real estate investors | Property cash flow covers the mortgage |

| Asset depletion/dissipation | High-net-worth, retirees | Assets divided over loan term = income |

| 1099 income | Independent contractors | 1099s averaged over 1–2 years |

| Profit & loss statements | Business owners | CPA-prepared P&L used in place of returns |

| Foreign income | Foreign nationals, expats | Foreign pay stubs, bank statements, employer letters |

| Rental income (full schedule) | Landlords with multiple properties | All rental income counted, not just net |

| Verbal verification of employment | Recent job changers | Employer call confirms income without full docs |

Edge case worth knowing: Some non-QM lenders offer "no-doc" or "SISA" (Stated Income, Stated Assets) programs for very high-credit, high-equity borrowers. These are rare and come with significant rate premiums, but they exist for situations where documentation is genuinely impossible to produce.

The gatekeeping that traditional banks do around income documentation is exactly what non-QM lending was designed to disrupt. If your income is real but hard to document the conventional way, there's almost certainly a non-QM product that works.

Which Non-QM Lenders Have the Best Rates Right Now?

As of May 2026, the most competitive non-QM rates are coming from established non-bank mortgage providers with large loan volumes and AI-driven underwriting platforms. Rate shopping matters enormously in this space — spreads between lenders on the same loan profile can be 0.5% to 1.5%.

Top non-QM lenders to compare in 2026:

Angel Oak Lending — Widely considered the pioneer of non-QM lending. They offer one of the broadest product menus in the industry, including bank statement loans, investor cash flow (DSCR), and asset qualifier programs. Their rates are competitive for borrowers with 700+ credit scores.

Griffin Funding — Strong reputation for self-employed borrowers and investors. Known for transparent rate disclosure and a streamlined application process. Offers bank statement, DSCR, asset depletion, and foreign national loans.

Acra Lending — Specializes in credit-challenged borrowers and jumbo non-QM. Good option for recent bankruptcy or foreclosure situations.

A&D Mortgage — Heavy investor focus with strong DSCR and multi-family products. Competitive for portfolio builders.

Citadel Servicing — One of the few lenders still offering high-DTI programs. Good for borrowers with strong income but heavy debt obligations.

How to get the best rate:

- Work with a mortgage broker who has access to multiple non-QM lenders (not just one)

- Bring a larger down payment — even 5% extra can drop your rate meaningfully

- Clean up any credit report errors before applying

- Compare GFEs (Good Faith Estimates) from at least 3 lenders

- Ask specifically about rate buy-down options

Non-QM rates in May 2026 are also being shaped by broader market forces. Our coverage of how the Federal Government's $200B MBS purchase is affecting mortgage rates in 2026 explains why the macro environment matters even for non-agency loans.

Can You Buy an Investment Property With a Non-QM Loan?

Yes — and for many real estate investors, non-QM loans are the preferred financing tool, not a fallback option. DSCR loans in particular are extraordinary for investment property purchases because they completely remove personal income from the qualification equation.

DSCR (Debt Service Coverage Ratio) loans qualify the property, not the borrower. The lender calculates whether the property's rental income covers the mortgage payment:

DSCR Formula:

DSCR = Monthly Rental Income ÷ Monthly Mortgage Payment (PITIA)

- DSCR above 1.25: Strong — most lenders love this

- DSCR of 1.0–1.24: Acceptable at most lenders

- DSCR below 1.0: Some lenders still approve with compensating factors; others won't touch it

DSCR loans now account for approximately 30% of all non-QM originations in 2026 — making them the single largest product category in the non-QM market. That's not an accident. Real estate investors have discovered that DSCR loans let them scale a portfolio without their personal income becoming the bottleneck.

Other non-QM products useful for investors:

- Fix-and-flip loans — Short-term bridge financing for renovation projects

- Multi-family non-QM — For 5+ unit properties outside conventional limits

- Portfolio loans — Blanket financing for multiple properties under one loan

For investors running the numbers on rental properties, pair this with our Vacation Rental Investment: Run These Numbers Before You Buy guide — it covers the cash flow analysis that DSCR lenders will scrutinize.

How Long After Bankruptcy Can You Get a Non-QM Mortgage?

Non-QM mortgage lenders can approve borrowers as soon as one day after a bankruptcy discharge in some programs — compared to 2–4 years for FHA loans and up to 7 years for conventional loans. This is one of the most impactful advantages of the non-QM market for borrowers recovering from financial hardship.

Waiting period comparison by loan type:

| Loan Type | Chapter 7 Bankruptcy | Chapter 13 Bankruptcy | Foreclosure |

|---|---|---|---|

| Conventional (Fannie/Freddie) | 4 years | 2 years | 7 years |

| FHA | 2 years | 1 year | 3 years |

| VA | 2 years | 1 year | 2 years |

| Non-QM | 1 day – 1 year | 1 day – 1 year | 1 day – 1 year |

The trade-off: the closer you are to the bankruptcy discharge, the higher the rate and down payment required. A borrower who discharged bankruptcy yesterday will face very different terms than one who's 18 months out with a rebuilt credit profile.

Typical non-QM terms for recent credit events:

- Down payment: 20–30% minimum

- Credit score: 580–620 minimum (varies by lender)

- Rate premium: 2–4% above standard non-QM rates

- Reserve requirements: 6–12 months of mortgage payments in liquid assets

The impeccable move here is to use the non-QM loan as a bridge — get into the property, rebuild your credit over 2–3 years, then refinance into a conventional loan at a lower rate.

What Are the Risks of Getting a Non-QM Mortgage?

Non-QM loans carry real risks that borrowers should understand before signing. The flexibility comes with a cost, and in some cases, that cost can be significant.

Primary risks to understand:

1. Higher interest rates

Paying 1–3% more in interest adds up fast. On a $400,000 loan, a 2% rate premium costs roughly $8,000 per year in additional interest — that's $240,000 over a 30-year term if you never refinance.

2. Larger down payment requirements

Most non-QM lenders require 10–30% down, compared to 3–5% for conventional loans. This ties up more capital upfront.

3. Less consumer protection

QM loans come with legal protections for borrowers — lenders must prove they assessed your ability to repay. Non-QM loans have fewer of these protections, which means more responsibility falls on the borrower to understand what they're signing.

4. Prepayment penalties

Some non-QM loans include prepayment penalties — fees charged if you pay off the loan early (including through refinancing). Always ask about this before closing.

5. Balloon payments

Certain non-QM products include balloon payments — large lump-sum amounts due at the end of a shorter term (e.g., 5 or 7 years). If you can't refinance or sell by then, you're in trouble.

6. Market risk for investors

DSCR loans are tied to rental income. If your property sits vacant for months, the math that qualified you for the loan no longer works — but the payment is still due.

Common mistake: Borrowers focus so much on getting approved that they don't read the loan terms carefully. Always review the Note and Deed of Trust with a real estate attorney before closing, especially for non-QM products.

Are Non-QM Mortgages a Good Option for Real Estate Investors?

For the right investor, non-QM mortgages — especially DSCR loans — are one of the most powerful financing tools available in 2026. They allow portfolio scaling that conventional financing simply can't match once you hit the 10-loan Fannie Mae limit or once your personal income can't support more debt.

When non-QM is the right call for investors:

- You own 10+ properties and conventional lenders won't add more

- Your personal income is low but your properties cash flow well

- You want to move fast on a deal without 60-day conventional timelines

- You're buying a property type (like short-term rental or mixed-use) that conventional lenders won't finance

When non-QM might not be the right call:

- You can qualify conventionally — always take the lower rate if you can

- Your DSCR is below 1.0 and the property is a stretch financially

- You're a first-time investor without cash reserves to cover vacancies

The non-QM lending growth in 2026 is being driven largely by real estate investors who've figured out that DSCR loans let them treat each property as its own financial entity. That's an extraordinary shift from the old model where your personal W-2 income was the ceiling on everything you could buy.

For investors building a portfolio from scratch, our Cash Flow Real Estate Investing: Find Deals That Pay Day One guide pairs perfectly with understanding non-QM financing options. And if you're comparing non-QM to other investment financing tools, our Best HELOC Lenders for Investment Property 2026 breakdown covers another popular option worth knowing.

What Mistakes Do People Make When Applying for Non-QM Loans?

The biggest mistakes in the non-QM application process are avoidable — and they almost always come down to not understanding how these loans are underwritten.

Top mistakes to avoid:

1. Going directly to a single lender

Non-QM rates and guidelines vary wildly between lenders. Borrowers who apply to only one lender often leave money on the table or get denied when another lender would have approved them. Work with a mortgage broker who specializes in non-QM.

2. Not organizing bank statements before applying

Non-QM underwriters look at every deposit in your bank statements. Large, unexplained deposits trigger questions. Clean up your statements — document the source of any irregular deposits before you apply.

3. Misrepresenting income or assets

Non-QM loans have more flexibility, but they still require honesty. Mortgage fraud is a federal crime regardless of loan type. Don't inflate deposit amounts or fabricate income sources.

4. Ignoring the prepayment penalty clause

Some borrowers plan to refinance into a conventional loan in 2–3 years. If their non-QM loan has a 3-year prepayment penalty, that plan gets expensive fast. Read the fine print.

5. Underestimating reserve requirements

Many non-QM lenders require 6–12 months of mortgage payments in liquid reserves after closing. Borrowers who drain their accounts for the down payment often get denied at the finish line.

6. Not comparing the total cost of the loan

Rate is one number. APR (which includes fees) is the real number. Non-QM loans sometimes have origination fees of 1–3 points. Factor that into your comparison.

Frequently Asked Questions About Non-QM Mortgage Lenders

Q: Is a non-QM loan the same as a subprime loan?

No. Non-QM loans are underwritten with documented ability-to-repay analysis — just using alternative methods. Subprime loans from the pre-2008 era often had no income verification at all. The regulatory environment is fundamentally different today.

Q: Can I get a non-QM loan for a primary residence?

Yes. Non-QM loans are available for primary residences, second homes, and investment properties. Bank statement loans and asset depletion loans are commonly used for primary home purchases.

Q: How long does a non-QM loan take to close?

Most non-QM loans close in 21–45 days. Some lenders with AI-driven underwriting platforms can close in as little as 15 days for straightforward DSCR loans.

Q: Do non-QM lenders report to credit bureaus?

Yes. Non-QM mortgage payments are reported to the major credit bureaus just like conventional loans. On-time payments build credit; missed payments hurt it.

Q: Can I refinance a non-QM loan into a conventional loan later?

Yes — and this is a common strategy. Borrowers use a non-QM loan to purchase now, then refinance into a conventional loan once they meet standard guidelines (improved credit, longer self-employment history, etc.).

Q: What's the maximum loan amount for non-QM loans?

There's no universal cap. Many non-QM lenders go up to $3 million or more on jumbo products. Some go higher for the right borrower profile.

Q: Are non-QM loans available in all 50 states?

Most major non-QM lenders like Angel Oak Lending and Griffin Funding operate in the majority of U.S. states, but coverage varies. Always confirm your state is included before starting the application.

Q: Do non-QM lenders require an appraisal?

Most do, yes. Some DSCR lenders accept desktop appraisals or automated valuation models (AVMs) for lower-risk properties, but a full appraisal is standard for most non-QM products.

Q: What's the minimum down payment for a non-QM loan?

Typically 10–20% for most products, with 20–30% required for borrowers with lower credit scores or recent credit events. Some DSCR programs allow 15% down for strong-cash-flow properties.

Q: How is AI changing non-QM underwriting?

AI-driven non-QM underwriting platforms are analyzing bank statement patterns, rental income consistency, and asset liquidity faster and more accurately than manual review. This is compressing approval timelines and allowing more precise risk pricing — which benefits borrowers with strong profiles who were previously lumped into broad risk buckets.

Conclusion: Is a Non-QM Lender Right for You?

Non-QM mortgage lenders exist because the financial lives of millions of Americans don't fit inside a W-2 box — and that's not a flaw, it's just reality. Whether you're a self-employed business owner, a real estate investor scaling a rental portfolio, or someone rebuilding after a financial setback, there's likely a non-QM product designed for your situation.

The non-QM market representing an estimated 15% of total originations in 2026 isn't a niche anymore. It's a legitimate, growing segment of the mortgage industry — and with AI-driven underwriting making approvals faster and pricing more precise, the gap between non-QM and conventional financing is narrowing in meaningful ways.

Your actionable next steps:

- Identify your borrower profile — self-employed, investor, credit event, or high-net-worth. This determines which non-QM product fits.

- Pull your credit report — know your score before any lender does.

- Gather 12–24 months of bank statements — organized and ready to explain any large deposits.

- Work with a mortgage broker who has access to multiple non-QM lenders, not just one.

- Compare at least 3 loan estimates — rate, APR, fees, prepayment penalty, and reserve requirements.

- Build a refinance timeline — if your goal is to move to conventional financing in 2–3 years, make sure the non-QM loan terms support that plan.

The information is out there. The lenders are real. The products work. What's been gatekept for too long is the clear, broker-level explanation of how to actually use them — and that's exactly what we're here for.

For more on navigating your mortgage options, explore our full mortgage options hub and our FHA Loan vs Conventional Loan comparison for 2026 — two resources that give you the full picture before you commit to any financing path.

{kind=link}