Last updated: April 23, 2026

Quick Answer: The FHA loan vs conventional loan debate doesn’t have a universal winner — it depends on your credit score, down payment, and how long you plan to stay in the home. Borrowers with credit scores below 620 and limited savings almost always save more upfront with an FHA loan. But borrowers with scores above 700 and 20% down will typically pay less over time with a conventional loan, largely because they avoid mortgage insurance entirely.

Key Takeaways

- FHA loans require a minimum 3.5% down payment with a 580+ credit score, or 10% down with scores between 500–579.

- Conventional loans typically require a 620+ credit score and can go as low as 3% down through programs like Fannie Mae’s HomeReady.

- FHA mortgage insurance (MIP) is permanent for most borrowers — it doesn’t cancel unless you refinance. PMI on a conventional loan cancels automatically at 20% equity.

- FHA loans are assumable — a major advantage in a high-rate environment like 2026.

- FHA 203k renovation loans let you finance a home purchase AND repairs in a single loan — conventional renovation products exist but are less accessible.

- State-specific FHA loan requirements vary slightly by county loan limits, but the core credit and down payment rules are federally set.

- Best FHA lenders in 2026 include Rocket Mortgage, Better Mortgage, New American Funding, and Guild Mortgage.

- A conventional loan wins long-term for buyers with strong credit. An FHA loan wins for buyers who need to get in the door now.

What Is the Difference Between an FHA and Conventional Loan?

An FHA loan is backed by the Federal Housing Administration, meaning the government insures the lender against default. A conventional loan is not government-backed — it follows guidelines set by Fannie Mae or Freddie Mac and carries more risk for the lender, which is why qualifications are stricter.

Here’s the core breakdown:

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Government-backed | ✅ Yes | ❌ No |

| Minimum credit score | 500 (10% down) / 580 (3.5% down) | 620 |

| Minimum down payment | 3.5% | 3% (with qualifying programs) |

| Mortgage insurance | MIP (usually permanent) | PMI (cancels at 20% equity) |

| Loan limits (2026) | Up to $524,225 (standard) / $1,209,750 (high-cost areas) | Up to $806,500 (conforming) |

| Assumable | ✅ Yes | ❌ Rarely |

| Seller concessions | Up to 6% | 3%–9% depending on down payment |

| Property condition | Stricter (FHA appraisal standards) | More flexible |

| Best for | Lower credit, limited savings | Strong credit, 20%+ down |

The real difference between FHA and conventional loans comes down to who carries the risk. With FHA, the government absorbs it. With conventional, the lender does — and they price that risk into your rate and PMI requirements.

FHA Loan vs Conventional Loan: Which One Actually Saves You More Money?

This is the question that matters most, and the honest answer is: it depends on when you’re measuring.

Short-term (0–5 years): FHA often wins for buyers with lower credit scores because the interest rate is typically lower and qualification is easier. Getting into a home sooner means building equity sooner.

Long-term (7+ years): Conventional usually wins because PMI cancels and you’re not paying MIP for the life of the loan.

Let’s run real numbers. Assume a $350,000 home purchase in 2026:

Scenario A — FHA with 3.5% down ($12,250 down):

- Loan amount: $337,750 + 1.75% upfront MIP = $343,663

- Monthly MIP: ~$235/month (0.55% annual rate for most borrowers)

- Estimated rate: ~6.5%

- Monthly P&I + MIP: ~$2,410

Scenario B — Conventional with 5% down ($17,500 down):

- Loan amount: $332,500

- PMI: ~$166/month (estimated ~0.6% for a 680 credit score)

- Estimated rate: ~7.0% (higher because of lower credit score)

- Monthly P&I + PMI: ~$2,380

Scenario C — Conventional with 20% down ($70,000 down):

- Loan amount: $280,000

- No PMI

- Estimated rate: ~6.75%

- Monthly P&I: ~$1,815

The numbers make it clear: if you have the 20% down payment, conventional wins by a wide margin. If you’re choosing between 3.5% FHA and 5% conventional with a 680 score, the gap is surprisingly small — but FHA MIP stays longer.

💡 The real money-saver nobody talks about: FHA loans are assumable. If you lock in a 6.5% rate today and rates drop to 5% in three years, the next buyer can assume your loan — making your home far more attractive to sell. That’s an extraordinary negotiating chip.

For a deeper look at how financing decisions affect your bottom line, check out our Real Estate Financing Guide: Mortgages, Credit & Down Payments 2026.

MIP vs PMI: The Mortgage Insurance Battle That Costs You Thousands

This is where most buyers get blindsided. Both FHA and conventional loans can require mortgage insurance — but they work very differently.

FHA Mortgage Insurance (MIP)

FHA loans charge two types of MIP:

- Upfront MIP (UFMIP): 1.75% of the loan amount, paid at closing or rolled into the loan.

- Annual MIP: Paid monthly. For most borrowers in 2026, this is 0.55% annually on a 30-year loan with less than 10% down.

When does FHA MIP go away?

- If you put 10% or more down, MIP cancels after 11 years.

- If you put less than 10% down, MIP stays for the life of the loan — the only way out is refinancing into a conventional loan.

Conventional PMI

PMI on a conventional loan is more flexible:

- Automatic cancellation when your loan balance hits 78% of the original purchase price (Homeowners Protection Act).

- Requested cancellation when you reach 80% LTV (loan-to-value) and can demonstrate it through payments or appreciation.

- No PMI at all if you put 20% down.

PMI rates vary based on credit score and down payment, typically ranging from 0.2% to 2% annually.

The Long-Term Math

On a $350,000 home with 3.5% down, FHA MIP over 30 years adds up to roughly $84,600 in total mortgage insurance costs. A conventional borrower with the same down payment who hits 20% equity in year 8 might pay $13,000–$16,000 in PMI total before it cancels.

That’s not a small difference. That’s a used car, a home renovation, or a serious investment account contribution.

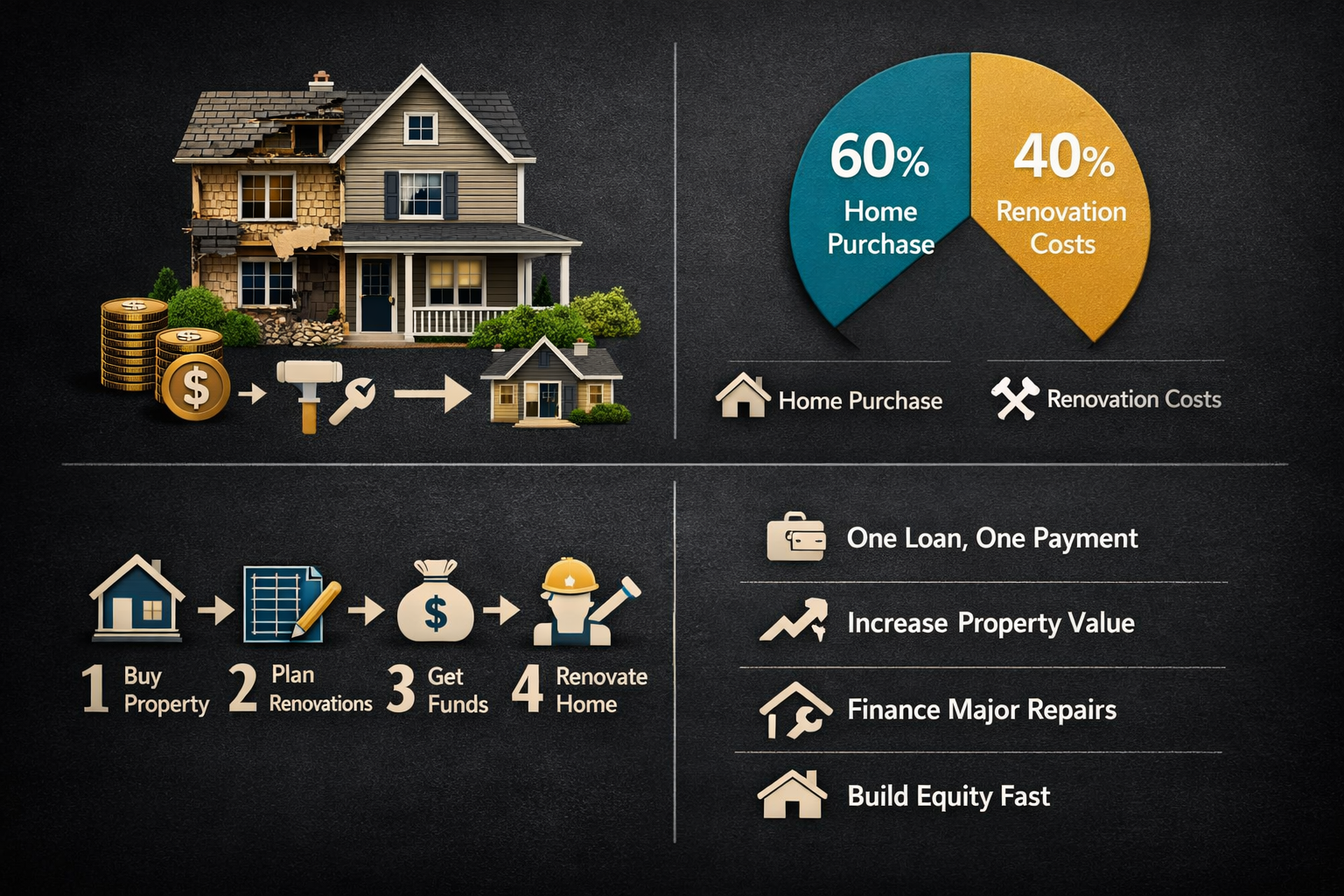

FHA 203k Renovation Loans: The Secret Weapon Most Buyers Don’t Know About

FHA doesn’t just help you buy a home — it can help you buy a fixer-upper and fund the repairs in a single loan. That’s the FHA 203k loan, and it’s genuinely one of the most underused tools in real estate.

How the FHA 203k Loan Works

The FHA 203k renovation loan wraps the purchase price and renovation costs into one mortgage. There are two versions:

Standard FHA 203k:

- For major structural repairs, additions, or renovations over $35,000

- Requires a licensed HUD consultant to oversee the work

- Minimum repair amount: $5,000

FHA 203k Streamline (Limited):

- For cosmetic repairs and non-structural upgrades under $35,000

- Simpler process, no HUD consultant required

- Great for kitchens, bathrooms, flooring, roofing

FHA 203k Loan Requirements

- Minimum credit score: 580 (most lenders prefer 620+)

- Down payment: 3.5% of the total loan amount (purchase + renovation)

- Property must be your primary residence

- Work must begin within 30 days of closing and be completed within 6 months

FHA rehab loan vs conventional renovation loans: Fannie Mae’s HomeStyle Renovation and Freddie Mac’s CHOICERenovation are the conventional equivalents — but they require higher credit scores (typically 620–680+) and stricter income documentation. For buyers with moderate credit who want to buy a fixer-upper, the FHA 203k renovation loan is often the only realistic path.

Thinking about flipping? See how renovation financing stacks up in our guide to the Best Loans for Flipping Houses in Any Market (2026 Guide).

FHA Loan Requirements by State: TX, NC, GA, TN, SC, OH, PA, MI, IN

The core FHA loan requirements are set federally — but loan limits vary by county, and some states have additional programs layered on top. Here’s what buyers need to know in 2026:

Federal FHA Loan Requirements (All States)

- Minimum credit score: 580 (3.5% down) or 500 (10% down)

- Debt-to-income ratio: Max 43% (some lenders allow up to 57% with compensating factors)

- Property must be primary residence

- FHA-approved appraisal required

- Steady employment history (typically 2 years)

State-by-State FHA Loan Limit Highlights (2026)

| State | Standard County Limit | High-Cost County Limit (where applicable) |

|---|---|---|

| Texas (FHA loan TX) | $524,225 | $805,000 (Austin-area counties) |

| North Carolina (FHA loan NC) | $524,225 | $805,000 (select counties) |

| Georgia (FHA loan GA) | $524,225 | $805,000 (Atlanta metro) |

| Tennessee (FHA loan TN) | $524,225 | Standard applies to most counties |

| South Carolina (FHA loan SC) | $524,225 | Standard applies statewide |

| Ohio (FHA loan OH) | $524,225 | Standard applies statewide |

| Pennsylvania (FHA loan PA) | $524,225 | $805,000 (Philadelphia suburbs) |

| Michigan (FHA loan MI) | $524,225 | Standard applies to most counties |

| Indiana (FHA loan IN) | $524,225 | Standard applies statewide |

Note: Loan limits are updated annually by HUD. Always verify current limits at the HUD website for your specific county.

State-specific tip: Several of these states — including Texas, Georgia, and North Carolina — have state housing finance agencies (like TDHCA, Georgia Dream, and NC Home Advantage) that offer down payment assistance programs that can be layered with FHA financing. That combination can get a buyer into a home with minimal out-of-pocket costs.

For buyers watching regional market shifts that affect what you can afford, our Spring 2026 Housing Price Shifts breakdown is worth a read.

FHA Loans for Manufactured and Modular Homes

FHA does allow loans on manufactured homes and modular homes — but the requirements are tighter than for site-built properties.

FHA loans for manufactured homes require:

- The home must be built after June 15, 1976 (HUD code compliance)

- It must be on a permanent foundation

- It must be classified as real property (not personal property/chattel)

- Minimum loan term: 20 years

- The land must be owned or leased long-term

FHA modular home loans follow similar rules. Modular homes are generally easier to finance than manufactured homes because they’re built to local building codes and typically appreciate more like site-built homes.

Conventional loans for manufactured homes exist but are even more restrictive — many lenders simply won’t touch them. FHA is often the most accessible path for manufactured home buyers, making it a genuinely fresh option in markets where land costs have pushed buyers toward alternative housing types.

Best FHA Lenders in 2026: Who’s Actually Worth Your Time

Not all FHA lenders are created equal. Rates, fees, and service quality vary significantly. Here’s a comparison of the top FHA lenders worth considering in 2026:

| Lender | Best For | Min. Credit Score | Notable Feature |

|---|---|---|---|

| Rocket Mortgage | Speed and digital experience | 580 | Fast pre-approval, strong app |

| Better Mortgage | Low fees, rate transparency | 580 | No origination fee on some products |

| New American Funding | Diverse borrowers, manual underwriting | 500 | Strong for non-traditional credit profiles |

| Guild Mortgage | First-time buyers, state programs | 540 | Pairs well with down payment assistance |

| LoanDepot | Refinancing into conventional | 580 | Good for FHA-to-conventional refi |

| Pennymac | Competitive rates | 580 | Solid for straightforward FHA purchases |

| Mr. Cooper | Existing customers, servicing | 580 | Strong loan servicing reputation |

| Guaranteed Rate | FHA 203k loans | 580 | Experienced renovation loan team |

| CrossCountry Mortgage | Flexible underwriting | 580 | Wide product range |

| Flagstar Bank | Manufactured homes | 580 | One of few lenders active in this space |

| Cardinal Financial | Tech-forward process | 580 | Strong digital tools |

So based reality check: Shopping at least 3–5 lenders before committing to an FHA loan can save you $10,000–$20,000 over the life of the loan. Lenders are not gatekeeping better rates from you — you just have to ask. Let it cook before you commit to the first pre-approval letter you receive.

For buyers who want to understand the full pre-approval process, our Fast-Track Your Homeownership with Pre-Approval & Market Trends guide walks through it step by step.

When Should You Choose Conventional Even If You Qualify for FHA?

This is the question most articles skip — and it’s where the real money decisions get made.

Choose conventional over FHA if:

- ✅ Your credit score is 700 or above — conventional rates become competitive or better

- ✅ You have 20% down — no PMI, no MIP, no contest

- ✅ You plan to stay in the home 10+ years — the permanent MIP on FHA adds up significantly

- ✅ You’re buying an investment property or second home — FHA is primary residence only

- ✅ The property doesn’t meet FHA standards — older homes with deferred maintenance often fail FHA appraisals

- ✅ You want to avoid the assumability factor — if you’re selling in a market where rates are falling, FHA assumability may not matter much

Stick with FHA if:

- ✅ Your credit score is below 660 — FHA rates will almost certainly be lower

- ✅ You have limited savings and need the 3.5% down minimum

- ✅ You’re buying a fixer-upper and want to use the FHA 203k renovation loan

- ✅ You’re in a high-rate environment and want the assumability option for future resale

- ✅ You need higher seller concession allowances (up to 6% vs. 3% on conventional)

Zero down home loan alternatives: If even 3.5% is a stretch, look at USDA loans (rural areas, zero down) and VA loans (eligible veterans, zero down). These are often better than both FHA and conventional for qualifying buyers. Down payment assistance programs in most states can also effectively create a no money down mortgage scenario when layered with FHA.

For more strategies on getting into a home with less cash upfront, our Top 7 Down Payment Strategies Ranked is an impeccable resource.

FAQ: FHA Loan vs Conventional Loan

Q: What is the minimum credit score for an FHA loan?

The FHA minimum is 500 with a 10% down payment, or 580 with a 3.5% down payment. Most lenders, however, set their own overlays and prefer 620+.

Q: Are FHA loans assumable?

Yes. FHA loans are assumable, meaning a qualified buyer can take over your existing loan and interest rate when you sell. In a high-rate environment, this is a significant selling advantage.

Q: What is the FHA loan limit in 2026?

The standard FHA loan limit for a single-family home is $524,225 in most U.S. counties. High-cost areas can reach up to $1,209,750. Limits are set by HUD annually.

Q: How does FHA mortgage insurance work?

FHA charges an upfront MIP of 1.75% of the loan amount plus an annual MIP (paid monthly). For most 30-year loans with less than 10% down, annual MIP is approximately 0.55% and does not cancel — it lasts the life of the loan.

Q: Can I use an FHA loan for a rental property?

No. FHA loans are for primary residences only. You must occupy the property within 60 days of closing and live there for at least one year.

Q: What is the FHA 203k loan?

The FHA 203k loan lets you finance both the purchase and renovation of a home in a single loan. The Standard 203k covers major structural work; the Streamline version covers cosmetic repairs under $35,000.

Q: Can I get an FHA loan with no money down?

FHA itself requires a minimum 3.5% down. But when combined with state or local down payment assistance programs, your effective out-of-pocket cost can be zero. This is the most common path to a no money down mortgage for non-veteran buyers.

Q: How does FHA compare to conventional for a first-time buyer with a 640 credit score?

At a 640 score, FHA will almost always offer a lower interest rate. The trade-off is the permanent MIP. If you plan to build equity quickly and refinance into conventional within 5–7 years, FHA can be a smart entry point.

Q: What is the difference between FHA and conventional loan appraisal requirements?

FHA appraisals are stricter. The appraiser must note health and safety issues — peeling paint, broken windows, missing handrails — and these must be repaired before closing. Conventional appraisals focus primarily on value, not condition.

Q: Can FHA loans be used for new construction?

Yes. FHA offers an FHA construction loan (FHA One-Time Close) that covers land purchase, construction, and permanent financing in a single closing. Requirements are similar to standard FHA loans.

Q: What’s the FHA Title 1 loan?

The FHA Title 1 loan is a home improvement loan for existing homeowners — not a purchase loan. It allows up to $25,000 for single-family homes without requiring equity, making it useful for repairs that don’t add enough value to qualify for a cash-out refinance.

Q: Is conventional or FHA better for buying a condo?

Both work for condos, but FHA requires the condo project to be on the FHA-approved list. Conventional is more flexible here. If the condo you want isn’t FHA-approved, conventional may be your only option.

Conclusion: Make the Smart Call for Your Situation

The FHA loan vs conventional loan debate isn’t about which loan is objectively better — it’s about which one is better for you, right now, with your specific numbers.

Here’s the impeccable bottom line:

- Credit score below 660 + limited savings? Start with FHA. Get in the door, build equity, and refinance to conventional when your credit and LTV support it.

- Credit score 700+ with 10–20% down? Run conventional numbers first. The permanent MIP on FHA will likely cost you more over time.

- Buying a fixer-upper? The FHA 203k renovation loan is one of the most underused tools in real estate. Fresh opportunity hiding in plain sight.

- Selling in the next 5–10 years in a high-rate market? FHA’s assumability is an extraordinary advantage that conventional loans simply don’t offer.

The difference between FHA and conventional loan costs can swing tens of thousands of dollars over a 30-year mortgage. That’s not a number to guess at — it’s a number to calculate with real quotes from multiple lenders.

Actionable next steps:

- Check your credit score and get a free credit report at AnnualCreditReport.com

- Get pre-qualified with at least 3 lenders from the comparison table above

- Ask each lender to show you the total cost of both FHA and conventional options side by side

- Factor in your timeline — if you’re staying 5 years or less, upfront costs matter more than long-term MIP

- Explore state-specific down payment assistance programs before assuming you need to wait to save more

Nobody should be gatekeeping this information from you. The numbers are available, the tools are free, and the right loan for your situation is absolutely findable — you just have to let it cook and do the comparison work before you sign anything.

For more on navigating the 2026 mortgage market, see our breakdown of Current Mortgage Rates February 2026 and our 15 vs 30-Year Mortgage Rates 2026: Long-Term Savings Guide.

References

- U.S. Department of Housing and Urban Development (HUD). FHA Single Family Housing Policy Handbook 4000.1. HUD, 2021. https://www.hud.gov/program_offices/housing/sfh/handbook_4000-1

- Consumer Financial Protection Bureau (CFPB). What is private mortgage insurance? CFPB, 2023. https://www.consumerfinance.gov/ask-cfpb/what-is-private-mortgage-insurance-en-1953/

- Fannie Mae. HomeReady Mortgage Guidelines. Fannie Mae, 2024. https://www.fanniemae.com/homeready

- Federal Housing Finance Agency (FHFA). FHFA Announces Conforming Loan Limit Values for 2025. FHFA, 2024. https://www.fhfa.gov/news/news-release/fhfa-announces-conforming-loan-limit-values-for-2025

- HUD. FHA Mortgage Limits. HUD, 2024. https://entp.hud.gov/idapp/html/hicostlook.cfm

- Rocket Mortgage. FHA vs. Conventional Loan: Which Is Right For You? Rocket Mortgage, 2024. https://www.rocketmortgage.com/learn/fha-vs-conventional-loan

- Consumer Financial Protection Bureau. Homeowners Protection Act — Private Mortgage Insurance Cancellation. CFPB, 2023. https://www.consumerfinance.gov/ask-cfpb/when-can-i-remove-private-mortgage-insurance-pmi-from-my-loan-en-202/

Meta Title: FHA Loan vs Conventional Loan: Which Saves More Money in 2026?

Meta Description: FHA loan vs conventional loan — full 2026 comparison covering MIP vs PMI, 203k renovation loans, state requirements, best FHA lenders, and when conventional wins.

Tags: FHA loan vs conventional loan, FHA loan requirements, mortgage insurance MIP vs PMI, FHA 203k renovation loan, conventional loan, first-time home buyer mortgage, best FHA lenders 2026, down payment strategies, FHA loan limits, home buying financing, FHA assumable loan, no money down mortgage

{kind=link}