}

Last updated: April 23, 2026

Quick Answer: A HELOC on investment property is a revolving line of credit secured by the equity in a rental or non-owner-occupied property. It works similarly to a credit card — draw what you need, repay it, and draw again — but it comes with stricter qualification standards, higher interest rates, and lower loan-to-value limits than a primary residence HELOC. For investors who qualify, it’s one of the most capital-efficient tools available for scaling a real estate portfolio without selling existing assets.

Key Takeaways

- Investment property HELOCs typically cap at 65–75% combined loan-to-value (CLTV), compared to 85–90% on a primary residence.

- Most lenders require a minimum credit score of 680–720 for an investment property HELOC, with the best rates reserved for 740+.

- Debt Service Coverage Ratio (DSCR) of at least 1.20–1.25 is standard — meaning the property’s rental income must exceed its debt payments by 20–25%.

- HELOC rates on investment properties run 1–3 percentage points higher than primary residence rates, typically prime + 1% to prime + 3% as of 2026.

- The BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) pairs naturally with investment property HELOCs to recycle capital across multiple deals.

- A HELoan (home equity loan) gives a fixed lump sum — better for investors who want predictable payments on a single large project.

- No appraisal HELOCs exist but are rare on investment properties; most lenders require a full appraisal or AVM with inspection.

- Rates vary by state — Florida, Texas, Arizona, and New Jersey each have distinct lender landscapes and rate ranges.

HELOC on Investment Property: What It Is and How It Actually Works

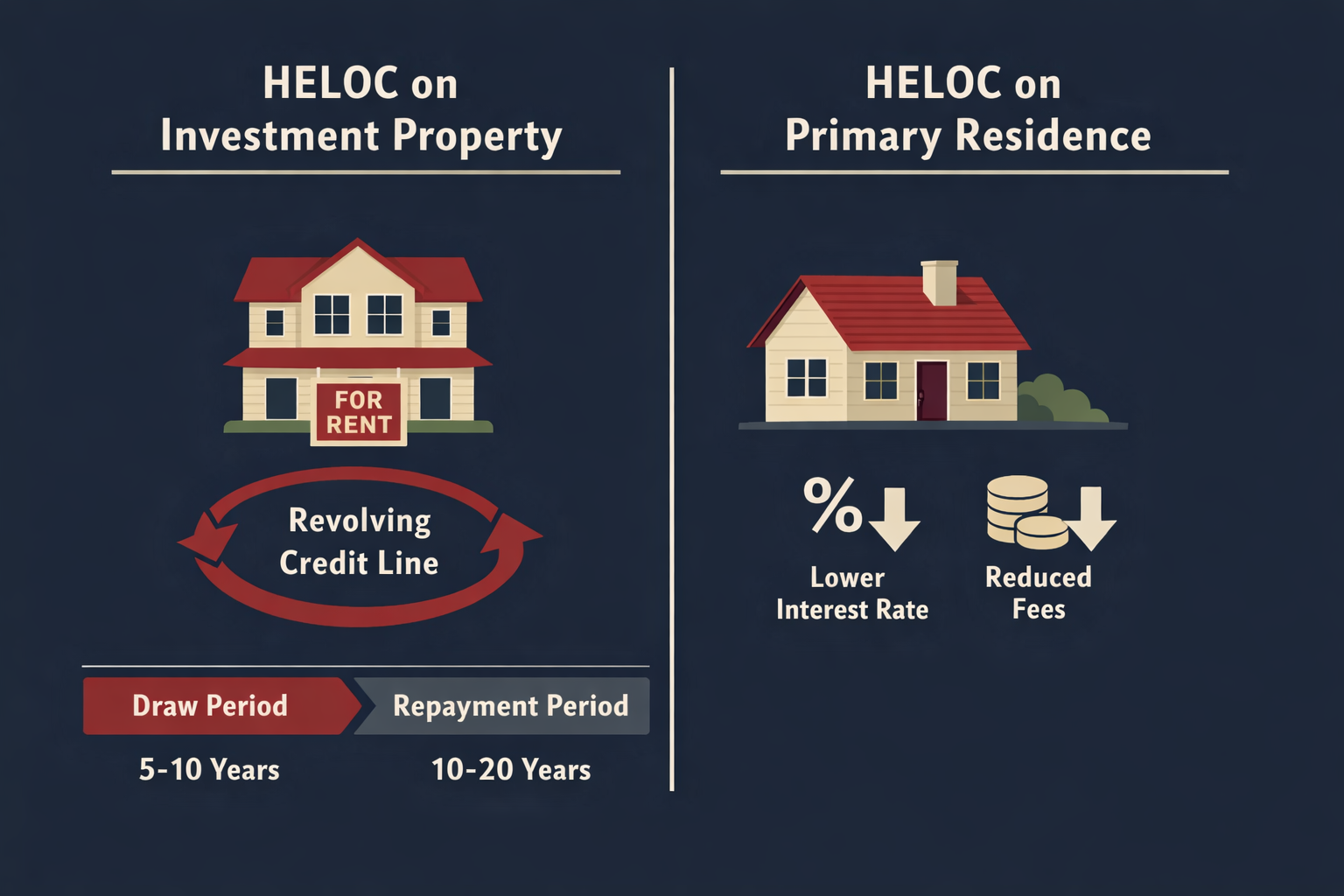

A HELOC on investment property is a home equity line of credit attached to a property you don’t live in — a rental home, duplex, small apartment building, or commercial-residential hybrid. The lender extends a credit line based on the equity you’ve built in that property, and you can draw from it during a set draw period (usually 5–10 years), repay it, and draw again.

Here’s how the mechanics break down:

- Draw period: You access funds as needed, paying interest only on what you’ve drawn (interest only HELOC structure is common during this phase).

- Repayment period: After the draw period closes, the balance converts to a fully amortizing loan — typically over 10–20 years.

- Variable rate: Most HELOCs are tied to the prime rate, so your rate moves with Federal Reserve decisions.

The critical difference from a personal loan or cash-out refinance: you’re not locked into a fixed lump sum. Draw $40,000 for a down payment on deal two, repay it from rental income, then draw again for deal three. That revolving structure is exactly why a HELOC on investment property is so attractive for active portfolio builders.

“The equity in your existing properties is often the most underused asset on an investor’s balance sheet.” — A perspective shared consistently by experienced real estate brokers and portfolio lenders.

For a deeper look at how real estate financing structures compare across different investment strategies, check out our Real Estate Financing Guide: Mortgages, Credit & Down Payments 2026.

At Real Estate Rank IQ, we break down real estate financing strategies so investors can make smarter moves with the equity they already own — and the HELOC on investment property is one of the most misunderstood tools in the game.

Investment Property HELOC vs Primary Residence HELOC: Key Differences

These two products share the same basic structure but are treated very differently by lenders. Investment property HELOCs carry more risk in a lender’s eyes — if an investor hits financial trouble, they’ll protect their primary home first, which means the investment property gets foreclosed on sooner.

| Feature | Primary Residence HELOC | Investment Property HELOC |

|---|---|---|

| Max CLTV | 85–90% | 65–75% |

| Minimum Credit Score | 620–660 | 680–720+ |

| Rate Premium | Base prime rate | Prime + 1% to Prime + 3% |

| Income Verification | Standard W-2/tax returns | Rental income + DSCR required |

| Lender Availability | Wide | Significantly narrower |

| Draw Period | 10 years (typical) | 5–10 years |

| Appraisal Required | Sometimes waived | Almost always required |

| Interest Deductibility | Limited post-2017 | Often deductible as business expense |

The tax angle is worth highlighting. On a primary residence, HELOC interest deductibility is restricted under the Tax Cuts and Jobs Act of 2017 — it’s only deductible if the funds are used to “buy, build, or substantially improve” the home. On an investment property, HELOC interest used for business purposes (property improvements, acquiring additional rentals) is generally deductible as a business expense on Schedule E. Always confirm this with a CPA who specializes in real estate.

Why Real Estate Investors Use HELOCs to Scale Their Portfolio

The short answer: speed and capital efficiency. Selling a property to fund the next one triggers capital gains taxes, resets your depreciation clock, and takes months. A HELOC on investment property lets you access equity in weeks without selling anything.

Top reasons investors tap investment property equity:

- Down payments on new acquisitions — Draw from an existing rental’s equity to fund 20–25% down on the next property.

- Renovation capital — Fund value-add improvements on a new acquisition without touching your cash reserves.

- Bridge financing — Cover gaps between a property purchase and a long-term loan closing.

- BRRRR cycling — The Buy, Rehab, Rent, Refinance, Repeat method relies heavily on recyclable credit lines.

- Deal stacking — Acquire multiple properties in a compressed timeline using a single equity line.

- Emergency reserves — Keep the line open as a liquidity buffer without paying interest until you draw.

The math is straightforward. If you own a rental property worth $400,000 with a $200,000 mortgage balance, you have $200,000 in equity. At 70% CLTV, a lender might extend a HELOC up to $80,000 ($400,000 × 70% = $280,000 − $200,000 existing mortgage = $80,000 available line). That $80,000 could be a full down payment on a $320,000–$400,000 second rental property.

For investors building a portfolio from scratch, our How to Invest in Real Estate: Beginner’s Blueprint 2026 covers the foundational strategies that make HELOC stacking possible.

HELOC Requirements for Investment Properties

This is where most investors get surprised. The bar is higher than a primary residence, and not every lender even offers this product. Here’s exactly what you need.

Minimum Credit Score Requirements

Most lenders require a 680–720 minimum FICO score for a HELOC on investment property. The best rates — and the highest available credit lines — go to borrowers at 740 and above.

- 720–739: Qualified, but expect rate premiums

- 740–759: Standard pricing, full product access

- 760+: Best available rates, maximum CLTV

A HELOC with bad credit (below 660) on an investment property is extremely difficult through conventional lenders. Hard money lenders and some credit unions may work with lower scores, but the rate premium makes the math painful. More on that in a later section.

Your HELOC credit score matters beyond just approval — every 20-point tier can shift your rate by 0.25–0.5%, which compounds significantly over a 10-year draw period.

Equity Requirements (LTV)

Standard maximum combined loan-to-value (CLTV) for an investment property HELOC is 65–75%, depending on the lender and property type.

Example calculation:

- Property value: $350,000

- Existing mortgage balance: $175,000

- Max CLTV at 70%: $350,000 × 0.70 = $245,000

- Available HELOC: $245,000 − $175,000 = $70,000

Single-family rentals typically get the best LTV treatment. Multi-unit properties (2–4 units) may see lenders drop to 65% CLTV. Five-plus unit properties generally don’t qualify for residential HELOC products at all — those require commercial lines of credit.

Debt Service Coverage Ratio (DSCR)

DSCR measures whether the property’s rental income covers its debt obligations. Most investment property HELOC lenders require a minimum DSCR of 1.20–1.25.

DSCR Formula:

DSCR = Net Operating Income ÷ Total Debt Service

If a property generates $2,500/month in rent and has $1,800/month in total debt payments (mortgage + HELOC payment), the DSCR is 2,500 ÷ 1,800 = 1.39 — well above the 1.20 threshold.

A DSCR below 1.0 means the property is cash-flow negative. No conventional lender will approve a HELOC in that scenario. For a full breakdown of DSCR loan qualification, see our DSCR Loan Requirements: What Investors Need to Qualify 2026.

Income Documentation

Lenders want to see:

- 2 years of tax returns (personal and business if applicable)

- Current lease agreements for all rental units

- 12–24 months of rental income history (bank statements or Schedule E)

- Profit and loss statements for self-employed borrowers

- Existing mortgage statements for the subject property

Some lenders offering no doc HELOC products exist in the non-QM space, but they’re rare on investment properties and typically come with significantly higher rates and lower LTV caps (often 55–60% CLTV). These products are more common for high-net-worth investors with strong asset profiles.

Property Types That Qualify

✅ Eligible:

- Single-family rentals (1 unit)

- 2–4 unit residential properties (duplex, triplex, fourplex)

- Condominiums (with warrantable condo approval)

- Townhomes used as rentals

❌ Typically ineligible for residential HELOC:

- 5+ unit apartment buildings

- Commercial properties

- Raw land

- Short-term rental properties in some markets (lender-specific)

- Properties with active code violations

Current HELOC Rates for Investment Properties

As of 2026, investment property HELOC rates are running in the 8.5%–12%+ range, depending on credit score, LTV, property type, and lender. The prime rate as of early 2026 sits around 7.5%, and most investment property HELOCs price at prime + 1% to prime + 3%.

For comparison:

- Primary residence HELOC: ~7.5%–9.5%

- Investment property HELOC: ~8.5%–12%+

- Cash-out refinance (investment): ~7.25%–8.75% fixed

- Hard money loan: ~10%–15%+

- DSCR loan: ~7.5%–9.5%

The rate gap between a primary residence HELOC and an investment property HELOC is real — but the flexibility of a revolving line often justifies the premium for active investors.

HELOC Rates by State: Florida, Texas, Arizona, New Jersey

State-specific factors — lender competition, foreclosure laws, property tax structures, and local market conditions — all influence the rates investors actually see.

HELOC Rates Florida 🌴

Florida is a judicial foreclosure state, which means lenders carry more risk and often price investment property HELOCs slightly higher. Rates in Florida for investment property HELOCs typically range from 9.0%–12.5% in 2026. Credit unions like Suncoast Credit Union and Space Coast Credit Union are worth checking — credit union HELOC rates tend to run 0.5–1% below major bank rates in competitive Florida markets.

HELOC Rates Texas 🤠

Texas has unique constitutional restrictions on home equity lending (Article XVI, Section 50(a)(6)) that historically limited HELOC products on primary residences. Investment properties in Texas operate under different rules — conventional investment property HELOCs are available at 8.75%–11.5% in 2026. Portfolio lenders and regional banks are often more active in Texas than national lenders for this product.

HELOC Rates Arizona 🌵

Arizona is a non-judicial foreclosure state, which generally means faster foreclosure timelines and slightly lower lender risk premiums. Investment property HELOC rates in Arizona tend to run 8.5%–11.0% in 2026. Phoenix and Scottsdale markets have seen strong investor activity, and several regional lenders actively compete for investment property HELOC business.

HELOC Rates New Jersey 🏙️

New Jersey is a judicial foreclosure state with one of the longest foreclosure timelines in the country — sometimes 3+ years. That risk is priced into investment property HELOCs, which typically run 9.5%–13%+ in 2026. NJ investors should compare credit union HELOC rates aggressively, as local institutions sometimes offer better terms than national banks in this market.

Best HELOC Lenders for Investment Properties (Full Comparison Table)

The lender landscape for investment property HELOCs is narrower than most investors expect. Many major banks have pulled back from this product post-2020. Here’s a current overview of active players in 2026.

| Lender | Min Credit Score | Max CLTV | Rate Range | Draw Period | Notes |

|---|---|---|---|---|---|

| Figure HELOC | 640 | 75% | 8.5%–14%+ | 5 years | Fully digital, fast funding (5 days); Figure HELOC reviews are mixed on customer service |

| PenFed Credit Union | 700 | 70% | 8.75%–11.5% | 10 years | Strong for 1–4 unit properties |

| Third Federal S&L | 720 | 65% | 8.5%–10.75% | 10 years | Conservative underwriting, low fees |

| Connexus Credit Union | 700 | 70% | 8.75%–11.0% | 10 years | Credit union HELOC rates competitive |

| TD Bank | 720 | 70% | 9.0%–12.0% | 10 years | East Coast focus, good for NJ/FL investors |

| SoFi HELOC | 680 | 70% | 8.75%–11.5% | 10 years | SoFi HELOC — no fees, digital-first |

| Local/Regional Banks | 680–720 | 65–75% | Varies | 5–10 years | Often most flexible on property types |

| Non-QM/Portfolio Lenders | 640–680 | 55–65% | 10%–14%+ | 5 years | For complex income situations |

Notable absences: USAA HELOC — USAA discontinued their HELOC product and currently does not offer home equity lines of credit. VA loan HELOC — VA loans don’t include a HELOC product; veterans can access equity through VA cash-out refinances instead.

Better HELOC — Better.com has offered HELOC products on primary residences but has limited availability for investment properties as of 2026. Check current availability directly.

Decision rule: If you need fast capital and have a clean credit profile, Figure HELOC’s digital-first process is worth exploring. If you want the lowest rate and can wait 3–6 weeks, a credit union is almost always the better play.

HELoan vs HELOC: Which Is Better for Real Estate Investors?

A HELoan (home equity loan) — also called a second mortgage — gives you a fixed lump sum at a fixed interest rate, repaid over a set term. A HELOC is a revolving line with a variable rate. Both use your investment property equity as collateral.

What is a HELoan? It’s essentially a fixed-rate second mortgage. You borrow a specific amount, get it all at once, and make equal monthly payments over 5–30 years.

| Factor | HELoan | HELOC |

|---|---|---|

| Disbursement | Lump sum | Draw as needed |

| Rate type | Fixed | Variable (usually) |

| Best for | Single large project | Multiple deals over time |

| Payment structure | Principal + interest from day 1 | Interest-only during draw |

| Predictability | High | Lower (rate fluctuates) |

| Flexibility | Low | High |

| Closing costs | Higher (similar to mortgage) | Lower to none |

Choose a HELoan if:

- You have one specific project with a defined cost (e.g., a full gut renovation)

- You want payment certainty and can’t absorb rate risk

- You’re in a rising rate environment and want to lock in now

Choose a HELOC if:

- You’re actively acquiring multiple properties

- You want to draw, repay, and redraw across different deals

- You can manage variable rate exposure through strong cash flow

Home equity line of credit vs home equity loan — the winner depends entirely on your investment timeline and risk tolerance. Most active portfolio builders prefer the HELOC for its flexibility.

How Investors Use a HELOC to Fund the Next Deal

The BRRRR Method and HELOC Stacking

The BRRRR method — Buy, Rehab, Rent, Refinance, Repeat — is the strategy that pairs most naturally with a HELOC on investment property. Here’s the cycle:

- Buy a distressed property using HELOC funds as the down payment (or full purchase on cheaper markets)

- Rehab the property using additional HELOC draws

- Rent it out to generate cash flow and build DSCR

- Refinance with a long-term DSCR loan or conventional mortgage, pulling equity back out

- Repeat — use the refinance proceeds to repay the HELOC, then draw again for the next deal

The HELOC becomes a permanent capital recycling tool. Each deal replenishes the line, and the investor never has to sell an asset to fund the next acquisition. So based — this is exactly how experienced investors build portfolios of 10, 20, or 30 properties without raising outside capital.

For more on investment strategies that pair with this approach, explore our 4 Types of Real Estate Investments: Complete 2026 Guide.

Using a HELOC as a Down Payment

Drawing from a HELOC on investment property to fund a down payment on a new acquisition is one of the most common use cases. The key consideration: the new lender needs to know about the HELOC.

Most conventional lenders will count the HELOC payment in your debt-to-income ratio calculation, which can affect how much you qualify for on the new loan. DSCR lenders, who qualify based on property income rather than personal DTI, are often more flexible here.

Quick example:

- HELOC draw: $75,000 at 9.5% (interest-only = ~$594/month)

- New property purchase price: $300,000

- Down payment: $75,000 (25%)

- New DSCR loan: $225,000 at 8.0%

- Monthly rent on new property: $2,400

- Total debt service on new property: ~$1,651 + $594 HELOC = $2,245

- DSCR: 2,400 ÷ 2,245 = 1.07 (tight, but workable)

Funding Renovations Without Refinancing

Cash-out refinancing in a high-rate environment means replacing a lower-rate existing mortgage with a new, higher-rate loan on the entire balance. That’s expensive. A HELOC on investment property lets investors fund renovations without touching the first mortgage.

If you have a 4.5% fixed mortgage from 2021 and need $60,000 for a kitchen-and-bath renovation to push rents up by $400/month, a HELOC at 9.5% on just that $60,000 costs far less than refinancing the entire mortgage balance at 8%+.

This is one of the most impactful — and most gate-kept — strategies in real estate investing. Now you know.

No Appraisal HELOC and No Doc HELOC: Are They Real?

Short answer: They exist, but they’re rare and come with tradeoffs on investment properties.

A no appraisal HELOC uses an Automated Valuation Model (AVM) — essentially an algorithm that estimates property value using comparable sales data — instead of a full in-person appraisal. Some lenders offer this on primary residences with strong equity positions. On investment properties, most lenders still require a full appraisal or at minimum a drive-by appraisal with an AVM.

Why it matters: A full appraisal on an investment property typically costs $400–$800 and takes 2–4 weeks. No appraisal HELOCs can close significantly faster.

Figure HELOC is one of the few lenders advertising a streamlined process that may use AVM on qualifying properties — their 5-day funding claim is built partly on this. Results vary by property type and location.

A no doc HELOC — where income documentation is minimal or waived — exists primarily in the non-QM lending space. These products typically require:

- 700+ credit score

- Strong equity position (55–65% max CLTV)

- Significant liquid assets

- Rate premiums of 2–4% above standard products

For investors with complex income structures (multiple LLCs, large depreciation write-offs that suppress taxable income), no doc HELOC products can be worth exploring — but run the numbers carefully against the rate premium.

HELOC With Bad Credit: What Are Your Options?

A HELOC with bad credit on an investment property is genuinely difficult. Here’s a realistic breakdown:

Credit score 660–679: A small number of portfolio lenders and credit unions will work in this range, but expect:

- Maximum CLTV of 60–65%

- Rate premiums of 1–2% above standard pricing

- Additional asset verification requirements

Credit score 620–659: Conventional investment property HELOCs are largely unavailable. Options include:

- Hard money second liens — expensive (12–15%+) but fast

- Private lenders — relationship-based, terms vary widely

- Seller financing — negotiate equity access directly with a property seller

- Business line of credit — if your rental operation is structured as an LLC with revenue history

Equity loans with poor credit are possible but rarely cost-effective. The better play is usually to spend 6–12 months improving the credit score before applying. Paying down revolving balances, disputing errors, and avoiding new credit inquiries can move a score from 640 to 700+ within a year.

Let it cook before you see results — credit improvement is a slow process, but the rate savings on a $100,000 HELOC line are worth the wait.

How to Refinance a HELOC When Rates Drop

Refinancing a HELOC (refi HELOC) means replacing your existing line with a new one at better terms. This is worth doing when rates drop significantly or when your property has appreciated enough to qualify for a larger line.

Options for refinancing a HELOC:

- New HELOC with a different lender — Pay off the existing line and open a new one. Watch for prepayment penalties on the original HELOC (typically triggered if you close within 2–3 years).

- Convert to a HELoan — Lock in a fixed rate on the outstanding balance, eliminating variable rate exposure.

- Cash-out refinance — Refinance the first mortgage and HELOC into a single new loan. Only makes sense if the new rate is competitive with your existing first mortgage rate.

- Refinancing and home equity loans — Some lenders offer combo products that consolidate first and second liens.

How soon can you do a HELOC after purchasing a home (or investment property)? Most lenders require you to have owned the property for at least 6–12 months before they’ll approve a HELOC. Some portfolio lenders will go as short as 3 months with strong equity documentation. The “seasoning” requirement exists because lenders want to see a stable ownership history before extending a second lien.

HELOC Risks Every Investor Needs to Understand Before Drawing

A HELOC on investment property is a powerful tool — and a genuinely dangerous one if the market shifts or cash flow dries up. These are the risks that don’t get enough attention.

1. Variable Rate Exposure

Most HELOCs are tied to the prime rate. If rates rise 2% during your draw period, your interest cost on a $100,000 balance jumps from ~$9,500/year to ~$11,500/year. That’s $2,000 in additional annual carrying cost that comes directly out of cash flow.

2. Property Value Decline

If your investment property drops in value, lenders can freeze or reduce your HELOC line — even if you’ve never missed a payment. This happened widely during 2008–2010 and can happen again. Don’t build a business plan that depends on a HELOC line staying open indefinitely.

3. Overleveraging

Using a HELOC to fund down payments on multiple properties simultaneously creates a layered debt structure. If one property goes vacant or needs major repairs, the cash flow from other properties has to cover the HELOC payment. Stress-test your portfolio for 2–3 months of vacancy on any single property.

4. Draw Period Ending

When the draw period closes, the HELOC converts to a repayment-only phase. Monthly payments increase significantly because you’re now paying both principal and interest. Plan for this transition — don’t get caught with a large balance when the draw period ends.

5. Cross-Collateralization Risk

If the HELOC lender and your first mortgage lender are the same institution, a default on one product can trigger action on both. Keep your first mortgage and HELOC with separate lenders where possible.

6. Tax Law Changes

The deductibility of investment property HELOC interest depends on how funds are used and current tax law. Always work with a CPA who understands real estate investment taxation before drawing.

For a broader look at how economic conditions affect investment property performance, our article on How the Economy Shapes Real Estate Prices & Demand 2026 is worth reading before you draw.

Frequently Asked Questions

What is a HELOC for investment properties?

A HELOC for investment property is a revolving line of credit secured by the equity in a non-owner-occupied property — such as a rental home, duplex, or small apartment building. The borrower can draw funds, repay them, and draw again during the draw period, typically 5–10 years. It functions like a credit card backed by real estate equity.

How do I qualify for a HELOC on a rental property?

To qualify for a HELOC on a rental property, you generally need a minimum credit score of 680–720, at least 25–35% equity in the property (max 65–75% CLTV), a DSCR of 1.20 or higher, 2 years of tax returns, and current lease agreements showing rental income. The property must be 1–4 units and in good condition.

What is the minimum credit score for an investment property HELOC?

Most lenders require a minimum FICO score of 680–720 for a HELOC on investment property. Borrowers with scores above 740 access the best rates and highest credit limits. Scores below 660 make conventional approval very difficult.

How does a HELOC work on an investment property?

The lender approves a maximum credit line based on your property’s equity. During the draw period (typically 5–10 years), you access funds as needed and pay interest only on what you’ve drawn. After the draw period, the balance converts to a fully amortizing repayment loan over 10–20 years.

What is the difference between a HELoan and a HELOC?

A HELoan (home equity loan) provides a fixed lump sum at a fixed interest rate, repaid in equal monthly installments. A HELOC is a revolving credit line with a variable rate — you draw and repay as needed. HELoans offer payment predictability; HELOCs offer flexibility.

How long does it take to get a HELOC on an investment property?

The typical timeline is 3–6 weeks from application to funding for a conventional investment property HELOC. Digital-first lenders like Figure HELOC advertise 5-day funding on qualifying applications. Complex income situations or appraisal delays can extend the timeline to 8–10 weeks.

Can I use a HELOC on investment property as a down payment for another property?

Yes. Drawing from a HELOC on investment property to fund a down payment on a new acquisition is one of the most common investor strategies. The new lender will factor the HELOC payment into your debt-to-income or DSCR calculation, so ensure the new property’s rental income supports the combined debt load.

Are HELOC interest payments tax-deductible on investment properties?

HELOC interest on investment properties is generally deductible as a business expense on Schedule E when the funds are used for business purposes — property improvements, acquisitions, or operating expenses. This is different from primary residence HELOC rules. Consult a real estate CPA to confirm based on your specific situation and current tax law.

What happens when my investment property HELOC draw period ends?

When the draw period ends, the HELOC enters the repayment phase. You can no longer draw funds, and the outstanding balance converts to a fully amortizing loan — meaning monthly payments increase because you’re now paying both principal and interest. Plan for this transition by either paying down the balance during the draw period or refinancing before the conversion.

Can I get a HELOC on an investment property with bad credit?

It’s extremely difficult through conventional lenders. Borrowers with scores below 660 may find options through hard money lenders, private lenders, or non-QM portfolio lenders — but rates will be significantly higher (often 12–15%+) and LTV caps lower (55–60%). Improving your credit score before applying is almost always the better financial decision.

Conclusion: The Extraordinary Power of Equity — Used Correctly

A HELOC on investment property is one of the most impactful financing tools available to real estate investors in 2026 — when used with discipline and a clear exit strategy. The ability to draw, repay, and redraw equity across multiple deals without selling existing assets is genuinely extraordinary. It’s the kind of strategy that separates investors building 3-property portfolios from those building 30-property portfolios.

But the risks are real. Variable rates, overleveraging, and draw period transitions have caught plenty of investors off guard. The investors who use HELOCs successfully treat the credit line as a short-term bridge — not a permanent financing solution — and always ensure the underlying property cash flow can absorb the additional debt service.

Your next steps:

- Pull your credit report and verify your score across all three bureaus before approaching lenders.

- Calculate your current CLTV on any investment properties you own to estimate available equity.

- Run your DSCR on each property to confirm you meet the 1.20+ threshold.

- Compare at least 3 lenders — include a credit union, a digital lender, and a regional bank.

- Talk to a real estate CPA about the tax implications before drawing.

- Build a draw-and-repay plan before you access any funds.

At Real Estate Rank IQ, we’re committed to giving investors the impeccable, no-gatekeeping financial education that most platforms charge for. The equity in your rental portfolio is already working for you through appreciation — make sure it’s also working for your next acquisition.

For more on building a real estate investment portfolio with smart financing, explore our investment property news and strategy coverage and our full real estate investment strategies hub.

{kind=link}