Last updated: May 24, 2026

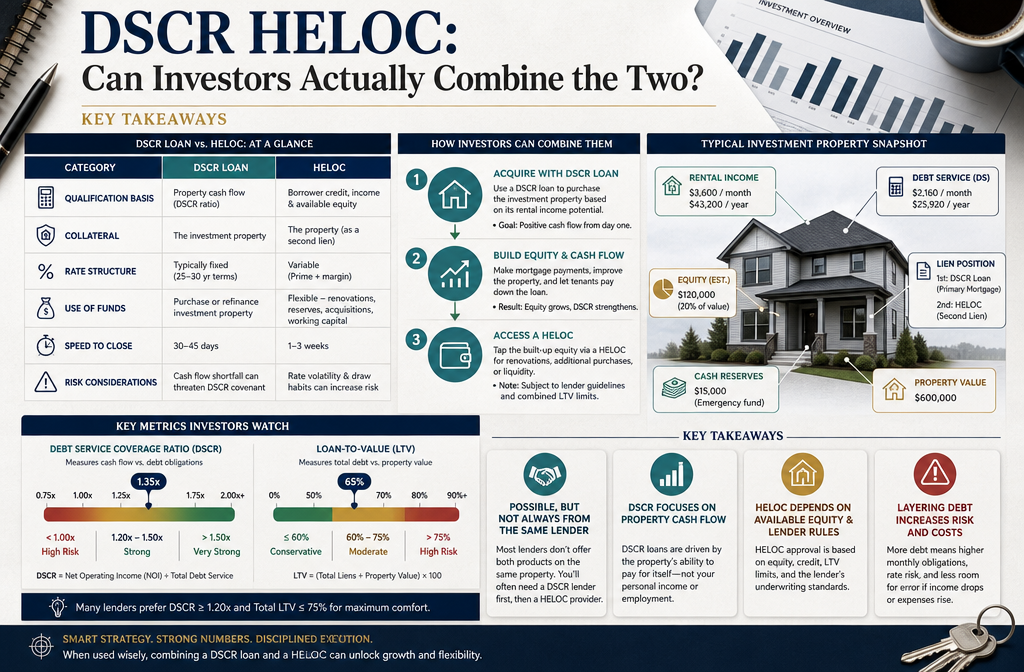

Quick Answer: Yes, investors can combine DSCR and HELOC products — but it's not as straightforward as walking into your local bank and asking for one. A DSCR HELOC is a non-QM equity line on an investment property that qualifies borrowers based on the property's rental income rather than personal income. These products exist, they're growing in 2026, and for the right investor, they're an extraordinary tool. The catch? Not every lender offers them, the rates run higher than traditional HELOCs, and you need to know exactly what you're walking into before you sign anything.

Key Takeaways

- A DSCR HELOC uses rental income — not your W-2 or tax returns — to qualify for an equity line on an investment property.

- Most lenders require a minimum DSCR of 1.0 to 1.25 and a credit score of at least 620 to 680, depending on the lender.

- Interest rates on DSCR HELOCs typically run 8% to 12% in 2026, higher than traditional HELOCs due to the non-QM risk profile.

- Borrowers can generally access 65% to 80% combined loan-to-value (CLTV), meaning the equity in your rental property determines your borrowing ceiling.

- These products are offered primarily by non-QM lenders and specialty mortgage companies, not traditional banks.

- DSCR HELOCs work best for investors who are self-employed, have complex tax returns, or own multiple rental properties.

- The biggest risk is a rental income drop — if your DSCR falls below the lender's threshold, you could face a credit freeze or loan call.

- Using a DSCR HELOC for renovations on rental properties is one of the most common and effective use cases.

- Always run the numbers on your debt service coverage ratio before applying — lenders will, and you should too.

- Compare DSCR equity products against traditional investment property loans and cash-out refinances before committing.

What Exactly Is a DSCR HELOC and How Does It Work?

A DSCR HELOC is a home equity line of credit on an investment property where qualification is based on the property's debt service coverage ratio — not the borrower's personal income. Instead of submitting pay stubs and W-2s, the lender looks at whether the rental income from the property covers the debt payments.

Here's the core formula every investor needs to know:

DSCR = Gross Rental Income ÷ Total Monthly Debt Obligations

So if a rental property brings in $3,000 per month and the total monthly debt (mortgage, taxes, insurance, HOA) is $2,400, the DSCR is 1.25. Most lenders want to see a DSCR of at least 1.0, meaning the income at minimum covers the debt. Stronger applications show 1.25 or higher.

The HELOC component works like a revolving line of credit secured by the equity in your investment property. You draw funds as needed, pay interest on what you use, and repay over a set draw period — typically 5 to 10 years — followed by a repayment period.

Why this matters for investors: Traditional HELOCs require income verification through tax returns and W-2s. Self-employed investors, those who write off significant expenses, or anyone with multiple LLCs often show low taxable income on paper — even when their properties are cash-flowing well. A DSCR HELOC sidesteps that problem entirely by letting the property's income do the talking.

"The property qualifies. Not you." — That's the entire pitch of DSCR equity products, and for the right borrower, it's so based.

DSCR HELOC: Can Investors Actually Combine the Two?

This is the question that keeps showing up in investor forums, Facebook groups, and late-night YouTube rabbit holes — and the answer is yes, with some important context.

The DSCR HELOC: Can Investors Actually Combine the Two? question really comes down to whether your specific property and financial profile meet the non-QM lending criteria that these products require. Traditional mortgage lenders don't offer this product. You won't find it at Chase or Wells Fargo. But the non-QM lending space — which has seen significant DSCR loan growth in 2026 — has made these products more accessible than they were even two years ago.

Here's what combining DSCR and HELOC actually looks like in practice:

- Step 1: You own a rental property with significant equity (typically 20-35% equity minimum after the HELOC is factored in).

- Step 2: The property generates rental income that covers its own debt service at a ratio of 1.0 or higher.

- Step 3: You apply with a non-QM lender who offers DSCR equity products — no income docs, no employment verification required.

- Step 4: The lender orders an appraisal, verifies the lease agreements, and underwrites based on the property's cash flow.

- Step 5: You receive a revolving credit line that you can draw from for renovations, down payments on additional properties, or operating reserves.

The key distinction: this is not a DSCR loan (which is a first mortgage) and it's not a traditional HELOC (which requires personal income verification). It's a hybrid product sitting in the non-QM HELOC space, and it's genuinely fresh territory for many investors.

For a deeper look at how DSCR loans work as standalone products, check out our guide on DSCR loan requirements for investors.

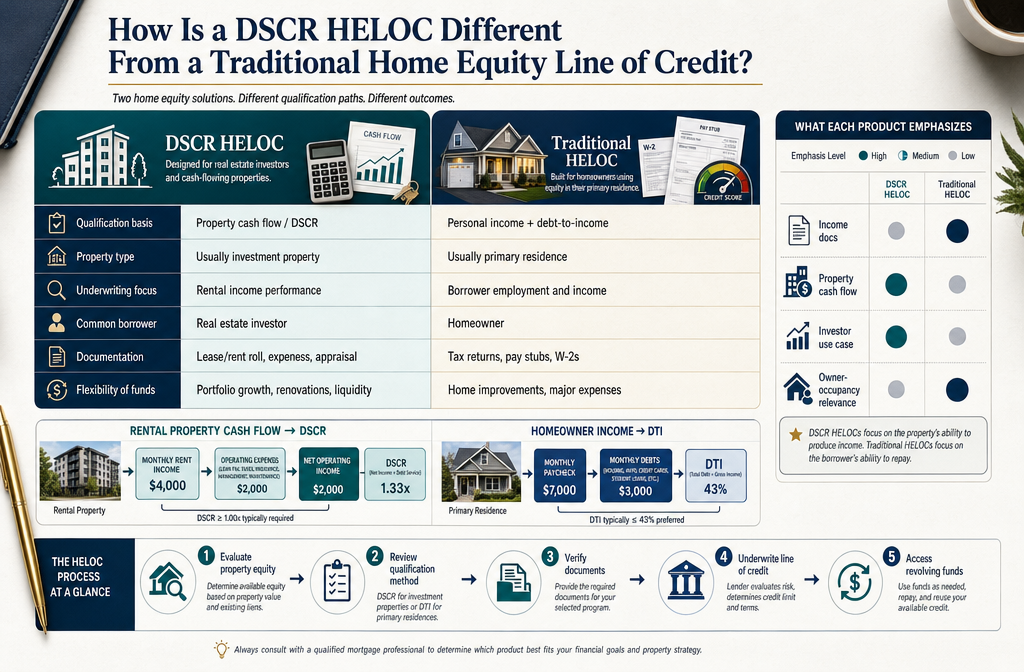

How Is a DSCR HELOC Different From a Traditional Home Equity Line of Credit?

The difference is significant. A traditional HELOC qualifies you based on your personal income, credit score, and debt-to-income ratio. A DSCR HELOC qualifies the property based on its rental income coverage ratio.

| Feature | Traditional HELOC | DSCR HELOC |

|---|---|---|

| Qualification basis | Personal income (W-2, tax returns) | Property rental income (DSCR ratio) |

| Income docs required | Yes — pay stubs, tax returns | No — lease agreements and rent rolls |

| Property type | Primary residence or second home | Investment property |

| Typical credit score | 620–700+ | 620–700+ |

| Interest rate range | 7%–9% (2026 estimates) | 8%–12% (2026 estimates) |

| Max CLTV | 80%–90% | 65%–80% |

| Lender type | Traditional banks, credit unions | Non-QM lenders, specialty lenders |

| DTI requirement | Yes (typically under 43–45%) | Not typically required |

| Self-employed friendly | Limited | Yes |

The DSCR HELOC vs traditional HELOC comparison comes down to one thing: who is being underwritten. Traditional HELOCs underwrite the borrower. DSCR HELOCs underwrite the asset.

This is why the product is so impeccable for investors who have built strong rental portfolios but show modest taxable income after depreciation and expense deductions. The property's performance is the application.

One more critical difference: traditional HELOCs are widely available. DSCR HELOCs are specialty products. You're not going to find them by Googling "HELOC near me." You'll need to work with non-QM lenders or mortgage brokers who specialize in investor financing. Our breakdown of HELOC on investment property strategies covers the broader landscape if you want context before you start shopping lenders.

What Credit Score Do I Need to Qualify for a DSCR HELOC?

Most DSCR HELOC lenders require a minimum credit score of 620 to 680, with better rates available at 700 and above. The credit score requirement is lower than you might expect because the property's income is doing most of the heavy lifting in the underwriting process.

That said, credit score still matters — here's how it typically breaks down:

- 620–659: Possible approval, but expect higher rates and stricter DSCR requirements (often 1.25+ minimum).

- 660–699: Standard approval range for most non-QM HELOC products. Rates improve noticeably.

- 700–739: Strong profile. Better rates, more lender options, potentially higher CLTV allowed.

- 740+: Best rates available. Some lenders may allow up to 80% CLTV at this range.

Common mistake: Investors assume that because a DSCR product doesn't require income docs, credit score doesn't matter. It absolutely does. A 620 score with a 1.0 DSCR is a much harder approval than a 700 score with a 1.35 DSCR.

Edge case: If you have a thin credit file (not bad credit, just limited history), some non-QM lenders will work with alternative credit data. This is worth asking about directly.

What Are the Typical Interest Rates for DSCR HELOCs?

DSCR HELOC rates in 2026 generally range from 8% to 12%, with most borrowers landing somewhere in the 9% to 11% range depending on credit score, DSCR ratio, property type, and lender.

These rates run higher than traditional HELOCs for a straightforward reason: non-QM products carry more perceived risk for lenders, and that risk premium shows up in the rate. You're essentially paying for the flexibility of not having to document personal income.

What moves your rate:

- Credit score (biggest factor after DSCR)

- DSCR ratio — a 1.35 DSCR will get better pricing than a 1.05

- Property type — single-family rentals typically get better rates than multi-unit or short-term rentals

- Loan-to-value — lower LTV means lower rate

- Lender competition — shopping multiple non-QM lenders can save you 0.5% to 1.5%

Rate reality check for 2026: The broader interest rate environment has kept non-QM rates elevated. Investors who locked in DSCR equity products in 2021 or 2022 got significantly better pricing. If you're entering the market now, factor the current rate environment into your cash flow projections before drawing on any equity line. Our article on how the economy shapes real estate prices and demand gives useful context on where rates are heading.

What Documents Do I Need to Apply for a DSCR HELOC?

The document list for a DSCR HELOC is significantly shorter than a traditional mortgage application — that's part of the appeal. No-doc or low-doc doesn't mean no paperwork, though. Here's what most lenders will ask for:

Required in most cases:

- Current lease agreements for the subject property

- 12-month rental history or rent roll (for multi-unit properties)

- Most recent mortgage statement for the property

- Property insurance declaration page

- Recent property tax statement

- Credit authorization

- Property appraisal (ordered by the lender)

Sometimes required:

- Entity documents if the property is held in an LLC or trust

- 2-3 months of bank statements (to verify rental deposits are actually being received)

- Short-term rental income history (for Airbnb/VRBO properties — lenders often use 75% of gross income for these)

What you typically do NOT need:

- W-2s or pay stubs

- Personal tax returns

- Employment verification

- Debt-to-income documentation

This is the no doc HELOC advantage in practice. For self-employed investors or those with complex financial structures, this streamlined process is genuinely extraordinary compared to the traditional mortgage gauntlet.

Pro tip: Have your lease agreements and rent rolls organized and current before you apply. Lenders move faster when the income documentation is clean and verifiable.

What Are the Biggest Risks of Using a DSCR HELOC for Investment Property?

The biggest risk is straightforward: if your rental income drops, your DSCR falls — and that can trigger a credit freeze, a loan call, or force you into a difficult refinance. DSCR HELOCs are tied to property performance, and property performance can change.

The major risks, ranked:

Vacancy risk. An empty property has a DSCR of zero. If a lender reviews your account during an extended vacancy, they may freeze your draw access.

Rate risk. Most DSCR HELOCs carry variable rates. If rates rise significantly, your monthly interest payments on drawn funds increase — which can compress your cash flow on the property itself.

Overleveraging. Using a HELOC to fund more acquisitions is smart until it isn't. If multiple properties face headwinds simultaneously, a highly leveraged portfolio can unravel quickly.

Lender-specific risks. Non-QM lenders have different policies around draws, freezes, and reviews than traditional banks. Read the fine print on what triggers a review of your line.

Market value drops. If property values decline, your CLTV could exceed the lender's threshold, resulting in a reduced credit line or a freeze.

What happens if rental income drops? This is the question every investor needs to answer before signing. Most lenders include language allowing them to reduce or suspend draw access if the property's DSCR falls below the minimum. Some lenders do annual reviews. Others only check at origination. Know which type you're dealing with.

The best defense is maintaining a cash reserve — ideally 3 to 6 months of debt service — so that a temporary vacancy doesn't cascade into a financial crisis. Our guide on how to analyze a rental property before you buy covers the stress-testing framework you need before taking on any additional leverage.

How Much Can I Borrow With a DSCR HELOC?

The borrowing limit on a DSCR HELOC is determined by the combined loan-to-value (CLTV) the lender allows, which typically ranges from 65% to 80% of the property's appraised value.

Example calculation:

- Property appraised value: $500,000

- Existing mortgage balance: $280,000

- Lender allows 75% CLTV: $500,000 × 0.75 = $375,000

- Maximum HELOC line: $375,000 − $280,000 = $95,000

So in this scenario, the investor could access up to $95,000 as a revolving line of credit.

Factors that affect your borrowing ceiling:

- Property type (single-family vs. multi-unit vs. short-term rental)

- Credit score (higher score = higher CLTV allowed by some lenders)

- DSCR ratio (stronger cash flow = more flexibility)

- Lender guidelines (non-QM lenders vary significantly here)

- State regulations (some states cap HELOCs or have specific disclosure requirements)

Can investors use a DSCR HELOC for multiple properties? Yes — but each property is evaluated separately. You can have a DSCR HELOC on Property A and a separate one on Property B, as long as each property qualifies on its own DSCR. Some lenders cap the number of financed properties an investor can have, so check that threshold early.

Are There Any Lenders That Specialize in DSCR HELOCs for Investors?

Yes, but this market is dominated by non-QM lenders and specialty mortgage companies, not traditional banks. The DSCR HELOC space in 2026 includes a growing number of lenders who have built investor-specific equity products.

Where to find DSCR HELOC lenders:

- Non-QM wholesale lenders — Companies like Deephaven Mortgage, Angel Oak Mortgage, and Visio Lending have historically offered DSCR equity products. Always verify current product availability directly.

- Specialty investment property lenders — Firms that focus exclusively on investor financing often have HELOC products built around DSCR qualification.

- Mortgage brokers — This is often the most efficient path. A broker who specializes in non-QM investor loans can shop your scenario to multiple lenders simultaneously. Our comparison of mortgage broker vs. direct lender options breaks down when each approach makes more sense.

- Private lenders and hard money shops — Some offer equity lines with DSCR-style qualification, though terms vary wildly and rates can be significantly higher.

What to ask any lender before applying:

- Do you offer a HELOC specifically on non-owner-occupied investment properties?

- Do you qualify based on DSCR rather than personal income?

- What is your minimum DSCR requirement?

- What is your maximum CLTV for investment property equity lines?

- Do you conduct annual reviews that could affect my draw access?

For a curated list of lenders currently active in this space, our best HELOC lenders for investment property guide and best DSCR loan lenders for investment properties are solid starting points. Don't gatekeep yourself from shopping — the rate differences between lenders on these products can be substantial.

Can I Use a DSCR HELOC to Renovate Rental Properties?

Absolutely — and this is one of the most effective use cases for a DSCR HELOC. Using equity from one property to renovate another (or the same property) is a classic wealth-building move that experienced investors have been running for years.

Common renovation use cases:

- Updating kitchens and bathrooms to justify higher rents

- Converting single-family homes into multi-unit properties (where local zoning allows)

- Adding ADUs (accessory dwelling units) to increase income

- Bringing deferred maintenance current to improve DSCR on another property

- Repositioning a property from long-term to short-term rental

Why a DSCR HELOC works well for renovations: The revolving nature of the credit line means you draw only what you need, when you need it. You're not paying interest on $80,000 if you only spend $40,000 on the renovation. This is more capital-efficient than a cash-out refinance, which gives you a lump sum and starts charging interest immediately on the full amount.

The RERIQ take: Let it cook before you see results. Renovation-driven rent increases take time to materialize in your DSCR. Don't draw the full line, renovate, and immediately expect the new rent to cover the increased debt service overnight. Build a runway.

Are DSCR HELOCs Better Than Traditional Investment Property Loans?

DSCR HELOCs and traditional investment property loans serve different purposes — comparing them is like comparing a Swiss Army knife to a hammer. Both are useful, but for different jobs.

Choose a DSCR HELOC if:

- You already own a rental property with significant equity

- You need flexible, revolving access to capital (not a lump sum)

- You're self-employed or have complex income documentation

- You want to fund renovations or a down payment on a new acquisition

- You don't want to disturb your existing first mortgage rate

Choose a traditional investment property loan (or DSCR first mortgage) if:

- You're purchasing a new property

- You need a large lump sum and don't need revolving access

- You want the lowest possible rate (first mortgages typically price better than HELOCs)

- You have strong W-2 income and can qualify conventionally

DSCR vs HELOC for investors — the real comparison: A DSCR loan is a first mortgage. A DSCR HELOC is a second lien. They're not competing products — they're often used together. An investor might have a DSCR first mortgage on a property and layer a DSCR HELOC on top to access equity without refinancing.

For investors building a portfolio, understanding the full real estate financing landscape is non-negotiable. Know your tools.

What Are Common Mistakes Investors Make With DSCR HELOCs?

The most common mistake is treating a DSCR HELOC like free money. It's not. It's leveraged capital secured by your property, and it comes with real consequences if mismanaged.

The top mistakes, straight up:

Not stress-testing the DSCR. Investors apply based on current rents and current rates, but don't model what happens if rents drop 10% or vacancy hits 90 days. Run the downside scenario before you sign.

Ignoring the variable rate risk. Many DSCR HELOCs are variable rate products. If rates move up significantly, your drawn balance gets more expensive. Model your payments at current rate + 2%.

Using HELOC funds for non-income-producing expenses. Drawing on your investment property equity to fund personal expenses or speculative investments is a fast track to overleveraging.

Not reading the draw and freeze provisions. Some lenders have aggressive review clauses. Know exactly what triggers a freeze on your line before you depend on it.

Applying with the wrong lender. Going to a traditional bank for a DSCR HELOC wastes time. Work with non-QM specialists from the start.

Skipping the accounting. Once you're drawing on a HELOC, tracking interest, draws, and repayments becomes critical. Using dedicated accounting software for real estate investors keeps your books clean and your tax position optimized.

Confusing DSCR HELOC qualification with DSCR loan qualification. The underwriting criteria overlap but aren't identical. A lender who approved your DSCR first mortgage may have different standards for an equity line product.

FAQ: DSCR HELOC Questions Investors Actually Ask

Q: Can I get a DSCR HELOC on a property held in an LLC?

A: Yes — many non-QM lenders specifically accommodate LLC-held properties. You'll need to provide entity documents and may need a personal guarantee depending on the lender.

Q: Is a DSCR HELOC the same as a no-doc HELOC?

A: They overlap significantly. A DSCR HELOC is a type of no-doc or low-doc HELOC where the property's income — not your personal income — drives qualification. Not all no-doc HELOCs use DSCR methodology, so confirm the underwriting approach with your lender.

Q: What DSCR ratio do I need to qualify?

A: Most lenders require a minimum DSCR of 1.0 to 1.25. A ratio of 1.25 or higher gives you the best shot at approval and better pricing.

Q: Can I use a DSCR HELOC as a down payment on another investment property?

A: Yes, and this is one of the most popular use cases. Using equity from one property to fund the down payment on another is a core portfolio-scaling strategy.

Q: How long does it take to get approved for a DSCR HELOC?

A: Expect 3 to 6 weeks from application to funding, though some specialty lenders can move faster. The appraisal is typically the longest part of the process.

Q: Are DSCR HELOCs available in all states?

A: Not necessarily. Some states have restrictions on second-lien products or specific HELOC regulations. Texas, for example, has historically had strict home equity lending rules. Verify availability in your state with the lender before applying.

Q: What happens to my DSCR HELOC if I sell the property?

A: The HELOC must be paid off at closing, just like any other lien. Make sure to factor the outstanding balance into your net proceeds calculation when evaluating a sale.

Q: Can I get a DSCR HELOC on a short-term rental property?

A: Some lenders will, but they often apply a haircut to the income — typically using 75% of gross short-term rental revenue rather than 100%. Expect stricter scrutiny and potentially higher rates.

Q: Is the interest on a DSCR HELOC tax deductible?

A: For investment properties, interest on a HELOC used for business purposes (renovations, property improvements) is generally deductible. Consult a tax professional for your specific situation.

Q: How is a DSCR HELOC different from a cash-out refinance?

A: A cash-out refinance replaces your existing mortgage with a larger one and gives you the difference in cash. A DSCR HELOC is a second lien that doesn't touch your first mortgage. If you have a low rate on your first mortgage, a HELOC preserves it. A cash-out refi replaces it.

Q: What's the draw period on a DSCR HELOC?

A: Typically 5 to 10 years, followed by a repayment period of 10 to 20 years. During the draw period, you usually make interest-only payments on what you've drawn.

Q: Are DSCR HELOCs growing in availability in 2026?

A: Yes. DSCR loan growth in 2026 has extended into equity products as non-QM lenders compete for investor business. More options are available now than in 2023 or 2024, though they remain a specialty product.

Conclusion: Should You Pursue a DSCR HELOC?

The DSCR HELOC: Can Investors Actually Combine the Two? question has a clear answer — yes, and in 2026, more lenders are making it possible than ever before. For self-employed investors, portfolio builders, and anyone sitting on significant rental property equity, this product is worth serious consideration.

The case for it is impeccable when the numbers work: no income docs, property-driven qualification, revolving access to capital, and the ability to scale without disturbing existing low-rate first mortgages. That's a fresh combination of flexibility that traditional lending simply doesn't offer.

But let it cook before you see results. A DSCR HELOC is a tool, not a shortcut. The investors who use it well are the ones who stress-test their DSCR, understand the variable rate risk, and deploy the capital into income-producing improvements or acquisitions — not lifestyle upgrades.

Your next steps:

- Calculate your current DSCR on any property you're considering. If it's below 1.0, work on improving occupancy or rents before applying.

- Pull your credit report and address any issues that could push you below the 680 threshold.

- Contact 2 to 3 non-QM lenders or a broker who specializes in investor financing and ask specifically about DSCR equity line products.

- Compare the DSCR HELOC against a cash-out refinance — run both scenarios with current rates before deciding.

- Get your documents organized — lease agreements, rent rolls, mortgage statements, and insurance docs.

The equity in your rental properties is working capital. A DSCR HELOC is one of the most extraordinary ways to put it to work — if you go in with your eyes open and your numbers right.

Have questions about DSCR financing or investment property equity lines? Reach out to the RERIQ team at news@realestaterankiq.com or explore more investor resources at realestaterankiq.com.

{kind=link}