Last updated: May 24, 2026

Quick Answer: An interest only HELOC lets you borrow against your home equity and pay only the interest during the draw period — which keeps monthly payments low. But when the repayment period kicks in, your payment can more than double overnight. That shift, called HELOC payment shock, catches thousands of homeowners completely off guard every year. Whether it's big trouble depends entirely on how prepared you are.

Key Takeaways 🏠

- An interest only HELOC has two phases: a draw period (typically 10 years) where you pay only interest, and a repayment period (typically 20 years) where you pay principal + interest.

- With current HELOC rates averaging around 7.41% in 2026, even a $50,000 balance means a meaningful payment jump when repayment begins.

- HELOC payment shock is real — monthly payments can increase by 50% to 150% when the draw period ends.

- Real estate investors and high-income professionals can use interest only HELOCs strategically — but only with a clear exit or repayment plan.

- Most homeowners who struggle with HELOCs made the same mistake: they treated the draw period like free money and never planned for repayment.

- You typically need at least 15–20% equity remaining in your home after the HELOC to qualify.

- Alternatives like home equity loans, cash-out refinances, and HELOCs from a credit union may offer more predictable terms.

- The interest only mortgage trend in 2026 is drawing renewed scrutiny from regulators — know the rules before you sign.

What Exactly Is a HELOC and How Does Interest Only Work?

A HELOC (Home Equity Line of Credit) is a revolving credit line secured by your home's equity. During the draw period — usually 10 years — you can borrow, repay, and borrow again up to your approved limit. An interest only HELOC means that during this draw period, your required monthly payment covers only the interest on what you've borrowed, not the principal balance itself.

Here's the practical breakdown:

- Draw period: Typically 5–10 years. You access funds as needed and pay only interest on the outstanding balance.

- Repayment period: Typically 10–20 years. The line closes, and you repay the full principal plus interest — fully amortized.

- Variable rate: Most HELOCs carry a variable interest rate tied to the prime rate, meaning your interest-only payment can change month to month.

Example: Borrow $60,000 at a 7.41% rate. During the interest only draw period, your monthly payment is roughly $370. When repayment begins over 20 years, that same balance generates a payment closer to $475–$480 — and if rates have risen, it could be higher.

The interest only structure isn't inherently dangerous. It's a tool. Like any tool, the outcome depends on how you use it.

Interest Only HELOC: Low Payments Now, Big Trouble Later? — The Full Picture

This is the core question, and the honest answer is: it depends on your plan.

The "low payments now" part is 100% accurate. Interest only HELOC payments are structurally designed to be lower during the draw period, which is exactly why they're attractive to real estate investors, self-employed borrowers managing cash flow, and homeowners doing renovations. That's not gatekeeping — that's just how the product works.

The "big trouble later" part is also real — but it's not automatic. The trouble comes from two specific scenarios:

- You borrow the maximum and don't reduce the balance before repayment begins.

- Your income or financial situation changes before the HELOC repayment period hits.

The interest only HELOC pros and cons break down like this:

| Factor | Pro | Con |

|---|---|---|

| Monthly payment during draw | Low — interest only | Doesn't reduce principal |

| Cash flow flexibility | High | Can encourage overborrowing |

| Rate structure | Access to equity at variable rates | Rates can rise (currently ~7.41% in 2026) |

| Repayment transition | Long draw period to plan | Payment shock risk is real |

| Tax deductibility | Interest may be deductible if used for home improvements | Rules are specific — consult a CPA |

The interest only mortgage trend in 2026 has regulators watching this space more carefully. If you're considering this product, get the full picture before signing. Our Real Estate Financing Guide breaks down the broader mortgage landscape if you want context.

How Much Lower Are Interest Only HELOC Payments Compared to a Regular HELOC?

Interest only payments are significantly lower — often 30% to 50% less than a fully amortizing payment on the same balance. The gap is most dramatic on larger balances and longer repayment periods.

Here's a direct comparison using current HELOC rates of approximately 7.41% (2026 estimate based on prime rate trends):

| Balance | Interest Only Payment | Fully Amortizing (20-yr) |

|---|---|---|

| $25,000 | ~$154/month | ~$199/month |

| $50,000 | ~$309/month | ~$397/month |

| $75,000 | ~$463/month | ~$596/month |

| $100,000 | ~$617/month | ~$795/month |

Note: These are estimates based on a 7.41% annual rate. Actual payments vary by lender, rate changes, and draw balance.

The difference looks manageable on paper. But here's what the numbers don't show: if you've been paying interest only for 10 years and haven't touched the principal, the entire balance is still sitting there when repayment begins. That's the HELOC payment reset moment that surprises people.

What Happens When the Interest Only Period Ends on a HELOC?

When the HELOC draw period ends, the line closes and HELOC amortization begins. You can no longer borrow from the line, and your monthly payment recalculates to include both principal and interest — spread over the remaining repayment period (typically 20 years).

This is HELOC payment shock. Your payment doesn't just go up a little — it can jump dramatically, especially if:

- You borrowed a large amount during the draw period

- Interest rates rose since you opened the HELOC

- You made only minimum (interest only) payments throughout the draw period

Real scenario: You opened a HELOC in 2016 with a $80,000 balance. You paid interest only for 10 years. In 2026, repayment begins. At current interest only HELOC rates 2026 of ~7.41%, your new payment on that $80,000 over 20 years is approximately $635/month — compared to the ~$494/month interest only payment you were making. That's a $141/month jump, and that's assuming rates didn't climb further.

If rates rose to 9% by the time repayment hit, that payment jumps to $720/month. That's a 45% increase from what you were paying.

Three things that happen at HELOC repayment:

- The draw period closes — no more borrowing

- The balance is locked in and fully amortized

- Monthly payments increase, sometimes sharply

Am I Risking Losing My Home With an Interest Only HELOC?

Yes — and this is not fear-mongering. A HELOC is secured by your home. If you default on HELOC repayment, the lender can foreclose.

The risk is highest when:

- You borrowed close to your equity limit. If home values drop and you owe more than the home is worth across your first mortgage and HELOC combined, you're in a tough spot.

- Your income drops before repayment begins. The draw period can lull you into a false sense of security. Ten years feels long — until it doesn't.

- You can't refinance out of the HELOC. If rates are high or your credit has declined, you may be stuck with the payment reset.

The safest mindset: treat the HELOC like a loan you're actively paying down, not a credit card with a 10-year grace period. Pay down principal voluntarily during the draw period. Let it cook before you see results — consistent extra payments during the draw phase dramatically reduce the payment shock later.

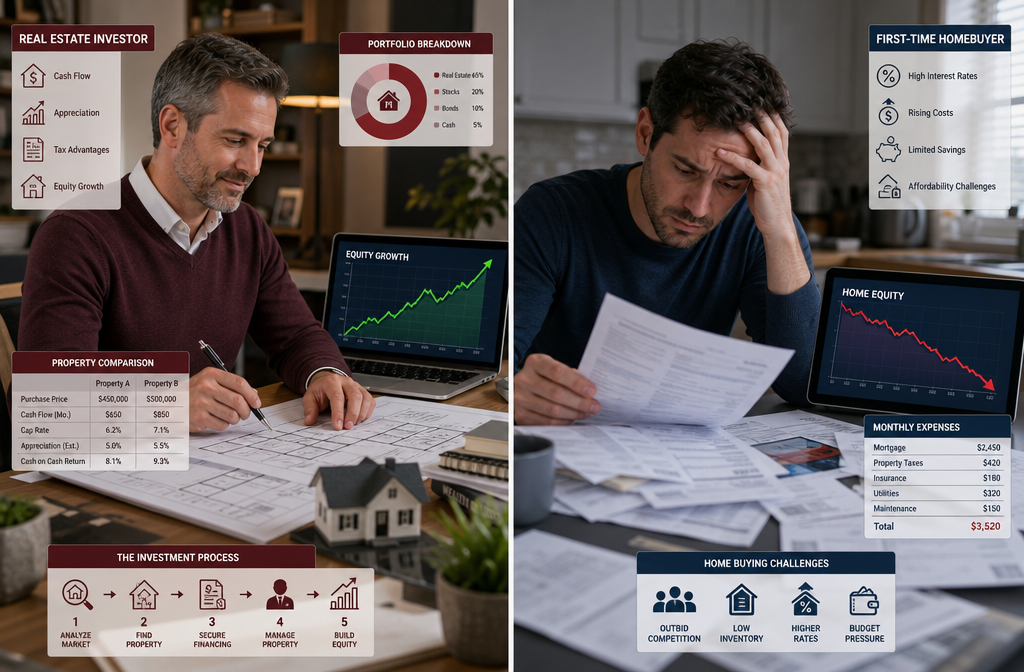

Who Should Consider an Interest Only HELOC (and Who Should Avoid It)?

Strong candidates for an interest only HELOC:

- Real estate investors using the HELOC to fund a down payment on a rental property, with rental income covering the payment

- Self-employed borrowers with irregular income who need payment flexibility during lean months

- High-income professionals doing a major home renovation with a clear plan to refinance or pay down the balance

- Short-term bridge users — someone who needs liquidity for 1–3 years and plans to pay off the balance before repayment begins

Who should probably avoid it:

- First-time homebuyers with tight budgets and no financial cushion

- Anyone who plans to borrow the maximum and make minimum payments indefinitely

- Homeowners in markets where property values are flat or declining (limited equity buffer)

- Anyone without a clear plan for what happens when the HELOC repayment period begins

So based on your financial situation is the honest filter here. An interest only HELOC is an extraordinary tool in the right hands — and a financial trap in the wrong ones.

For investors specifically, check out our deep-dive on HELOC on investment property strategies to see how experienced investors use this product without getting burned.

What Are the Biggest Risks of Interest Only HELOC Loans?

The biggest risks aren't hidden — they're just easy to ignore when the payments are low. Here's the full list, ranked by how often they catch borrowers off guard:

1. HELOC Payment Shock

The most common risk. Monthly payments jump significantly when the draw period ends and HELOC amortization kicks in. Borrowers who never paid down principal face the full balance at repayment.

2. Variable Rate Exposure

Most HELOCs carry variable rates. With current HELOC rates at approximately 7.41% in 2026, a rate increase of even 1–2% meaningfully raises your interest only payment during the draw period — and your fully amortized payment after.

3. Equity Erosion

If home values decline and you've maxed your HELOC, you could end up underwater — owing more than the home is worth across all liens.

4. Refinancing Risk

If you plan to refinance before repayment begins, you need good credit, sufficient equity, and a favorable rate environment. None of those are guaranteed.

5. Overborrowing

The revolving nature of a HELOC during the draw period makes it easy to keep pulling funds. Without discipline, borrowers can accumulate a much larger balance than originally planned.

6. HELOC Closing Costs

Opening a HELOC isn't free. HELOC closing costs typically run 2%–5% of the credit limit, including appraisal fees, title search, and origination fees. Factor this into your cost analysis.

How Do Interest Rates Impact My Total HELOC Cost?

Interest rates are the single biggest variable in your total HELOC cost — and with a variable rate product, this matters more than most borrowers realize.

Here's how rate changes affect a $75,000 interest only HELOC over a 10-year draw period:

| Rate | Annual Interest Cost | 10-Year Total Interest (Draw Period Only) |

|---|---|---|

| 6.5% | ~$4,875 | ~$48,750 |

| 7.41% | ~$5,558 | ~$55,580 |

| 8.5% | ~$6,375 | ~$63,750 |

| 9.5% | ~$7,125 | ~$71,250 |

Assumes full $75,000 balance outstanding throughout. Actual costs vary based on draw activity.

The interest only HELOC rates 2026 environment is sitting around 7.41% for well-qualified borrowers, based on current prime rate trends. That's not a crisis rate — but it's not cheap either. Every rate increase during your draw period adds to your total cost and increases the payment when repayment begins.

Decision rule: If rates are rising and you're considering a HELOC vs home equity loan, a fixed-rate home equity loan may offer more predictability. A HELOC gives you flexibility; a home equity loan gives you certainty. Choose based on which risk you're more comfortable carrying.

For a broader look at financing options in the current market, our mortgage broker vs direct lender comparison is worth reading before you shop lenders.

Can I Switch From Interest Only to Principal and Interest Payments?

Yes — and this is one of the most underused strategies for managing HELOC risk. Most HELOC agreements allow voluntary principal payments during the draw period. You're not locked into paying interest only; that's just the minimum required payment.

Three practical options:

- Pay extra principal voluntarily during the draw period. Even an extra $200–$300/month toward principal dramatically reduces the balance before repayment begins — and cuts your HELOC payment shock.

- Refinance the HELOC into a fixed home equity loan. If you want to lock in a rate and a predictable payoff schedule, some lenders allow you to convert or refinance your HELOC balance.

- Request a loan modification. In some cases, lenders will restructure the repayment terms — especially if you're proactive and reach out before you're in distress.

What you can't do: You generally can't extend the draw period indefinitely or restart the clock. Once the HELOC draw period 2026 closes, repayment begins on schedule.

The impeccable move is to treat the draw period as a window to reduce your balance — not a vacation from real payments.

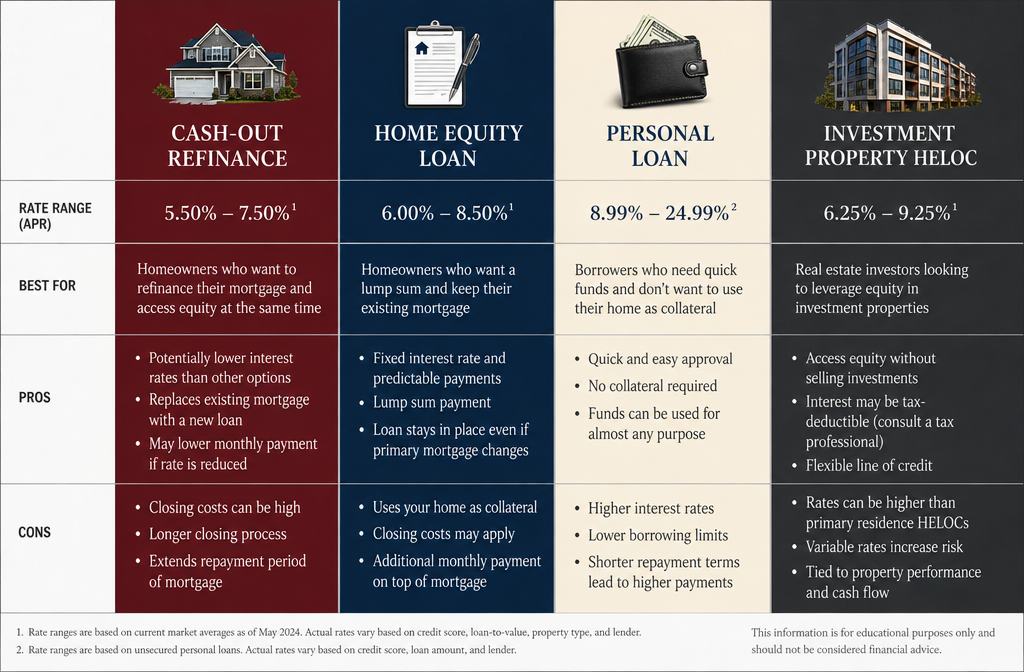

What Are Alternatives to an Interest Only HELOC?

If the variable rate and payment shock risk of an interest only HELOC don't fit your situation, there are solid alternatives:

1. Home Equity Loan (HEL)

Fixed rate, fixed payment, lump sum. This is the HELOC vs home equity loan tradeoff: less flexibility, but complete predictability. Better for borrowers who know exactly how much they need.

2. Cash-Out Refinance

Replace your existing mortgage with a new, larger mortgage and pocket the difference. Rates are fixed (or adjustable), and you consolidate into one payment. Works best when current mortgage rates are lower than your existing rate.

3. HELOC From a Credit Union

A HELOC credit union product often comes with lower rates, fewer fees, and more borrower-friendly terms than big bank HELOCs. If you qualify for membership, this is worth comparing.

4. Better HELOC Products

Some fintech lenders (including platforms marketed as "better HELOC" options) offer hybrid products with fixed-rate draw options or rate caps. These can reduce variable rate exposure while keeping the revolving credit structure.

5. Personal Loan

No home equity required, no foreclosure risk. Higher rates, but your home isn't collateral. Good for smaller amounts ($10,000–$30,000) with a short payoff timeline.

6. Investment Property HELOC

For real estate investors specifically, our guide on best HELOC lenders for investment property covers lenders who specialize in this product and what the qualification requirements look like in 2026.

How Much Home Equity Do I Need to Qualify for a HELOC?

Most lenders require you to maintain at least 15–20% equity in your home after the HELOC is factored in. The calculation they use is called the Combined Loan-to-Value ratio (CLTV).

CLTV Formula:

(First Mortgage Balance + HELOC Limit) ÷ Home Value = CLTV

Example:

- Home value: $400,000

- First mortgage balance: $250,000

- Desired HELOC: $50,000

- CLTV: ($250,000 + $50,000) ÷ $400,000 = 75%

Most lenders cap CLTV at 80–85% for a HELOC. A HELOC credit union may go slightly higher for well-qualified members.

Additional qualification factors:

- Credit score: Typically 680+ for standard approval; 720+ for best rates

- Debt-to-income ratio: Usually 43% or below

- Income verification: W-2, tax returns, or bank statements for self-employed borrowers

- Home appraisal: Required to confirm current market value

Fresh tip: If your home has appreciated significantly since purchase, you may have more equity than you think. Get a current appraisal or a broker price opinion before assuming you don't qualify.

What Mistakes Do Homeowners Typically Make With Interest Only HELOCs?

The same mistakes show up over and over. These aren't edge cases — they're patterns that brokers with 15+ years in the field see regularly.

Mistake #1: Treating the draw period as free money

Making only the minimum interest only payment for 10 years and doing nothing to reduce principal. The balance is identical at repayment as it was on day one.

Mistake #2: Not accounting for rate increases

Opening a HELOC at a low introductory rate and not stress-testing what happens if rates climb 2–3 points. Variable rate exposure is real.

Mistake #3: Using HELOC funds for depreciating assets

Borrowing against home equity to buy a car, fund a vacation, or cover everyday expenses. Your home is collateral — it should fund things that appreciate or generate income.

Mistake #4: Ignoring HELOC closing costs

Assuming the HELOC is "free" to open. HELOC closing costs can run $500–$5,000+ depending on the lender and credit limit.

Mistake #5: No exit strategy

Not having a clear plan for how the HELOC balance gets paid off. "I'll figure it out in 10 years" is not a strategy.

Mistake #6: Maxing the line right before repayment

Drawing the full balance close to the end of the draw period, then immediately facing full HELOC amortization on the maximum balance.

For investors who want to avoid these traps and actually build wealth with equity, our rental property analysis checklist pairs well with HELOC strategy planning.

How Do I Calculate My Total Repayment With an Interest Only HELOC?

Total HELOC repayment cost = interest paid during draw period + principal + interest paid during repayment period.

Step-by-step calculation:

Step 1: Determine your average outstanding balance during the draw period.

(If you borrowed $60,000 and kept it fully drawn for 10 years, average balance = $60,000)

Step 2: Calculate draw period interest cost.

$60,000 × 7.41% = $4,446/year × 10 years = $44,460 in interest during draw period

Step 3: Calculate repayment period cost.

$60,000 amortized over 20 years at 7.41% = approximately $468/month

$468 × 240 months = $112,320 total paid during repayment

Of that, roughly $52,320 is interest; $60,000 is principal.

Step 4: Add it up.

$44,460 (draw interest) + $112,320 (repayment total) = $156,780 total paid on a $60,000 HELOC

That's $96,780 in total interest on a $60,000 loan — if you never paid down principal during the draw period. That number should make you think twice about what you're using the funds for.

Are Interest Only HELOCs Good for Real Estate Investors?

For real estate investors, an interest only HELOC can be an extraordinary tool — when used correctly. The low payment during the draw period preserves cash flow, which is the lifeblood of any rental portfolio.

Where it works well for investors:

- Funding a down payment on a rental property. The rental income covers the HELOC payment, and the new asset appreciates independently.

- Financing a fix-and-flip. Draw the funds, complete the renovation, sell the property, and pay off the HELOC before repayment begins. Clean exit.

- Bridge financing between deals. Short-term liquidity without selling existing assets.

- Portfolio scaling. Experienced investors use equity in paid-down properties to fund acquisitions — the interest only HELOC keeps carrying costs low while the new asset builds equity.

Where it gets risky for investors:

- Overleveraging across multiple properties with HELOC balances on each

- Assuming rental income will always cover the payment (vacancies happen)

- Not accounting for the HELOC payment reset when projecting long-term cash flow

The investors who use HELOCs best treat them like a revolving credit facility — draw, deploy, repay, repeat. They don't let balances sit and compound. That discipline is what separates strategic equity use from financial stress.

For a deeper look at investment financing in 2026, our guide on cash flow real estate investing covers how to structure deals so the numbers work from day one.

Frequently Asked Questions

Q: What is the current average HELOC rate in 2026?

A: Current HELOC rates in 2026 are averaging approximately 7.41% for well-qualified borrowers, based on prime rate trends. Your actual rate depends on credit score, CLTV, and lender.

Q: How long is a typical HELOC draw period?

A: Most HELOCs have a draw period of 10 years, followed by a repayment period of 10–20 years. Some lenders offer 5-year draw periods with shorter repayment windows.

Q: Can I pay off my HELOC early?

A: Yes. Most HELOCs allow early payoff without penalty, though some lenders charge an early closure fee (typically $300–$500) if you close the account within the first 2–3 years.

Q: Is HELOC interest tax deductible in 2026?

A: HELOC interest may be deductible if the funds are used to buy, build, or substantially improve the home securing the loan. Using HELOC funds for other purposes (debt consolidation, vacations, etc.) generally does not qualify. Consult a tax professional for your specific situation.

Q: What's the difference between a HELOC and a home equity loan?

A: A HELOC is a revolving credit line with a variable rate. A home equity loan is a lump-sum loan with a fixed rate and fixed monthly payment. HELOCs offer flexibility; home equity loans offer predictability.

Q: Can I get a HELOC on an investment property?

A: Yes, but it's harder. Investment property HELOCs require more equity (typically 30–40% remaining after the HELOC), higher credit scores, and carry higher rates than primary residence HELOCs.

Q: What happens if I can't afford the payment when repayment begins?

A: Contact your lender before you miss a payment. Options may include a loan modification, refinancing the balance into a new loan, or a repayment plan. Ignoring it risks foreclosure since the HELOC is secured by your home.

Q: How does a HELOC credit union compare to a bank HELOC?

A: Credit union HELOCs often feature lower rates, reduced fees, and more flexible underwriting than big bank products. The tradeoff is that credit unions require membership and may have more limited online tools.

Q: What is HELOC amortization?

A: HELOC amortization is the process of repaying the principal balance plus interest over the repayment period, structured so the loan is fully paid off by the end of the term. During the draw period, no amortization occurs if you're making interest only payments.

Q: Is an interest only HELOC a good idea for a first-time homebuyer?

A: Generally, no. First-time buyers with limited financial cushion and less experience managing variable-rate debt are more vulnerable to HELOC payment shock. A fixed home equity loan or other financing option is usually a safer starting point.

Conclusion: So, Is It Low Payments Now and Big Trouble Later?

The honest answer: it can be either — and which one you get depends entirely on the plan you bring to the table.

An interest only HELOC is a fresh, flexible financing tool that real estate investors and high-income professionals have used to build serious wealth. The low payments during the draw period are real. The flexibility is real. The tax advantages (when used correctly) are real.

But so is the HELOC payment shock. So is the variable rate risk. So is the foreclosure exposure if repayment becomes unmanageable.

The homeowners and investors who win with this product treat the draw period as a working window — not a vacation from financial responsibility. They pay down principal voluntarily, watch their rate environment, and have a clear exit strategy before they ever sign the paperwork.

Your next steps:

- Run the numbers using the repayment calculation in this article before you open a HELOC.

- Compare products — get quotes from at least one HELOC credit union and one bank or fintech lender.

- Stress-test your payment at rates 2–3 points higher than today's 7.41% to see if you can still afford repayment.

- Consult a CPA about the tax deductibility of your intended use.

- Have a payoff plan — know exactly how and when the balance gets to zero.

The interest only HELOC: low payments now, big trouble later? Only if you let it be. Let it cook before you see results — build your equity strategy with intention, and this product can be one of the most powerful tools in your real estate arsenal.

For more on real estate financing strategies, visit Real Estate Rank IQ or reach out at news@realestaterankiq.com. Subscribe to our YouTube channel @Realestaterankiq for video breakdowns of the topics that matter most to buyers, investors, and agents in 2026.

{kind=link}