Last updated: May 24, 2026

Quick Answer: Yes, you can get a HELOC with bad credit — but the pool of lenders willing to work with you is smaller, the rates are higher, and the equity requirements are stricter. Credit scores as low as 580 can still qualify with the right lender, especially credit unions, community banks, and non-QM lenders who evaluate the full picture of your finances, not just your FICO number.

Key Takeaways

- Most traditional banks require a minimum credit score of 620–680 for a HELOC, but alternative lenders go as low as 580

- Non-QM home equity products and portfolio lenders are the most flexible options for borrowers with poor credit

- HELOC rates in 2026 average around 7.41% for well-qualified borrowers — expect 9%–13%+ with bad credit

- Lenders weigh your combined loan-to-value (CLTV) ratio heavily; 80% or below gives you the best shot

- A cosigner with strong credit can meaningfully improve your approval odds

- Bad credit HELOCs carry real risk — your home is the collateral, so missed payments can lead to foreclosure

- Alternatives like home equity loans, cash-out refinancing, and hard money loans may serve bad credit borrowers better in some situations

- Improving your credit score by even 40–60 points before applying can save you tens of thousands in interest over the life of the line

What Exactly Is a HELOC and How Does It Work With Bad Credit?

A HELOC (Home Equity Line of Credit) is a revolving credit line secured by your home's equity — think of it like a credit card, but backed by your property. You borrow what you need, pay it back, and borrow again during the draw period (typically 5–10 years), then repay the remaining balance during the repayment period (usually 10–20 years).

With bad credit, the mechanics of a HELOC don't change — but the terms do. Lenders see a low credit score as a signal of higher default risk, so they compensate by charging higher interest rates, requiring more equity, and sometimes capping how much you can borrow.

Here's how the math works in practice:

- Your home is worth $350,000

- You owe $200,000 on your mortgage

- Your equity is $150,000

- Most lenders allow you to borrow up to 80%–85% of your home's value, minus what you owe

- At 80% CLTV: $350,000 × 0.80 = $280,000 − $200,000 = $80,000 available to borrow

With bad credit, some lenders drop that ceiling to 75% or even 70% CLTV, which directly shrinks your borrowing power. The equity in your home is doing the heavy lifting here — and that's actually your biggest negotiating chip.

For a deeper look at how home equity financing fits into a broader investment strategy, check out our guide on HELOC on Investment Property: How Smart Investors Scale.

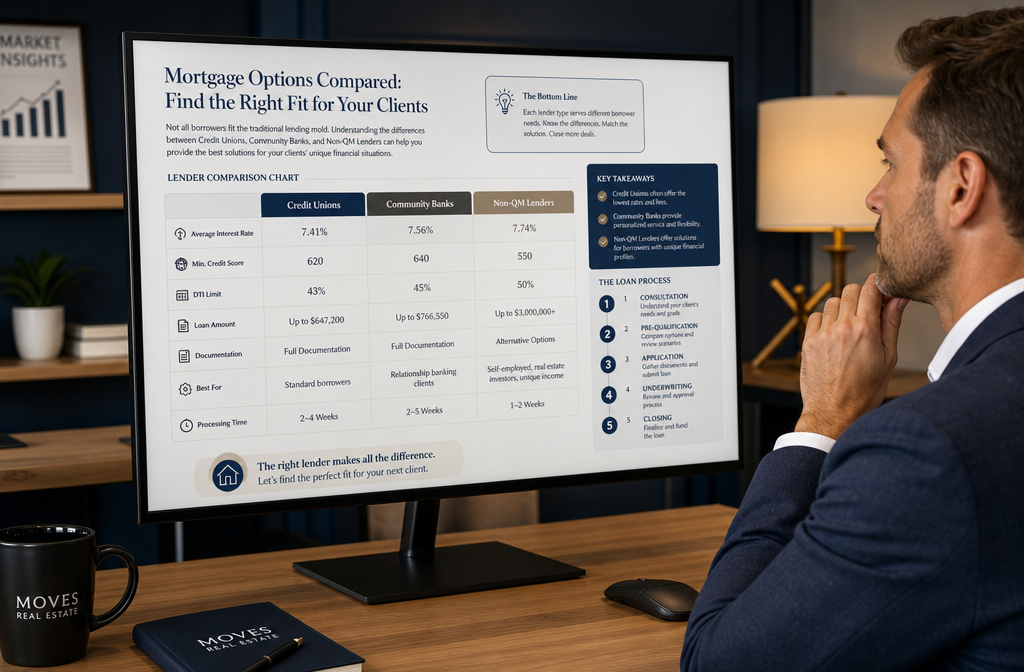

HELOC With Bad Credit: The Lenders Who Still Say Yes

This is the part most financial sites are gatekeeping — and we're not about that. Not every lender slams the door on borrowers with credit scores below 640. Here's who's actually working with bad credit borrowers in 2026.

Credit Unions

Credit unions are consistently the most borrower-friendly institutions for a HELOC loan with bad credit. Because they're member-owned and not profit-driven, they have more flexibility in underwriting. Many credit unions will approve applicants with scores as low as 580–600, especially if you've been a member for a while and have a clean payment history with them.

Best move: Join a local credit union before you need the loan. Membership tenure matters.

Community Banks

Community banks operate with portfolio lending — meaning they keep loans on their own books instead of selling them to the secondary market. This gives them the freedom to approve borrowers that big banks would reject. They're evaluating you as a person, not just a number.

Non-QM Lenders

Non-QM (non-qualified mortgage) lenders are built for borrowers who don't fit the standard mold. These include self-employed borrowers, real estate investors, and yes — people with bruised credit. Non-QM home equity products are increasingly common in 2026, and some of these lenders will go down to a 580 credit score with sufficient equity.

The trade-off? Rates are higher, sometimes significantly. Expect to pay 10%–13%+ on a non-QM HELOC versus the current average HELOC rates in 2026 of around 7.41% for prime borrowers.

Online and Alternative Lenders

Some fintech-forward lenders and online platforms have emerged with flexible underwriting models that factor in bank statement income, rental income, and asset-based qualification — not just your FICO score. These are worth exploring, especially if you're self-employed or have irregular income.

| Lender Type | Min. Credit Score | CLTV Limit | Rate Range (Est.) | Best For |

|---|---|---|---|---|

| Big Banks (Chase, Wells Fargo) | 660–700 | 80–85% | 7.5%–9% | Strong credit borrowers |

| Credit Unions | 580–620 | 80% | 8%–10% | Members with relationship history |

| Community Banks | 580–620 | 75–80% | 8.5%–10.5% | Local borrowers, portfolio loans |

| Non-QM Lenders | 560–600 | 65–75% | 10%–13%+ | Self-employed, investors, bad credit |

| Online/Fintech Lenders | 580–640 | 75–80% | 9%–12% | Digital-first, flexible income docs |

So based: Working with a mortgage broker to shop multiple lenders at once is one of the smartest moves a bad credit borrower can make. One inquiry, multiple options. See our breakdown of Mortgage Broker vs Direct Lender: Which Saves Investors More?

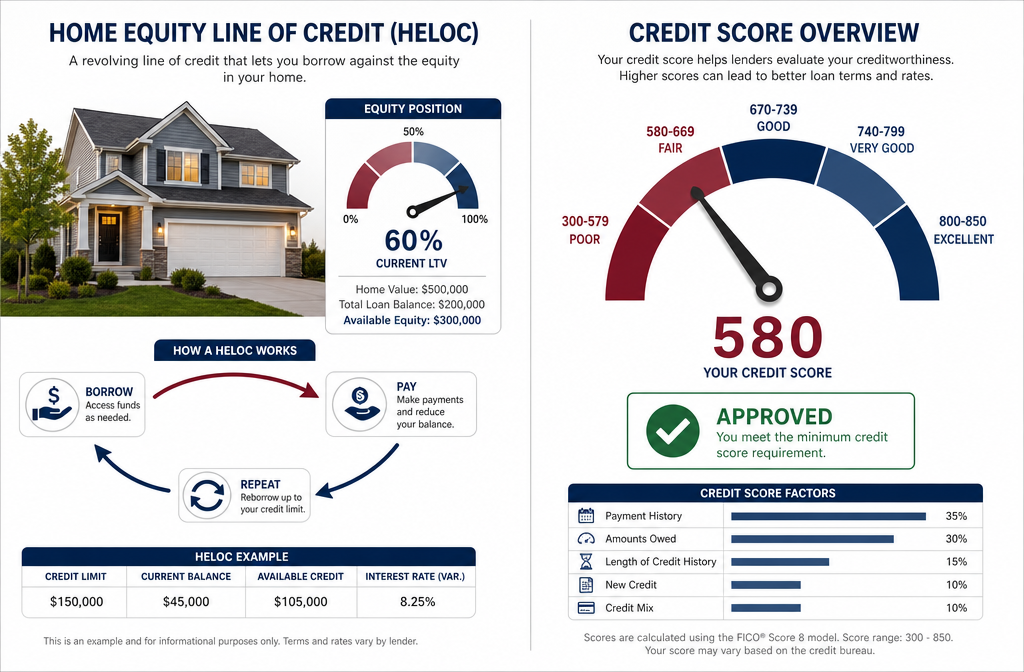

What Minimum Credit Score Do I Need for a Home Equity Line of Credit?

The standard minimum credit score for a HELOC at most traditional lenders is 620, but the sweet spot for competitive rates starts at 680 and above. Below 620, your options shrink fast — but they don't disappear.

Here's the realistic breakdown by credit tier:

- 740+ — Best rates, most lenders, easiest approval

- 680–739 — Good rates, most lenders still available

- 640–679 — Higher rates, some lenders pull back, more documentation required

- 620–639 — Limited lenders, tighter CLTV requirements, expect rate premiums

- 580–619 — Credit unions, community banks, non-QM lenders only; strong equity required

- Below 580 — HELOC approval is extremely difficult; alternatives are more realistic

The HELOC credit score threshold isn't the only factor lenders look at, but it's often the first filter. If your score is sitting at 610, getting it to 640 before applying could open up a meaningfully different set of lenders.

For context on how credit scores affect real estate financing broadly, our Real Estate Financing Guide: Mortgages, Credit & Down Payments breaks it all down.

How Much Can I Borrow With Bad Credit Using a Home Equity Line of Credit?

With bad credit, your borrowing limit on a HELOC is determined by two things: your CLTV ratio and the lender's risk appetite. Most bad credit HELOC lenders cap CLTV at 75%–80%, compared to 85%–90% for prime borrowers.

Example calculation:

- Home value: $400,000

- Mortgage balance: $250,000

- Lender CLTV limit (bad credit): 75%

- Max loan amount: ($400,000 × 0.75) − $250,000 = $50,000

If the same borrower had good credit and a lender allowing 85% CLTV:

- ($400,000 × 0.85) − $250,000 = $90,000

That's a $40,000 difference — just from the credit score impact on CLTV limits. This is why building equity and improving your credit score simultaneously is the most powerful combo play for home equity loan bad credit situations.

Common mistake: Applying for the maximum available credit line. Lenders see this as a risk signal. Apply for what you actually need.

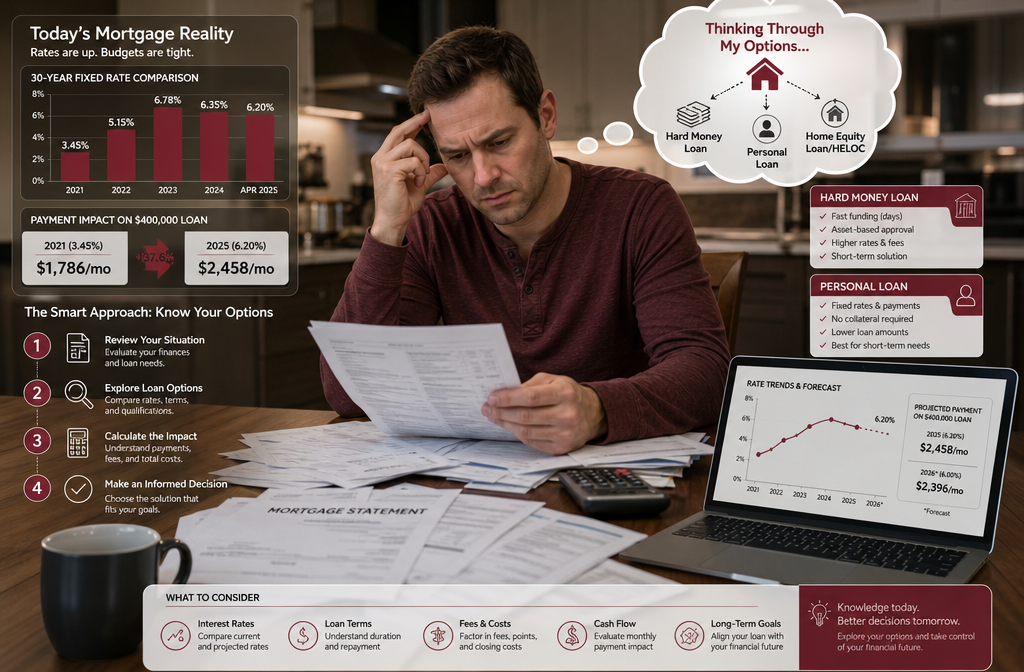

What Interest Rates Should I Expect for a HELOC With Poor Credit?

Current HELOC rates in 2026 average around 7.41% for well-qualified borrowers. For bad credit borrowers, expect to pay a significant premium on top of that.

Here's the realistic rate picture for a HELOC loan with bad credit in 2026:

- Credit score 640–679: 9%–10.5%

- Credit score 600–639: 10.5%–12%

- Credit score 580–599: 12%–14% (non-QM lenders)

- Below 580: Hard money or private lenders, 14%–18%+

HELOCs are typically tied to the Prime Rate, which moves with Federal Reserve decisions. In 2026, with rates still elevated compared to the pre-2022 environment, bad credit borrowers are feeling this double pressure — high base rates plus a credit risk premium stacked on top.

The real cost: On a $50,000 HELOC at 12% vs. 7.41%, you'd pay roughly $2,295 more per year in interest alone. Over a 10-year draw period, that's a serious number. This is why we always say: let it cook before you see results — meaning, if you have 6–12 months before you need the funds, use that time to repair your credit first.

Are There Alternatives to a HELOC If My Credit Is Really Bad?

If your credit score is below 580 or lenders keep saying no, a HELOC isn't your only path. There are several bad credit home equity options worth knowing.

Home Equity Loan (Bad Credit)

Unlike a HELOC, a home equity loan gives you a lump sum at a fixed interest rate. Some lenders are slightly more willing to approve a home equity loan bad credit application because the fixed structure is easier to underwrite. Rates will still be elevated, but the predictability can work in your favor.

Cash-Out Refinance

Replacing your existing mortgage with a new, larger one and pocketing the difference. If you have an FHA loan, FHA allows cash-out refis with credit scores as low as 500 (with 20% equity). This can be a better path than a home equity line of credit bad credit scenario.

Hard Money Loans

Bad credit HELOC vs. hard money in 2026 is a real conversation worth having. Hard money lenders are asset-based — they care about the property's value, not your credit score. Rates are steep (12%–18%), terms are short (6–24 months), but approval is fast. Best for real estate investors who need quick capital and have a clear exit strategy.

For investors specifically, our guide on Best HELOC Lenders for Investment Property 2026 covers the full landscape.

DSCR Loans

For rental property owners, a DSCR (Debt Service Coverage Ratio) loan qualifies based on the property's rental income, not your personal credit. This is an extraordinary option for investors who have cash-flowing properties but imperfect credit. See our Best DSCR Loan Lenders for Investment Properties 2026 for ranked options.

Personal Loans

Unsecured, no home collateral required, but rates for bad credit borrowers can hit 20%–30%. Only makes sense for smaller amounts ($5,000–$15,000) when you can't qualify for anything else.

No Doc HELOC

A no doc HELOC (also called a stated income or bank statement HELOC) skips traditional income verification. These products exist primarily in the non-QM space and are more accessible to self-employed borrowers or those with complex income structures. Credit score requirements vary by lender but generally start around 600.

| Alternative | Min. Credit Score | Rate Range | Best For |

|---|---|---|---|

| Home Equity Loan | 580–620 | 9%–13% | Lump sum needs, fixed payment preference |

| Cash-Out Refi (FHA) | 500 | 7%–10% | Existing FHA borrowers with equity |

| Hard Money Loan | None (asset-based) | 12%–18% | Investors, short-term needs |

| DSCR Loan | 620 | 7.5%–10% | Rental property investors |

| No Doc HELOC | 600+ | 10%–14% | Self-employed, non-traditional income |

| Personal Loan | 580 | 18%–30% | Small amounts, no equity available |

What Documents Do I Need to Prove I Can Handle a HELOC With Bad Credit?

With bad credit, lenders require more documentation — not less. The goal is to compensate for the credit score with other proof of financial stability. Here's what to have ready.

Standard documents every lender will want:

- Last 2 years of federal tax returns (W-2s or 1099s)

- Last 2–3 months of bank statements

- Recent pay stubs (last 30 days)

- Current mortgage statement showing balance

- Homeowner's insurance declaration page

- A recent property appraisal or automated valuation

Additional documents bad credit borrowers should prepare:

- Letter of explanation for any derogatory marks on your credit report (late payments, collections, bankruptcy)

- 12–24 months of bank statements if you're self-employed or have variable income

- Proof of rental income (lease agreements, Schedule E from tax returns) if applicable

- Asset statements — retirement accounts, investment accounts, savings — showing reserves

- Documentation of credit improvements — if you've paid off collections or resolved disputes recently, show it

Fresh tip: Pull your own credit report from AnnualCreditReport.com before applying. Dispute any errors. Even one incorrect late payment removed can move your score 20–30 points. That's free money.

Can I Improve My Chances of HELOC Approval With a Cosigner?

Yes — a creditworthy cosigner can significantly improve your odds of approval for a HELOC with bad credit. The cosigner's credit score, income, and debt-to-income ratio are factored into the application alongside yours, which can push the combined profile into an approvable range.

Important caveats:

- Not all lenders allow cosigners on HELOCs — ask explicitly before applying

- The cosigner is equally responsible for the debt. If you miss payments, their credit takes the hit

- The HELOC will appear on the cosigner's credit report, affecting their debt-to-income ratio for future borrowing

- Family members are the most common cosigners, but lenders don't require a family relationship

Choose a cosigner if: Your credit score is 580–619 and you have a family member or trusted person with a 700+ score, stable income, and low existing debt.

Skip the cosigner if: The relationship risk isn't worth it, or if the cosigner has their own credit challenges.

Common Mistakes People Make When Trying to Get a HELOC With Bad Credit

These are the moves that turn a possible approval into a definite rejection — and we see them constantly.

1. Applying to too many lenders at once

Multiple hard inquiries in a short window can drop your score 5–15 points. Rate shopping is smart, but do it within a 14–45 day window so the bureaus count it as a single inquiry.

2. Ignoring the debt-to-income ratio

Lenders want your total debt payments (including the new HELOC) to stay below 43% of gross monthly income. Many bad credit borrowers focus on the score and ignore DTI — and get denied for that reason instead.

3. Applying for the maximum credit line

This signals financial desperation to underwriters. Apply for a specific, justified amount tied to a clear purpose (renovation, debt consolidation, investment).

4. Not addressing credit report errors first

Errors on credit reports are more common than most people realize. Disputing and removing inaccurate negative items before applying is one of the highest-ROI moves available to you.

5. Skipping the credit union option

Most people go straight to big banks and get rejected. Credit unions are frequently the right first call for equity loans with poor credit — and most people never try them.

6. Underestimating closing costs

HELOCs come with closing costs: appraisal fees, title search, origination fees. These typically run $500–$2,000 or more. Factor this into your decision.

How Long Does It Take to Get Approved for a HELOC With Low Credit?

For a standard HELOC at a traditional lender, approval takes 2–6 weeks from application to funding. With bad credit, add time — because manual underwriting reviews take longer than automated approvals.

Realistic timeline breakdown:

- Application and document submission: 1–3 days

- Lender review and underwriting: 1–3 weeks (longer for bad credit, non-QM)

- Property appraisal: 1–2 weeks

- Conditional approval and additional document requests: 3–7 days

- Closing: 1–3 days

- Funding: 3-business-day right of rescission for primary residences, then funds release

Total realistic timeline for bad credit applicants: 4–8 weeks

Hard money loans and some non-QM products can close in 7–14 days if speed is critical — but you'll pay for that speed in rate.

Risks of Getting a HELOC When My Credit Is Not Great

This section deserves straight talk. A HELOC with bad credit is not free money — and the risks are real.

Your home is the collateral. Miss enough payments and the lender can foreclose. This isn't a credit card where the worst outcome is a collections call. It's your house.

Variable rates can spike your payment. Most HELOCs have variable interest rates tied to the Prime Rate. If rates rise, your monthly payment rises with them — sometimes significantly. Bad credit borrowers already paying 11%–12% are especially exposed.

The draw period ends. During the draw period, many HELOCs only require interest payments. When the repayment period starts, your payment can jump dramatically as principal gets added. This "payment shock" catches a lot of borrowers off guard.

It can deepen a debt spiral. If you're using a HELOC to pay off credit cards and then running those cards back up, you've converted unsecured debt into secured debt backed by your home. That's a dangerous trade.

Impeccable discipline is required. A HELOC is a tool — and like any tool, the outcome depends entirely on how you use it.

For investors evaluating whether a HELOC makes sense as part of a broader strategy, our Real Estate Financing Guide covers the full financial picture.

How Does a HELOC Impact My Credit Score in the Long Term?

A HELOC affects your credit in several ways — both positive and negative — and understanding this is key to using it strategically.

Short-term impacts (first 6–12 months):

- Hard inquiry at application: −2 to −5 points (temporary)

- New account opening lowers average account age: −5 to −15 points (temporary)

- Increased total available credit (if you don't draw on it): can improve credit utilization ratio positively

Long-term impacts:

- On-time payments are reported monthly and build your payment history — the single biggest factor in your credit score (35% of FICO)

- Low utilization of the HELOC (using less than 30% of the line) signals responsible credit management

- Consistent repayment over 12–24 months can meaningfully improve your score — often enough to refinance into better terms later

The strategic play: Use a HELOC responsibly for 18–24 months, make every payment on time, keep utilization low, and your credit score can improve enough to refinance at a significantly lower rate. That's the real long game.

For more on how credit scores work in real estate transactions, see our resource on understanding credit scores for real estate transactions.

Frequently Asked Questions

Q: Can I get a HELOC with a 580 credit score?

Yes, but your options are limited to credit unions, community banks, and non-QM lenders. You'll need significant equity (typically 25%–35% of your home's value) and a strong debt-to-income ratio to offset the low score.

Q: What is the minimum credit score for a HELOC at most banks?

Most traditional banks set the minimum at 620, with better terms starting at 680. Below 620, you're looking at alternative lenders.

Q: What are current HELOC rates in 2026?

The average HELOC rate in 2026 is approximately 7.41% for well-qualified borrowers. Bad credit borrowers should expect 9%–14% depending on their credit profile and lender type.

Q: Is a home equity loan easier to get than a HELOC with bad credit?

Slightly, in some cases. Home equity loans have fixed rates and structured repayment, which some lenders find easier to underwrite for higher-risk borrowers. The credit score requirements are similar, but the fixed nature can work in your favor.

Q: What's a no doc HELOC?

A no doc HELOC skips traditional income verification (pay stubs, W-2s) and instead uses bank statements or asset statements to qualify. These are non-QM products aimed at self-employed borrowers and real estate investors with non-traditional income.

Q: Can I use a HELOC from a bad credit lender to buy an investment property?

Yes — and this is actually a common strategy among real estate investors. The key is ensuring the rental income from the investment property covers your costs. See our guide on HELOC on Investment Property: How Smart Investors Scale.

Q: How is a bad credit HELOC different from a hard money loan?

A HELOC is secured by your primary residence or investment property equity and functions as a revolving credit line. A hard money loan is typically a short-term, asset-based loan from a private lender with higher rates and shorter terms. Hard money is faster to close and credit-agnostic — but far more expensive.

Q: Does applying for a HELOC hurt my credit score?

The hard inquiry from a HELOC application typically drops your score 2–5 points temporarily. If you're rate shopping, do it within a 14–45 day window so multiple inquiries count as one.

Q: What DTI ratio do I need for a HELOC with bad credit?

Most lenders want a debt-to-income ratio below 43%. Some non-QM lenders go up to 50% DTI, but that's the outer limit for most programs.

Q: Can a cosigner help me get a HELOC with bad credit?

Yes, if the lender allows it. A cosigner with a 700+ credit score and low DTI can push a borderline application into approval territory. Not all lenders permit cosigners on HELOCs, so confirm this upfront.

Q: How long after bankruptcy can I get a HELOC?

Most lenders require a waiting period of 2 years after Chapter 13 discharge and 4 years after Chapter 7 discharge. Some non-QM lenders have shorter seasoning requirements — as little as 1–2 years — but rates will reflect the elevated risk.

Q: What's the fastest way to improve my credit score before applying for a HELOC?

Pay down revolving credit card balances (lowering utilization below 30%), dispute any errors on your credit report, and avoid opening new accounts. These three moves, done consistently over 3–6 months, can add 40–80 points to your score.

Conclusion: Your Equity Is the Asset — Use It Strategically

A HELOC with bad credit is not a myth — it's a real product offered by real lenders who are willing to look beyond the FICO score when the equity and income story makes sense. Credit unions, community banks, and non-QM lenders are the primary players in 2026, and they're not as hard to find as the big banks would have you believe.

That said, this is a tool that demands respect. Your home is on the line, rates are elevated, and the wrong approach can make a difficult financial situation worse. The extraordinary borrowers who succeed with bad credit HELOCs are the ones who go in with a clear plan: what the money is for, how it gets repaid, and what the exit strategy looks like.

Your next steps:

- Pull your credit report — identify errors and dispute them before applying

- Calculate your CLTV — know your equity position before talking to any lender

- Contact 2–3 credit unions in your area and ask specifically about their HELOC programs for lower credit scores

- Talk to a mortgage broker who has access to non-QM lenders — they can shop your file without multiple hard inquiries

- Compare a HELOC against alternatives — home equity loan, cash-out refi, or DSCR loan may serve your situation better

- Give it 6 months if you can — even a modest credit score improvement changes your rate dramatically

For investors looking at the broader financing picture, our Best States to Invest in Real Estate 2026 can help you identify where your equity has the most leverage.

The lenders who say yes to a HELOC with bad credit exist. The question is whether you're walking in prepared — or walking in hoping. Preparation wins every time.

Have questions about real estate financing or want to stay current on market trends? Visit Real Estate Rank IQ or reach out at news@realestaterankiq.com. Ranked by brokers. Read by everyone.

{kind=link}