Last updated: May 24, 2026

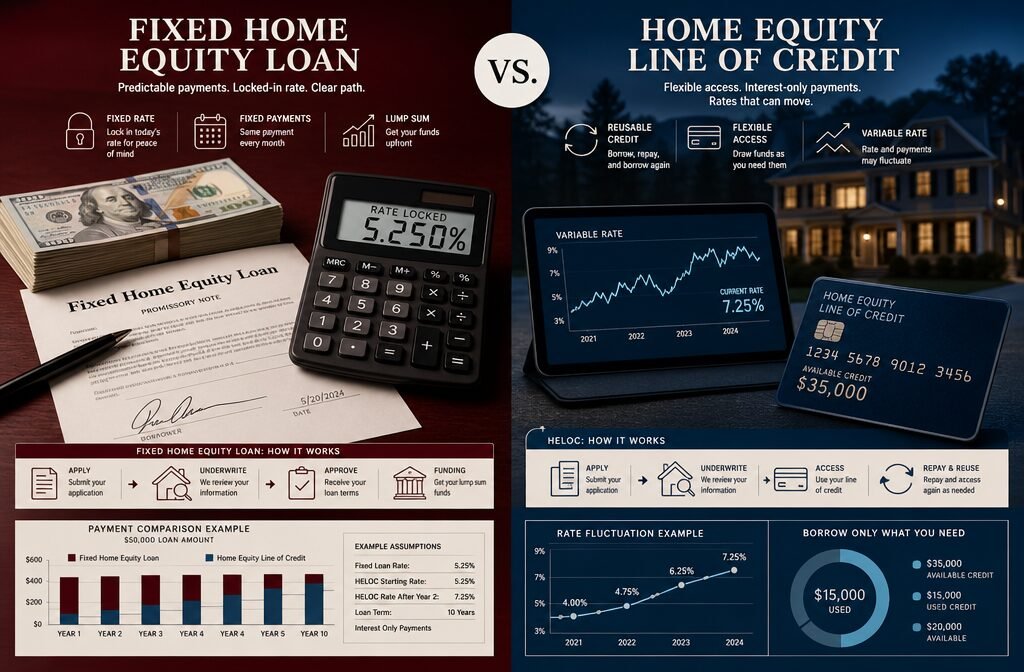

Quick Answer: A HELoan (home equity loan) gives you a lump sum at a fixed interest rate, while a HELOC (home equity line of credit) works like a credit card with a variable rate you draw from as needed. Choosing the wrong one for your situation can cost you thousands in unnecessary interest, fees, or lost flexibility — and in 2026, with HELoan rates around 8% and HELOC rates around 7%, that gap matters more than ever.

Key Takeaways

- A HELoan delivers a one-time lump sum with fixed payments — ideal for single, defined expenses.

- A HELOC is a revolving credit line with a variable rate — better for ongoing or unpredictable costs.

- In 2026, HELoan rates average around 8% and HELOC rates hover near 7%, though both vary by lender and credit profile.

- Both products use your home as collateral — missing payments puts your property at risk.

- Closing costs exist for both options, typically ranging from 2% to 5% of the loan amount.

- Most lenders cap borrowing at 80%–85% of your home's combined loan-to-value (CLTV).

- Credit score requirements differ: HELOCs often require a minimum score of 620–660, while HELoans may accept slightly lower scores depending on the lender.

- Interest may be tax-deductible if funds are used for home improvements — consult a tax professional.

- Real estate investors should weigh both options carefully; a HELOC offers more flexibility for scaling a portfolio.

- Picking the wrong product for your cash flow situation is one of the most expensive mistakes homeowners make.

What Exactly Is a HELoan and How Is It Different From a HELOC?

A HELoan, or home equity loan, is a second mortgage that gives you a fixed lump sum upfront, repaid over a set term at a locked interest rate. A HELOC, or home equity line of credit, is a revolving credit facility secured by your home — you draw what you need, when you need it, and pay interest only on what you've used.

These two products are often lumped together under the umbrella of "home equity borrowing," but they work very differently in practice. Think of a HELoan like buying a flat-screen TV outright — you know the price, you pay it off in installments, done. A HELOC is more like a store credit card tied to your house — flexible, but the rate can move on you.

Key structural differences at a glance:

| Feature | HELoan | HELOC |

|---|---|---|

| Disbursement | Lump sum at closing | Draw as needed during draw period |

| Interest rate | Fixed | Variable (usually tied to Prime Rate) |

| Repayment | Fixed monthly payments | Interest-only during draw period, then full repayment |

| Best for | One-time, defined expenses | Ongoing or phased expenses |

| Rate type | Fixed vs variable home equity | Variable home equity |

| Predictability | High | Lower |

| Typical draw period | N/A | 5–10 years |

| Typical repayment term | 5–30 years | 10–20 years after draw period |

The home equity loan vs HELOC decision isn't just about rates — it's about how you plan to use the money and how much payment certainty you need.

HELoan vs HELOC: The Difference That Costs Borrowers Thousands (Full Breakdown)

This is where the real money is on the table. The HELoan vs HELOC: The Difference That Costs Borrowers Thousands isn't a scare tactic — it's math. Borrowers who pick the wrong product for their situation routinely overpay in interest, get hit with fees they didn't expect, or lose flexibility at the worst possible time.

Here's how the cost difference plays out in a real scenario:

Example: $80,000 borrowed over 10 years

- HELoan at 8% fixed: Monthly payment ≈ $970. Total interest paid ≈ $36,400.

- HELOC at 7% variable (assuming rate holds): Interest-only during a 5-year draw period ≈ $467/month, then full repayment kicks in. If rates rise to 9% during repayment, total interest could exceed $42,000+.

So the HELOC looks cheaper upfront — and it often is, if rates stay low and you manage the draw period well. But if rates climb or you carry a balance longer than planned, the HELoan's fixed structure wins. That's the difference that costs borrowers thousands.

When the HELoan wins:

- You need all the money now (renovation, debt consolidation, large purchase)

- You want payment certainty for budgeting

- You expect rates to rise

When the HELOC wins:

- You need money in phases (multi-stage renovation, business expenses)

- You plan to pay it off quickly

- You want flexibility to borrow only what you need

For a deeper look at how investors specifically use these tools, check out our guide on HELOC on investment property and how smart investors scale.

Which One Has Lower Interest Rates Right Now?

In 2026, HELOC rates are generally lower than HELoan rates — but the gap comes with a catch.

As of May 2026, current home equity rates look roughly like this:

- HELoan rates 2026: Averaging around 8% for well-qualified borrowers

- HELOC rates 2026: Averaging around 7%, though variable and tied to the Prime Rate

The HELOC's lower starting rate is attractive, but it's a variable rate — meaning it moves with the market. If the Federal Reserve raises rates, your HELOC payment goes up. If rates drop, you benefit. It's a two-way street.

The HELoan interest rate is locked from day one. You know exactly what you're paying for the life of the loan. That predictability has real value, especially for borrowers on fixed incomes or tight monthly budgets.

📌 Decision rule: If you think rates will rise over your repayment timeline, the HELoan's fixed rate is worth the premium. If you're confident you'll pay off the balance within 2–3 years, the lower HELOC rate likely saves you money.

For context on how broader financing conditions affect your options, our Real Estate Financing Guide breaks down the full mortgage and equity landscape.

How Much Can You Actually Borrow With Each Option?

Both a HELoan and a HELOC are capped by your available home equity — and most lenders won't let you borrow against all of it.

The standard rule: Lenders typically allow a combined loan-to-value (CLTV) of 80%–85%. That means if your home is worth $400,000 and you owe $250,000 on your mortgage, your available equity is $150,000 — but you can only borrow up to 80%–85% of the home's value total.

Quick math:

- Home value: $400,000

- 80% CLTV cap: $320,000

- Minus existing mortgage: $250,000

- Maximum borrowing: $70,000

This calculation applies to both the home equity credit line vs loan — the cap is the same. What differs is how you access those funds.

Some lenders, particularly for investment properties, may set the CLTV cap lower (70%–75%). If you're a real estate investor looking at your options, the best HELOC lenders for investment property guide covers which lenders are most flexible on these limits.

Edge case: If your home has appreciated significantly since purchase, you may have more borrowing power than you realize. A fresh appraisal can sometimes unlock more equity than an automated valuation model (AVM) shows.

Are There Closing Costs for Home Equity Loans vs Lines of Credit?

Yes — both products carry closing costs, and this is one of the most overlooked expenses in the home equity line of credit vs loan decision.

HELoan closing costs typically run 2%–5% of the loan amount. On an $80,000 loan, that's $1,600–$4,000 paid upfront (or rolled into the loan balance).

HELOC closing costs are generally lower — some lenders advertise "no closing cost" HELOCs — but read the fine print. Those costs are often recouped through slightly higher rates or annual fees. Expect to see:

- Application fees: $0–$500

- Appraisal fees: $300–$700

- Annual fees: $50–$100/year

- Early termination fees if you close the line within 2–3 years

Common mistake: Borrowers focus entirely on the interest rate and ignore closing costs. A HELoan at 8% with $1,500 in closing costs can be cheaper over 5 years than a HELOC at 7% with a $150/year annual fee plus a $500 early closure penalty.

Run the full-cost math, not just the rate comparison.

Who Should Choose a HELoan and Who Should Pick a HELOC?

The HELoan vs HELOC decision really comes down to your financial personality, your project timeline, and your risk tolerance. There's no universally "better" option — but there is a right one for your situation.

Choose a HELoan if:

- You have a single, defined expense (roof replacement, debt payoff, one-time renovation)

- You want fixed monthly payments that never change

- You're on a fixed income or tight budget

- You believe interest rates will rise over your repayment period

- You're a first-time borrower who wants simplicity

Choose a HELOC if:

- You're funding a multi-phase project (staged renovation, business startup costs)

- You want the flexibility to borrow only what you need

- You plan to pay off the balance quickly

- You're a real estate investor who needs a revolving credit tool for deal flow

- You're comfortable with variable rate risk

HELoan vs HELOC for real estate investors deserves its own note: investors often prefer HELOCs because the revolving structure lets them pull equity, buy a property, pay down the line, and repeat. It's a capital recycling strategy. That said, if an investor needs a large, one-time capital injection for a specific acquisition, a HELoan's fixed structure offers cleaner accounting.

If you're weighing how to finance your next investment move, also look at DSCR loan requirements for real estate investors as an alternative that doesn't require using your primary residence as collateral.

What Happens If You Can't Make Payments on a HELoan or HELOC?

Both products use your home as collateral — which means missing payments carries serious consequences. This is not a "so based" moment to be casual about.

If you default on a HELoan, the lender can initiate foreclosure proceedings. Because it's a second mortgage, the primary mortgage lender gets paid first in a foreclosure sale — meaning the HELoan lender may push harder to collect before equity disappears.

If you default on a HELOC, the lender can freeze your line of credit immediately — stopping any further draws — and begin collection or foreclosure proceedings if the default continues.

Key risks to understand:

- HELOC payments can increase sharply when the draw period ends and full principal + interest repayment begins (called "payment shock")

- Variable HELOC rates can push payments higher during rising rate environments

- Both products will damage your credit score if payments are missed

📌 Edge case: Some HELOCs allow interest-only payments during the draw period. Borrowers who get comfortable paying only interest for 10 years can be blindsided when the repayment phase starts and payments jump significantly. Plan for this from day one.

Common Mistakes People Make When Deciding Between HELoan and HELOC

The HELoan vs HELOC: The Difference That Costs Borrowers Thousands isn't always about rates — sometimes it's about avoidable decisions made before the ink dries.

Mistake #1: Choosing a HELOC for a one-time expense

If you know exactly what you need and when, a HELOC's flexibility is wasted — and you're paying for the variable rate risk with no upside.

Mistake #2: Choosing a HELoan for a phased project

Borrowing $100,000 upfront for a renovation that costs $30,000 now and $70,000 over two years means paying interest on $70,000 you haven't spent yet.

Mistake #3: Ignoring the HELOC repayment phase

The draw period feels manageable. The repayment phase can be brutal if you've maxed the line and rates have moved up.

Mistake #4: Not shopping multiple lenders

HELoan and HELOC rates vary significantly between banks, credit unions, and online lenders. A difference of 0.5% on an $80,000 loan over 10 years is roughly $4,000 in interest.

Mistake #5: Forgetting about closing costs

As covered above — the "no closing cost" HELOC isn't free. It's just structured differently.

Mistake #6: Using home equity for depreciating assets

Borrowing against your home to buy a car or fund a vacation is a financial move that doesn't add up. Home equity is a long-term asset — use it for things that build value or reduce higher-cost debt.

Let it cook before you see results — home equity strategies take time to pay off, and the borrowers who win are the ones who plan the full repayment arc, not just the first payment.

Can You Use a Home Equity Loan or HELOC for Home Renovations?

Absolutely — and this is one of the most popular and financially sound uses for both products. Home renovations funded through home equity borrowing can increase your property's value, which builds the equity back over time.

HELoan for renovations: Best for a single, fully scoped project with a known budget. You get all the money upfront, contractors get paid on schedule, and your payment is fixed.

HELOC for renovations: Best for phased projects where costs come in stages — demo first, then framing, then finishes. You draw as invoices come in and only pay interest on what you've used.

For renovation planning tools, our roundup of the best apps for home renovations can help you scope and budget your project before you borrow.

Important: The IRS has historically allowed a tax deduction on interest paid for home equity debt used to "buy, build, or substantially improve" the home securing the loan (subject to limits). This is a fresh advantage of renovation-focused borrowing — but tax law changes, so verify with a CPA before assuming deductibility.

What Are the Tax Implications of Borrowing With Each Method?

The tax treatment of HELoan vs HELOC interest is one area where many borrowers are gate keeping themselves from real savings — simply because they don't ask.

The general rule (as of 2026): Interest on home equity debt is deductible only if the funds are used to buy, build, or substantially improve the home that secures the loan. This applies to both HELoans and HELOCs equally.

What's NOT deductible:

- Using home equity to pay off credit card debt

- Using it for a vacation, car, or personal expenses

- Using it for investment properties (different rules apply — consult a tax advisor)

What IS potentially deductible:

- Kitchen remodel funded by a HELoan

- Bathroom addition funded through a HELOC draw

- Major structural repairs using either product

The deduction limit applies to combined mortgage debt up to $750,000 (for loans originated after December 15, 2017, under the Tax Cuts and Jobs Act). Amounts above that threshold don't qualify.

📌 Always consult a licensed CPA or tax professional before making borrowing decisions based on expected tax benefits. Tax law is not static.

How Do Credit Score Requirements Differ Between These Two Options?

Credit score requirements for HELoans and HELOCs are similar but not identical — and your score has a direct impact on the rate you'll receive.

Typical minimums:

- HELoan: Most lenders require a minimum credit score of 620, though scores of 700+ get the best rates

- HELOC: Minimum scores typically start at 620–660, with premium rates reserved for 720+ borrowers

What else lenders evaluate:

- Debt-to-income ratio (DTI): Most lenders want DTI below 43%

- Combined loan-to-value (CLTV): As discussed, typically capped at 80%–85%

- Employment and income verification

- Payment history on existing mortgage

Edge case for self-employed borrowers: Proving income can be more complex. Lenders may require two years of tax returns, profit-and-loss statements, or bank statements. Some non-QM lenders offer bank statement HELoans for self-employed borrowers, though rates are higher.

If you're comparing financing options and want to understand how credit scores affect your mortgage costs more broadly, our FHA Loan vs Conventional Loan comparison is a solid place to build your knowledge base.

When Does a HELOC Make More Financial Sense Than a Fixed Home Equity Loan?

A HELOC makes more financial sense than a fixed HELoan in four specific scenarios.

1. You need phased funding. If your project or expense rolls out over 12–24 months, a HELOC lets you draw only what you need and avoid paying interest on unused funds.

2. You plan to repay quickly. If you expect to pay off the balance within 2–3 years, the lower HELOC rate (around 7% in 2026) saves money compared to the HELoan rate (around 8%), even accounting for variable rate risk.

3. You're a real estate investor recycling capital. The revolving structure of a HELOC is impeccable for investors who buy, improve, and refinance or sell properties. You draw, deploy, repay, and draw again — without reapplying for a new loan each time.

4. You want a financial safety net. A HELOC with a $100,000 limit that you don't fully use still gives you access to capital in an emergency. A HELoan gives you all the money (and all the debt) whether you need it or not.

For investors specifically, pairing a HELOC strategy with cash-flow analysis is extraordinary — our guide on cash flow real estate investing explains how to run those numbers before you borrow.

How Quickly Can You Get Funds With a HELoan vs a HELOC?

Both products take time — this is not a same-day funding situation. But there are meaningful differences in speed and access once approved.

HELoan funding timeline:

- Application to closing: typically 2–6 weeks

- Funds disbursed: as a lump sum at closing

- There is a mandatory 3-business-day right of rescission after closing before funds are released (for primary residences)

HELOC funding timeline:

- Application to approval: typically 2–6 weeks (similar to HELoan)

- Once the line is open: funds are accessible immediately via checks, a debit card, or online transfer

- Ongoing access: draw anytime during the draw period without reapplying

The practical difference: A HELOC wins on ongoing speed. Once it's open, accessing $10,000 takes minutes. A HELoan requires a full new application each time you need additional funds.

For urgent capital needs, neither product is fast enough to compete with a personal loan or hard money lender. But for planned expenses, both are impeccable tools when set up in advance.

FAQ: HELoan vs HELOC

Q: What is a HELoan?

A HELoan is a home equity loan — a second mortgage that gives you a fixed lump sum at a fixed interest rate, repaid in equal monthly installments over a set term (typically 5–30 years).

Q: Is a HELOC or home equity loan better for debt consolidation?

A HELoan is generally better for debt consolidation because you receive the full payoff amount upfront at a fixed rate, making it easy to eliminate high-interest debt in one move. A HELOC works but requires more discipline since the credit line stays open.

Q: Can I have both a HELoan and a HELOC at the same time?

Yes, technically — but your combined borrowing is still capped by your CLTV limit. Having both simultaneously reduces how much you can access through each.

Q: What's the difference between a home equity line of credit vs a loan for investment properties?

For investment properties, lenders apply stricter CLTV caps (often 70%–75%) and higher rate premiums. HELOCs on investment properties are less common but available through specialized lenders. HELoans on investment properties are more widely offered.

Q: Do HELOCs have prepayment penalties?

Some HELOCs include early closure fees if you close the line within 2–3 years of opening it. Always check the terms before signing.

Q: How does a variable HELOC rate actually change?

Most HELOCs are tied to the U.S. Prime Rate. When the Federal Reserve adjusts the federal funds rate, the Prime Rate typically moves with it, and your HELOC rate adjusts accordingly — usually within one billing cycle.

Q: Can I deduct HELoan interest on my taxes?

Only if the funds were used to buy, build, or substantially improve the home securing the loan. Personal expenses, debt consolidation, and investment property uses generally don't qualify. Consult a tax professional.

Q: What credit score do I need for a HELOC in 2026?

Most lenders require a minimum score of 620–660 for a HELOC. To get the best rates (around 7% in 2026), aim for 720 or higher.

Q: What's the maximum I can borrow with a home equity loan?

Most lenders cap borrowing at 80%–85% of your home's value, minus your existing mortgage balance. On a $400,000 home with a $250,000 mortgage, the maximum is roughly $70,000–$90,000 depending on the lender's CLTV limit.

Q: Is a HELOC considered a second mortgage?

Yes. Both a HELoan and a HELOC are second mortgages — they're secured by your home and sit behind your primary mortgage in the lien priority order.

Conclusion: Make the Right Call Before It Costs You

The HELoan vs HELOC: The Difference That Costs Borrowers Thousands is real — and it plays out in interest paid, fees absorbed, and flexibility lost when borrowers pick the wrong product for their situation.

Here's the short version:

- Need a lump sum for a defined expense and want payment certainty? The HELoan at around 8% fixed is your move.

- Need phased access to capital and plan to repay quickly? The HELOC at around 7% variable likely saves you money.

- Real estate investor recycling equity across deals? The HELOC's revolving structure is built for you.

- Self-employed or complex income? Shop non-QM lenders and prepare your documentation in advance.

Your next steps:

- Pull your current mortgage balance and get a home value estimate — calculate your available equity before you talk to a lender.

- Define exactly how you'll use the funds and whether the expense is one-time or phased.

- Get quotes from at least 3 lenders — banks, credit unions, and online lenders — and compare the full cost (rate + closing costs + fees).

- Consult a CPA if you're expecting to deduct the interest.

- Read the fine print on HELOC draw periods, repayment terms, and early closure fees before signing.

The brokers at Real Estate Rank IQ have seen borrowers leave thousands on the table by rushing this decision. Don't be that borrower. Let it cook before you see results — do the math, compare the full cost, and pick the product that actually fits your financial life.

For more on financing strategies that work in 2026, explore our mortgage broker vs direct lender comparison and the full real estate financing guide.

{kind=link}