Last updated: May 24, 2026

Quick Answer: The best mortgage lenders for first-time investors in 2026 are those offering DSCR loans, non-QM products, or investor-friendly conventional financing with fast digital underwriting. Lenders like Kiavi, LendingOne, Visio Lending, Griffin Funding, and Angel Oak Mortgage consistently approve investment property loans faster than traditional banks — often within 5 to 15 business days. The key is matching your financial profile to the right loan type before you apply.

Key Takeaways 🏠

- Credit score minimums for investment property loans typically start at 620 for conventional and 640–680 for DSCR and non-QM products.

- Down payments for first-time investors run 15–25% for conventional loans; DSCR lenders may require 20–25%.

- DSCR loans qualify you based on rental income, not personal income — a major advantage for self-employed borrowers.

- FHA loans can be used on 2–4 unit properties if you occupy one unit, making them a legitimate entry point for first-time investors.

- Interest rates on investment properties typically run 0.5–0.75 percentage points higher than primary residence rates.

- Cash reserves of 6 months of PITI (principal, interest, taxes, insurance) are commonly required per investment property.

- Non-QM lending growth in 2026 has expanded options significantly for investors with non-traditional income.

- Fastest approvals come from online-first lenders with automated underwriting — not brick-and-mortar banks.

- The 6% mortgage rate as the new norm in 2026 means your debt service calculations matter more than ever.

- Common mistakes include applying with the wrong lender type, underestimating reserves, and skipping pre-approval.

Best Mortgage Lenders for First-Time Investors: Who Approves Fast in 2026

Finding the best mortgage lenders for first-time investors comes down to three things: loan product fit, speed of underwriting, and how much flexibility the lender gives borrowers who don’t fit the traditional W-2 mold. In 2026, that flexibility is everything.

The 6% mortgage rate as the new norm has shifted how investors run their numbers. With rates stabilizing in the mid-to-upper 6% range for investment properties, the lender you choose — and how fast they move — can be the difference between closing a deal and losing it to a cash buyer.

Here’s a breakdown of the lenders earning the most respect from first-time real estate investors right now:

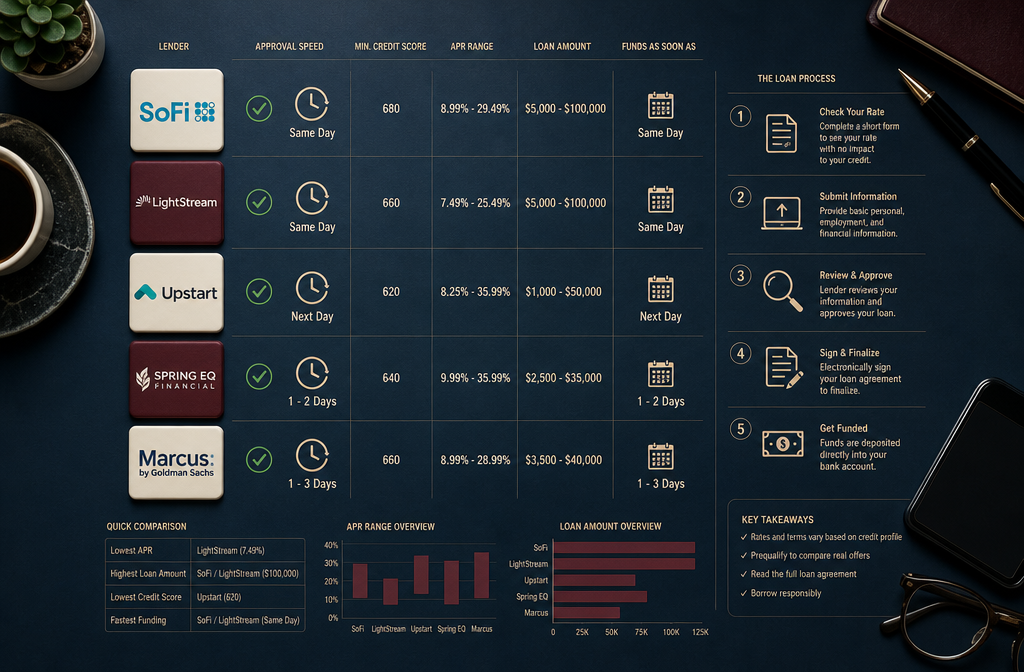

Kiavi (Formerly LendingHome)

Kiavi is one of the most investor-friendly hard money lenders for beginners in the country. They specialize in fix-and-flip and rental property financing, with approvals that can come through in as little as 5–7 business days. Their rental loan product is DSCR-based, meaning your personal income doesn’t drive the decision — the property’s cash flow does. Minimum credit score: 660. Down payment: 20–25%.

LendingOne

LendingOne is a direct private lender focused exclusively on real estate investors. They offer bridge loans, rental loans, and new construction financing. First-time investors appreciate their straightforward qualification process and dedicated loan advisors. Approval timelines typically run 7–14 business days. They’re so based when it comes to investor education — their team actually explains the product instead of just pushing you through.

Visio Lending

Visio Lending is one of the most recognized names in DSCR loan rates 2026. They lend exclusively on residential investment properties and vacation rentals, with no personal income verification required. Loan amounts range from $100K to $2M. Minimum DSCR of 1.0 (meaning rent covers the mortgage payment). Approval in roughly 10–21 business days.

Griffin Funding

Griffin Funding offers an extraordinary range of non-QM mortgage products — bank statement loans, asset-based loans, DSCR loans, and more. They’re a strong pick for self-employed investors or high-income professionals with complex tax returns. Their team moves fast and their product menu is one of the widest in the non-QM space.

Angel Oak Mortgage

Angel Oak Mortgage is one of the pioneers of non-QM lending and has been expanding aggressively through non-QM lending growth in 2026. They offer DSCR loans, bank statement loans, and investor cash flow products. Credit score minimums start around 640. They’re particularly strong for investors buying in competitive markets who need a lender that can move.

Rocket Mortgage (Investor Products)

Rocket Mortgage investor products are best for first-time investors who want the comfort of a major brand with digital speed. Rocket offers conventional investment property loans with fast online processing. They’re not a DSCR lender, so you’ll need to qualify on personal income — but their underwriting timeline is among the fastest for conventional investment home financing.

Better Mortgage (Investor Conventional Loans)

Better Mortgage investor loans work well for straightforward single-family rental purchases where the borrower has strong W-2 income. Their fully digital process can get you to pre-approval in under 24 hours. They’re not the pick for complex investor scenarios, but for a clean deal? Impeccable speed.

Choose based on your profile:

- Self-employed or complex income → Griffin Funding, Angel Oak, Visio

- Fix-and-flip or short-term rental → Kiavi, LendingOne

- Clean W-2 income, single-family rental → Rocket Mortgage, Better Mortgage

- Scaling a rental portfolio → Visio Lending, LendingOne

For a deeper comparison of how working with a broker vs. going direct affects your rate and speed, check out our guide on mortgage broker vs. direct lender options for investors.

What Credit Score Do You Need to Qualify for an Investment Property Loan?

Most investment property loans require a minimum credit score of 620–680, depending on the loan type. Conventional loans through Fannie Mae start at 620, but expect better rates and fewer overlays at 680+. DSCR lenders and non-QM mortgage lenders typically want 640–680 minimum, with the best pricing reserved for scores above 720.

Here’s a practical breakdown:

| Loan Type | Minimum Credit Score | Ideal Score for Best Rates |

|---|---|---|

| Conventional (Fannie/Freddie) | 620 | 740+ |

| DSCR Loan | 640–680 | 720+ |

| Hard Money / Bridge | 600–620 | 660+ |

| Non-QM (Bank Statement) | 640 | 700+ |

| FHA (Owner-Occupied Multi-Unit) | 580 (3.5% down) | 620+ |

Common mistake: Applying for an investment property loan with a score in the low 600s and expecting conventional pricing. You’ll either get denied or pay a significant rate premium. Pull your credit 60–90 days before applying and clean up any errors or high utilization.

How Much Down Payment Do First-Time Real Estate Investors Typically Need?

First-time investors should plan for a 15–25% down payment on most investment property loans. Conventional loans allow 15% down on single-family investment properties in some cases, but 20–25% is the standard for avoiding heavy pricing adjustments. DSCR lenders and non-QM lenders almost universally require 20–25%.

- Single-family rental (conventional): 15–20% minimum

- 2–4 unit investment property: 20–25%

- DSCR loan: 20–25%

- Hard money / bridge loan: 10–30% (varies widely by lender and deal)

- FHA (owner-occupied 2–4 unit): 3.5% with 580+ credit score

The FHA path is the most overlooked entry point for first-time investors. If you’re willing to live in one unit of a duplex, triplex, or fourplex, you can put as little as 3.5% down and let the rental income from the other units offset your mortgage. That’s not gatekeeping — that’s just how the program works, and most people don’t use it.

For more on getting into investment real estate with limited capital, see how to invest in real estate with $5,000 or less in 2026.

Which Online Lenders Have the Fastest Mortgage Approval Process?

Online-first lenders consistently beat traditional banks on speed for investment property loans. The fastest approvals in 2026 come from lenders with automated underwriting systems and dedicated investor loan teams.

Fastest approval timelines by lender type:

- Hard money lenders (Kiavi, LendingOne): 5–15 business days

- DSCR lenders (Visio, Griffin Funding): 10–21 business days

- Non-QM lenders (Angel Oak): 14–21 business days

- Online conventional lenders (Rocket, Better): 21–30 business days

- Traditional banks and credit unions: 30–45+ business days

Speed matters in competitive markets. In 2026, investor share of homes in many metros remains elevated, meaning you’re often competing against experienced buyers who close fast. A lender that takes 45 days is a liability.

What speeds up your approval:

- Having all documents ready before you apply (more on that below)

- Choosing a lender that specializes in investor loans — not a general mortgage company

- Getting pre-approved before you’re under contract

- Responding to underwriter requests within 24 hours

Are There Special Mortgage Programs for First-Time Real Estate Investors?

There’s no single government-backed program exclusively for first-time real estate investors the way there is for first-time homebuyers. But several loan products are specifically built for investors — and a few standard programs have investor-friendly features worth knowing.

Programs and products worth knowing:

- DSCR loans: Qualify based on rental income, not personal income. No tax returns, no W-2s. This is the most investor-friendly product category in 2026.

- FHA multi-unit loans: Buy a 2–4 unit property, live in one unit, and rent the rest. Low down payment, government-backed. Best entry point for first-timers.

- Portfolio loans: Held by the lender rather than sold to Fannie/Freddie. More flexible underwriting, but typically higher rates.

- Bank statement loans: For self-employed investors who can’t show traditional income on tax returns. Qualify using 12–24 months of bank deposits.

- Asset depletion loans: Qualify using liquid assets (investment accounts, savings) rather than income. Strong option for high-net-worth investors who are semi-retired or have irregular income.

For a full breakdown of DSCR products specifically, our DSCR loan requirements guide covers exactly what you need to qualify.

How Much Higher Are Interest Rates for Investment Property vs. Primary Residence?

Investment property mortgage rates run approximately 0.5–0.75 percentage points higher than primary residence rates for conventional loans. For DSCR and non-QM products, the spread can be 1.0–2.0 percentage points above a standard 30-year fixed rate.

With the 6% mortgage rate as the new norm for primary residences in 2026, that means:

- Conventional investment property: Roughly 6.5–7.0%

- DSCR loan: Roughly 7.0–8.5% depending on credit, LTV, and DSCR ratio

- Hard money / bridge loan: 9.0–12%+ (short-term, asset-based)

- Non-QM bank statement: 7.5–9.0%

The rate premium exists because investment properties carry higher default risk in the eyes of lenders — borrowers are more likely to walk away from a rental than their primary home during financial stress.

How to get the best rate:

- Put 25–30% down (reduces lender risk)

- Score above 740

- Show strong DSCR (1.25 or higher is ideal)

- Compare at least 3–5 lenders — rate variation between lenders on the same product can be 0.5–1.0%

For current rate context, our DSCR loan lenders ranked and reviewed article has fresh 2026 data.

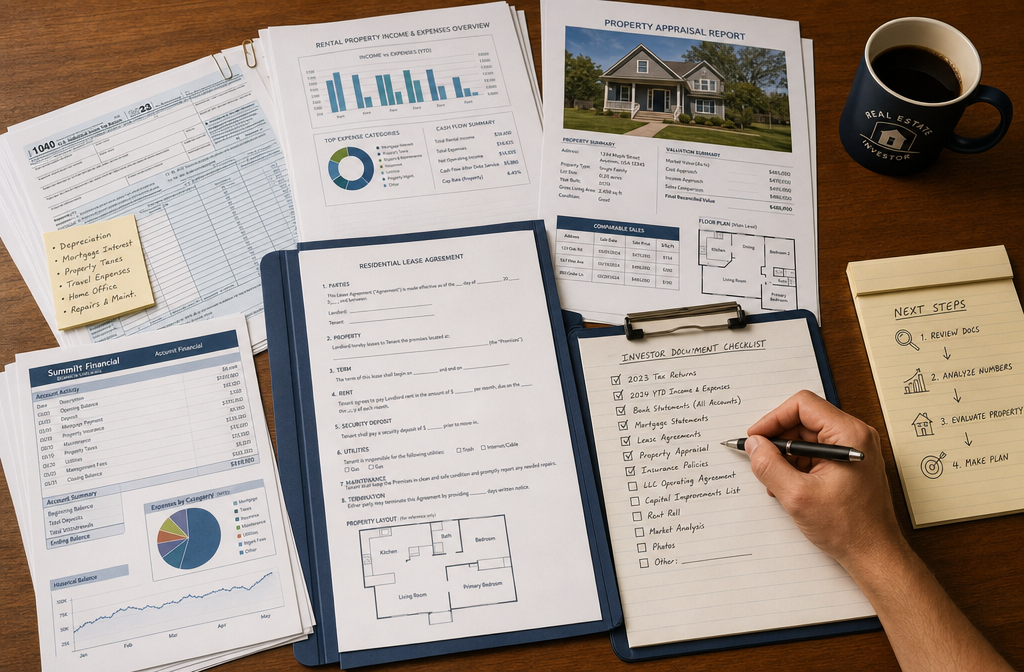

What Documents Do You Need to Get Approved for an Investment Property Mortgage?

For conventional investment loans, expect to provide two years of tax returns, W-2s or 1099s, two months of bank statements, and documentation of all existing properties. For DSCR loans, the document list is significantly shorter — primarily the lease agreement or rental income projection, a property appraisal, and proof of insurance.

Conventional investment property — document checklist:

- Last 2 years of federal tax returns (personal and business if self-employed)

- Last 2 years of W-2s or 1099s

- Last 2–3 months of bank statements

- Proof of down payment and reserves

- Signed purchase contract

- Property appraisal (ordered by lender)

- Rental income documentation (Schedule E if existing rental)

- HOA documents (if applicable)

- Insurance binder

DSCR loan — simplified document checklist:

- Lease agreement or market rent analysis

- Property appraisal

- 2–3 months of bank statements (for reserves verification)

- Entity documents (if purchasing in LLC)

- Insurance binder

- Credit authorization

Pro tip: If you’re buying in an LLC — which many investors do for liability protection — confirm your lender accepts LLC borrowers before you apply. Some conventional lenders don’t. Most DSCR and non-QM lenders do.

Can You Use FHA Loans for a Multi-Unit Property as a First-Time Investor?

Yes — FHA loans can be used to purchase 2, 3, or 4-unit properties as long as the borrower occupies one of the units as their primary residence. This is one of the most underused strategies for first-time investors, and it’s so based that more people aren’t talking about it.

FHA multi-unit basics:

- Property types: 2-unit (duplex), 3-unit (triplex), 4-unit (fourplex)

- Down payment: 3.5% with 580+ credit score; 10% with 500–579

- Rental income: Up to 75% of projected rental income from the non-owner-occupied units can be counted toward qualification

- Occupancy requirement: Must live in one unit for at least 12 months

- Loan limits: Vary by county; FHA limits for multi-unit are higher than single-family limits

Example: A duplex in a mid-tier market priced at $400,000 with market rent of $1,800/month on the second unit. With FHA, you could put down $14,000 (3.5%), count $1,350/month of that rent toward your qualifying income, and effectively have a tenant helping cover your mortgage from day one.

For a deeper look at multifamily investing math, our apartment investing numbers guide breaks it all down.

What Are the Biggest Mistakes First-Time Real Estate Investors Make With Financing?

The biggest financing mistakes first-time investors make are applying with the wrong lender type, underestimating cash reserve requirements, and treating the mortgage rate as the only cost that matters. These mistakes don’t just slow deals down — they kill them.

The most common financing mistakes:

- Applying to a retail bank for an investor loan. Traditional banks are slow, conservative, and often unfamiliar with DSCR or non-QM products. You’ll waste weeks and possibly damage your credit with hard inquiries.

- Not accounting for reserves. Lenders require 6 months of PITI in liquid reserves per investment property. If you’re buying a $300K property with a $1,800/month payment, you need $10,800 in reserves — on top of your down payment and closing costs.

- Buying in an LLC without checking lender requirements first. Many conventional lenders won’t lend to an LLC. You may need to buy personally and transfer to an LLC later (check with a real estate attorney on the due-on-sale clause implications).

- Ignoring closing costs. Investment property closing costs run 2–5% of the purchase price. On a $350K property, that’s $7,000–$17,500 out of pocket.

- Not comparing lenders. The first lender you talk to is rarely the best one. Rate and fee differences between lenders on the same loan can cost or save you thousands over the life of the loan.

- Skipping pre-approval. Sellers — especially those dealing with investors — want to see proof you can close. No pre-approval letter means you’re not a serious buyer.

For a broader look at the investment strategy side, our beginner’s blueprint for real estate investing covers the full picture.

How Much Cash Reserves Do Lenders Require for Investment Property Loans?

Most lenders require 6 months of PITI (principal, interest, taxes, and insurance) in liquid reserves for each investment property in your portfolio. For first-time investors with one property, that’s 6 months of the new property’s payment. If you already own your primary residence, some lenders also want 2–6 months of reserves for that property too.

Reserve requirements by lender type:

| Lender Type | Typical Reserve Requirement |

|---|---|

| Conventional (Fannie/Freddie) | 6 months PITI per investment property |

| DSCR Lenders | 3–6 months PITI |

| Hard Money / Bridge | Varies; often less strict |

| Portfolio Lenders | 3–12 months (lender discretion) |

What counts as reserves:

- Checking and savings accounts ✅

- Money market accounts ✅

- Retirement accounts (typically 60–70% of vested balance) ✅

- Stocks and bonds (typically 70% of value) ✅

- Cash in hand ❌ (not verifiable)

- Gift funds ❌ (generally not acceptable for reserves)

What’s the Difference Between Conventional and Portfolio Investment Loans?

Conventional investment loans follow Fannie Mae or Freddie Mac guidelines and are sold on the secondary market. Portfolio loans are held by the lender and follow the lender’s own underwriting rules — which means more flexibility but often higher rates.

Conventional loans:

- Follow strict Fannie/Freddie guidelines

- Lower rates (tied to secondary market pricing)

- Stricter income, credit, and reserve requirements

- Fannie Mae caps investors at 10 financed properties

- Require standard documentation (tax returns, W-2s)

Portfolio loans:

- Lender sets their own rules

- More flexible on income documentation, credit, and property condition

- Higher rates (lender takes on full default risk)

- No cap on financed properties (lender decides)

- Common for investors scaling beyond 4–10 properties

DSCR loans are technically a type of portfolio or non-QM loan — they qualify based on the property’s income, not the borrower’s personal income. They’re the fastest-growing product category for real estate investment lenders in 2026 for good reason.

Choose conventional if: You have clean W-2 income, strong credit, and are buying your first 1–4 investment properties.

Choose portfolio/DSCR if: You’re self-employed, have complex income, own multiple properties, or want to scale without hitting Fannie Mae’s 10-property cap.

How Long Does Mortgage Underwriting Typically Take for Investment Properties?

Investment property underwriting takes longer than primary residence loans because lenders do additional analysis on rental income, property condition, and borrower reserves. Expect 21–45 days for conventional loans and 10–21 days for DSCR and non-QM products through specialized lenders.

Underwriting timeline by loan type:

- Hard money / bridge loan: 5–15 business days

- DSCR loan (specialized lender): 10–21 business days

- Non-QM (bank statement, asset depletion): 14–21 business days

- Conventional investment loan (online lender): 21–30 business days

- Conventional investment loan (traditional bank): 30–45+ business days

What slows underwriting down:

- Missing or incomplete documents

- Appraisal delays (especially in rural or low-comp markets)

- Title issues on the subject property

- Borrower response time to conditions

- Complex income structures requiring additional review

What speeds it up:

- Using a lender that specializes in investor loans

- Having a complete document package ready before application

- Choosing a property in a market with strong comparable sales for the appraiser

Which Banks Are Most Friendly to New Real Estate Investors With Limited History?

Specialized non-bank lenders — not traditional banks — are the most investor-friendly options for borrowers with limited investment history. Kiavi, LendingOne, Visio Lending, Griffin Funding, and Angel Oak Mortgage are consistently cited as the most accessible real estate investment lenders for first-timers.

Traditional banks like Chase, Wells Fargo, and Bank of America do offer investment property loans, but their underwriting is conservative, their approval timelines are long, and their loan officers often have limited experience with investor-specific products like DSCR or portfolio loans.

Best lenders for investors with limited history:

| Lender | Best For | Min. Credit | Speed |

|---|---|---|---|

| Kiavi | Fix-and-flip, rental DSCR | 660 | 5–15 days |

| LendingOne | Bridge + rental loans | 620 | 7–14 days |

| Visio Lending | Long-term rental DSCR | 680 | 10–21 days |

| Griffin Funding | Non-QM, bank statement | 640 | 14–21 days |

| Angel Oak Mortgage | Non-QM, DSCR | 640 | 14–21 days |

| Rocket Mortgage | Conventional investment | 620 | 21–30 days |

Note: Lender minimums and timelines shift with market conditions. Always verify current requirements directly with the lender before applying.

Can You Use Rental Income to Help Qualify for the Mortgage?

Yes — rental income can be used to qualify for an investment property mortgage, but the rules vary significantly by loan type. For conventional loans, lenders typically count 75% of documented rental income (from a signed lease or Schedule E). For DSCR loans, the property’s rental income is the primary qualification factor.

How rental income is counted:

- Conventional (existing rental with lease): 75% of gross rent added to qualifying income

- Conventional (new purchase, no lease yet): Lender uses appraiser’s market rent estimate, counts 75%

- DSCR loan: Rental income divided by PITIA (principal, interest, taxes, insurance, association dues) = DSCR ratio. Need 1.0–1.25+ to qualify

- FHA multi-unit (owner-occupied): Up to 75% of projected rent from non-owner units counted

DSCR example:

- Monthly rent: $2,200

- Monthly PITIA: $1,800

- DSCR: 2,200 ÷ 1,800 = 1.22

A DSCR of 1.22 means the property generates 22% more income than it costs to carry. Most DSCR lenders want a minimum of 1.0–1.25. The higher the ratio, the better your rate and terms.

This is why DSCR loans are extraordinary for self-employed investors and those with high write-offs on their taxes — the property’s income does the heavy lifting, not your personal return.

For more on how to analyze a property’s income before you apply, check out our rental property analysis checklist.

FAQ: Best Mortgage Lenders for First-Time Investors

Q: What’s the minimum credit score to get approved for an investment property loan?

Most investment property loans require a minimum of 620–680, depending on the loan type. Conventional loans start at 620; DSCR and non-QM lenders typically want 640–680 minimum.

Q: Can a first-time investor get a DSCR loan?

Yes. DSCR lenders don’t require prior landlord experience. They qualify the loan based on the property’s rental income, not your investment history. First-timers use DSCR loans regularly.

Q: How many investment properties can I finance with conventional loans?

Fannie Mae allows up to 10 financed properties. After that, you’ll need portfolio loans, DSCR products, or commercial financing to continue scaling.

Q: Is it harder to get approved for an investment property than a primary home?

Yes. Investment property loans require higher credit scores, larger down payments, and more cash reserves than primary residence loans. The approval process is also more detailed.

Q: Can I use a HELOC on my primary home to fund the down payment on an investment property?

Yes — and many investors do exactly this. A HELOC on your primary residence can provide the down payment capital for a rental property. Our guide on HELOC strategies for investment properties covers this in detail.

Q: What’s the fastest way to get pre-approved for an investment property loan?

Apply with an online-first lender that specializes in investor loans (Kiavi, LendingOne, Griffin Funding). Have your full document package ready before you apply. Pre-approval can come through in 24–72 hours for DSCR products.

Q: Do I need an LLC to buy a rental property?

No — you can buy in your personal name. Many first-time investors do. If you want to buy in an LLC, make sure your lender accepts LLC borrowers before you apply, since most conventional lenders don’t.

Q: What is a good DSCR ratio for getting approved?

A DSCR of 1.25 or higher is considered strong. A ratio of 1.0 means break-even (rent covers the mortgage exactly). Some lenders approve at 1.0; others require 1.2 or 1.25 minimum.

Q: Are hard money loans a good option for first-time investors?

Hard money loans are short-term, asset-based loans best suited for fix-and-flip projects or bridge situations. They’re not ideal for long-term holds due to high rates (9–12%+). For a buy-and-hold strategy, DSCR or conventional loans are better fits.

Q: How do investment property mortgage rates in 2026 compare to 2023?

Rates have stabilized compared to the rapid increases of 2022–2023. In 2026, the 6% mortgage rate as the new norm for primary residences means investment properties are generally pricing in the 6.5–8.5% range depending on loan type — lower than the 2023 peaks for most products.

Conclusion: Let It Cook Before You See Results

Getting the right mortgage as a first-time investor isn’t about finding a magic lender — it’s about knowing which loan product fits your profile and then moving with intention. The best mortgage lenders for first-time investors in 2026 are the ones who specialize in investor financing, move fast, and don’t require you to have a perfect tax return to get a yes.

If you’re self-employed or have complex income, DSCR and non-QM lenders like Visio, Griffin Funding, and Angel Oak are your lane. If you have clean W-2 income and want the lowest rate, conventional products through Rocket or Better Mortgage will serve you well. And if you’re just getting started with limited capital, the FHA multi-unit path is genuinely underrated.

Your next steps:

- Pull your credit — know your score and fix any errors before you apply.

- Calculate your reserves — make sure you have 6 months of PITI plus down payment plus closing costs liquid.

- Choose your loan type — DSCR, conventional, FHA multi-unit, or non-QM based on your income profile.

- Compare at least 3 lenders — rate and fee differences are real and worth the extra call.

- Get pre-approved before you shop — serious sellers and listing agents expect it.

The investors who build impeccable portfolios aren’t the ones who move the fastest. They’re the ones who prepare the best, choose the right financing tools, and let it cook before they see results. Start there.

For more investor resources, explore our Investment Hub or check out the best states to invest in real estate in 2026 for market-specific data to back your next move.

{kind=link}