{"cover":"Professional landscape format (1536×1024) editorial hero image showing a confident real estate investor reviewing loan documents at a modern desk, with a calculator, architectural blueprints, and stacks of cash visible. Background features a blurred urban skyline through floor-to-ceiling windows. Color palette: deep burgundy red, rich black, and cream white. Dramatic side lighting creates depth. No text overlays. Magazine cover aesthetic, cinematic quality, high contrast.","content":["Landscape format (1536×1024) split-screen infographic illustration comparing a hard money loan structure versus a traditional bank mortgage. Left side shows a private lender handing keys directly to an investor with a stopwatch showing 7 days. Right side shows a bank building with a long approval queue and 30-day calendar. Clean financial graphic style, burgundy and navy color scheme, minimal annotation labels on each side, white background, editorial quality.","Landscape format (1536×1024) detailed cost breakdown visual showing a real estate investor studying a fee itemization sheet. Foreground displays a large financial breakdown chart with labeled line items: origination fees 2-4 points, interest rate 10-15%, closing costs, prepayment penalties. A magnifying glass hovers over the numbers. Warm office lighting, cream and burgundy tones, realistic editorial photography style, no large text overlays, professional financial setting.","Landscape format (1536×1024) dramatic wide-angle shot of a distressed fixer-upper property being renovated, with construction workers visible. In the foreground, an investor holds a tablet displaying a fix-and-flip profit projection spreadsheet with before-and-after property photos side by side. Golden hour lighting, gritty urban neighborhood backdrop, navy and cream color tones, photojournalistic editorial quality, small data labels visible on the tablet screen only.","Landscape format (1536×1024) conceptual comparison visual showing four distinct financing paths laid out as road signs at an intersection: Hard Money, DSCR Loan, HELOC, and Crowdfunding. A real estate investor stands at the crossroads studying a map. Background shows a suburban neighborhood with mixed property types. Aerial perspective, clean graphic overlay on realistic photography, burgundy accent colors on signage, editorial magazine quality, no large headline text."]

Last updated: May 24, 2026

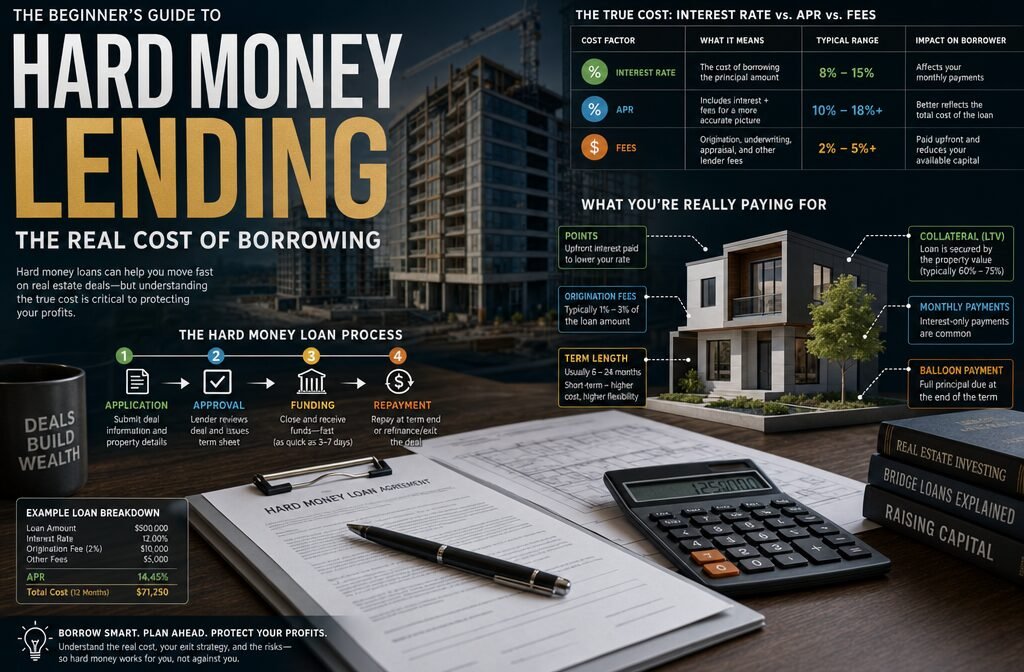

Quick Answer: Hard money loans are short-term, asset-based loans from private lenders — not banks — that use real estate as collateral. They typically carry interest rates between 10% and 15%, fund in as little as 5 to 10 business days, and are designed for investors who need speed over low cost. For beginners, the real cost goes well beyond the interest rate and includes origination fees, points, closing costs, and extension fees that can add up fast if you're not paying attention.

Key Takeaways

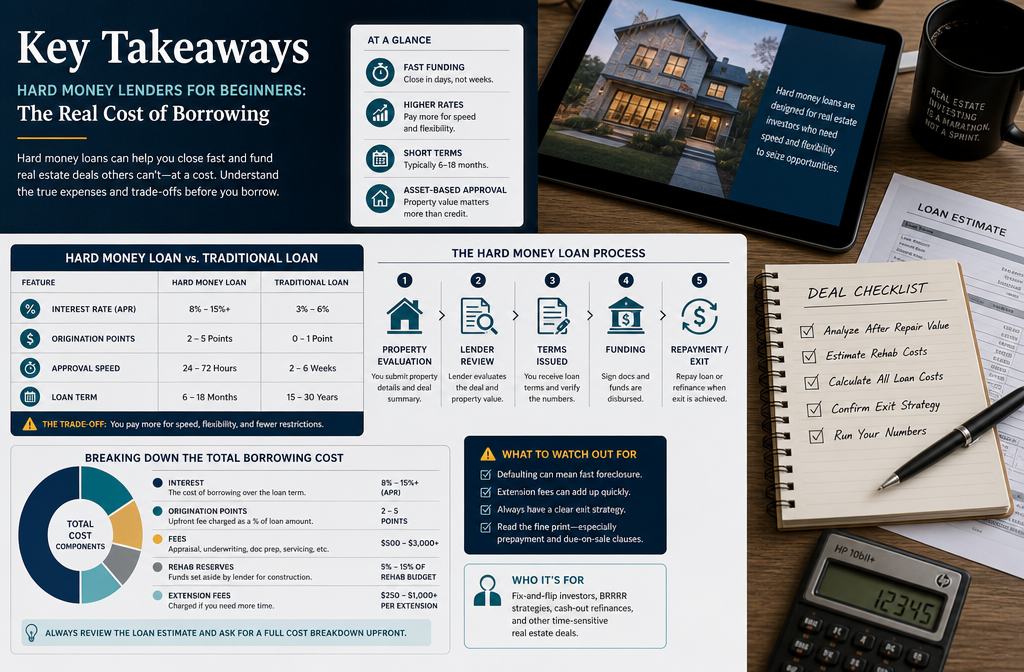

- Hard money loans are secured by the property, not your credit score — making them accessible even for borrowers with credit scores as low as 500 to 600

- Interest rates typically range from 10% to 15% in 2026, compared to 6% to 7% for conventional mortgages

- Origination fees (called "points") usually run 2 to 4% of the loan amount — that's $6,000 to $12,000 on a $300,000 loan before you even start

- Loan terms are short — typically 6 to 24 months — so you need a clear exit strategy before you borrow

- Hard money loans are best for fix-and-flip projects, bridge financing, and time-sensitive acquisitions — not long-term buy-and-hold investing

- Top lenders for beginners include Kiavi, LendingOne, New Silver, and RCN Capital

- If you can't repay, the lender can foreclose — and they will, because the deal economics still work in their favor

- Alternatives like DSCR loans, HELOCs, and real estate crowdfunding may be cheaper depending on your situation

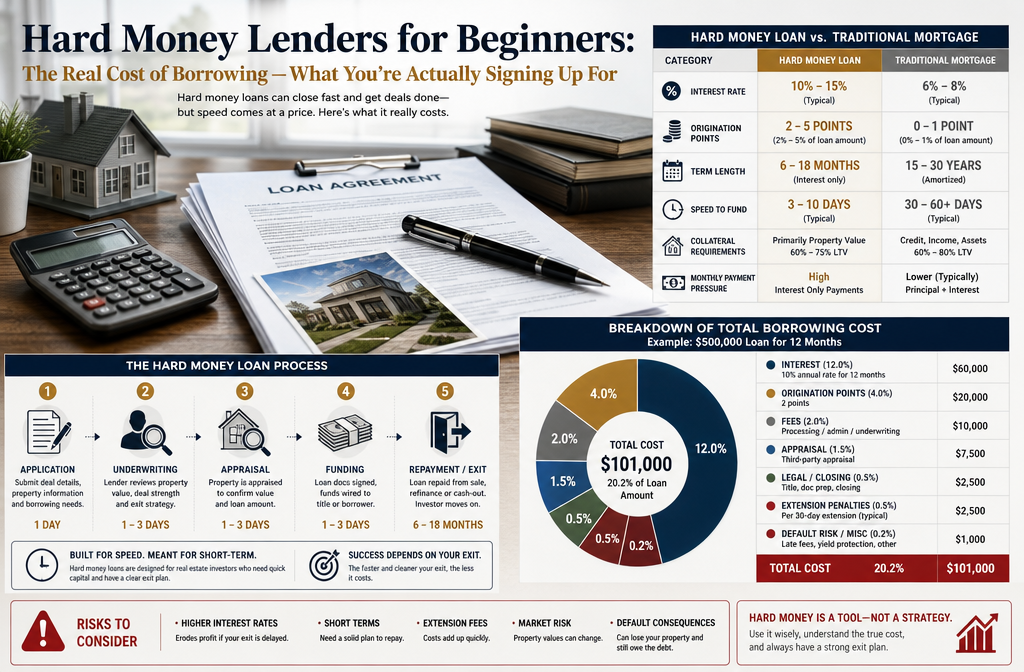

Hard Money Lenders for Beginners: The Real Cost of Borrowing — What You're Actually Signing Up For

Hard money lenders for beginners is one of those topics the industry has been gate keeping for years. Most educational content either oversimplifies it ("just get a hard money loan and flip houses!") or buries the real numbers in fine print. This guide breaks down exactly what borrowing from a hard money lender costs — not just the headline rate, but everything.

Here's the honest picture: hard money loans are expensive by design. They exist to solve a specific problem — fast capital for real estate deals that don't fit traditional lending boxes. When a bank says no (or says "maybe, in 45 days"), a hard money lender says yes in 48 hours. That speed and flexibility has a price, and beginners who don't understand that price often see their profit margins evaporate on their first deal.

The total cost of a hard money loan includes:

- Interest rate: 10% to 15% annually (sometimes higher for riskier deals)

- Origination points: 2 to 4 points (each point = 1% of the loan amount)

- Closing costs: $1,500 to $3,000+ in lender fees, title, and escrow

- Appraisal or BPO fees: $300 to $700 typically

- Extension fees: 0.5% to 1.5% per month if you need more time

- Prepayment penalties: Some lenders charge these if you pay off early (usually 3 to 6 months of interest minimum)

On a $250,000 hard money loan held for 9 months at 12% interest with 3 points upfront, you're looking at roughly $22,500 in interest plus $7,500 in origination fees — a total financing cost of $30,000 before any other deal expenses. That's not a reason to avoid hard money loans. It's a reason to run your numbers before you commit.

What Exactly Is a Hard Money Loan and How Is It Different From a Bank Loan?

A hard money loan is a short-term loan from a private lender or investor group, secured by real property. The lender's primary concern is the value of the collateral — the property — not your income, employment history, or debt-to-income ratio.

The key differences from a bank loan:

| Feature | Hard Money Loan | Traditional Bank Loan |

|---|---|---|

| Approval basis | Property value (LTV) | Borrower creditworthiness |

| Approval timeline | 5 to 10 business days | 30 to 60 days |

| Loan term | 6 to 24 months | 15 to 30 years |

| Interest rate (2026) | 10% to 15% | 6% to 7.5% |

| Credit score required | 500 to 650+ (varies) | 620 to 740+ |

| Points/origination | 2 to 4 points | 0 to 1 point |

| Best use case | Fix-and-flip, bridge, distressed | Primary residence, rental hold |

Banks underwrite the borrower. Hard money lenders underwrite the deal. That's the fundamental difference — and it's why a self-employed investor with irregular income but a strong property can get funded by a hard money lender when a bank turns them away.

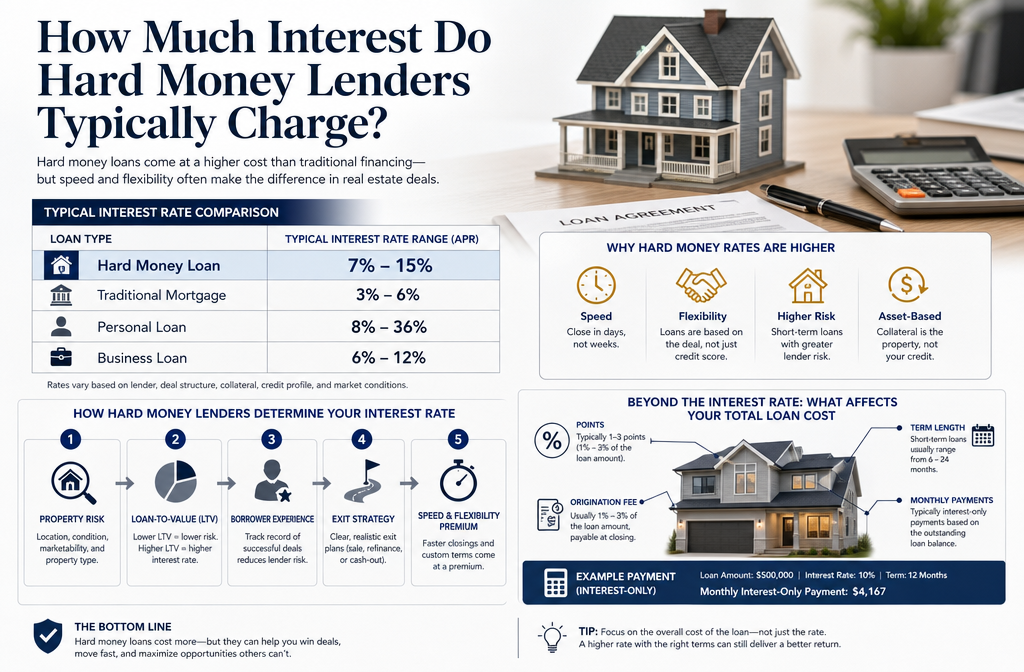

How Much Interest Do Hard Money Lenders Typically Charge?

Hard money interest rates in 2026 generally fall between 10% and 15% annually, with most experienced investors landing in the 11% to 13% range depending on the lender, the deal, and the borrower's track record.

A few factors that push your rate higher:

- First-time borrower with no track record

- Lower credit score (below 600)

- Higher loan-to-value ratio (above 70% to 75%)

- Distressed or rural property

- Shorter loan term with higher risk profile

A few factors that can bring your rate down:

- Repeat borrower relationship with the lender

- Strong credit (680+)

- Low LTV (60% or below)

- Established fix-and-flip track record with documented exits

So based reality check: Hard money rates are not designed to compete with conventional mortgages. They're priced for short-term use. If you're holding a hard money loan for 18 months, you're paying a premium for that flexibility — and that's fine if your deal math supports it.

What Credit Score Do I Need to Qualify for a Hard Money Loan?

Most hard money lenders will work with credit scores starting around 550 to 600, and some advertise hard money loans with no credit check or as low as 500. The property is the primary collateral, so your credit score matters less than it does for conventional financing.

That said, credit score still affects your terms:

- 500 to 580: You may qualify, but expect higher rates, lower LTV limits (60% or less), and more scrutiny on the deal

- 580 to 650: Standard hard money territory — most lenders will work with you at competitive rates

- 650+: You'll get the best rates and terms, and some lenders may treat you like a preferred borrower

Hard money lenders bad credit situations are genuinely workable — but "workable" doesn't mean "cheap." The worse your credit, the more the lender compensates through rate and lower leverage. If you're a 500 credit score hard money lender scenario, expect to bring more cash to the table and pay a higher rate.

For context on other loan types that are more credit-sensitive, check out our breakdown of FHA loans vs. conventional loans to understand where hard money fits in the financing spectrum.

What Are the Total Fees I Can Expect When Getting a Hard Money Loan?

The total fees on a hard money loan go well beyond the interest rate — and this is where beginners get caught off guard. Here's a realistic fee breakdown for a $300,000 hard money loan:

Sample Fee Breakdown — $300,000 Loan

| Fee Type | Estimated Cost |

|---|---|

| Origination points (3%) | $9,000 |

| Lender processing fee | $1,000 to $1,500 |

| Appraisal / BPO | $400 to $700 |

| Title insurance | $1,000 to $2,000 |

| Escrow / closing fees | $500 to $1,500 |

| Draw inspection fees (if rehab) | $150 to $300 per draw |

| Extension fee (if needed) | 0.5% to 1.5% per month |

| Estimated upfront total | $12,000 to $16,000+ |

Hard money loan requirements vary by lender, but most will also want:

- A clear exit strategy (sale or refinance)

- Property appraisal or comparable market analysis

- Proof of funds for down payment (typically 20% to 30% of purchase price)

- Basic entity documentation if borrowing through an LLC

The impeccable investors who thrive with hard money loans are the ones who model every one of these costs into their deal analysis before they ever call a lender.

How Fast Can I Get Approved and Funded With a Hard Money Lender?

Speed is the primary reason investors use hard money — and it's real. Most hard money lenders can approve a loan in 24 to 72 hours and fund within 5 to 10 business days. Some can close in as few as 3 to 5 days for repeat borrowers with clean deals.

Compare that to conventional bank loans, which routinely take 30 to 60 days to close. In competitive markets — especially the fix and flip market in 2026 — that speed difference is often the margin between winning a deal and losing it to a cash buyer.

What speeds up approval:

- Clean title on the property

- Clear exit strategy documented upfront

- Pre-existing relationship with the lender

- Simple deal structure (purchase only, not complex rehab)

What slows it down:

- Title issues or liens on the property

- First-time borrower with no track record

- Complex renovation scope requiring detailed draw schedules

- Missing documentation (entity docs, insurance, etc.)

Are Hard Money Loans Good for Real Estate Investors or Just for People With Bad Credit?

Hard money loans are primarily a tool for real estate investors — not a fallback for people who got rejected by a bank. This is one of the most common misconceptions beginners carry into their first deal.

The typical hard money borrower in 2026 isn't someone who couldn't qualify for a mortgage. They're an investor who needs to close in 7 days on a distressed property, or a developer who needs bridge financing while a long-term loan is being arranged, or an experienced flipper who runs multiple projects simultaneously and needs capital that moves at the speed of their business.

Hard money loans are a strong fit if you:

- Are buying a distressed property that doesn't qualify for conventional financing

- Need to close faster than any bank can move

- Are self-employed with income that's hard to document for traditional underwriting

- Are executing a fix-and-flip with a clear exit within 6 to 18 months

- Need a hard money bridge loan while transitioning from one property to another

Hard money loans are a poor fit if you:

- Plan to hold the property long-term (buy-and-hold rental)

- Don't have a clear exit strategy

- Are counting on appreciation alone to make the deal work

- Can't afford the carrying costs if the project runs over schedule

For long-term rental holds, a DSCR loan is almost always the better call. The hard money vs DSCR loan comparison comes down to timeline: hard money for short-term execution, DSCR for long-term cash flow.

Can I Use a Hard Money Loan for a Fix-and-Flip Project?

Yes — fix-and-flip is the most common use case for hard money loans, and it's where these products genuinely shine. Hard money fix and flip loans are structured specifically for this strategy, often covering both the purchase price and a portion of the renovation costs.

Here's how a typical fix-and-flip hard money loan works:

- Lender evaluates the ARV (After Repair Value) — the estimated value of the property after renovations

- Loan is sized based on ARV — typically 65% to 75% of ARV

- Rehab funds are held in reserve and released in draws as work is completed

- Borrower completes renovations, lists the property, and sells

- Loan is repaid at closing from sale proceeds

The best fix and flip lenders in 2026 include names like Kiavi, LendingOne, New Silver, and RCN Capital — all of which specialize in investor lending and have streamlined processes for repeat borrowers.

Flipping houses with hard money works best when:

- Your ARV estimate is conservative and verified

- Your renovation budget has a 10% to 15% contingency buffer

- Your timeline accounts for market conditions (days on market in your area)

- Your total cost basis (purchase + rehab + financing) leaves at least 20% profit margin

For a deeper look at which markets are producing the best returns right now, our guide to the best real estate markets for flipping houses in 2026 breaks it down by data.

What Kind of Property Can Be Used as Collateral for a Hard Money Loan?

Most hard money lenders will accept residential and commercial investment properties as collateral. The property just needs to have verifiable value that supports the loan amount.

Commonly accepted property types:

- Single-family homes (most common)

- 2 to 4 unit multifamily properties

- Small apartment buildings (5+ units — fewer lenders, higher scrutiny)

- Commercial properties (retail, office, mixed-use)

- Land (fewer lenders, lower LTV — usually 50% or less)

- Fix-and-flip properties in any condition

Properties that are harder to finance with hard money:

- Rural properties with limited comparable sales

- Highly specialized commercial properties (churches, gas stations)

- Properties with significant title issues or environmental concerns

- Mobile homes and manufactured housing (some lenders, not all)

The lender's main question is always: "If the borrower defaults, can we sell this property and recover our capital?" The more liquid and marketable the property, the better your terms will be.

What Happens If I Can't Repay a Hard Money Loan?

If you can't repay a hard money loan, the lender has the right to foreclose on the property — and they will exercise that right. Hard money lenders are not banks with bureaucratic foreclosure processes. They move faster, and the deal economics often favor them taking the property.

Here's what typically happens in a default scenario:

- Missed payment or maturity default — lender sends a notice of default

- Grace period — usually 10 to 30 days depending on the loan documents

- Extension negotiation — some lenders will offer a short extension (with fees) if the deal is viable

- Foreclosure proceedings — if no resolution, the lender initiates foreclosure under state law

- Property auction or REO — lender recovers capital through sale

Because hard money lenders typically lend at 65% to 75% of value, they have a built-in equity cushion. Even in a down market, they can often recover their principal. That's why they can afford to move fast — their downside is protected.

The smart move if you're struggling:

- Communicate early — lenders prefer a workout to a foreclosure

- Explore a hard money refinance into a longer-term product if the property has equity

- Consider selling the property before the loan matures if the deal isn't working

Which Hard Money Lenders Are Best for First-Time Real Estate Investors?

Four lenders consistently stand out for beginners in 2026: Kiavi, LendingOne, New Silver, and RCN Capital. Each has different strengths depending on your deal type and experience level.

Kiavi (formerly LendingHome) is one of the largest hard money lenders in the country, with a tech-forward platform that makes the application process straightforward. They specialize in fix-and-flip and rental bridge loans, and their online portal gives borrowers real-time visibility into their loan status. Good for: first-timers who want a structured, transparent process.

LendingOne focuses on residential investment properties and offers both fix-and-flip and rental loans. They're known for competitive rates and a dedicated account manager model — which matters when you're new and have questions. Good for: beginners who want a human point of contact.

New Silver uses AI mortgage underwriting to accelerate approvals — some borrowers report term sheets within minutes. They're particularly active in the fix-and-flip space and publish their rates and terms transparently online. Good for: tech-savvy investors who want speed and transparency.

RCN Capital is a national lender with a strong broker network, offering hard money fix and flip loans, bridge loans, and long-term rental financing. They work with both direct borrowers and through mortgage brokers, giving beginners flexibility in how they access the product. Good for: investors who prefer working through a broker relationship.

For a broader look at financing options as you build your portfolio, our real estate financing guide covers the full spectrum from conventional to creative.

What Mistakes Do Beginners Usually Make With Hard Money Loans?

The most common beginner mistakes with hard money loans are predictable — and almost all of them come down to underestimating costs or overestimating speed.

Mistake #1: Underestimating the total cost of capital

Beginners focus on the interest rate and forget about points, fees, draw costs, and extensions. Model every line item before you commit.

Mistake #2: Overestimating the ARV

If your after-repair value estimate is off by 10%, your entire profit margin can disappear. Get a professional appraisal or at minimum three solid comparable sales.

Mistake #3: No exit strategy

A hard money loan without a clear exit is a financial emergency waiting to happen. Know before you borrow whether you're selling or refinancing — and have a backup plan.

Mistake #4: Underestimating renovation timelines

Contractors run late. Materials get delayed. Permits take longer than expected. Build buffer into your timeline, because extension fees are expensive.

Mistake #5: Borrowing the maximum available

Just because a lender will give you 75% of ARV doesn't mean you should take it. Lower leverage = lower risk and often better terms.

Mistake #6: Not comparing lenders

Hard money rates vary significantly between lenders. Getting three quotes before committing is basic due diligence — and it's extraordinary how many beginners skip this step.

Let it cook before you see results is real advice here. Your first hard money deal should be conservative — smaller loan, lower LTV, clear exit — so you can learn the process without a catastrophic downside.

Are There Any Alternatives to Hard Money Loans for Real Estate Investing?

Yes — and depending on your situation, one of these alternatives might be a better fit than hard money.

DSCR Loans: Debt Service Coverage Ratio loans qualify based on the property's rental income, not your personal income. They're better for buy-and-hold investors and carry rates closer to conventional mortgages. See our guide to DSCR loan requirements for a full breakdown.

HELOCs on Investment Property: If you already own property with equity, a HELOC on an investment property can provide flexible, lower-cost capital for your next deal. Rates are typically lower than hard money, though qualification is stricter.

Real Estate Crowdfunding: Platforms that pool investor capital for specific deals. Lower minimums, no personal liability, but you're a passive investor — not the operator. Check out our comparison of 7 real estate crowdfunding platforms to see which fits your goals.

Private Money Lenders: Individual investors (often found through networking) who lend their own capital. Terms are negotiable and can be more flexible than institutional hard money, but finding them requires relationship-building.

Seller Financing: The seller acts as the lender. No bank, no hard money lender — just you and the seller agreeing on terms. Works best with motivated sellers and properties that are free and clear.

Bridge Loans from Banks: Some banks and credit unions offer bridge loans with better rates than hard money, though the approval process is slower and qualification is stricter.

How Do Hard Money Loan Terms Compare to Traditional Mortgage Rates?

The rate gap between hard money and conventional mortgages is significant and intentional. In 2026, conventional mortgage rates are hovering around 6% to 7.5% for investment properties, while hard money rates run 10% to 15%. That's a 4 to 8 percentage point spread.

But comparing the two products purely on rate misses the point. They serve different purposes:

- Conventional mortgages are built for long-term holds, require full underwriting, and take 30 to 60 days to close

- Hard money loans are built for short-term execution, underwrite the deal not the borrower, and close in days

The real comparison should be: "What is the cost of missing this deal because I waited for conventional financing?" In a competitive market, the answer is often "more than the rate difference."

For investors tracking where the broader market is heading, our analysis of 2026 real estate trends and how 6% rates are reshaping strategies gives useful context on the current rate environment.

FAQ: Hard Money Lenders for Beginners

Q: What is the minimum credit score for a hard money loan?

Most hard money lenders will work with scores as low as 500 to 550. The property value matters more than your credit, but lower scores typically mean higher rates and lower leverage.

Q: Can I get a hard money loan with no credit check?

Some lenders advertise hard money loans no credit check, but most still pull a soft credit inquiry. "No credit check" usually means credit isn't the primary qualifier — not that they ignore it entirely.

Q: How much down payment do I need for a hard money loan?

Typically 20% to 35% of the purchase price. Hard money lenders generally lend up to 65% to 75% of the property's value (or ARV for fix-and-flip deals), so you need to cover the gap.

Q: What is a hard money bridge loan?

A hard money bridge loan is short-term financing used to "bridge" the gap between two transactions — for example, buying a new property before selling your current one, or holding a property while arranging long-term financing.

Q: Can I do a hard money refinance?

Yes. A hard money refinance replaces an existing loan (hard money or otherwise) with a new hard money loan, often to access equity or extend the timeline. It's common when a project runs long and the original loan is maturing.

Q: How does AI mortgage underwriting affect hard money approvals?

Lenders like New Silver use AI mortgage underwriting to analyze deals faster and more consistently. This means faster term sheets — sometimes within minutes — and more data-driven (less relationship-dependent) approvals. It's a fresh development that's making hard money more accessible to first-timers.

Q: Is the investor share of homes in 2026 affecting hard money availability?

The investor share of homes in 2026 remains a topic of policy debate, but hard money lending activity has stayed strong, particularly in the fix-and-flip and value-add segments where institutional investors are less active.

Q: What's the difference between hard money and private money?

Hard money lenders are typically organized companies with set underwriting criteria. Private money lenders are individuals lending their own capital, often with more flexible terms negotiated deal-by-deal.

Q: How many points is normal for a hard money loan?

Two to four points is standard. One point equals 1% of the loan amount. On a $200,000 loan, two points = $4,000 upfront.

Q: Can I use a hard money loan to buy a rental property?

You can, but it's not ideal for long-term holds because of the high carrying cost. The typical strategy is to use hard money to acquire and stabilize the property, then refinance into a DSCR loan or conventional mortgage for the long-term hold.

Q: What happens to my hard money loan if the market drops?

If the property value drops significantly, you may find yourself in a position where you owe more than the property is worth. This is why conservative LTV ratios and realistic ARV estimates matter — they give you a buffer if the market moves against you.

Q: Are hard money loans regulated?

Hard money lenders are regulated at the state level, and rules vary significantly by state. Some states require lenders to be licensed; others have fewer requirements. Always verify your lender's licensing status before borrowing.

Conclusion: What Beginners Should Do Before Their First Hard Money Deal

Hard money lenders for beginners doesn't have to be an intimidating topic — but it does require respect for the numbers. The product is extraordinary in the right context: fast, flexible, and genuinely accessible to investors who don't fit the conventional lending mold. The cost is real, and it compounds quickly if your deal runs long.

Before you borrow, do these five things:

- Model every cost — interest, points, fees, extensions — into your deal analysis. If the deal doesn't work with all costs included, it doesn't work.

- Know your exit — sale or refinance, and have a backup plan for each.

- Compare at least three lenders — Kiavi, LendingOne, New Silver, and RCN Capital are solid starting points, but rates and terms vary.

- Be conservative on ARV — use the lower end of comparable sales, not the highest.

- Build timeline buffer — add 20% to 30% to your renovation timeline estimate and make sure your loan term covers it.

Hard money is a tool. Impeccable investors use it strategically — not as a last resort, and not without understanding what they're signing. Get the numbers right, pick the right lender for your deal type, and let it cook before you see results.

For more on building your investment strategy from the ground up, our beginner's blueprint for real estate investing and our guide to the best loans for flipping houses are the logical next reads.

{kind=link}