Last updated: May 24, 2026

Quick Answer: Getting pre-approved for an investment property requires a credit score of at least 620 (ideally 700+), a down payment of 15–25%, documented income or rental cash flow, and a debt-to-income ratio below 45%. The process typically takes 3–10 business days with a conventional lender, or as fast as 24–48 hours with a DSCR loan lender. Knowing exactly what lenders want before you apply is what separates investors who close deals from those who keep losing them to cash buyers.

Key Takeaways

- Minimum credit score for most investment property loans is 620, but 700+ gets you significantly better rates.

- Down payments range from 15% (single-unit) to 25% (multi-unit) for conventional loans — no FHA or VA options on pure investment properties.

- DSCR loans let investors qualify based on rental income alone — no personal income verification required, making them ideal for self-employed borrowers and LLC investors.

- Conventional lenders cap financing at 10 financed properties; portfolio lenders and DSCR lenders go beyond that.

- Debt-to-income ratio must generally stay below 43–45% — rental income from the subject property can sometimes offset this.

- Pre-approval letters typically expire in 60–90 days; if you don’t find a property in time, you’ll need to refresh.

- Investment property mortgage rates in 2026 run 0.5–0.75% higher than primary residence rates — the 6% mortgage rate new norm in 2026 means investors are commonly seeing 6.75–7.5% on 30-year fixed loans.

- Investors using an LLC for property ownership face extra steps but can still get pre-approved through commercial or DSCR lenders.

- Rental income from existing properties can count toward your qualifying income — with the right documentation.

How to Get Pre-Approved for an Investment Property: Step by Step

Getting pre-approved for an investment property is not the same as getting pre-approved for a home you plan to live in. Lenders treat these loans differently — higher rates, stricter requirements, and a much closer look at your financial picture. Here’s the full process, broken down so you can walk into any lender conversation ready.

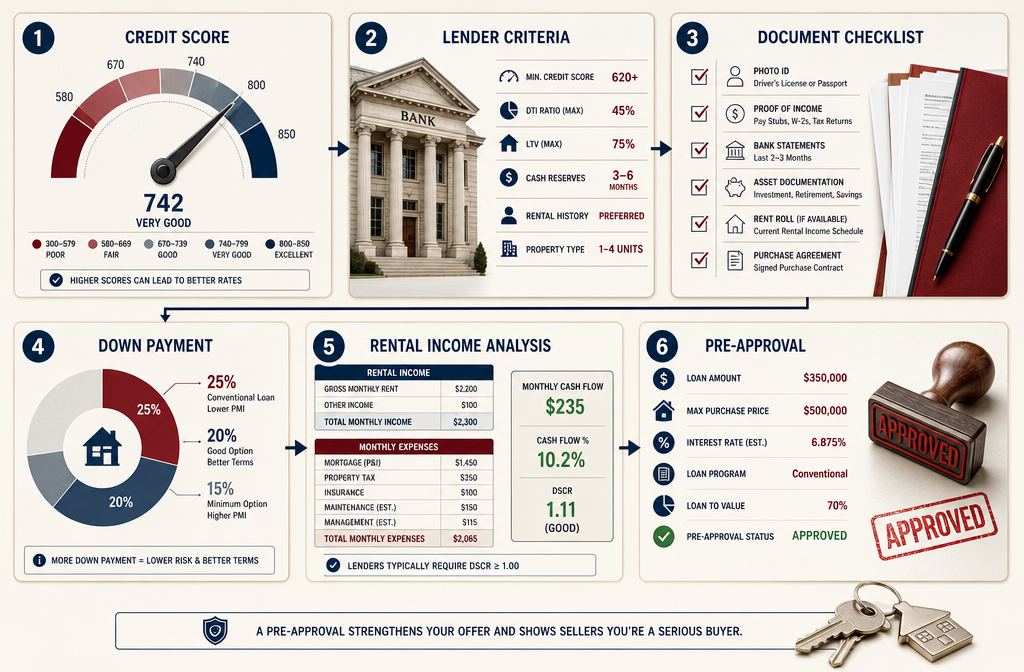

Step 1: Know Your Credit Score Before the Lender Does

Pull your credit report before you apply. Most conventional lenders want a minimum score of 620, but anything below 700 is going to cost you in rate. If your score is sitting at 680, it’s worth spending 30–60 days paying down revolving balances before you apply — that move alone can push you into a better rate tier.

Step 2: Calculate Your Down Payment

Investment properties require real money down. Plan for 15% minimum on a single-unit rental and 25% on a 2–4 unit property. There are no FHA or VA loans available for pure investment properties, so whatever you bring to the table needs to be sourced and documented.

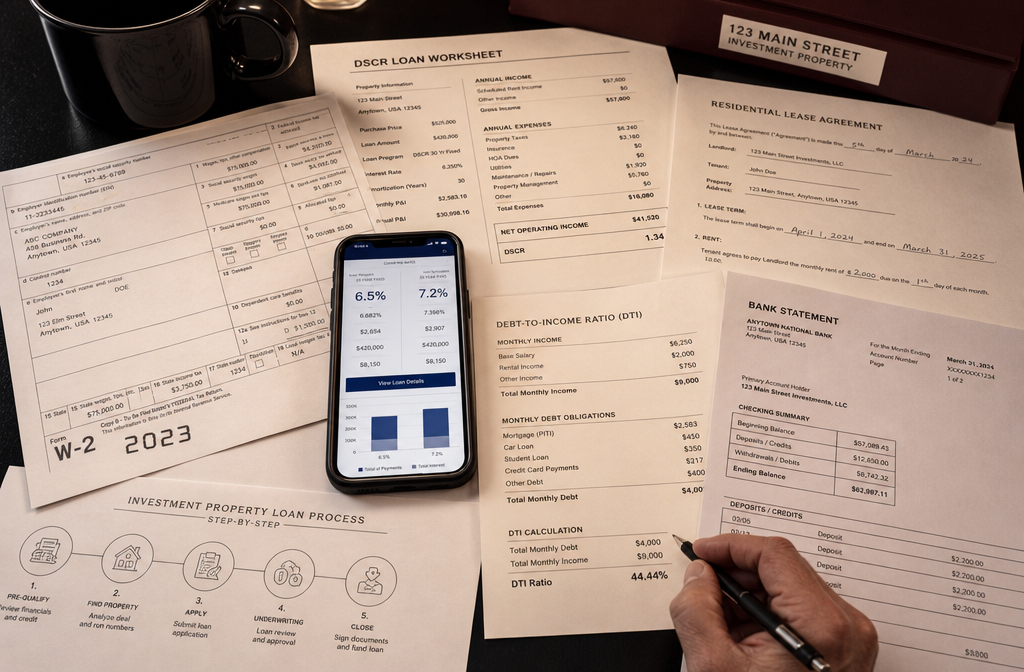

Step 3: Gather Your Financial Documents

Lenders will want two years of tax returns, two months of bank statements, proof of existing rental income (if applicable), and a current mortgage statement for any properties you already own. Self-employed borrowers often need additional documentation — more on that below.

Step 4: Choose the Right Loan Type

Conventional loans, DSCR loans, and portfolio loans each have different pre-approval paths. If you have strong W-2 income, conventional is usually the cleanest route. If your income is complex or you’re buying under an LLC, a DSCR loan pre-approval process is often faster and more flexible.

Step 5: Submit Your Pre-Approval Application

Once you’ve picked your lender and loan type, submit your application with all required documents. A good lender will give you a pre-approval letter within 3–10 business days. DSCR lenders can often turn this around in 24–48 hours.

Step 6: Review the Pre-Approval Letter

Read the letter carefully. It should specify the loan amount, loan type, rate range, and any conditions. Conditions are common — things like “subject to property appraisal” or “pending verification of rental income.” These are normal, not red flags.

What Credit Score Do You Need for an Investment Property Loan?

Most lenders require a minimum credit score of 620 for investment property loans, but the real sweet spot is 700 or higher. A score below 680 will trigger higher rates and may require a larger down payment to compensate for perceived risk.

Here’s how credit score tiers typically affect your investment property financing:

| Credit Score Range | Likely Outcome |

|---|---|

| 760+ | Best available rates, easiest approval |

| 720–759 | Strong approval, competitive rates |

| 680–719 | Approved, but rate is noticeably higher |

| 640–679 | Possible approval with larger down payment |

| Below 620 | Most conventional lenders will decline |

Common mistake: Many investors apply with a score in the low 600s thinking they’ll “figure it out later.” That approach usually results in a denial or a rate so high the deal doesn’t pencil. Let it cook — spend a few months cleaning up your credit before you apply, and the numbers will work in your favor.

How Much Down Payment Is Required for an Investment Property?

The minimum down payment for an investment property is 15% for a single-unit rental and 25% for a 2–4 unit property under conventional loan guidelines. There is no low-down-payment program available for pure investment properties the way there is for primary residences.

Down payment breakdown by property type:

- Single-family rental (1 unit): 15% minimum, 20–25% preferred

- Small multifamily (2–4 units): 25% minimum

- 5+ unit commercial: 20–35% depending on the lender and property type

- DSCR loans: Typically 20–25% down regardless of unit count

The investment property down payment requirement is one of the biggest barriers for new investors — and it’s intentional. Lenders know that when an investor has real skin in the game, they’re less likely to walk away if the market dips.

Pro tip: If you already own a primary residence with equity, a HELOC can be a smart way to fund part of your down payment. Check out our breakdown of how smart investors use a HELOC on investment property to scale their portfolios.

What Documents Do Lenders Want for Investment Property Pre-Approval?

Lenders want proof that you can handle the loan — and for investment properties, that bar is higher than for a primary residence. Here’s the standard document list:

For W-2 employees:

- Last 2 years of federal tax returns (personal)

- Last 2 years of W-2s

- 2 most recent pay stubs

- 2–3 months of bank statements (all accounts)

- Current mortgage statements for all owned properties

- Existing lease agreements (if you have rental income)

For self-employed borrowers:

- Last 2 years of personal AND business tax returns

- Year-to-date profit and loss statement

- Business bank statements (2–3 months)

- CPA letter confirming business ownership and income stability

For DSCR loans (no personal income verification):

- Signed lease agreement or market rent appraisal

- Property operating history (if it’s an existing rental)

- 2–3 months of bank statements (asset verification)

- Entity documents if purchasing under an LLC

Edge case: If you’re self-employed and your tax returns show significant write-offs (which reduce your taxable income), a conventional loan may be difficult to qualify for even if you’re genuinely cash-flowing well. This is exactly the scenario where a DSCR loan pre-approval becomes the smarter play.

What’s the Difference Between Residential and Investment Property Mortgage Rates?

Investment property mortgage rates are consistently higher than primary residence rates — typically by 0.5 to 0.75 percentage points for conventional loans, and sometimes more for DSCR or portfolio products.

With the 6% mortgage rate new norm in 2026 for primary residences, investors are generally looking at current investment property mortgage rates in the 6.75–7.5% range on a 30-year fixed conventional loan. DSCR loans often run slightly higher, in the 7.0–8.5% range depending on the lender, LTV, and property type.

Why the rate gap exists:

- Investment properties have higher default rates than owner-occupied homes

- Lenders price in the risk that an investor will prioritize their primary home if finances get tight

- Fannie Mae and Freddie Mac impose loan-level price adjustments (LLPAs) on investment properties

Choose conventional if: You have strong W-2 income, a credit score above 700, and you want the lowest possible rate.

Choose DSCR if: Your income is self-employed, variable, or held in a business entity — and the property’s rental income can cover the debt service.

For a deeper look at how DSCR lending stacks up, our guide to the best DSCR loan lenders for investment properties in 2026 breaks down the top options by rate, requirements, and borrower type.

Can You Get Pre-Approved Using Rental Income From Other Properties?

Yes — existing rental income from other properties can count toward your qualifying income, but only if it’s properly documented. Lenders typically want to see a signed lease agreement and at least two years of rental income history reported on your tax returns (Schedule E).

How lenders count rental income:

- Most conventional lenders use 75% of gross rental income to account for vacancies and expenses

- That 75% figure is then added to your other qualifying income

- If a property is newly rented with no tax history, the lender may use a market rent appraisal (Form 1007) instead

Important nuance: If you have rental properties that are still mortgaged, those mortgage payments count against your DTI. The net effect of rental income on your pre-approval depends on whether the income offset exceeds the debt obligation.

This is also why learning how to analyze a rental property before you buy matters — not just for your own underwriting, but for showing lenders a property that cash-flows on paper.

DSCR vs. Conventional Pre-Approval: Which Path Is Right for You?

DSCR (Debt Service Coverage Ratio) loans and conventional loans are the two most common pre-approval paths for investment properties in 2026 — and they serve very different borrower profiles.

DSCR loans qualify you based on the property’s income, not your personal income. The lender calculates the DSCR by dividing the property’s gross monthly rent by the total monthly debt service (principal, interest, taxes, insurance, and HOA if applicable). A DSCR of 1.0 means the property breaks even; most lenders want 1.1–1.25 or higher.

Conventional loans qualify you based on your personal income, credit, and DTI ratio. They typically offer lower rates but require full income documentation.

| Factor | Conventional Loan | DSCR Loan |

|---|---|---|

| Income verification | Full (W-2, tax returns) | None (property cash flow only) |

| Min. credit score | 620 (700+ preferred) | 620–660 |

| Down payment | 15–25% | 20–25% |

| Rate (2026 estimate) | 6.75–7.25% | 7.0–8.5% |

| LLC eligible | No (personal only) | Yes |

| Self-employed friendly | Difficult | Highly compatible |

| Max properties | 10 (Fannie/Freddie) | No cap (lender-dependent) |

So based: If you’re a self-employed investor or you’re buying under an LLC, DSCR is the move. If you have clean W-2 income and fewer than 10 financed properties, conventional will usually save you money on rate.

For investors exploring LLC loans for investment properties, DSCR is often the only realistic path since most conventional lenders won’t lend to an LLC directly.

What Debt-to-Income Ratio Do Banks Look For in Investment Loans?

Most lenders cap the debt-to-income ratio (DTI) for investment property loans at 43–45%. Some portfolio lenders will stretch to 50% for strong borrowers, but that’s not the norm.

How DTI is calculated:

DTI = Total monthly debt payments ÷ Gross monthly income

Your total monthly debt includes all existing mortgage payments, car loans, student loans, credit card minimums, and the proposed new investment property payment.

Ways to improve your DTI before applying:

- Pay down high-balance revolving accounts

- Pay off or eliminate installment loans close to payoff

- Document all rental income properly on your tax returns

- Use a DSCR loan (which bypasses personal DTI entirely)

Edge case: If your DTI is borderline at 44%, adding a co-borrower with strong income can push you over the approval threshold. This is a legitimate and common strategy — just make sure the co-borrower understands their liability.

Are Hard Money Loans Better Than Traditional Bank Financing for Investment Properties?

Hard money loans are faster and more flexible than traditional bank financing, but they come at a significant cost. They’re not better or worse — they serve a completely different purpose.

Hard money loans are designed for:

- Fix-and-flip projects where speed matters

- Properties that don’t qualify for conventional financing (distressed, non-warrantable)

- Bridge situations where you need to close fast and refinance later

Hard money loan characteristics:

- Rates: Typically 10–14% in 2026

- Terms: 6–24 months (short-term only)

- LTV: 65–75% of after-repair value (ARV)

- Approval speed: 3–7 days, sometimes faster

- Income verification: Minimal to none

Traditional bank financing is better for:

- Long-term buy-and-hold rentals

- Investors who want the lowest possible rate

- Properties in good condition that appraise cleanly

The bottom line: if you’re buying a turnkey rental and planning to hold it for years, get pre-approved through a conventional or DSCR lender. If you’re flipping a distressed property and need to close in two weeks, hard money makes sense — but have your exit strategy ready before you sign.

How Many Investment Properties Can You Finance at Once?

Conventional loans backed by Fannie Mae and Freddie Mac cap financing at 10 financed properties per borrower. That includes your primary residence. So in practice, most investors can hold up to 9 investment properties under conventional financing before hitting the wall.

What happens after 10 properties:

- You’ll need to work with portfolio lenders who hold loans in-house

- DSCR lenders generally have no hard cap on the number of financed properties

- Commercial loans (5+ unit properties) operate under completely different guidelines

Impeccable planning tip: If you’re approaching that 10-property ceiling, start building relationships with portfolio lenders and DSCR lenders now — before you need them. Waiting until you’re at the limit creates unnecessary pressure and timeline risk.

For investors thinking about scaling into multifamily, our guide on multi-family real estate investments from first duplex to full portfolio covers the financing progression in detail.

How Do You Calculate Potential Rental Income for Pre-Approval?

Lenders calculate qualifying rental income using either a signed lease agreement or a market rent appraisal (Form 1007 or 1025 for multifamily). They then apply a 75% vacancy factor to that gross rent figure.

Example calculation:

- Market rent: $2,400/month

- 75% of gross rent: $1,800/month (this is what counts toward qualifying income)

- Monthly PITI payment: $1,600

- Net contribution to DTI: The $1,800 offsets the $1,600 payment, creating a small positive effect on DTI

For DSCR loans, the calculation is different:

- Annual gross rent: $28,800

- Annual debt service (PITI): $22,400

- DSCR: $28,800 ÷ $22,400 = 1.29 (above the typical 1.25 threshold — this deal gets approved)

Knowing how to run these numbers before you apply is what separates investors who get pre-approved quickly from those who waste time chasing deals that won’t qualify. Our rental property analysis resources can help you build this skill fast.

For vacation rental investors, the income calculation gets more complex — check out our guide on what numbers to run before buying a vacation rental investment before you apply for pre-approval on a short-term rental.

Common Mistakes Investors Make When Trying to Get Pre-Approved

These mistakes are not gatekeeping secrets — they’re just things most lenders won’t explain until it’s too late.

1. Applying with too many recent credit inquiries

Every hard pull on your credit drops your score slightly. If you’ve been rate shopping with five lenders in the past 30 days, your score may have taken a hit. Mortgage inquiries within a 14–45 day window are typically grouped as one inquiry by scoring models, but outside that window, each one counts separately.

2. Moving money around right before applying

Large, unexplained deposits in your bank account are a red flag. Lenders will ask you to source every deposit over a certain threshold. If you moved money from savings to checking to “look more liquid,” that creates a paper trail that slows down your approval.

3. Underreporting rental income on tax returns

This is a double-edged sword. Investors who write off everything legally end up with low taxable income — which hurts them when they try to qualify for a conventional loan. If you plan to scale your portfolio, talk to a CPA about balancing tax efficiency with qualifying income before your next tax filing.

4. Applying for the wrong loan type

Self-employed investors applying for conventional loans often get denied — not because they can’t afford the property, but because their tax returns don’t show enough qualifying income. A DSCR loan would have approved the same borrower in 48 hours.

5. Not having reserves documented

Most lenders require 6 months of PITI reserves for each investment property you own. If you have three rentals and are buying a fourth, you may need reserves documented for all four properties. This catches investors off guard constantly.

6. Skipping pre-approval and going straight to offers

Fresh mistake that costs time and deals. Sellers and listing agents in 2026 take pre-approval letters seriously. Showing up to a competitive listing without one is like showing up to a job interview without a resume.

How Long Does Investment Property Pre-Approval Usually Take?

Most conventional lenders issue a pre-approval letter within 3–10 business days after receiving a complete application and all required documents. DSCR lenders often move faster — 24–48 hours in many cases — because they’re not verifying personal income.

Factors that slow down the process:

- Incomplete document submission (missing tax returns, bank statements)

- Complex income situations (multiple businesses, multiple rental properties)

- Low credit score requiring manual underwriting

- Title or ownership issues on existing properties

Pre-approval letter validity: Most letters are valid for 60–90 days. If your pre-approval expires before you find a property, you’ll need to refresh it — which typically means updated bank statements and a new credit pull. In a slow market, this can happen more than once.

Pro move: Ask your lender upfront how long the letter is valid and what the refresh process looks like. Some lenders make renewal simple; others restart the full process. That detail matters when you’re in a competitive market.

What Type of Investors Should Consider Getting Pre-Approved Right Now in 2026?

Getting pre-approved for investment property in 2026 makes the most sense for investors who are actively deal-hunting, have their financial house in order, and want to move fast when the right property appears.

You should get pre-approved now if:

- You’re actively searching for a rental property and making offers

- You have a credit score above 680 and a documented down payment ready

- You want to lock in current investment property mortgage rates before any potential rate movement

- You’re a self-employed investor who wants to use a DSCR loan and needs to know your exact buying power

You should wait if:

- Your credit score is below 650 (spend 3–6 months improving it first)

- You don’t have your down payment fully sourced and documented

- You’re still deciding on your investment strategy (single-family vs. multifamily vs. short-term rental)

If you’re still exploring which investment type fits your goals, our complete guide to the 4 types of real estate investments is a solid starting point before you commit to a pre-approval path.

What Happens If Your Pre-Approval Expires Before You Find a Property?

If your investment property pre-approval expires before you find a deal, you simply need to renew it. This is common and not a problem — as long as your financial situation hasn’t changed significantly.

The renewal process typically involves:

- Updated bank statements (most recent 2–3 months)

- A new credit pull (this is a hard inquiry, so be aware)

- Updated pay stubs or rental income documentation if applicable

- Confirmation that no new debts have been added

What can cause a problem at renewal:

- A new car loan or credit card opened since the original pre-approval

- A drop in credit score from missed payments or new inquiries

- A job change or income reduction

- Depleted reserves (if you spent down savings)

Extraordinary tip: If you’re in a slow market and expect the search to take 90+ days, ask your lender about a 120-day pre-approval or a portfolio lender who issues longer validity windows. Some lenders will also do a “soft refresh” at 60 days to extend the letter without a full new application.

FAQ: Investment Property Pre-Approval

Q: Can I get pre-approved for an investment property with no income?

A: Yes — through a DSCR loan. DSCR loans qualify you based on the property’s rental income, not your personal income. This makes them the go-to option for investors who are self-employed, retired, or whose tax returns show low taxable income. You’ll still need a down payment (typically 20–25%) and a credit score of at least 620.

Q: Can an LLC get pre-approved for an investment property?

A: Yes, but not through conventional Fannie/Freddie loan programs. Investment property loans for LLCs are typically done through DSCR lenders, commercial lenders, or portfolio lenders. The LLC must often have been established for at least a few months, and the lender may still require a personal guarantee from the principal.

Q: What is a DSCR loan and how does DSCR loan pre-approval work?

A: A DSCR (Debt Service Coverage Ratio) loan qualifies the borrower based on the rental property’s income rather than personal income. Pre-approval involves submitting a lease agreement or market rent appraisal, bank statements for asset verification, and basic entity documents if buying under an LLC. Approval can happen in 24–48 hours.

Q: How does the AI mortgage approval process work in 2026?

A: Many lenders now use AI-powered underwriting tools to analyze bank statements, tax returns, and credit data faster than traditional manual review. The AI mortgage approval process can flag issues instantly, speed up document verification, and reduce the time from application to pre-approval letter. Borrowers still interact with a human loan officer, but the backend analysis is increasingly automated.

Q: How much do I need in reserves for an investment property loan?

A: Most conventional lenders require 6 months of PITI (principal, interest, taxes, insurance) reserves for each investment property you own, including the one you’re buying. DSCR lenders may require 3–6 months depending on their guidelines.

Q: Can I use a gift for the down payment on an investment property?

A: Generally, no. Most conventional and DSCR lenders require that the down payment on an investment property come from your own funds — not a gift. This is different from primary residence loans, where gift funds are often allowed. Some portfolio lenders may make exceptions, but it’s not standard.

Q: Does rental income from a short-term rental (Airbnb) count for pre-approval?

A: It can, but it’s more complex than long-term rental income. Lenders typically want 12–24 months of Airbnb income history documented on your tax returns. Some DSCR lenders will use a short-term rental income appraisal, but not all. This is a case where choosing the right lender matters as much as the numbers.

Q: What’s the minimum down payment for an investment property in 2026?

A: The minimum down payment for a single-family investment property is 15% under conventional loan guidelines. For a 2–4 unit property, it’s 25%. DSCR loans typically require 20–25% regardless of unit count. There are no 3.5% or 5% down options for pure investment properties.

Q: How do I get pre-approved for investment property with no income on paper?

A: Use a DSCR loan. These loans ignore your personal income entirely and focus on whether the property’s rent covers the debt service. You’ll need solid credit (620+), a 20–25% down payment, and a property with a DSCR of at least 1.0–1.25.

Q: Does getting pre-approved hurt my credit score?

A: Yes, a pre-approval involves a hard credit inquiry, which can lower your score by a few points temporarily. If you’re shopping multiple lenders, try to do all applications within a 14–45 day window — credit scoring models typically count multiple mortgage inquiries in that period as a single inquiry.

Conclusion: Your Pre-Approval Is the Starting Gun, Not the Finish Line

Getting pre-approved for an investment property is the single most important step you can take before making an offer. It tells sellers you’re serious, tells you exactly what you can afford, and tells your lender that you’ve done the work. The investors who move fast in this market are the ones who already have their pre-approval in hand.

Your action plan:

- Pull your credit report today and address anything below 700

- Calculate your down payment and confirm it’s fully sourced and documented

- Gather your last 2 years of tax returns, 2 months of bank statements, and existing lease agreements

- Decide between conventional and DSCR based on your income profile

- Apply with a lender who specializes in investment property financing — not just any bank

- Get your pre-approval letter and start making offers with confidence

The market in 2026 rewards prepared investors. With current investment property mortgage rates sitting in the 6.75–7.5% range, deals still pencil when you buy right. The extraordinary investors aren’t waiting for rates to drop — they’re getting pre-approved, running the numbers, and letting it cook until the right property shows up.

For more on building your investment strategy from the ground up, check out our beginner’s blueprint for how to invest in real estate — and if you’re ready to go deeper on financing options, our investment property financing hub has everything you need.

{kind=link}