Last updated: May 24, 2026

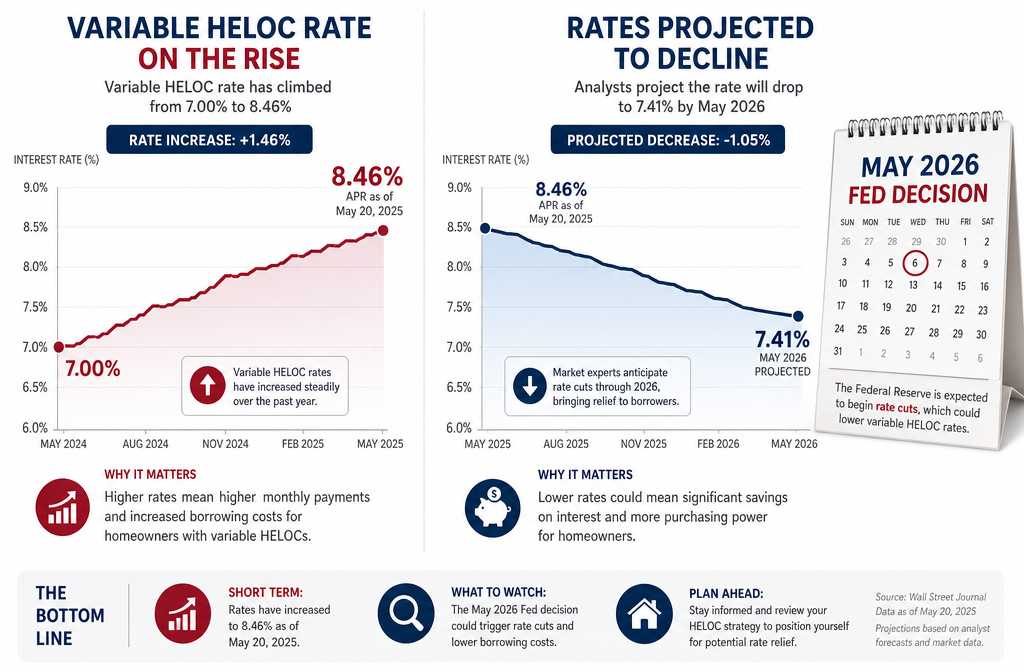

Quick Answer: A HELOC refinance can save you real money — but only under the right conditions. If your current rate is above today’s average (HELOC rates have dropped from a peak of 8.46% in 2025 to around 7.41% in 2026), your credit score has improved, or your draw period is ending, refinancing makes sense. If your home value has dropped, your closing costs outweigh your savings, or you’re close to paying off the balance, it’s probably not worth it.

Key Takeaways 🏠

- HELOC rates have fallen from 8.46% in 2025 to approximately 7.41% in 2026, creating a real window to save on interest

- The May 2026 Fed rate decision kept rates steady, but most analysts expect at least one cut before year-end — which would push HELOC rates lower

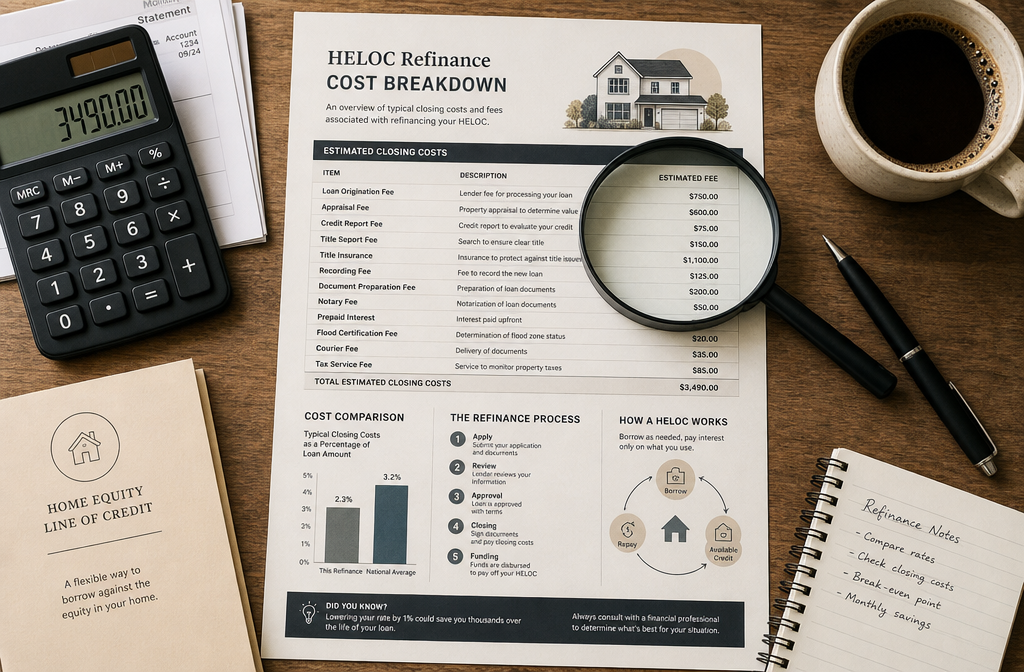

- Closing costs on a HELOC refinance typically run 2%–5% of the credit line amount, so the math has to work in your favor

- You can refinance a HELOC into a new HELOC, a home equity loan (HELoan), or roll it into a cash-out mortgage refinance

- A credit score of 680+ is generally the floor for HELOC refinance approval; 720+ gets you the best rates

- If your home value has dropped and you’re sitting at 85%+ combined loan-to-value (CLTV), most lenders will decline the refi

- The IRS allows mortgage interest deductions on HELOCs only when funds are used to buy, build, or substantially improve the home

- Investors using a HELOC on a rental property should read our guide on how smart investors use a HELOC on investment property before refinancing

What Exactly Is a HELOC Refinance and How Does It Work?

A HELOC refinance means replacing your existing home equity line of credit with a new loan — either a new HELOC, a fixed-rate home equity loan, or a cash-out mortgage refinance. The goal is usually to get a lower rate, better terms, or convert a variable rate to something more predictable.

Here’s how the process works:

- You apply with a lender (your current one or a new one) to replace your existing HELOC

- The lender orders an appraisal to confirm your home’s current value and available equity

- Underwriting reviews your credit score, income, debt-to-income ratio, and combined loan-to-value (CLTV)

- You close on the new loan, which pays off the old HELOC balance

- Your new terms begin — new rate, new draw or repayment period, new monthly payment

A standard HELOC has two phases: a draw period (usually 10 years) where you borrow as needed, and a repayment period (usually 10–20 years) where you pay back what you borrowed. Refinancing can reset that clock, extend your draw period, or lock in a fixed rate before the repayment phase hits.

HELOC refinance options include:

- Equity line refinance — new HELOC with better terms

- HELOC vs HELoan refinance — converting to a fixed home equity loan for payment stability

- Cash-out mortgage refi — rolling the HELOC balance into your primary mortgage

HELOC Refinance: When It Saves You Money and When It Doesn’t — The Full Breakdown

This is the core question, and the answer depends on four variables: your current rate vs. today’s rates, your remaining balance, your closing costs, and how long you plan to stay in the home.

When a HELOC refinance saves you money:

| Scenario | Why It Works |

|---|---|

| Your current HELOC rate is above 7.41% | You can capture the 2026 rate drop from the 2025 peak of 8.46% |

| Your credit score improved significantly | Better score = better rate = real savings |

| You’re entering the repayment period | Refinancing before the draw period ends can reset terms and lower payments |

| You want rate certainty | Converting to a fixed HELoan protects you from future Fed hikes |

| You have a large balance ($50K+) | The savings justify the closing costs |

When it doesn’t save you money:

| Scenario | Why It Hurts |

|---|---|

| Your balance is under $20K | Closing costs eat the savings |

| Your home value dropped | You may not have enough equity to qualify |

| You’re almost done repaying | Resetting the term costs more in interest long-term |

| Your credit score dropped | You’ll get a worse rate, not a better one |

| You plan to sell soon | You won’t recoup closing costs before you move |

The break-even rule is simple: divide your total closing costs by your monthly savings. If that number is more months than you plan to stay in the home, the refi heloc doesn’t pay off.

How Much Can You Save by Refinancing Your HELOC?

The savings depend on your balance, the rate difference, and your loan term. Here’s a concrete example using current HELOC refinance rates 2026:

Example: $75,000 HELOC balance

- Old rate: 8.46% (2025 peak) → Monthly interest: ~$529

- New rate: 7.41% (2026 average) → Monthly interest: ~$463

- Monthly savings: ~$66

- Annual savings: ~$792

If closing costs run $2,000–$3,750 (2%–5% of the $75K line), your break-even point is roughly 30–57 months. That’s a solid deal if you’re staying put for 3–5+ years.

Now bump that balance to $150,000:

- Monthly savings jump to ~$131

- Annual savings: ~$1,575

- Break-even on $3,000–$7,500 in closing costs: 23–57 months

The bigger your balance, the faster refinancing pays for itself. This is why real estate investors with large equity lines tend to benefit most from a refi heloc when rates fall.

💡 Pro tip: Before running numbers, check where current HELOC rates stand. As of May 2026, the average HELOC rate sits around 7.41% — down meaningfully from the 8.46% peak in 2025. That spread is real money if your balance is significant.

What Are the Closing Costs and Fees for a HELOC Refinance?

Closing costs on a HELOC refinance typically run 2%–5% of the credit line amount, though some lenders offer no-closing-cost options (usually by rolling fees into the rate).

Common HELOC closing costs refinance breakdown:

- Application fee: $75–$500

- Appraisal fee: $300–$600 (required in most cases)

- Title search and insurance: $200–$900

- Attorney/closing fee: $200–$500 (varies by state)

- Annual fee: $50–$100/year on some HELOCs

- Early termination fee: $300–$500 if you close the old HELOC within 2–3 years of opening it

Some lenders — especially credit unions — offer HELOCs with minimal closing costs, sometimes as low as $500 flat. The trade-off is usually a slightly higher rate or a requirement to keep the line open for a minimum period.

No-closing-cost HELOC refi: If a lender advertises zero closing costs, read the fine print. Either the fees are baked into the rate (you pay over time instead of upfront) or there’s an early closure penalty if you pay it off within 24–36 months.

For investors comparing loan structures, our breakdown of mortgage broker vs. direct lender options covers how to shop for the best deal on equity-based financing.

When Is a HELOC Refinance a Bad Idea?

A HELOC refinance is a bad idea when the costs outweigh the savings, your financial position has weakened, or the timing is off. These aren’t edge cases — they’re common traps that catch homeowners off guard.

Skip the refi if any of these apply:

1. Your balance is too low

Refinancing a $15,000–$20,000 balance rarely makes financial sense. The closing costs alone can wipe out 12–24 months of interest savings.

2. You’re almost through the repayment period

If you’ve got 2–3 years left on repayment, refinancing resets the clock. You could end up paying more total interest even at a lower rate because you’re stretching the term.

3. Your credit score dropped

A lower score since you opened the original HELOC means you won’t qualify for better terms. You might actually get a higher rate — the opposite of what you want.

4. You’re planning to sell the home

Closing costs on a refi heloc need time to recover. If you’re selling within 18–24 months, you’ll likely lose money on the transaction.

5. You’re using it to fund lifestyle expenses

Refinancing to pull more cash out for non-home-related spending is a pattern that erodes equity over time. It’s a financial move that looks smart on paper but costs you long-term.

6. HELOC rates are rising

If the Fed signals rate hikes ahead, locking into a new variable-rate HELOC could backfire. In that environment, converting to a fixed HELoan is smarter than a straight equity line refinance.

Am I Eligible for a HELOC Refinance With My Current Credit Score?

Most lenders require a minimum credit score of 680 to qualify for a HELOC refinance. The best HELOC refinance rates 2026 go to borrowers with scores of 720 or higher.

Credit score tiers and what to expect:

| Credit Score | Eligibility | Rate Impact |

|---|---|---|

| 760+ | Strong approval odds | Best available rates |

| 720–759 | Good approval odds | Competitive rates |

| 680–719 | Approval possible | Rates 0.5%–1% higher |

| 640–679 | Difficult, limited lenders | Rates 1.5%–2%+ higher |

| Below 640 | Most lenders will decline | May need to wait and rebuild |

Beyond credit score, lenders also look at:

- Combined loan-to-value (CLTV): Most lenders cap at 80%–85% CLTV. If your primary mortgage plus the HELOC exceeds that threshold, you won’t qualify.

- Debt-to-income ratio (DTI): Most lenders want DTI below 43%, though some go to 50% for strong borrowers.

- Income verification: Self-employed borrowers may need 2 years of tax returns. W-2 earners typically need recent pay stubs and employment verification.

For a deeper look at how credit scores affect your real estate financing options, check out our credit score guide for real estate transactions.

Can You Refinance a HELOC If Your Home Value Has Dropped?

Yes, but it’s significantly harder — and in many cases, you won’t qualify. If your home value has dropped since you opened the HELOC, your available equity may no longer meet lender requirements.

Here’s why this matters: lenders calculate your CLTV by adding your primary mortgage balance plus your HELOC limit, then dividing by the home’s current appraised value. If that number exceeds 80%–85%, most lenders will decline the application.

Example:

- Home value in 2023: $400,000

- Home value in 2026: $350,000 (dropped $50K)

- Primary mortgage balance: $240,000

- HELOC balance: $50,000

- CLTV: ($240K + $50K) / $350K = 82.9%

At 82.9% CLTV, some lenders will still work with you — but your options narrow fast. If the home dropped further to $320,000, that CLTV hits 90.6%, and most conventional lenders walk away.

What to do if your home value has dropped:

- Wait for the market to recover before refinancing (let it cook before you see results)

- Pay down the primary mortgage to improve your CLTV

- Look at credit unions, which sometimes allow higher CLTV ratios than banks

- Consider whether a personal loan or other unsecured financing makes more sense for smaller balances

Our 2026 real estate market trends guide covers how home values are shifting across U.S. markets right now — worth checking before you order an appraisal.

What Are the Tax Implications of a HELOC Refinance?

The tax treatment of a HELOC refinance depends entirely on how the funds were — and will be — used. This is an area where the IRS draws a clear line, and crossing it costs you the deduction.

The IRS rule (post-2017 Tax Cuts and Jobs Act):

Mortgage interest on a HELOC is only deductible if the funds were used to buy, build, or substantially improve the home that secures the loan. Using HELOC funds for debt consolidation, vacations, or business expenses does not qualify for the deduction.

What this means for a refinance:

If you’re refinancing a HELOC that was originally used for a qualifying home improvement, the interest on the new loan generally remains deductible — up to the $750,000 combined mortgage debt limit for married filers ($375,000 for single filers).

Key tax considerations:

- Keep records of how HELOC funds were originally used — this documentation matters at tax time

- If you’re rolling a HELOC into a cash-out mortgage refinance, the deductibility rules for the combined loan still apply

- Rental property investors: HELOC interest on an investment property is typically deductible as a business expense, not a personal mortgage interest deduction — a different (and often more favorable) treatment

- Always consult a CPA or tax advisor before refinancing if the deduction matters to your tax strategy

This is one of those areas where gatekeeping the right information makes a real difference. Most people don’t know the distinction between personal and investment property HELOC tax treatment — and it’s extraordinary how much that difference can affect your annual tax bill.

Is a HELOC Refinance Better Than a Cash-Out Mortgage Refinance?

It depends on your situation, but here’s the straight answer: a HELOC refinance is usually better when you want to preserve your existing mortgage rate. A cash-out mortgage refinance makes more sense when HELOC rates are significantly higher than first-mortgage rates.

HELOC Refinance vs. Cash-Out Mortgage Refinance:

| Factor | HELOC Refinance | Cash-Out Mortgage Refi |

|---|---|---|

| Keeps existing mortgage rate | ✅ Yes | ❌ No — replaces it |

| Rate type | Variable (or fixed HELoan) | Fixed |

| Closing costs | Lower (2%–5% of equity line) | Higher (2%–6% of full loan) |

| Flexibility | Draw as needed | Lump sum upfront |

| Best for | Preserving a low first mortgage | Consolidating all debt at one rate |

| Tax deductibility | Same rules apply | Same rules apply |

The 2026 context: Many homeowners locked in mortgage rates of 3%–4% in 2020–2022. Doing a cash-out refinance today means trading that rate for a 6%+ first mortgage. For those borrowers, a HELOC refinance is almost always the better move — you keep the impeccable low rate on your primary mortgage and only refinance the equity line.

For investors comparing financing structures, our guide on HELOC lenders for investment property breaks down the top lenders offering the most competitive HELOC refinance rates 2026.

What Mistakes Do People Make When Refinancing a HELOC?

The most common mistake is refinancing without calculating the break-even point. People see a lower rate and assume they’re saving money — without accounting for closing costs, term extension, or the impact on their total interest paid.

Top HELOC refinance mistakes to avoid:

1. Ignoring the total cost of the new term

A lower rate on a longer term can cost you more in total interest. Always compare total interest paid, not just monthly payment.

2. Not shopping multiple lenders

Your current lender isn’t automatically the best option. Credit unions, community banks, and online lenders often offer more competitive HELOC refinance options than big national banks.

3. Forgetting early termination fees

If you opened your current HELOC recently, closing it to refinance may trigger a penalty of $300–$500 or more. Factor that into your cost calculation.

4. Refinancing into another variable rate without a plan

If rates are expected to rise (watch the Fed rate decision May 2026 signals), refinancing from one variable HELOC to another just delays the problem. Consider a fixed HELoan instead.

5. Using the refi to pull more cash without a clear purpose

Increasing your credit line during a refinance feels like a fresh start, but it’s a trap if you don’t have a specific, productive use for the funds. Real estate investors who scale with equity know the difference between strategic leverage and lifestyle debt.

6. Not checking the appraisal before applying

If your home value has shifted, find out before you pay an application fee. Some lenders offer a preliminary value estimate before you commit to a full application.

How Long Does a Typical HELOC Refinance Take?

A HELOC refinance typically takes 2–6 weeks from application to closing. The timeline varies based on the lender, appraisal scheduling, and how quickly you can provide documentation.

Typical HELOC refinance timeline:

| Stage | Timeframe |

|---|---|

| Application and document submission | Days 1–5 |

| Appraisal ordered and completed | Days 5–15 |

| Underwriting review | Days 10–20 |

| Conditional approval and final docs | Days 18–25 |

| Closing | Days 25–42 |

What slows it down:

- Appraisal scheduling delays (common in busy spring/summer markets)

- Missing income documentation (especially for self-employed borrowers)

- Title issues on the property

- Lender backlogs during high-volume periods

What speeds it up:

- Having all documents ready before you apply (tax returns, pay stubs, mortgage statement, homeowners insurance)

- Choosing a lender who does in-house underwriting

- Applying during slower lending seasons (late fall, winter)

What Happens If You Can’t Make Payments After Refinancing Your HELOC?

Missing payments on a HELOC — refinanced or not — is serious because the loan is secured by your home. If you default, the lender can foreclose.

The payment risk reality:

A HELOC refinance doesn’t eliminate financial risk — it restructures it. If you refinanced to lower your monthly payment and then encounter a job loss, medical expense, or income drop, you’re still on the hook for a secured debt.

What happens if you miss payments:

- 30 days late: Late fee assessed, credit score drops

- 60–90 days late: Lender may freeze the credit line, credit damage accelerates

- 90–120 days late: Account may be referred to collections or foreclosure proceedings begin

- Foreclosure: Lender can force the sale of your home to recover the balance

Options if you’re struggling after a refi:

- Contact your lender immediately — many offer hardship programs or temporary payment deferrals

- Request a loan modification to extend the term and lower payments

- Explore refinancing again into a longer-term fixed loan if equity allows

- Consult a HUD-approved housing counselor (free service) before missing payments

For homeowners weighing whether to stay, sell, or leverage equity, our 2026 decision guide for homeowners sitting on big equity lays out the options clearly.

How Do HELOC Rates Compare to Personal Loan Rates in 2026?

HELOC rates are generally lower than personal loan rates because HELOCs are secured by your home. As of 2026, average HELOC rates sit around 7.41%, while personal loan rates for qualified borrowers typically range from 10%–20%+ depending on credit.

Rate comparison (2026 estimates):

| Loan Type | Typical Rate Range | Secured? |

|---|---|---|

| HELOC (variable) | 7.0%–9.5% | Yes (home) |

| Home Equity Loan (fixed) | 7.5%–9.0% | Yes (home) |

| Personal loan (good credit) | 10%–15% | No |

| Personal loan (fair credit) | 15%–25%+ | No |

| Credit card | 20%–29%+ | No |

The trade-off is obvious: HELOCs are cheaper, but they put your home at risk. Personal loans are more expensive, but defaulting won’t cost you your house. For large amounts ($30,000+), the rate savings on a HELOC are substantial. For smaller amounts where the closing costs eat the savings, a personal loan or 0% intro APR credit card might actually be the smarter short-term play.

FAQ: HELOC Refinance Questions Answered

Q: Can you refinance a HELOC with a different lender?

Yes. You can refinance a HELOC with any lender that offers home equity products. Shopping multiple lenders is smart — your current lender has no obligation to give you the best rate.

Q: What is the current average HELOC rate in 2026?

As of May 2026, the average HELOC rate is approximately 7.41%, down from the 2025 peak of 8.46%. Rates vary by lender, credit score, and CLTV.

Q: Can I refinance a HELOC into a fixed-rate loan?

Yes. You can convert a variable-rate HELOC into a fixed-rate home equity loan (HELoan). This gives you payment certainty and protects you if rates rise. The trade-off is losing the flexible draw feature.

Q: Does refinancing a HELOC hurt your credit score?

It can cause a temporary dip. The lender will pull a hard inquiry, and opening a new account lowers your average account age. Most borrowers see a 5–15 point temporary drop that recovers within 6–12 months.

Q: How much equity do I need to refinance a HELOC?

Most lenders require at least 15%–20% equity after accounting for both your primary mortgage and the HELOC. That means your CLTV must stay at or below 80%–85%.

Q: Is a HELOC refinance the same as refinancing and home equity loans together?

Not exactly. Refinancing and home equity loans are separate products. A HELOC refinance replaces your equity line. A cash-out mortgage refinance replaces your primary mortgage and may absorb the HELOC balance. A HELoan is a fixed alternative to a HELOC.

Q: What is the best time to refinance a HELOC in 2026?

The best time to refinance a HELOC in 2026 is when your current rate is meaningfully above today’s market rate, your credit score is strong, and you have sufficient equity. With HELOC rates falling from 8.46% in 2025 to 7.41% in 2026, many borrowers are in a solid window right now.

Q: Can self-employed borrowers refinance a HELOC?

Yes, but documentation requirements are stricter. Most lenders want 2 years of tax returns, a year-to-date profit and loss statement, and sometimes 12–24 months of bank statements. Income averaging is common.

Q: What happens to my HELOC draw period when I refinance?

A new HELOC resets the draw period — typically back to 10 years. If you refinance into a HELoan, there’s no draw period; you receive a lump sum and begin repayment immediately.

Q: Are there no-closing-cost HELOC refinance options?

Some lenders offer no-closing-cost HELOCs, but fees are typically embedded in a slightly higher rate or recaptured through an early termination penalty if you close the line within 2–3 years.

Conclusion: Make the HELOC Refinance Work For You — Not Against You

A HELOC refinance is one of the most powerful tools in a homeowner’s or investor’s financial toolkit — but only when the numbers actually work. With HELOC rates falling from 8.46% in 2025 to around 7.41% in 2026, and the Fed holding steady while signaling potential cuts ahead, the current environment is genuinely favorable for borrowers who have strong equity and good credit.

The move is fresh if your balance is large, your rate is above market, and you’re staying in the home long enough to clear the break-even on closing costs. It’s so based to lock in a fixed HELoan if you’re worried about rate volatility. And it’s absolutely worth letting it cook before you see results — the savings compound over time, not overnight.

Actionable next steps:

- Pull your current HELOC statement — confirm your rate, balance, and remaining draw/repayment period

- Check your home’s current value — use a free AVM tool or request a broker opinion before paying for an appraisal

- Review your credit score — if it’s below 720, spend 3–6 months improving it before applying

- Calculate your break-even — divide estimated closing costs by monthly savings to see if the timeline makes sense

- Shop at least 3 lenders — your bank, a credit union, and an online lender

- Talk to a tax advisor — especially if the deductibility of interest matters to your filing

For investors ready to scale with equity, our guide on how smart investors use a HELOC on investment property is the next read. And if you’re comparing mortgage structures for your overall financing strategy, our mortgage options hub covers the full landscape.

The equity in your home is working capital. A HELOC refinance done right puts more of it in your pocket — not your lender’s.

Have questions about HELOC refinancing or real estate financing strategies? Reach out at news@realestaterankiq.com or explore more at realestaterankiq.com.

{kind=link}