Last updated: May 24, 2026

Quick Answer: Most lenders require you to wait at least 6 to 12 months after purchasing a home before approving a HELOC. Some lenders — particularly portfolio and credit union lenders — will move as fast as 30 to 90 days if you have strong equity, a solid credit score, and a clean financial profile. The exact timeline depends on your lender’s seasoning requirements, how much equity you have, and whether the property is a primary residence or an investment property.

Key Takeaways

- Standard waiting period: 6 to 12 months is the most common seasoning window lenders require before approving a HELOC after a home purchase.

- Minimum equity threshold: Most lenders want you to retain at least 15–20% equity after the HELOC draw, meaning your combined loan-to-value (CLTV) ratio should stay at or below 80–85%.

- Credit score floor: A score of 620 is the bare minimum at most lenders; 680+ gets you better rates, and 720+ puts you in the best tier.

- Your down payment matters: A larger down payment at purchase means more equity on day one — which can accelerate your HELOC eligibility.

- Investment property HELOCs take longer: Expect stricter requirements, higher rates, and longer wait times on non-owner-occupied properties.

- HELOC rates in May 2026 are averaging around 7.41% (variable), making timing and lender selection critical.

- Fast HELOC approval in 2026 is possible through credit unions, online lenders, and portfolio banks — but you still need to meet equity and income benchmarks.

- HELOC vs. cash-out refinance is a real decision to make after purchase — both have trade-offs depending on your current mortgage rate.

- Seasoning rules vary by lender — there is no universal federal mandate, so shopping around pays off.

- Common mistake: Applying too soon with insufficient equity and getting a hard credit pull that damages your score before you’re actually ready.

How Soon Can I Do a HELOC After Purchasing a Home?

The honest answer: it depends on your lender, your equity position, and your financial profile — but 6 months is the most common minimum, and 12 months is where you’ll find the widest pool of lenders willing to work with you.

Here’s what’s actually happening behind the scenes. When you buy a home, lenders want to see that you’re a stable borrower before letting you pull equity out. They call this a seasoning period — essentially a waiting room where your mortgage history gets established and your equity position becomes verifiable.

The three factors that determine your actual wait time:

- Lender type — Banks, credit unions, and online lenders all have different seasoning policies. Some portfolio lenders (those who keep loans in-house rather than selling them) can move in 30–90 days.

- Equity at purchase — If you put 30–40% down, you may qualify faster because you already have substantial equity on day one.

- Property type — Primary residences get the most flexibility. Investment properties and second homes face stricter timelines and higher hurdles.

“New homeowner HELOC timing is one of the most misunderstood parts of real estate finance. People assume they’re locked out for a year — but the real answer is ‘it depends,’ and knowing what it depends on is everything.”

If you’re a real estate investor looking to scale using equity, our HELOC on Investment Property guide breaks down exactly how smart investors use this tool to buy more real estate.

How Long Do You Have to Wait Before Getting a Home Equity Line of Credit?

The minimum waiting period for most conventional lenders is 6 months from your closing date. Some lenders require a full 12 months. A small group of portfolio lenders and credit unions will consider applications as early as 30–90 days post-purchase.

This isn’t a federal law — it’s lender policy. That distinction matters because it means the timeline is negotiable depending on who you’re borrowing from.

Waiting Period Breakdown by Lender Type

| Lender Type | Typical Waiting Period | Notes |

|---|---|---|

| Major banks (Chase, Wells Fargo, BofA) | 12 months | Strict seasoning, conventional underwriting |

| Credit unions | 3–6 months | More flexible, relationship-based lending |

| Online lenders (Figure, Spring EQ) | 6–12 months | Fast process, but seasoning still applies |

| Portfolio lenders | 30–90 days | Keep loans in-house, more discretion |

| Hard money / private lenders | Immediate (sometimes) | High rates, short terms, not ideal for HELOCs |

Decision rule: If you’re in a hurry and have strong equity, start with credit unions and portfolio lenders. If you can wait 12 months, you’ll have access to the best rates and the most competitive products.

Can I Get a HELOC Immediately After Buying a House?

Technically, yes — but practically, it’s rare and comes with significant trade-offs. A handful of portfolio lenders and private lenders will approve a HELOC shortly after closing, sometimes within 30 days. But you’ll pay for that speed in the form of higher rates, stricter equity requirements, and less favorable terms.

Most mainstream lenders simply won’t touch a HELOC application from someone who closed on their home last month. Their reasoning is sound: they want to see payment history, confirm the appraisal holds, and verify that the borrower isn’t over-leveraging immediately after purchase.

When “immediately” might work:

- You put down 40%+ at purchase and have substantial equity

- You’re working with a local credit union or community bank that knows your financial profile

- You’re a self-employed borrower with strong documented income and assets

- The property is in a high-appreciation market where equity built fast

When it won’t work:

- You used a low down payment (3–5%) program

- Your credit score is below 680

- You’re applying at a major national bank

- The property is an investment property or second home

What Are the Minimum Waiting Periods for a HELOC After Home Purchase?

The minimum seasoning requirement across most lenders ranges from 0 to 12 months, with 6 months being the most common floor for competitive products. Here’s how it breaks down by loan and lender category:

- 0–30 days: Portfolio lenders, hard money lenders, some private banks (rare, high rates)

- 3–6 months: Credit unions, some community banks, select online lenders

- 6 months: Standard minimum for most conventional HELOC products

- 12 months: Required by major national banks and some government-backed guidelines

Mortgage seasoning rules exist because lenders want to verify that the purchase appraisal was accurate and that the borrower is managing payments responsibly. Some lenders also use the seasoning period to ensure the property hasn’t been “flipped” or artificially inflated in value.

One important edge case: if you purchased a home with cash and are now seeking a HELOC, some lenders treat this as a delayed financing situation and may have separate guidelines — often requiring 6 months before they’ll use the purchase price as the basis for equity calculation.

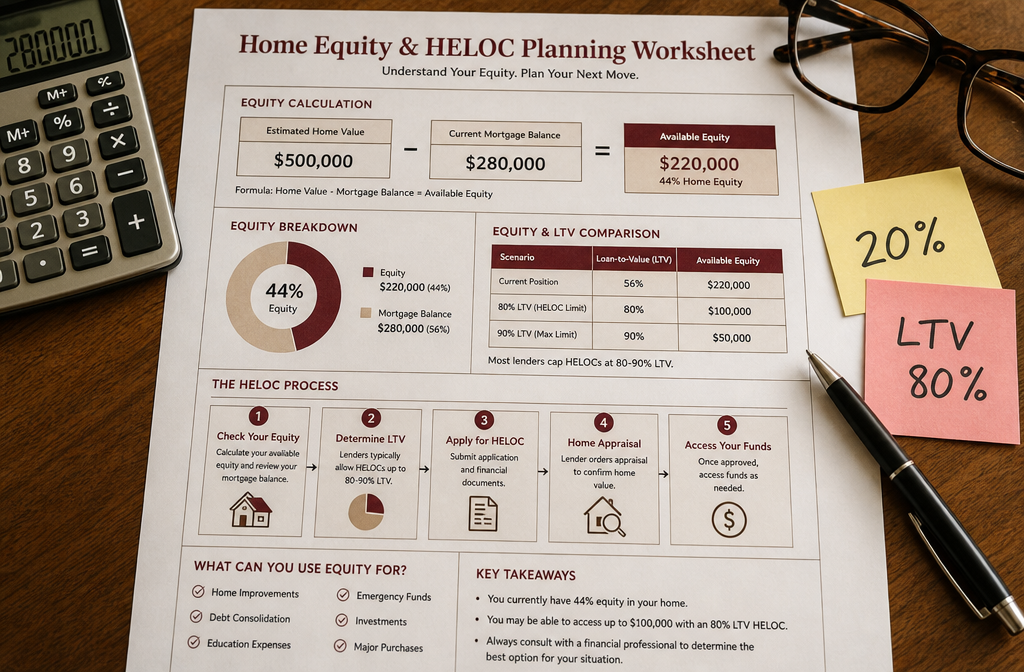

How Much Equity Do You Need to Qualify for a HELOC?

Most lenders require you to maintain at least 15–20% equity in your home after the HELOC is established. In practical terms, this means your combined loan-to-value ratio (CLTV) — your first mortgage plus the HELOC — should not exceed 80–85% of your home’s appraised value.

Quick Equity Math Example

Say you bought a home for $400,000 and put 20% down ($80,000). Your mortgage balance is $320,000. Your home is now appraised at $420,000.

- Home value: $420,000

- Mortgage balance: $320,000

- Available equity at 80% CLTV: $420,000 × 0.80 = $336,000 − $320,000 = $16,000 HELOC limit

- Available equity at 85% CLTV: $420,000 × 0.85 = $357,000 − $320,000 = $37,000 HELOC limit

That’s not a massive line of credit — which is why timing matters. Waiting for equity to build through appreciation and mortgage paydown gives you access to a much larger, more useful HELOC.

Equity buildup after purchase happens through three channels:

- Your down payment — instant equity on day one

- Mortgage paydown — slow but steady, especially in early years when payments are interest-heavy

- Appreciation — market-driven, varies by location

For investors looking at the bigger picture of equity strategy, our 2026 decision guide for homeowners sitting on big equity covers when to tap, hold, or sell.

Does My Down Payment Impact When I Can Get a HELOC?

Yes — your down payment is one of the biggest factors in how quickly you can access a HELOC after purchase. A larger down payment means more equity from day one, which directly affects your CLTV ratio and your lender’s willingness to approve a HELOC sooner.

Here’s the real-world impact:

- 3–5% down: You’re starting with almost no equity. Even after 6–12 months of payments, you may not have enough equity to qualify — especially if appreciation has been flat.

- 10% down: You’re closer, but still likely need 6–12 months of appreciation or paydown to hit the 20% equity threshold most lenders want.

- 20% down: You hit the standard equity threshold at purchase. With a 6-month seasoning period and a lender offering 85% CLTV, you may qualify for a modest HELOC relatively quickly.

- 30–40% down: You’re in the strongest position. Some lenders will approve a HELOC in as little as 30–90 days because your equity position is impeccable from the start.

The gate-keeping reality: Low down payment programs (FHA, 3% conventional) are extraordinary for getting into a home, but they effectively lock you out of HELOC access for longer. That’s not a reason to avoid them — it’s just a trade-off to plan around.

What Credit Score Do You Need for a HELOC After Buying a Home?

The minimum credit score for most HELOC products is 620, but 680 is where you start getting competitive rates, and 720+ puts you in the best pricing tier. Your credit score affects not just approval odds but also your interest rate — and with HELOC rates in May 2026 averaging around 7.41% (variable), even a 0.5% rate difference adds up fast over a $50,000 draw.

HELOC Credit Score Tiers (2026)

| Credit Score Range | Approval Likelihood | Rate Impact |

|---|---|---|

| Below 620 | Very unlikely | Most lenders won’t approve |

| 620–659 | Possible, limited options | Highest rates, strictest terms |

| 660–699 | Good, more lenders available | Above-average rates |

| 700–719 | Strong, most lenders approve | Near-average rates |

| 720–759 | Excellent, best product access | Competitive rates |

| 760+ | Top tier | Best available rates |

Other HELOC qualifications beyond credit score:

- Debt-to-income ratio (DTI): Most lenders cap at 43–50%

- Income verification: W-2 employees, self-employed borrowers, and investors all face different documentation requirements

- Employment history: 2 years of stable employment or self-employment history is standard

- Property appraisal: A fresh appraisal confirms current market value

Self-employed borrowers and high-income professionals with non-traditional income streams should check out our mortgage options guide for documentation strategies that work.

How Do Mortgage Seasoning Rules Affect HELOC Approval?

Mortgage seasoning rules are lender-imposed waiting periods that determine how long your mortgage must be “aged” before you can tap equity through a HELOC. These rules exist to protect lenders from borrowers who might over-leverage immediately after purchase, and they vary significantly by institution.

There’s no single federal rule that mandates a specific seasoning period for HELOCs (unlike cash-out refinances, where Fannie Mae and Freddie Mac guidelines apply to conventional loans). This means lenders set their own policies — and shopping around is not just smart, it’s essential.

How seasoning rules play out in practice:

- If you bought with a conventional loan, your lender’s seasoning requirement is their own policy — not Fannie/Freddie mandated for HELOCs

- If you bought with an FHA loan, the HELOC would be in second lien position, which many lenders avoid entirely — making your options narrower

- If you paid cash, some lenders use the delayed financing exception and may require 6 months before they’ll lend against the purchase price

Fast HELOC approval in 2026 is most accessible when you’ve been in the home 6+ months, have 20%+ equity, a 700+ credit score, and verifiable income. That combination opens doors at credit unions, online lenders, and community banks that can move in 2–4 weeks once the application is submitted.

Risks of Applying for a HELOC Too Soon After Home Purchase

Applying for a HELOC before you’re truly ready can hurt your finances in ways that take months to undo. The risks are real, and they’re worth understanding before you pull the trigger.

The Top Risks of Moving Too Fast

1. Hard credit inquiry damage

Every HELOC application triggers a hard pull on your credit. If you apply at multiple lenders while rate shopping and get denied repeatedly, those inquiries stack up and can drop your score 5–15 points — right when you need it strong.

2. Insufficient equity = denial or tiny credit line

If your CLTV is too high, you’ll either get denied or receive a credit line so small it’s not worth the closing costs. HELOC closing costs typically run $200–$500 in fees, plus potential appraisal costs of $300–$600.

3. Variable rate exposure at the wrong time

HELOCs are variable-rate products tied to the prime rate. With current HELOC rates around 7.41% in May 2026, taking on a large draw early — before you’ve built a financial cushion — can create payment pressure if rates rise.

4. Over-leveraging a new purchase

Stacking a HELOC on top of a fresh mortgage means you’re highly leveraged. If the market dips and your home value drops, you could end up underwater — owing more than the home is worth.

5. Lender relationship damage

A premature application that gets denied can flag you in a lender’s system. Some lenders won’t re-evaluate your application for 6–12 months after a denial.

Let it cook before you see results. Waiting 12 months — even when 6 is technically possible — often means more equity, better rates, and a smoother approval. Patience is a legitimate financial strategy.

HELOC vs. Cash-Out Refinance After Purchase: Which Makes More Sense?

For most new homeowners in 2026, a HELOC is the smarter choice over a cash-out refinance — unless your current mortgage rate is significantly higher than today’s refinance rates. Here’s the core logic:

If you bought your home in 2021–2023 at a rate of 3–4%, doing a cash-out refinance now means replacing that low rate with a new loan at today’s higher rates. That’s a painful trade. A HELOC lets you keep your existing mortgage intact and access equity through a separate line of credit.

HELOC vs. Cash-Out Refi: Quick Comparison

| Factor | HELOC | Cash-Out Refinance |

|---|---|---|

| Keeps existing mortgage rate | ✅ Yes | ❌ No — replaces it |

| Rate type | Variable (tied to prime) | Fixed |

| Access to funds | Revolving line (draw as needed) | Lump sum |

| Closing costs | Lower ($200–$500 typical) | Higher (2–5% of loan amount) |

| Best for | Ongoing projects, investing | Large one-time needs |

| Approval timeline | 2–6 weeks typically | 30–60 days |

| Seasoning requirement | 6–12 months (varies) | 6–12 months (Fannie/Freddie) |

Choose a HELOC if: You have a low existing mortgage rate, need flexible access to funds, and plan to use and repay in cycles (like funding renovations or investment property purchases).

Choose a cash-out refi if: Your current rate is already high, you want a fixed rate on the equity you’re pulling, and you need a large lump sum.

For investors specifically, our best HELOC lenders for investment property guide ranks the top picks for 2026.

Common Mistakes When Trying to Get a HELOC as a New Homeowner

New homeowners make the same HELOC mistakes repeatedly — and most of them are completely avoidable. So based on what we see in the market, here are the ones that cost people the most time and money:

Mistake #1: Applying before the seasoning period ends

Applying at month 4 when your lender requires 6 months is a wasted hard inquiry. Know your lender’s specific policy before submitting any application.

Mistake #2: Not shopping multiple lenders

HELOC requirements, rates, and seasoning rules vary dramatically. The first lender you call is rarely the best one. Get quotes from at least 3–5 lenders including a credit union, an online lender, and your current mortgage servicer.

Mistake #3: Ignoring the draw period terms

The HELOC draw period — typically 10 years — is when you can borrow and make interest-only payments. After that, you enter repayment. New homeowners sometimes focus only on getting approved and miss the fact that their payment will jump significantly when the draw period ends.

Mistake #4: Underestimating HELOC closing costs

While lower than a full refinance, HELOC closing costs still exist. Budget for appraisal fees, origination fees, title search fees, and potential annual fees. Some lenders waive closing costs but charge higher rates — read the fine print.

Mistake #5: Using HELOC funds for depreciating assets

A HELOC secured by your home should be used for things that hold or grow value — renovations, investment property down payments, debt consolidation at lower rates. Using it for vacations or cars is a real risk to your home equity.

Mistake #6: Not accounting for DTI impact

Your HELOC credit limit counts against your debt-to-income ratio even if you haven’t drawn on it. This can affect future mortgage applications if you’re planning to buy another property.

For first-time buyers navigating these decisions, our first-time home buyer tips guide covers the financial fundamentals you need before adding a HELOC to the mix.

Which Lenders Have the Fastest HELOC Approval for Recent Home Buyers?

Credit unions, online lenders like Figure and Spring EQ, and community portfolio banks consistently offer the fastest HELOC approval timelines in 2026. National banks tend to be slower and more rigid on seasoning requirements.

Fast HELOC Approval Options in 2026

Credit Unions:

- Often approve in 3–4 weeks

- More flexible on seasoning (some as low as 3 months)

- Relationship-based underwriting — your full financial picture matters, not just a score

- Membership requirement is the only catch

Online Lenders (Figure, Spring EQ, Hitch):

- Fully digital process, often 5–10 business days from application to approval

- Typically require 6 months of seasoning

- Competitive rates but read the terms carefully — some have prepayment penalties

Community and Portfolio Banks:

- Keep loans in-house, so they have more flexibility

- Can sometimes approve in 30–90 days post-purchase for strong borrowers

- Best for self-employed borrowers and investors with complex income

What to bring to any HELOC application:

- Last 2 years of tax returns (especially for self-employed)

- Recent pay stubs or proof of income

- Current mortgage statement

- Homeowner’s insurance documentation

- Property tax records

- Bank statements (last 2–3 months)

What Are Current HELOC Rates for New Homeowners? (May 2026)

HELOC rates in May 2026 are averaging approximately 7.41% (variable), though the rate you actually receive will depend on your credit score, equity position, lender, and the prime rate at the time of your draw. New homeowners with less established equity and shorter payment history typically land at the higher end of the rate range.

HELOCs are tied to the prime rate (which moves with Federal Reserve decisions), meaning your rate can change over time. This is fundamentally different from a fixed-rate home equity loan or a cash-out refinance.

Rate factors specific to new homeowners:

- Less seasoning = higher perceived risk = higher rate for some lenders

- Lower equity position (CLTV above 80%) triggers rate add-ons at many institutions

- Credit score under 700 typically adds 0.25–0.75% to your rate

- Investment property HELOCs carry rates 0.5–1.5% higher than primary residence products

For context on how the broader mortgage market is moving in 2026, our financing and mortgage market update has the latest data.

Investment Property HELOC: Different Rules, Different Timeline

Getting a HELOC on an investment property after purchase is significantly harder than on a primary residence — and the timeline is longer. Most lenders require 12 months of seasoning on investment properties, and many major banks simply don’t offer investment property HELOCs at all.

Key differences for investment property HELOCs:

- Equity requirement: Lenders typically want 30–40% equity (CLTV of 60–70%) versus 15–20% for primary residences

- Credit score: 700+ is often the floor; 720+ gets you competitive products

- Rate premium: Expect rates 0.5–1.5% higher than primary residence HELOC rates

- Lender pool: Smaller — primarily credit unions, portfolio lenders, and specialty investment property lenders

- Documentation: Rental income must be documented; lenders want to see lease agreements and rental history

- Seasoning: 12 months is standard; some lenders require the property to have rental history before approving

If you’re building a real estate portfolio and planning to use equity from one property to fund the next, this strategy is extraordinarily powerful — but the timing and lender selection are everything. Our HELOC on Investment Property guide is required reading before you start that conversation with a lender.

Frequently Asked Questions

Q: How soon can I do a HELOC after purchasing a home if I put 20% down?

A: With 20% down, you meet the standard equity threshold on day one. Most lenders still require a 6-month seasoning period, but you’ll be in a strong position to apply as soon as that window closes. Credit unions may work with you at 3–6 months.

Q: Can I use a HELOC to buy another property right after purchasing my first home?

A: Yes — this is a common investor strategy. But you’ll need to wait for the seasoning period (typically 6–12 months), build enough equity to support a meaningful credit line, and find a lender comfortable with investment-purpose draws. The HELOC on Investment Property guide covers this in detail.

Q: How long does it take to get a HELOC approved once I apply?

A: Once you submit a complete application, most lenders take 2–6 weeks to close. Online lenders like Figure can move in as few as 5 business days. Traditional banks may take 4–8 weeks. The appraisal is often the longest step.

Q: Does a HELOC affect my ability to get another mortgage?

A: Yes. Even an unused HELOC credit line can count against your debt-to-income ratio with some lenders. If you’re planning to buy another property soon, factor this in before opening a large HELOC.

Q: What happens during the HELOC draw period?

A: The HELOC draw period is typically 10 years. During this time, you can borrow up to your credit limit, repay, and borrow again — like a credit card. Payments are usually interest-only during the draw period. After it ends, you enter a repayment period (usually 10–20 years) where you pay principal and interest.

Q: Can I get a HELOC if I’m self-employed and just bought a home?

A: Yes, but it’s more complex. You’ll need 2 years of tax returns showing consistent income, and some lenders use your net income (after deductions) rather than gross — which can lower your qualifying income significantly. Work with a lender experienced in self-employed borrowers.

Q: Is there a minimum HELOC amount?

A: Many lenders have a minimum credit line of $10,000–$25,000. If your equity only supports a smaller line, some lenders won’t bother with the application. A home equity loan (fixed amount, fixed rate) may be a better option for smaller equity positions.

Q: What if my home value dropped after I bought it — can I still get a HELOC?

A: If your home’s appraised value has dropped, your available equity shrinks accordingly. If your CLTV is now above 80–85%, most lenders won’t approve a HELOC until values recover or your mortgage balance decreases enough.

Q: Are HELOC closing costs negotiable?

A: Sometimes. Some lenders waive closing costs entirely in exchange for keeping the HELOC open for a minimum period (usually 2–3 years). Others charge $200–$500 in fees. Always ask what’s negotiable and whether there’s a prepayment penalty.

Q: How does the prime rate affect my HELOC payment?

A: Most HELOCs are priced at prime rate plus a margin (e.g., prime + 0.5%). When the Fed raises rates, prime goes up, and so does your HELOC rate. With current HELOC rates around 7.41% in May 2026, a 1% rate increase would add roughly $500/year per $50,000 drawn.

Q: What’s the difference between a HELOC and a home equity loan for new homeowners?

A: A HELOC is a revolving line of credit with a variable rate — flexible but rate-sensitive. A home equity loan gives you a lump sum at a fixed rate. For new homeowners with smaller equity positions, a home equity loan may be easier to qualify for since the fixed payment is more predictable for lenders.

Q: Do I need a new appraisal to get a HELOC after a recent home purchase?

A: Most lenders require a new appraisal or at minimum an automated valuation model (AVM) check. Some will use your purchase price if the purchase was recent (within 6–12 months) and the market hasn’t moved significantly. Ask your lender upfront — a full appraisal adds $300–$600 to your costs.

Conclusion: The Right Move Is Timing + Preparation

So — how soon can you do a HELOC after purchasing a home? The real answer is: as soon as your equity, credit, and lender’s seasoning requirements align. For most homeowners, that’s 6 to 12 months. For investors with strong equity positions and the right lender relationship, it can be sooner.

The homeowners who win with HELOCs aren’t the ones who rush — they’re the ones who spend those first 6–12 months setting up the conditions for a smooth, fast approval. That means:

- Protecting your credit score — no new debt, no missed payments

- Tracking your home’s value — know what comparable homes are selling for in your area

- Choosing the right lender early — start conversations with credit unions and community banks before you’re ready to apply

- Understanding your equity math — run the CLTV numbers yourself before any lender does

- Planning your use of funds — have a clear, value-building purpose for the HELOC before you draw a single dollar

The HELOC is an extraordinary financial tool when used with intention. It’s not gatekeeping to say timing matters — it’s just the truth. Let the equity cook, build your financial profile, and when the window opens, you’ll be ready to move with confidence.

For more on navigating the 2026 housing market as a buyer, investor, or homeowner, explore our U.S. home buyers market trends guide and our financing and mortgage tips hub.

{kind=link}