{"cover":"Professional landscape format (1536×1024) hero image for a real estate finance article. A confident real estate investor sits at a modern desk reviewing property documents and a laptop screen showing rental income data and equity charts. Warm burgundy and navy blue color palette with cream accents. No W-2 tax forms visible — instead, a rental property photo pinned to a board and a cash flow spreadsheet open on screen. Soft studio lighting, editorial magazine aesthetic, sharp depth of field. No text overlays or headlines on the image.","content":["Landscape format (1536×1024) infographic-style illustration showing a DSCR loan mechanics diagram: a rental property on the left with an arrow pointing to a debt service coverage ratio calculation (NOI divided by debt payments equals 1.25), then an arrow to a cash-out check. Clean financial chart aesthetic, burgundy and navy blue color scheme, minimal annotation labels on the diagram elements, white background with subtle grid lines, editorial quality.","Landscape format (1536×1024) showing a split-screen comparison: left side shows a traditional mortgage application desk piled with W-2 forms, tax returns, and pay stubs in muted gray tones; right side shows a DSCR loan application with only a lease agreement and property appraisal report, in warm burgundy and gold tones. Clean dividing line down the center, overhead flat-lay perspective, editorial real estate finance aesthetic, no large text overlays.","Landscape format (1536×1024) close-up financial dashboard on a large monitor showing DSCR loan rate data for 2026 — a line graph trending around 7% with comparison bars for conventional vs DSCR rates, color-coded in burgundy and navy blue. A real estate investor's hand points to the screen. Modern home office background, bokeh effect on background, sharp focus on screen data, editorial quality, small chart axis labels visible.","Landscape format (1536×1024) wide-angle view of a diverse portfolio of investment properties — single-family rental, short-term vacation rental with Airbnb-style signage, and a small multifamily building — arranged in a triptych layout with DSCR ratio badges overlaid on each property (1.10, 1.25, 1.40). Aerial drone-style perspective, golden hour lighting, burgundy and cream color accents, clean real estate investment visual, editorial magazine quality, no large text headlines.","Landscape format (1536×1024) showing a real estate investor reviewing a checklist on a clipboard with items like credit score gauge at 680+, property appraisal report, lease agreement, and entity documents. The setting is a modern home office with a rental property visible through the window. Flat-lay composition from above, burgundy clipboard accent, navy blue desk surface, cream paper documents, editorial quality photography style, small handwritten-style labels on checklist items visible."]

Last updated: May 24, 2026

Quick Answer: A DSCR cash out refinance lets real estate investors pull equity from a rental property based on the property's income — not their personal tax returns or W-2. If your rental generates enough cash flow to cover its debt payments, you can qualify. No employer verification, no income documentation, no problem.

Key Takeaways

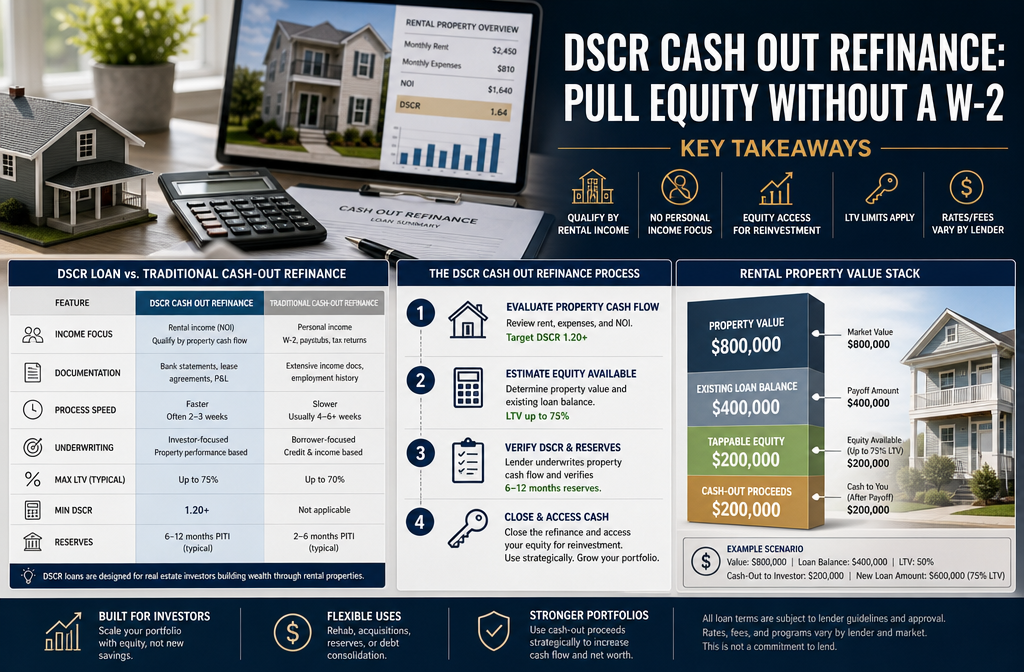

- DSCR stands for Debt Service Coverage Ratio — lenders divide your property's net operating income by its monthly debt payment to determine if you qualify.

- A DSCR of 1.0 or higher is typically the minimum; most lenders prefer 1.20 to 1.25 for a cash out refinance.

- No W-2, no tax returns, no pay stubs required — this is a non-QM (non-qualified mortgage) product designed for investors.

- Most lenders allow you to cash out up to 70–75% of the property's appraised value (LTV).

- DSCR loan rates in 2026 sit around 7% — slightly higher than conventional loans, but the trade-off is no income verification.

- DSCR loans work for single-family rentals, multifamily (typically up to 10 units), and short-term rentals like Airbnb properties.

- The BRRRR refinance strategy (Buy, Rehab, Rent, Refinance, Repeat) pairs naturally with DSCR cash out refinancing.

- DSCR loans now represent roughly 30% of non-QM originations, with refinance volume growing approximately 35% year over year — this product is mainstream, not fringe.

- Approval timelines typically run 3 to 5 weeks — faster than conventional investment property loans.

- This product is not ideal for owner-occupied homes, properties with negative cash flow, or borrowers with credit scores below 620.

What Exactly Is a DSCR Cash Out Refinance and How Does It Work?

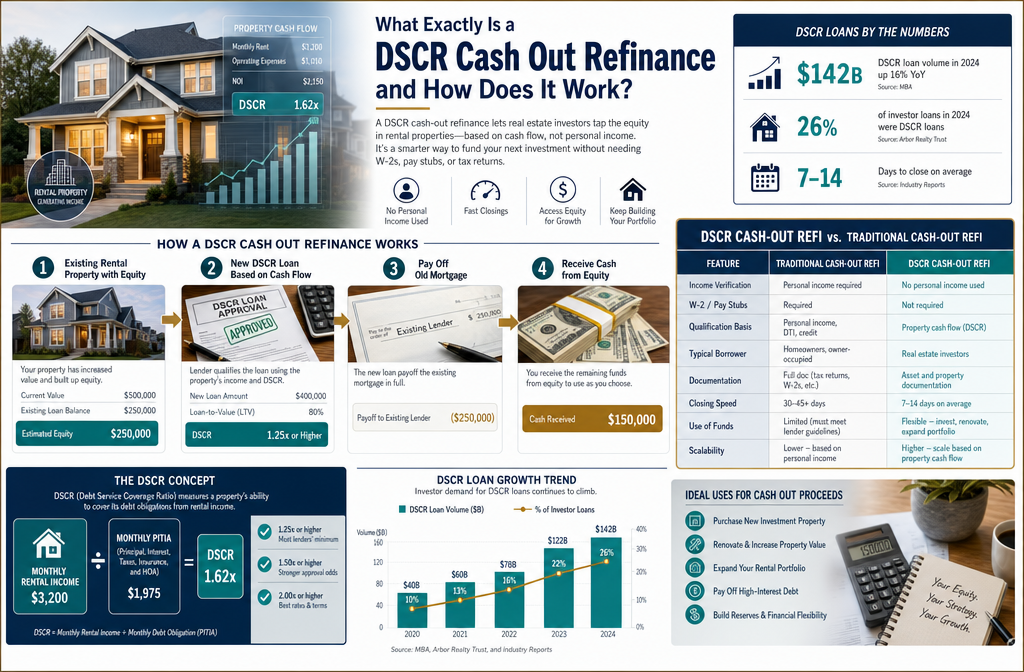

A DSCR cash out refinance is a type of investment property refinance where the lender qualifies you based on the rental income your property generates — not your personal income. You replace your existing mortgage with a new, larger loan and receive the difference in cash. The whole qualification process revolves around one number: your Debt Service Coverage Ratio.

Here's the math:

DSCR = Monthly Gross Rental Income ÷ Monthly Debt Payment (PITIA)

PITIA includes principal, interest, taxes, insurance, and any HOA dues.

Example:

- Monthly rent: $2,400

- Monthly PITIA: $1,800

- DSCR: 2,400 ÷ 1,800 = 1.33 ✅ (strong approval territory)

A DSCR above 1.0 means the property earns more than it costs to carry. A DSCR below 1.0 means the rent doesn't fully cover the mortgage — most lenders won't touch that for a cash out.

This is a DSCR loan no income verification product, which means your W-2, 1040s, and employment history are completely irrelevant to the underwriter. The property does the talking.

Why this matters in 2026: DSCR refinance volume has grown approximately 35% year over year as more self-employed investors, gig workers, and high-net-worth borrowers look for ways to access equity without showing personal income. It's not gatekeeping anymore — this product is widely available through non-QM lenders across the country.

For a deeper breakdown of qualifying criteria, check out our guide on DSCR loan requirements for real estate investors.

DSCR Cash Out Refinance: Pull Equity Without a W-2 — The Full Picture

This is the extraordinary part: you can walk into a lender's office with zero W-2 income and still pull five or six figures out of your rental property. That's not a loophole — it's exactly what this product was designed for.

Who this was built for:

- Self-employed borrowers whose tax returns show low taxable income (after write-offs)

- Real estate investors with large portfolios and complex income structures

- High-income professionals who recently changed jobs or are between positions

- Foreign nationals investing in U.S. rental properties

- Investors doing a BRRRR refinance strategy — pulling cash out to fund the next deal

The core mechanics of a cash out DSCR loan:

- You own a rental property with existing equity (either from appreciation or paid-down principal)

- A lender orders an appraisal to determine current market value

- The lender calculates your DSCR using current or projected market rent

- If the DSCR clears their threshold (usually 1.0–1.25), you're approved

- You receive a new loan for a higher amount than your current balance

- The difference between your old loan balance and the new loan amount is your cash out

What you can do with that cash:

- Fund the down payment on your next rental property

- Refinance a hard money loan you used to acquire or renovate a property

- Cover renovation costs on another asset

- Build a cash reserve for your portfolio

- Pay off high-interest business debt

The DSCR cash out refinance is essentially the investor's version of a home equity play — and it scales beautifully. If you're already thinking about portfolio growth, our breakdown of cash flow real estate investing strategies pairs directly with this approach.

How Much Cash Can You Pull Out With a DSCR Loan Without Showing Income?

Most DSCR lenders cap cash out refinances at 70–75% loan-to-value (LTV). That means if your property appraises at $400,000, the maximum new loan would be $280,000–$300,000. If your current balance is $180,000, you'd receive $100,000–$120,000 in cash.

LTV limits by scenario:

| Property Type | Typical Max LTV (Cash Out) |

|---|---|

| Single-family rental | 70–75% |

| 2–4 unit multifamily | 70–75% |

| 5–10 unit multifamily | 65–70% |

| Short-term rental (STR) | 65–70% |

| Mixed-use property | 60–65% |

Factors that affect how much you can pull:

- Appraised value — higher appraisal = more available equity

- DSCR ratio — a stronger ratio (1.3+) may allow higher LTV with some lenders

- Credit score — borrowers above 740 often get better LTV allowances

- Property type — STRs and mixed-use properties carry slightly tighter caps

- Lender guidelines — non-QM lenders vary significantly; shop multiple options

Common mistake: Investors assume they can cash out at 80% LTV like a conventional refinance. DSCR cash out loans carry a lower ceiling because lenders are taking on more risk without income verification. Plan your numbers around 70–75% to avoid surprises.

What Credit Score Do You Need for a DSCR Cash Out Refinance?

Most DSCR lenders require a minimum credit score of 620–640 for a cash out refinance. That said, the best rates and highest LTV allowances go to borrowers at 700 and above. If your score is below 660, expect a higher rate and stricter DSCR requirements.

Credit score tiers and what to expect:

| Credit Score | Typical Rate Impact | Max LTV (Cash Out) |

|---|---|---|

| 740+ | Best available rate | Up to 75% |

| 700–739 | Slight premium | 70–75% |

| 660–699 | Moderate premium | 65–70% |

| 620–659 | Higher rate, stricter DSCR | 60–65% |

| Below 620 | Most lenders decline | Not available |

Edge case: Some lenders will approve a DSCR cash out refinance with a 600 score if the DSCR is very strong (1.5+) and the LTV is conservative (under 60%). These are exceptions, not the rule.

Quick tip: If your credit score is sitting at 650 and you're planning a cash out in the next 6–12 months, let it cook before you pull the trigger. Paying down revolving balances and disputing errors can move your score 30–50 points in 60–90 days — and that difference can save you thousands in interest over the life of the loan.

How Do DSCR Loans Compare to Traditional Mortgage Refinancing?

DSCR loans and conventional investment property refinances serve the same goal — pulling equity from a rental — but the qualification process is completely different. Conventional loans look at you. DSCR loans look at the property.

Side-by-side comparison:

| Feature | Conventional Refinance | DSCR Cash Out Refinance |

|---|---|---|

| Income documentation | W-2, tax returns, pay stubs required | Not required |

| Qualification basis | Borrower's personal DTI | Property's rental income |

| Max properties financed | 10 (Fannie/Freddie limit) | No hard cap (varies by lender) |

| Max LTV (cash out) | 75–80% | 70–75% |

| Rates (2026) | ~6.5–7.0% | ~7.0–7.75% |

| Approval speed | 4–8 weeks | 3–5 weeks |

| Self-employed friendly | Limited | Yes |

| Loan type | QM (qualified mortgage) | Non-QM |

Choose a DSCR cash out refinance if:

- You're self-employed with significant write-offs on your taxes

- You already have 10+ financed properties (Fannie/Freddie won't touch you)

- You need to close faster than a conventional loan allows

- Your personal DTI is too high to qualify conventionally

Stick with conventional if:

- You have strong W-2 income and a clean tax return

- You want the absolute lowest rate available

- You're refinancing your primary residence (DSCR doesn't apply)

For a broader look at your mortgage options, our mortgage options guide covers the full spectrum from FHA to jumbo to non-QM products.

What Types of Properties Qualify for DSCR Cash Out Refinancing?

DSCR cash out refinancing works for income-producing investment properties — the key word being income-producing. The property must generate rent (or demonstrable rental income potential) because that's what the lender is underwriting.

Eligible property types:

- Single-family rentals (1 unit)

- 2–4 unit residential properties (duplex, triplex, fourplex)

- 5–10 unit small multifamily (some lenders go higher)

- Condominiums used as rentals (warrantable and non-warrantable)

- Short-term rentals / vacation rentals (Airbnb, VRBO)

- Mixed-use properties with residential rental component

Not eligible:

- Owner-occupied primary residences

- Fix-and-flip properties (no stabilized rental income)

- Raw land or vacant lots

- Commercial-only properties (retail, office, industrial)

- Properties in active foreclosure or with title issues

Important note on short-term rentals: STR properties are eligible, but lenders handle them differently. Some use AirDNA market data or a 12-month average of actual Airbnb income to calculate DSCR. Others use a percentage of gross STR revenue (typically 75%). If you're running a vacation rental, check out our Airbnb vs Vacasa property management comparison to understand how management structure affects your net income — and therefore your DSCR.

What Are the Typical DSCR Loan Rates in 2026?

DSCR loan rates in 2026 sit around 7% for well-qualified borrowers — generally 0.5 to 1.0 percentage points above comparable conventional investment property rates. The spread exists because DSCR loans are non-QM products and carry more lender risk.

Rate factors that move the needle:

- Credit score: The biggest driver. A 740+ score gets you near the bottom of the range; a 640 score can push your rate above 8%.

- LTV: Lower LTV = lower rate. Borrowing at 60% LTV will price better than 75%.

- DSCR strength: Some lenders tier rates based on DSCR. A 1.5 DSCR may qualify for a better rate than a 1.05.

- Property type: STRs and multifamily above 4 units typically carry a rate premium.

- Loan term: 30-year fixed is most common. Some lenders offer 5/1 or 7/1 ARMs at lower initial rates — use these carefully.

- Prepayment penalty: Many DSCR loans include a 3–5 year prepayment penalty (step-down structure). Factor this into your exit strategy.

So based reality check: A rate of 7–7.5% sounds high compared to the 3% pandemic-era rates, but the comparison that matters is cash-on-cash return vs. cost of capital. If your rental yields a 9–10% cash-on-cash return and your DSCR loan costs 7.25%, you're still positive. Run the numbers for your specific deal before making a rate judgment.

To compare lenders and find the most competitive pricing, our best DSCR loan lenders for investment properties guide is a solid starting point.

Can Real Estate Investors Use DSCR Refinancing for Multiple Properties?

Yes — and this is one of the biggest advantages of DSCR loans over conventional financing. There is no hard cap on the number of properties you can finance with DSCR loans, unlike Fannie Mae and Freddie Mac conventional loans, which limit most investors to 10 financed properties.

How portfolio investors use DSCR refinancing:

- BRRRR refinance strategy: Buy a distressed property, rehab it, rent it out, then do a DSCR cash out refinance to recycle your capital into the next deal. Rinse and repeat.

- Refinance hard money loan: Many investors use hard money loans to acquire and renovate properties quickly. Once the property is stabilized and rented, a DSCR refinance replaces the expensive short-term debt with a long-term fixed rate.

- Portfolio-level cash out: Pull equity from one property to fund the down payment on another — scaling without selling.

What lenders look for with multiple properties:

- Each property is underwritten individually based on its own DSCR

- Your overall credit profile still matters (score, payment history)

- Some lenders have portfolio caps (e.g., max $5M or 20 properties with one lender)

- Holding properties in an LLC is common and generally accepted — some lenders require it

Edge case: If you're doing a DSCR cash out refinance on multiple properties simultaneously, stagger your closings. Pulling equity from several properties at once can flag lenders and complicate title work. One at a time keeps things clean.

For investors building a portfolio from the ground up, our guide on how to invest in real estate with $5,000 or less shows how to get started before you have equity to pull.

Are DSCR Cash Out Refinances Good for Short-Term Rental Properties?

DSCR cash out refinancing works for short-term rentals, but it requires more documentation and lender selection than a standard long-term rental. The core challenge is income verification — STR income fluctuates seasonally, and lenders need to underwrite a stable DSCR.

How lenders calculate DSCR for STRs:

- Method 1: 12-month average of actual platform deposits (Airbnb, VRBO payouts)

- Method 2: AirDNA or similar market data showing projected annual revenue

- Method 3: A percentage of gross STR income (typically 75%) applied to the DSCR calculation

What makes STR DSCR refinances trickier:

- Not all DSCR lenders accept STR income — you need a lender that specifically handles short-term rental properties

- Seasonal markets (beach towns, ski resorts) can show strong summer numbers but weak winter DSCR — lenders average this out

- Some municipalities are restricting STR licenses; a lender may require proof of active licensure

- LTV caps are slightly lower (65–70%) compared to long-term rentals

Decision rule: If your STR property averages a DSCR of 1.25 or higher across a full 12-month period and you have 12 months of documented platform income, you're in a strong position. If you've owned the property less than 12 months, some lenders will use market data projections instead — but expect more scrutiny.

What Are the Most Common Mistakes People Make With DSCR Cash Out Loans?

The most common mistake is treating a DSCR cash out refinance like a conventional loan and being surprised when the rules are different. Here are the real pitfalls — and how to avoid them.

Mistake #1: Overestimating the property's DSCR

Investors sometimes calculate DSCR using gross rent without accounting for vacancy, insurance, taxes, or HOA. Lenders use PITIA — the full payment — in the denominator. Run the real numbers before applying.

Mistake #2: Ignoring the prepayment penalty

Many DSCR loans carry a 3–5 year step-down prepayment penalty (e.g., 5/4/3/2/1). If you plan to sell or refinance again within that window, you could owe thousands in penalties. Read the loan terms carefully.

Mistake #3: Pulling too much equity

Cashing out to 75% LTV leaves very little cushion. If the market dips or you need to sell, you could end up underwater. A conservative cash out (60–65% LTV) gives you more breathing room.

Mistake #4: Not shopping lenders

DSCR loan rates and guidelines vary significantly across lenders. One lender might quote 7.5% with a 1.25 DSCR requirement; another might offer 7.0% with a 1.10 minimum. Shopping 3–4 lenders is impeccable practice.

Mistake #5: Refinancing a hard money loan too early

If you used hard money to acquire a property and it's not yet stabilized (fully rented, 90-day seasoning), most DSCR lenders won't refinance it. Wait until the property has a signed lease and 60–90 days of rental history.

Mistake #6: Holding the property personally when lenders prefer an LLC

Some DSCR lenders require the property to be in an LLC. Others prefer it. If you're building a portfolio, structuring properties in entities from the start avoids title transfer headaches later.

What Documentation Do You Need to Get Approved for a DSCR Cash Out Refinance?

The documentation list for a DSCR cash out refinance is refreshingly short compared to a conventional loan — no income verification means no tax returns, no W-2s, and no employment letters.

Standard DSCR cash out refinance documentation:

- ✅ Government-issued photo ID

- ✅ Property appraisal (ordered by lender)

- ✅ Current lease agreement (or market rent analysis if vacant)

- ✅ 12 months of mortgage payment history (or payoff statement if refinancing hard money)

- ✅ Homeowners/landlord insurance declaration page

- ✅ Entity documents (if property is held in LLC — articles of organization, operating agreement)

- ✅ Bank statements (2–3 months, to verify reserves)

- ✅ Title report (ordered by lender/title company)

- ✅ STR income statements (if short-term rental — 12 months of platform payouts)

What you do NOT need:

- ❌ W-2 forms or pay stubs

- ❌ Personal tax returns (1040s)

- ❌ Employer verification letters

- ❌ Personal debt-to-income calculation

Reserve requirements: Most DSCR lenders want to see 3–6 months of PITIA in liquid reserves after closing. Some require 12 months for cash out transactions. This is non-negotiable — keep your reserves documented and accessible.

How Long Does the DSCR Loan Approval Process Usually Take?

A DSCR cash out refinance typically closes in 3 to 5 weeks from application to funding. This is generally faster than a conventional investment property refinance, which can run 4–8 weeks due to the income verification process.

Typical DSCR refinance timeline:

| Stage | Typical Duration |

|---|---|

| Application + initial review | 1–3 days |

| Appraisal ordered + completed | 7–14 days |

| Underwriting review | 5–7 days |

| Conditional approval + doc collection | 3–5 days |

| Clear to close | 1–2 days |

| Closing + funding | 1–3 days |

| Total | ~21–35 days |

What slows things down:

- Appraisal delays (common in rural markets or unique properties)

- Title issues (liens, unclear ownership, probate situations)

- LLC documentation that's incomplete or outdated

- Lender backlogs during high-volume periods

What speeds things up:

- Having all documents ready before application

- Using a lender that specializes in DSCR loans (not a general bank)

- A clean title with no encumbrances

- A property with an active lease and documented rental history

Who Should Not Use a DSCR Cash Out Refinance Strategy?

A DSCR cash out refinance is a fresh, powerful tool — but it's not the right move for everyone. Knowing when to pass is just as important as knowing when to pull the trigger.

Skip the DSCR cash out refinance if:

Your property has a DSCR below 1.0. If the rent doesn't cover the mortgage, you won't qualify for most DSCR lenders. Fix the cash flow problem first — raise rents, reduce expenses, or wait for the market to appreciate before refinancing.

You plan to sell within 3 years. Prepayment penalties on DSCR loans can eat into your proceeds significantly. If your exit timeline is short, a HELOC or bridge loan may cost less overall. Check out our breakdown of HELOC on investment property strategies for a comparison.

Your credit score is below 620. Most DSCR lenders won't approve a cash out refinance below this threshold. Work on your credit profile first.

The property is your primary residence. DSCR loans are for investment properties only. If you live in the home, you need a conventional cash out refinance.

You're in a negative equity position. If you owe more than the property is worth, a cash out refinance isn't possible regardless of DSCR.

You need the cash immediately. The 3–5 week timeline is faster than conventional, but if you need funds in 7 days, a DSCR refinance won't get there. A hard money bridge loan or personal line of credit may be a better short-term solution.

Your property is vacant with no rental history. Some lenders will use market rent projections, but many require an active lease. A vacant property is a harder approval.

Frequently Asked Questions

Q: What does DSCR stand for in real estate?

DSCR stands for Debt Service Coverage Ratio. It measures how much rental income a property generates relative to its mortgage payment. A DSCR of 1.25 means the property earns 25% more than it costs to carry.

Q: Can I do a DSCR cash out refinance if I'm self-employed?

Yes — this is one of the primary use cases. DSCR loans require no personal income documentation, making them ideal for self-employed borrowers whose tax returns show low net income due to business deductions.

Q: What is the minimum DSCR for a cash out refinance?

Most lenders require a minimum DSCR of 1.0 to 1.25 for a cash out transaction. Some lenders offer "DSCR below 1.0" products, but these carry higher rates and lower LTV caps.

Q: Can I use a DSCR loan to refinance a hard money loan?

Yes. Refinancing a hard money loan into a DSCR loan is one of the most common use cases, especially for BRRRR investors. The property typically needs 60–90 days of rental history and a signed lease before most DSCR lenders will refinance it.

Q: Are DSCR loans available for LLCs?

Yes. Most DSCR lenders actively lend to LLCs and other entities. Some lenders actually require the property to be held in an entity. Have your LLC documents — articles of organization and operating agreement — ready at application.

Q: How is DSCR different from a non-QM loan?

DSCR is a specific type of non-QM loan. Non-QM (non-qualified mortgage) is the broader category of loans that don't meet Fannie Mae/Freddie Mac guidelines. DSCR loans are non-QM products that qualify borrowers based on property income rather than personal income.

Q: What happens if my DSCR drops after closing?

Nothing — once your loan closes, the DSCR is locked in. The lender doesn't re-underwrite your DSCR after closing. However, if you want to refinance again in the future, your DSCR at that time will matter.

Q: Can I do a DSCR cash out refinance on a property I just bought?

Most lenders require a seasoning period of 6–12 months before allowing a cash out refinance on a recently purchased property. Some lenders allow delayed financing exceptions, but standard cash out requires seasoning.

Q: Do DSCR loans show up on my personal credit?

Most DSCR loans held in an LLC do not appear on your personal credit report. Loans held in your personal name will. Check with your lender on how they report to credit bureaus.

Q: Is a DSCR cash out refinance taxable?

The cash you receive from a refinance is not taxable income — it's debt, not earnings. However, consult a tax professional regarding interest deductibility and how the cash is used, especially if you're deploying it into other investments.

Q: What's the difference between a DSCR refinance and a DSCR purchase loan?

The qualification mechanics are the same — both use rental income to determine eligibility. The difference is that a cash out refinance replaces an existing mortgage and generates proceeds, while a purchase loan is used to acquire a new property.

Q: Where can I find DSCR loan lenders?

DSCR loans are offered by non-QM lenders, private lenders, and some regional banks. Avoid going to a traditional bank first — most don't offer DSCR products. Our guide to the best DSCR loan lenders for investment properties is a good place to start your search.

Conclusion: Pull the Equity, Not Your Hair Out

The DSCR cash out refinance is one of the most extraordinary tools available to real estate investors in 2026 — and the fact that it doesn't require a W-2 is exactly the point. Traditional lenders built their systems for employees. DSCR loans were built for investors.

If your rental property generates solid income, has meaningful equity, and you have a credit score above 660, you have a real path to pulling that equity without jumping through the income verification hoops that conventional lenders require.

Your action plan:

- Calculate your DSCR — divide your monthly gross rent by your full PITIA payment. If it's above 1.20, you're in strong territory.

- Pull your credit report — know your score before you apply. Anything above 700 gets you better rates.

- Get a rough appraisal estimate — use recent comps in your area to estimate your current LTV. If you're below 70%, you have room to cash out.

- Shop at least 3 DSCR lenders — rates and guidelines vary. Don't take the first offer.

- Decide what the cash does next — have a clear plan for the proceeds before you close. Idle capital is wasted capital.

The investors who are scaling their portfolios right now aren't waiting for rates to drop to 3% again. They're running their numbers, using the tools available in 2026, and letting their properties do the heavy lifting.

That's not gatekeeping — that's just how the game is played when you know the rules.

For more on building a cash-flowing portfolio, explore our real estate investment strategies hub and our guide on 4 types of real estate investments to see where DSCR refinancing fits in your bigger picture.

{kind=link}