Last updated: February 24, 2026

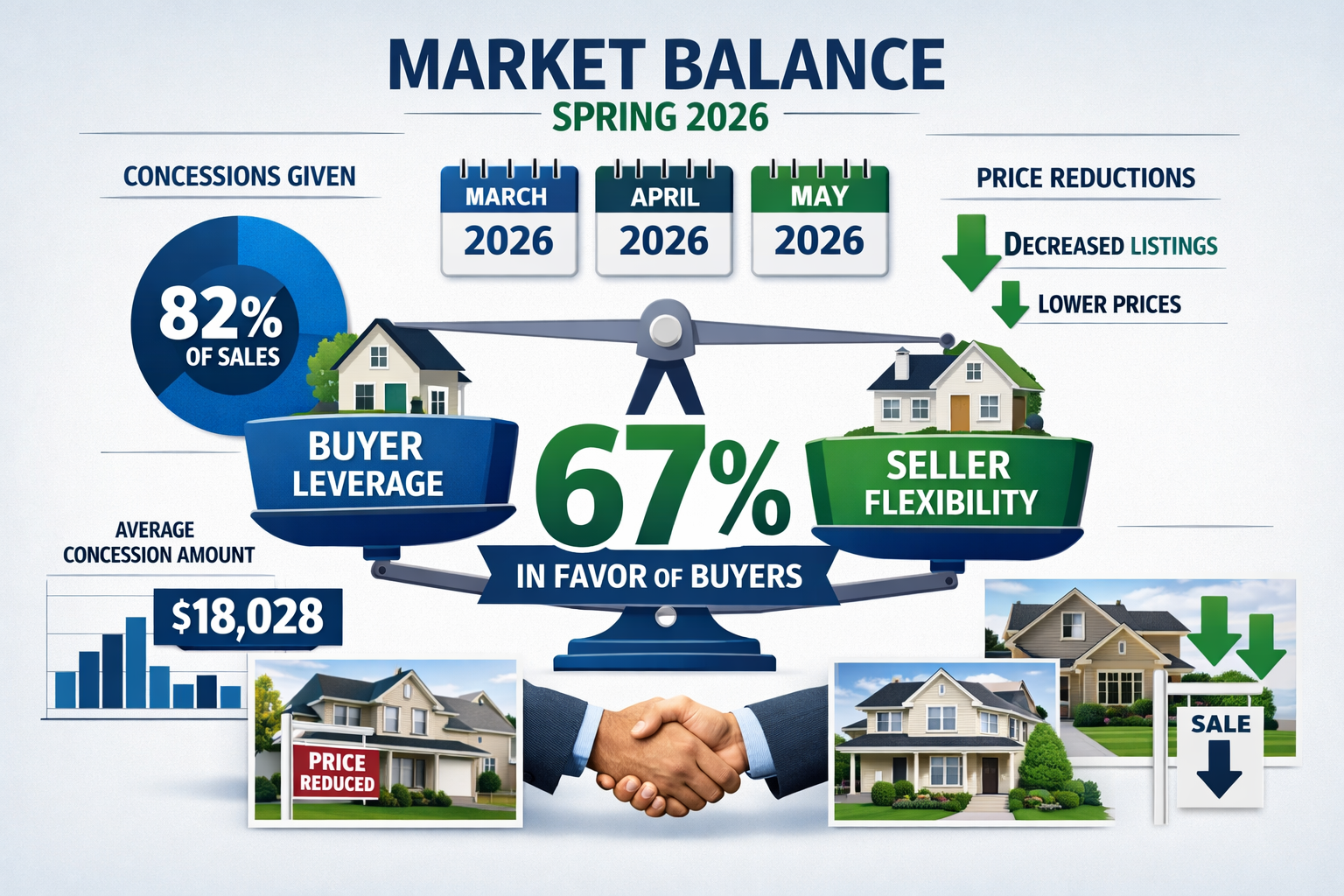

Spring 2026 is shaping up to be extraordinary for real estate negotiations. With 67% of homes now selling with seller-paid concessions averaging $18,028 and price reductions hitting 57% of listings, buyers and sellers face a fundamentally different market than the pandemic-era frenzy[1]. The housing market has become the most balanced it's been in almost a decade, creating fresh opportunities for strategic negotiators who understand the seasonal dynamics at play[4]. This comprehensive guide reveals the ranked 10 spring negotiation tactics for seller concessions in 2026 that can save thousands or help close deals faster.

Key Takeaways

- Market conditions favor negotiation: 67% of homes sold in early 2026 included seller concessions, with average contributions reaching $18,028 per transaction[1]

- Spring timing requires different tactics: Peak selling season (March-May) brings 33-day average sale times but also 35% of buyers paying above asking price in May-June[3]

- Price reductions are widespread: 57% of January 2026 listings had price cuts averaging $29,851, up from 39% the previous year[1]

- Rate buydowns provide competitive edge: Sellers offering to reduce buyer mortgage rates gain significant negotiation leverage in competitive spring markets[2]

- Closing cost coverage remains most requested: This concession reduces buyer cash requirements and remains the top-requested seller contribution[2]

- Repair credits beat actual repairs: Offering credit for repairs instead of completing them gives buyers control and speeds closing timelines

- Home warranties add perceived value: These relatively low-cost seller concessions ($400-600) can tip the balance in multiple-offer situations

- Appliance inclusions work strategically: Leaving high-end appliances can justify higher sale prices while costing sellers less than price reductions

- Timing your offer matters: Early spring (March-April) provides better negotiation leverage than peak competition months (May-June)[3]

- Flexibility beats stubbornness: The 2026 market rewards sellers who adapt quickly and buyers who present clean, attractive offers with strategic concession requests

Quick Answer

The ranked 10 spring negotiation tactics for seller concessions in 2026 leverage current market conditions where sellers are offering record concessions and price reductions. The top strategies include requesting closing cost coverage (most common and effective), negotiating rate buydowns to offset higher mortgage rates, securing repair credits instead of completed work, and timing offers strategically during early spring when competition is lower. Sellers benefit from offering home warranties, including appliances, and being flexible on closing dates—all of which cost less than price reductions while making properties more competitive during the peak March-May selling season when homes sell in just 33 days but face intense buyer competition[1][3].

What Makes Spring 2026 Different for Negotiating Seller Concessions?

Spring 2026 represents a fundamental shift in negotiation dynamics compared to recent years. The market has transitioned from pandemic-era seller dominance to the most balanced conditions in nearly a decade, creating opportunities for both buyers and sellers who understand how to leverage concessions strategically[4].

Current market data shows sellers are significantly more willing to negotiate. In January 2026, 67% of closed transactions included seller-paid concessions averaging $18,028—a substantial increase from previous years[1]. Additionally, 57% of homes experienced price reductions averaging $29,851, compared to just 39% of listings a year earlier[1].

Why this matters for spring negotiations:

- Mortgage rates stabilizing near 6% create a more predictable financing environment, allowing buyers to calculate exactly how much seller concessions can reduce their monthly payments[6]

- Inventory levels improving give buyers more options and negotiation leverage compared to the limited choices of 2021-2023

- Seasonal competition intensifies during peak spring months (May-June), when 35% of buyers pay above list price versus 24% in January[3]

- Days on market compress to just 33 days during spring compared to 49 days in winter, requiring faster decision-making and clearer negotiation strategies[3]

The key strategic insight: Early spring (March-April) offers the sweet spot for buyer negotiations, while late spring (May-June) favors sellers who can leverage increased competition. Understanding this timing is paramount for maximizing concession negotiations.

Common mistake to avoid: Assuming spring always favors sellers. While competition increases, the 2026 market shows sellers are more flexible than in years past, making concession requests viable even during peak season when presented strategically.

How Do Closing Cost Concessions Work in the 2026 Spring Market?

Closing cost concessions remain the most requested and commonly granted seller contribution in 2026. This tactic allows sellers to contribute funds at closing to cover buyer expenses like loan origination fees, appraisal costs, title insurance, and prepaid items[2].

The mechanics are straightforward: Instead of reducing the purchase price, sellers agree to pay a percentage (typically 2-3%) of the sale price toward buyer closing costs. For a $400,000 home, a 3% concession equals $12,000—reducing the buyer's cash needed at closing while keeping the sale price higher.

Why this strategy ranks #1 for spring 2026:

- Preserves comparable sales values by maintaining higher sale prices in the neighborhood

- Reduces buyer cash requirements without affecting the loan-to-value ratio for financing

- Appeals to multiple buyer types including first-time buyers, investors, and move-up purchasers

- Costs sellers less than equivalent price reductions because the higher sale price may offset the concession through better appraisal comps

Strategic implementation for buyers:

- Request specific dollar amounts rather than percentages (e.g., "$8,000 toward closing costs" instead of "3% concession")

- Ensure your lender confirms the maximum allowable concession for your loan type (FHA allows up to 6%, conventional typically 3-9% depending on down payment)

- Get preapproval documentation showing you qualify at the full purchase price before requesting concessions

- Present the request with your initial offer rather than during counteroffers

For sellers:

- Calculate your net proceeds with closing cost concessions versus price reductions to determine which costs less

- Advertise willingness to offer concessions in your listing to attract more buyers

- Set a maximum concession amount you'll consider (typically 2-3% of list price)

- Require buyers to be fully qualified at the purchase price before agreeing to concessions

Decision rule: Choose closing cost concessions if you need to reduce buyer barriers without lowering your home's perceived market value. This works best when comparable sales support your asking price and you're competing against similar homes without concession offers.

For more strategies on getting sellers to cover these expenses, check out our guide on how to get a home seller to pay closing costs upfront.

Why Are Rate Buydowns the Most Impactful Spring 2026 Concession?

Rate buydowns have emerged as an extraordinary negotiation tool in 2026 as mortgage rates hover near 6%[6]. This concession allows sellers to pay a one-time fee to reduce the buyer's mortgage interest rate, either temporarily or permanently[2].

Two main types of rate buydowns:

Temporary buydowns (2-1 or 1-0 structures):

- 2-1 buydown: Rate reduced by 2% first year, 1% second year, then returns to full rate

- 1-0 buydown: Rate reduced by 1% first year only

- Cost to seller: Typically 1-2% of loan amount

- Benefit to buyer: Lower initial payments, easier qualification

Permanent buydowns (discount points):

- Each point costs 1% of loan amount and reduces rate by approximately 0.25%

- Permanent reduction for loan life

- Cost to seller: Higher upfront (2-4% of loan amount for meaningful reduction)

- Benefit to buyer: Long-term savings, lower monthly payment throughout loan

Real-world example: On a $400,000 loan at 6% interest, a 2-1 buydown might cost the seller $8,000 but reduces the buyer's first-year payment from $2,398 to $2,128 (saving $270/month). This can be the difference between qualifying for the loan and not qualifying.

Why this ranks #2 for spring negotiations:

- Addresses the #1 buyer objection (affordability) without reducing sale price

- Helps buyers qualify who are on the edge of debt-to-income ratios

- Differentiates your property in competitive spring markets where multiple homes are similar

- Appeals to rate-sensitive buyers who are waiting for better financing conditions

Strategic timing: Rate buydowns work impeccably in early spring when buyers are comparing monthly payment scenarios across multiple properties. Advertising "Seller will buy down your rate" in listings generates significantly more showings.

Common mistake: Sellers offering generic "seller concessions available" without specifying rate buydowns. Being explicit about this benefit attracts more qualified buyers and positions your home as more affordable than competitors at the same price point.

Learn more about powerful negotiation strategies in our negotiation power moves guide.

What Repair Credits Should Buyers Request During Spring Inspections?

Repair credits rank #3 among spring 2026 negotiation tactics because they provide flexibility, speed up closings, and give buyers control over contractor selection and work quality.

The fundamental difference: Instead of requiring sellers to complete repairs before closing, buyers request a credit (dollar amount) at closing to handle repairs themselves after taking ownership.

Top repair credit categories for spring 2026:

Major systems (HVAC, electrical, plumbing):

- Average credit range: $2,000-$8,000

- Best approach: Get contractor estimates and request 75-100% of quoted amount

- Seller benefit: Avoids delays from contractor scheduling during busy spring season

Roof repairs:

- Average credit range: $3,000-$15,000 depending on scope

- Best approach: Request credit based on professional roofing inspection report

- Timing advantage: Spring roof repairs face 3-4 week contractor delays; credits avoid this

Foundation and structural issues:

- Average credit range: $5,000-$25,000+

- Best approach: Require structural engineer report, then negotiate based on findings

- Strategic note: Large structural credits may affect appraisal; sometimes price reduction works better

Cosmetic and minor repairs:

- Average credit range: $500-$3,000

- Best approach: Bundle multiple small items into one credit request

- Negotiation tip: Sellers more likely to grant these than major system credits

Why repair credits beat completed repairs in spring 2026:

- Speed matters: Spring homes sell in 33 days on average[3]—repair credits prevent closing delays

- Buyer control: Buyers choose contractors and supervise quality rather than accepting seller's cheapest option

- Seller convenience: Sellers avoid coordinating multiple contractors during move-out

- Lender approval: Credits are easier to document than work-in-progress for underwriting

Strategic framework for buyers:

- Request credits within 3-5 days of inspection to maintain momentum

- Provide specific dollar amounts backed by contractor estimates

- Prioritize safety and major system issues over cosmetic items

- Be prepared to split the difference (ask for $10,000, settle for $6,000-7,000)

For sellers:

- Set a maximum credit threshold before listing (e.g., "won't exceed $5,000 in credits")

- Get your own contractor estimates to counter inflated buyer quotes

- Offer credits for items you know need work rather than waiting for buyer discovery

- Consider pre-listing inspections to address major issues before spring market

Decision rule: Choose repair credits over price reductions when inspection items are legitimate but not deal-breakers. Credits maintain your sale price while addressing buyer concerns. Choose completed repairs only for items that affect appraisal value or buyer financing approval.

How Do Home Warranties Influence Spring 2026 Negotiations?

Home warranties rank #4 because they provide disproportionate perceived value relative to actual cost—a seller can invest $400-600 and create thousands of dollars in buyer confidence.

What home warranties cover in 2026:

- Major appliances (refrigerator, dishwasher, washer/dryer, oven)

- HVAC systems (heating and air conditioning)

- Electrical systems

- Plumbing systems

- Water heaters

- Garage door openers

Typical costs and coverage:

- Basic plans: $400-500 annually

- Comprehensive plans: $600-800 annually

- Service call deductibles: $75-125 per visit

- Coverage period: Usually 12 months from closing

Strategic value in spring negotiations:

For buyers:

- Reduces anxiety about inheriting expensive repair bills

- Particularly valuable for first-time buyers unfamiliar with home maintenance costs

- Provides 12-month buffer to budget for future repairs

- Can be negotiated as seller-paid for first year, then buyer decides whether to renew

For sellers:

- Costs less than $600 but can tip the balance in multiple-offer situations

- Signals confidence in home's condition ("I'm so confident, I'll warranty it")

- Addresses buyer concerns without making specific repair commitments

- Can substitute for small repair credit requests

When home warranties work best:

- Homes with older appliances or systems (8+ years old)

- First-time buyer transactions where peace of mind matters

- Properties where seller knows systems are functional but aging

- Competitive spring markets where small differentiators matter

When to skip warranties:

- Luxury homes where buyers expect newer, high-end systems

- Investment properties where investors self-insure

- Homes with brand-new systems that carry manufacturer warranties

- Situations where buyers specifically request cash credits instead

Negotiation language that works: "Seller will provide a comprehensive home warranty policy at closing covering all major systems and appliances for 12 months" is more compelling than "Seller may consider warranty."

Common mistake: Buyers assuming home warranties cover everything. These policies have exclusions, coverage limits, and require proper maintenance. Read the policy details before accepting a warranty in lieu of repair credits for known issues.

For insights on which warranty companies offer the best coverage, see our top 5 best home warranty companies guide.

What Appliances and Fixtures Should Sellers Include in Spring Offers?

Including appliances and fixtures ranks #5 because it allows sellers to add value without cash outlays while potentially justifying higher sale prices.

High-value inclusions for spring 2026:

Kitchen appliances:

- Refrigerator (especially high-end brands like Sub-Zero, Viking)

- Wine cooler or beverage refrigerator

- High-end range or cooktop

- Built-in microwave

- Dishwasher (if upgraded model)

Laundry equipment:

- Front-load washer and dryer sets

- Pedestal bases

- Stackable units in condos/townhomes

Technology and smart home:

- Smart thermostats (Nest, Ecobee)

- Video doorbell systems

- Smart lighting systems

- Whole-home audio equipment

- Security system equipment

Outdoor items:

- Patio furniture sets

- Grills (especially built-in models)

- Outdoor heaters or fire pits

- Lawn equipment and tools

- Shed contents

Strategic pricing implications:

Including a $3,000 refrigerator, $2,000 washer/dryer set, and $1,500 patio furniture (total $6,500 in items) might allow you to price $5,000-8,000 higher than comparable homes while still appearing more valuable. Buyers perceive "fully equipped" homes as move-in ready and worth premium pricing.

What to exclude (unless specifically negotiated):

- Family heirlooms and antiques

- Custom window treatments (unless they perfectly fit unusual windows)

- Expensive chandeliers or light fixtures with sentimental value

- Outdoor plants and landscaping features you want to transplant

- Any items that would leave visible gaps or damage if removed

Negotiation tactics for buyers:

- Review listing photos carefully and note all visible appliances and fixtures

- Specifically list desired items in your offer: "Offer includes refrigerator, washer, dryer, and patio furniture as shown in listing photos"

- Request items during inspection negotiations if not included initially

- Prioritize built-in or hard-to-remove items (sellers more likely to leave these)

For sellers:

- Decide before listing what stays and what goes—note exclusions in listing remarks

- Photograph your home without items you plan to take to avoid confusion

- Use high-end appliances and fixtures as marketing points in your listing description

- Price items you're willing to include separately so you can negotiate strategically

Decision rule: Include appliances and fixtures when they're not worth the hassle of moving but add perceived value to buyers. Exclude items with sentimental value or those you can sell separately for good money. In competitive spring markets, being generous with inclusions can eliminate buyer objections and speed the sale.

How Does Flexible Closing Timing Create Negotiation Leverage?

Flexible closing timing ranks #6 because it costs sellers nothing but can be worth thousands to buyers facing timing constraints—and vice versa.

Timing scenarios that create value:

Extended closing periods (45-60 days):

- Benefits buyers who need time to sell current home

- Allows buyers to secure better financing rates if they're waiting for rate improvements

- Gives buyers time to save additional down payment funds

- Helps buyers coordinate school schedules or job relocations

Accelerated closings (14-21 days):

- Appeals to cash buyers and investors who want quick possession

- Benefits sellers who've already purchased next home and face double payments

- Reduces seller carrying costs (mortgage, utilities, insurance)

- Minimizes market risk if conditions are deteriorating

Rent-back agreements:

- Seller stays in home 30-60 days after closing while buyer owns it

- Allows sellers to close quickly but move on their schedule

- Generates rental income for buyer during rent-back period

- Eliminates seller need for temporary housing

Early occupancy (rare but valuable):

- Buyer moves in before closing (requires special insurance and agreements)

- Benefits buyers with urgent housing needs

- Allows buyers to start renovations before closing

- Risky for sellers—only consider with substantial non-refundable deposits

Strategic spring 2026 applications:

Spring's compressed 33-day average sale timeline[3] means timing flexibility becomes a differentiator. When multiple offers come in at similar prices, the one with the seller's preferred timeline often wins.

For buyers in competitive spring markets:

- Ask the listing agent about seller's ideal closing date before submitting offers

- Offer seller's preferred timeline even if it's not your first choice

- Include rent-back option in your offer if seller hasn't purchased next home

- Be specific: "Flexible closing date between April 15 and May 30 at seller's preference"

For sellers:

- Disclose your ideal timeline to your agent so they can identify matching buyers

- Consider offers with perfect timing even if price is slightly lower

- Calculate the cost of your preferred timeline (e.g., 60-day closing saves you $3,000 in carrying costs = equivalent to $3,000 higher offer)

- Build timing preferences into your listing strategy

Real-world value calculation:

A seller with a $2,500 monthly mortgage payment who needs 60 days to close on their next home saves $5,000 in carrying costs with an extended closing. An offer at $395,000 with 60-day closing may net more than $398,000 with standard 30-day closing after accounting for the extra month of payments.

Common mistake: Buyers assuming all sellers want the fastest possible closing. Many sellers need time to find and close on their next home, making longer closings more attractive. Always ask about timing preferences before submitting offers.

What Pre-Listing Repairs Should Sellers Complete to Minimize Concession Requests?

Strategic pre-listing repairs rank #7 because they reduce negotiation friction and often return more value than their cost by preventing price reductions and concession requests.

High-ROI pre-listing repairs for spring 2026:

Inspection red flags:

- HVAC servicing and certification ($150-300): Prevents $2,000-5,000 concession requests

- Roof repairs for visible damage ($500-2,000): Avoids $5,000-10,000 credit demands

- Electrical panel upgrades if outdated ($1,500-3,000): Eliminates safety concerns that kill deals

- Plumbing leaks and water damage ($300-1,500): Prevents mold concerns and buyer walkouts

Cosmetic updates with disproportionate impact:

- Fresh neutral paint throughout ($2,000-4,000): Makes home show better, reduces "needs work" perception

- Updated light fixtures ($300-800): Modernizes appearance inexpensively

- New cabinet hardware ($100-300): Refreshes kitchen and bathrooms cheaply

- Professional deep cleaning ($300-500): Eliminates odors and grime that trigger lowball offers

Safety and code issues:

- GFCI outlet installation in kitchens/bathrooms ($200-400)

- Smoke and CO detector updates ($100-200)

- Handrail installation where required by code ($300-800)

- Grading issues causing water pooling ($500-2,000)

What NOT to repair before listing:

- Major renovations that won't return full value in your market

- Cosmetic updates based on your personal taste rather than buyer preferences

- Systems that work fine but are older (let buyers request credits if concerned)

- Minor cosmetic imperfections that don't affect functionality

Strategic approach:

- Get pre-listing inspection ($400-600): Identifies issues before buyers find them

- Prioritize safety and function over cosmetics

- Fix items that photograph poorly or create negative first impressions

- Disclose everything even after repairs to maintain trust

- Keep receipts to show buyers you've maintained the home

Spring timing considerations:

Complete repairs 2-3 weeks before listing to allow time for contractor scheduling during busy spring season. Don't let repair delays push your listing into late spring when you'll face maximum competition.

Cost-benefit analysis:

Spending $3,000 on pre-listing repairs typically prevents $5,000-8,000 in concession requests and price reductions. The ROI comes from buyers feeling confident the home is well-maintained rather than looking for problems to negotiate.

For a comprehensive preparation strategy, see our 60-day home selling plan.

How Do Buyers Leverage Multiple Offers to Negotiate Better Concessions?

Understanding multiple-offer dynamics ranks #8 because it determines whether buyers can negotiate concessions at all during competitive spring months when 35% of buyers pay above list price[3].

The spring 2026 multiple-offer reality:

During peak season (May-June), properties in desirable areas often receive 3-7 offers within days of listing. In these situations, traditional concession requests often fail unless structured strategically.

Tactics that work in multiple-offer scenarios:

Escalation clauses with concession caps:

- "Buyer will pay $5,000 above highest competing offer up to $425,000, with seller providing $8,000 closing cost credit at any accepted price"

- Keeps concession request in play even as price escalates

- Shows commitment while maintaining affordability through concessions

Appraisal gap coverage with concession trade:

- "Buyer will cover up to $10,000 appraisal gap if seller provides $10,000 closing cost credit"

- Reduces seller's appraisal risk while buyer gets concession

- Net effect: Buyer pays more if appraisal comes in low, but gets concession if it appraises

Waiving minor contingencies for major concessions:

- Waive home sale contingency but request rate buydown

- Shorten inspection period to 5 days but request repair credit threshold

- Accept property as-is for cosmetic issues but request credit for major systems

Clean offer with single strategic concession:

- Instead of requesting multiple concessions, focus on the one that matters most

- "Full price offer with seller paying 3% closing costs, no other requests"

- Simpler offers are easier for sellers to evaluate and accept

When concessions are impossible in multiple offers:

If you're competing against 5+ offers in peak spring, concession requests may automatically disqualify your offer. In these situations:

- Focus on price and terms rather than concessions

- Save concession negotiations for inspection period

- Choose properties with fewer competing offers

- Shop during early spring (March-April) when competition is 30% lower[3]

For sellers receiving multiple offers:

- Evaluate net proceeds after concessions, not just offer price

- Consider reliability of buyer (financing strength, down payment size)

- Factor in timing and contingencies alongside price and concessions

- Counter the best offer if it includes excessive concession requests

Decision rule: Request concessions in your initial offer only if you're offering full price or above, have strong financing, and minimal contingencies. Otherwise, submit a clean competitive offer and negotiate concessions during inspection if you win the property.

What Role Do Seller-Paid HOA Fees and Prepaid Items Play?

Seller-paid HOA fees and prepaid items rank #9 because they're often overlooked concessions that reduce buyer cash requirements without affecting the purchase price.

Common prepaid items sellers can cover:

HOA-related costs:

- HOA transfer fees ($200-500)

- First year HOA dues ($1,200-6,000 depending on community)

- Special assessment contributions (varies widely)

- Move-in fees for condos ($200-400)

Property-related prepaid items:

- Property taxes (pro-rated to closing)

- Homeowners insurance first year premium ($1,000-2,500)

- Flood insurance if required ($400-2,000)

- Prepaid interest (varies by closing date)

Utility and service transfers:

- Home warranty (covered earlier)

- Pest control contracts

- Lawn care service prepayment

- Pool maintenance contracts

Strategic value:

These items don't show up in the purchase price but directly reduce the cash buyers need at closing. For buyers stretching to afford down payments, covering $3,000-5,000 in prepaid items can make the difference between qualifying and not qualifying.

Negotiation approach for buyers:

- Identify all prepaid items required by your lender in the Loan Estimate

- Request seller coverage of specific items: "Seller to pay first year HOA dues ($2,400) and HOA transfer fee ($350)"

- Focus on items that benefit seller too (e.g., prepaying property taxes they owe anyway)

- Bundle these requests with other concessions for total package

For sellers:

- Understand which prepaid items you're responsible for regardless (pro-rated taxes, etc.)

- Offer to prepay items that make your property more attractive without reducing price

- Calculate total concession package including prepaid items to understand true cost

- Advertise "Seller will pay HOA fees for first year" in listings for HOA properties

When this tactic works best:

- Condo and townhome sales where HOA fees are substantial

- First-time buyers who need every dollar of cash reserves

- Properties with high property taxes or insurance costs

- Situations where buyer is slightly short on cash to close

Common mistake: Buyers forgetting to request these items and then scrambling to find extra cash at closing. Review your Loan Estimate carefully and negotiate prepaid items during the offer stage, not three days before closing.

How Should Agents Structure Concession Requests to Maximize Acceptance?

Professional representation and strategic structuring rank #10 because how you ask for concessions matters as much as what you request.

Effective concession request framework:

1. Establish credibility first:

- Prove buyer financial strength with full underwriting approval (not just prequalification)

- Show substantial earnest money deposit ($5,000-10,000 minimum)

- Demonstrate seriousness through quick response times and clear communication

2. Justify each concession request:

- "Buyer requests $6,000 closing cost credit based on attached lender estimate showing $8,200 in closing costs"

- "Buyer requests $4,500 repair credit based on attached contractor estimate for HVAC repairs identified in inspection"

- Never request round numbers without documentation

3. Package concessions strategically:

- Bundle related items: "Buyer requests $8,000 total: $5,000 closing costs + $3,000 appliance credit"

- Separate major from minor: "Primary request: $10,000 closing costs. Secondary: include refrigerator and washer/dryer"

- Prioritize and be willing to negotiate: "Buyer's priority is closing cost assistance; willing to be flexible on other items"

4. Use professional language:

Instead of: "Buyer wants seller to pay for everything because the house needs work"

Say: "Buyer respectfully requests seller contribution of $7,500 toward closing costs to offset the buyer's cash requirements, allowing this transaction to close successfully while maintaining the agreed purchase price of $415,000"

5. Timing matters:

- With initial offer: Include concessions if offering full price or above

- After inspection: Request repair credits based on inspection findings

- During appraisal gap: Negotiate concessions if property appraises low

- Before closing: Request prepaid item coverage if buyer's cash position changes

Agent-specific tactics:

For buyer's agents:

- Research comparable sales to see what concessions are typical in the area

- Build rapport with listing agent before submitting offers

- Present buyer's qualifications before discussing concessions

- Offer solutions, not just problems: "Buyer requests $5,000 credit rather than requiring seller to complete repairs"

For listing agents:

- Set seller expectations about typical concession requests before listing

- Develop standard responses to common requests

- Calculate net proceeds for sellers with various concession scenarios

- Advise sellers when accepting concessions makes more sense than price reductions

What makes concession requests fail:

- Excessive requests without justification ($20,000 in concessions on $300,000 purchase)

- Poor buyer qualifications (weak financing, low down payment, then requesting concessions)

- Aggressive or entitled tone in request language

- Timing requests poorly (asking for major concessions during multiple-offer situations)

- Failing to provide documentation for repair or cost estimates

What makes concession requests succeed:

- Strong buyer qualifications and quick closing capability

- Reasonable requests backed by documentation

- Professional presentation and respectful language

- Flexibility and willingness to negotiate

- Strategic timing based on market conditions

Decision rule: Structure concession requests as solutions that help both parties achieve their goals. Frame closing cost credits as "maintaining the sale price while helping buyer with cash requirements." Frame repair credits as "allowing faster closing without contractor delays." Always position requests as win-win scenarios.

For agents looking to improve their overall negotiation skills, explore our master negotiation strategies guide.

What Market Indicators Signal When to Push for Maximum Concessions?

Understanding market timing and indicators helps buyers and sellers know when to push hard for concessions versus when to compromise.

Buyer-favorable indicators (push for maximum concessions):

Inventory metrics:

- Months of supply above 6 months (balanced to buyer's market)

- Increasing active listings week-over-week

- High percentage of price reductions (57% in January 2026)[1]

- Growing days on market averages

Seller behavior signals:

- Multiple price reductions on the same listing

- Property relisted after expired listing

- Vacant or already-purchased-next-home sellers

- Seasonal pressure (listing in late fall/winter when demand drops)

Financing environment:

- Rising interest rates making buyers more payment-sensitive

- Tightening lending standards reducing buyer pool

- Economic uncertainty causing buyer hesitation

Property-specific factors:

- Days on market exceeding neighborhood average by 50%+

- Unique property requiring specific buyer type

- Deferred maintenance visible in photos

- Location issues (busy road, near commercial, etc.)

Seller-favorable indicators (minimize concession requests):

Inventory metrics:

- Months of supply below 4 months (seller's market)

- Decreasing active listings

- Low percentage of price reductions

- Homes selling in under 30 days on average

Buyer behavior signals:

- Multiple offers common in the neighborhood

- Properties selling at or above list price (35% in May-June 2026)[3]

- Bidding wars on similar properties

- High showing activity in first few days

Seasonal factors:

- Peak spring selling season (March-May)

- School calendar timing creating urgency

- Tax refund season (February-April) when buyers have down payment cash

- Low inventory combined with high demand

Property-specific advantages:

- Highly desirable location or school district

- Move-in ready condition

- Unique features not available in competing properties

- Priced competitively relative to recent sales

Strategic application for spring 2026:

The spring market creates a split scenario. Early spring (March-April) shows continued seller flexibility with high concession rates[1], making it ideal for buyers to request maximum concessions. Late spring (May-June) shifts toward seller advantage as competition intensifies[3], requiring buyers to minimize concession requests or risk losing properties.

Tactical timing:

- March 2026: Aggressive concession requests likely to succeed; sellers still flexible from winter market

- April 2026: Moderate concession requests; market transitioning to more competitive

- May-June 2026: Minimal concession requests; focus on winning the property first, negotiate during inspection

- July-August 2026: Return to moderate concessions as summer slowdown begins

How to read your specific market:

- Track active listings in your target area weekly

- Monitor sold-to-list price ratios (below 98% = buyer leverage; above 100% = seller leverage)

- Calculate average days on market for your price range and property type

- Review percentage of listings with price reductions

- Talk to local agents about multiple-offer frequency

Decision rule: Push for maximum concessions when inventory is rising, days on market are increasing, and price reductions are common. Minimize concession requests when facing multiple offers, low inventory, and properties selling quickly. The data tells you which market you're in—let it guide your strategy.

Frequently Asked Questions

What percentage of sellers are offering concessions in spring 2026?

67% of homes sold in early 2026 included seller-paid concessions, with average contributions of $18,028 per transaction[1]. This represents a significant increase from previous years and indicates sellers are substantially more willing to negotiate concessions than during the pandemic-era seller's market.

Are seller concessions better than price reductions?

Seller concessions often benefit both parties more than price reductions. Concessions maintain higher comparable sales values in the neighborhood, help buyers with cash requirements without affecting loan-to-value ratios, and can cost sellers less than equivalent price cuts when factoring in appraisal impacts. However, large concessions (over 6% of purchase price) may raise red flags for lenders and appraisers.

Can sellers offer concessions on FHA and VA loans?

Yes, but limits apply. FHA loans allow seller concessions up to 6% of the purchase price. VA loans allow up to 4% for closing costs plus unlimited concessions for discount points, prepaid items, and repairs. Conventional loans typically allow 3-9% depending on down payment size and loan type. Always verify limits with your lender before negotiating.

When should buyers request concessions—with the initial offer or after inspection?

The timing depends on market conditions. In competitive spring markets with multiple offers, include modest concessions (2-3% closing costs) with your initial offer only if you're offering full price or above. In slower markets or when you're the only offer, submit a clean initial offer and request concessions after inspection based on findings. This prevents your offer from being rejected due to excessive initial requests.

What's the difference between a seller credit and a seller concession?

The terms are often used interchangeably, but technically a seller credit is a specific dollar amount applied at closing ($5,000 credit), while seller concessions can include both credits and non-monetary items (including appliances, paying for warranties, etc.). Both reduce the buyer's cash requirements or out-of-pocket expenses.

How do seller concessions affect the appraisal?

Seller concessions don't directly affect the property's appraised value, but excessive concessions (over 6% of purchase price) may signal to the appraiser that the purchase price is inflated. Appraisers will note the concession amount in their report, and if concessions are significantly higher than typical for the area, it may trigger additional scrutiny of the sale price.

Can sellers offer concessions on cash purchases?

Yes, though it's less common. Cash buyers don't need closing cost assistance for lender fees, but sellers can still offer credits for repairs, include appliances, provide home warranties, or reduce the purchase price directly. Cash buyers often have more leverage to negotiate price reductions instead of concessions since they don't face lender restrictions.

What concessions work best for investment property purchases?

Investors typically prefer repair credits over completed repairs (so they can control contractor selection and costs), closing cost coverage to preserve cash for renovations, and flexible closing timelines to coordinate financing. Investors rarely value home warranties or appliance inclusions unless the property will be rented furnished. Price reductions often work better than concessions for investor purchases.

Are there tax implications for seller concessions?

Seller concessions reduce the seller's net proceeds but don't change the reported sale price for tax purposes. Buyers cannot deduct seller-paid closing costs from their taxes, though some closing costs (points, property taxes) may be deductible regardless of who pays them. Consult a tax professional for specific situations, as rules vary based on property type and use.

How do you negotiate concessions when buying new construction?

New construction builders rarely reduce base prices but often offer concessions through upgrades, closing cost credits, rate buydowns, or design center allowances. The best time to negotiate is during slow sales periods or at the end of the builder's fiscal quarter/year when they need to close deals. Focus requests on items the builder can provide at cost (upgrades, options) rather than cash concessions.

What happens if the seller agrees to concessions but the appraisal comes in low?

If the appraisal is below the purchase price, the lender will only allow concessions based on the appraised value, not the contract price. For example, if you negotiated a 3% concession on a $400,000 purchase ($12,000) but the property appraises at $390,000, the maximum concession becomes $11,700 (3% of $390,000). Buyers and sellers must then renegotiate the price, concessions, or buyer's down payment to close the gap.

Should sellers advertise concessions in their listing?

Yes, advertising willingness to offer concessions attracts more buyers and generates additional showings. Phrases like "Seller will contribute to closing costs," "Rate buydown available," or "Seller offering $10,000 in concessions" in listing descriptions and remarks increase buyer interest, particularly among first-time buyers and those with limited cash reserves. This strategy works impeccably in balanced or buyer's markets but may be unnecessary in competitive seller's markets.

Conclusion

The ranked 10 spring negotiation tactics for seller concessions in 2026 reflect a fundamentally transformed real estate market where flexibility and strategic thinking replace the rigid, seller-dominated dynamics of recent years. With 67% of transactions including concessions averaging $18,028 and price reductions affecting 57% of listings[1], both buyers and sellers have extraordinary opportunities to structure deals that meet their specific needs.

The key insight: Spring 2026 offers a split market. Early spring (March-April) favors buyers with continued seller flexibility and lower competition, making it the ideal time to request maximum concessions. Late spring (May-June) shifts toward seller advantage as competition intensifies and 35% of buyers pay above asking price[3], requiring buyers to focus on winning properties first and negotiating strategically during inspections.

Actionable next steps for buyers:

- Get fully underwritten approval (not just prequalification) before making offers to strengthen your negotiation position

- Target early spring (March-April) for maximum concession leverage before competition peaks

- Prioritize closing cost concessions and rate buydowns as your primary requests—these provide the most value

- Document all concession requests with contractor estimates, lender fee worksheets, and comparable sales data

- Work with experienced agents who understand how to structure and present concession requests professionally

- Monitor market indicators weekly to know when you have leverage versus when you need to compete aggressively

Actionable next steps for sellers:

- Complete strategic pre-listing repairs to minimize concession requests and inspection issues

- Set concession budgets before listing (typically 2-3% of sale price) so you can respond quickly to offers

- Advertise concession willingness in your listing to attract more buyers and generate additional showings

- Calculate net proceeds for various scenarios (price reductions vs. concessions) to make informed decisions

- Be flexible on timing as a zero-cost concession that can win you better offers

- Consider rate buydowns as a powerful differentiator in competitive spring markets

For real estate agents:

Master these negotiation tactics to provide impeccable service to your clients. The agents who understand how to structure concession requests professionally, justify them with data, and present them strategically will close more deals and earn more referrals in 2026. This market rewards expertise and preparation.

The spring 2026 market is so based for strategic negotiators. Whether you're buying your first home, selling to upgrade, or investing in rental properties, understanding these concession tactics gives you the edge to save thousands and close deals successfully. Don't gatekeep this knowledge—share it with your network and let it cook in your next negotiation.

For more expert guidance on real estate negotiations, market trends, and investment strategies, explore the comprehensive resources at Real Estate Rank IQ or subscribe to our YouTube channel @Realestaterankiq for weekly insights from licensed brokers with over 15 years of experience.

References

[1] Sellers Reduce Prices Offer Concessions To Sell Homes – https://donfenley.com/2026/02/09/sellers-reduce-prices-offer-concessions-to-sell-homes/

[2] Is 2026 The Real Estate Sweet Spot Why Acting Now Could Pay Off – https://communityimpact.com/sponsored/sponsored/2026/01/23/is-2026-the-real-estate-sweet-spot-why-acting-now-could-pay-off/

[3] Planning Your 2026 Real Estate Moves A Guide To The Best Buying And Selling Seasons – https://www.beneige.com/post/planning-your-2026-real-estate-moves-a-guide-to-the-best-buying-and-selling-seasons

[4] 2026 Real Estate Outlook What Leading Housing Economists Are Watching – https://www.nar.realtor/magazine/real-estate-news/2026-real-estate-outlook-what-leading-housing-economists-are-watching

[6] Re Market Pulse Week Of February 23 2026 – https://blog.coldwellbanker.com/re-market-pulse-week-of-february-23-2026/

{“@context”:”https://schema.org”,”@type”:”Article”,”headline”:”Ranked: 10 spring negotiation tactics for seller concessions in 2026″,”description”:” Master the top 10 spring negotiation tactics for seller concessions in 2026. Expert strategies for buyers and sellers to save thousands in today’s balanced mar”,”image”:”https://zsxkvszxbhpwnvzxdydv.supabase.co/storage/v1/object/public/generated-images/kie/8457cf8c-5121-4418-9f27-805dd3592fb2/slot-0-1771913348007.png”,”datePublished”:”2026-02-24T06:03:31.152998+00:00″,”dateModified”:”2026-02-24T06:09:55.268Z”,”author”:{“@type”:”Organization”,”name”:”real estate rank iq”},”publisher”:{“@type”:”Organization”,”name”:”real estate rank iq”}}

{kind=link}