Last updated: April 2, 2026

Quick Answer: Learning how to invest in real estate does not require a trust fund, a real estate license, or decades of experience. Beginners in 2026 can enter the market with as little as $10 through REITs or crowdfunding platforms, or with $3,000–$20,000 for more hands-on strategies like house hacking or rental properties. The key is matching the right strategy to your current financial position, risk tolerance, and time availability — then executing with a clear plan.

Key Takeaways

- REITs and crowdfunding platforms are the lowest-barrier entry points — some require as little as $10 to start.

- House hacking (living in one unit of a multi-family property while renting others) is widely considered the best first move for beginners with limited capital.

- Credit score matters — most conventional investment property loans require a minimum 620–680 score, but 720+ gets you the best rates.

- The 21st Century ROAD to Housing Act, passed by the Senate in March 2026, includes a temporary ban on large institutional investors buying single-family homes — a direct opening for individual beginners. [3]

- New FinCEN rules (effective March 2026) require reporting on all-cash purchases by LLCs and trusts — beginners using entities need to understand this compliance layer. [5]

- CBRE projects U.S. commercial real estate investment to rise 16% to $562 billion in 2026, signaling a recovering market with real entry opportunities. [4]

- The BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) is one of the most effective strategies for scaling without large amounts of upfront capital.

- Technology and apps have made real estate investing more accessible than at any point in history — platforms like Fundrise, Arrived, and Roofstock are built for beginners.

- Passive income through real estate is achievable, but it requires active financial preparation first — credit building, savings, and education are non-negotiable steps.

- Starting small and learning the mechanics of one strategy before expanding is the single most common advice from experienced investors.

Why Real Estate Is Still One of the Best Investments in Any Market

Real estate has produced consistent wealth for ordinary people across every economic cycle for over a century. Even in volatile markets, it holds three advantages that stocks and bonds simply cannot match: physical asset value, rental income, and tax benefits.

Here’s what makes real estate investing for beginners particularly attractive right now in 2026:

- Institutional investors are being pushed out. The U.S. Senate passed the 21st Century ROAD to Housing Act (89-10 vote) in March 2026, which includes a temporary ban on large institutional investors purchasing single-family homes. That means less competition for individual buyers at the entry level. [3]

- Supply constraints are easing. A White House executive order signed March 13, 2026 targets the removal of regulatory barriers to affordable home construction — streamlining permitting, capping fees, and reducing restrictive building codes. More supply entering the market creates more acquisition opportunities for new investors. [2] [8]

- Rent growth is returning. A March 2026 multifamily market update confirmed that supply pressures are easing in several markets, with rent growth returning and distressed sellers creating buy opportunities — particularly in the multifamily space. [1]

- CBRE forecasts a 16% rise in U.S. commercial real estate investment to $562 billion in 2026, driven by income returns and cap rate compression of 5–15 basis points. For beginners, this signals that the smart money is moving back in. [4]

- Morgan Stanley (March 2026) shifted focus from macro risks to micro opportunities, prioritizing cash-flow growth in multifamily, senior living, and industrial — sectors with muted supply and assets repriced 20–25% from peak values.

Real estate also benefits from leverage in a way that almost no other asset class allows. Putting 20% down on a $300,000 property means you control a $300,000 asset with $60,000. If that property appreciates 5%, you’ve gained $15,000 on a $60,000 investment — a 25% return on your actual capital deployed.

For a deeper look at how market conditions are shaping investment decisions right now, the 2026 Real Estate Trends guide on stable 6% rates breaks down exactly what buyers and investors are navigating this year.

How to Invest in Real Estate: The 7 Main Ways (Ranked for Beginners)

The biggest mistake beginners make is treating “real estate investing” as one single thing. There are at least seven distinct strategies, each with different capital requirements, risk profiles, and time commitments. Here’s an honest breakdown of each.

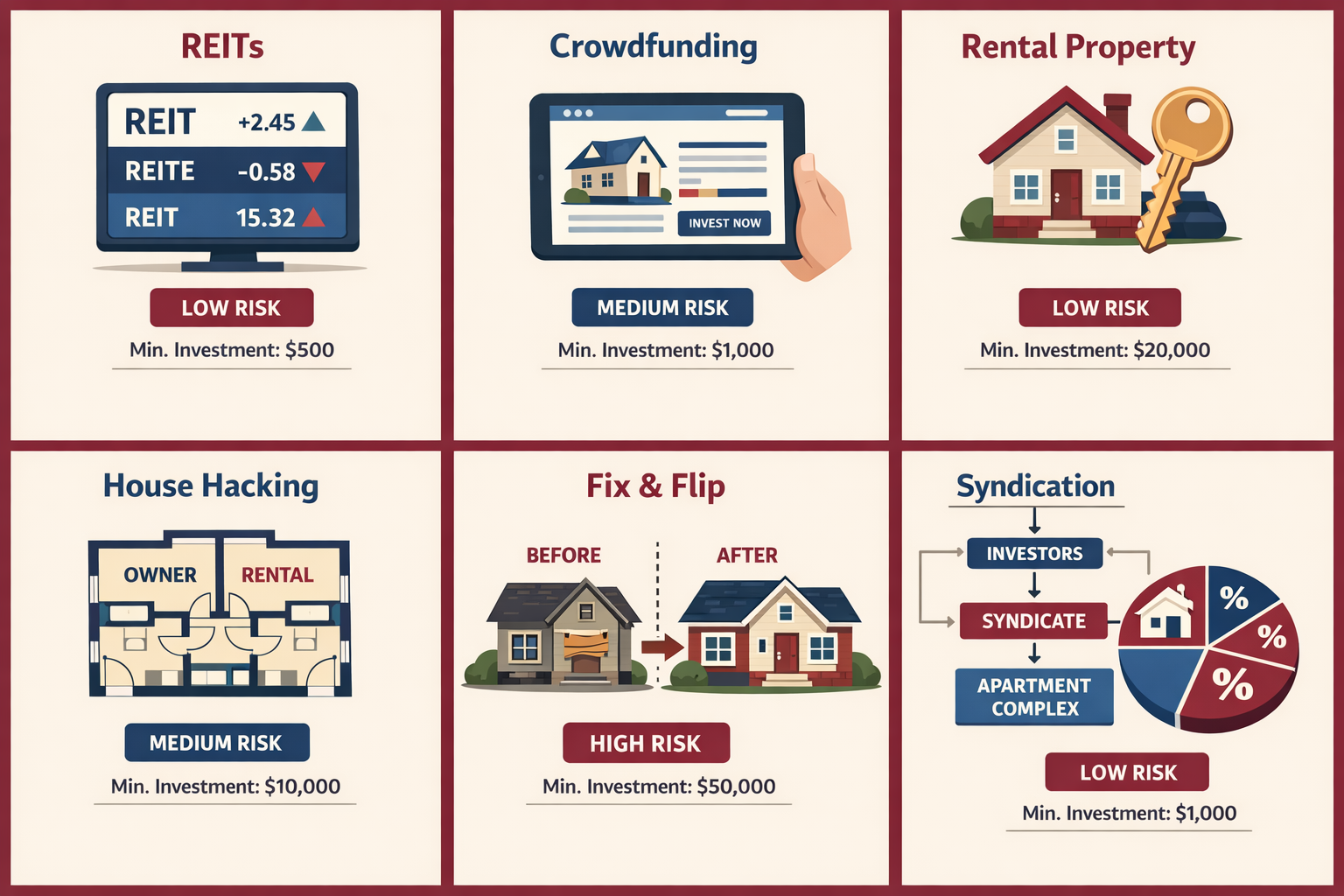

REITs (Real Estate Investment Trusts)

Best for: Complete beginners, passive income seekers, investors with under $1,000 to start.

A REIT is a company that owns income-producing real estate — think apartment complexes, shopping centers, office buildings, and warehouses. By law, REITs must distribute at least 90% of their taxable income to shareholders as dividends. That makes REITs for beginners one of the most straightforward paths to passive income real estate.

How it works: Buy shares of a REIT through any brokerage account (Fidelity, Schwab, Robinhood) the same way you’d buy a stock. Public REITs trade on major exchanges.

| Factor | Details |

|---|---|

| Minimum investment | $1–$50 per share (some fractional shares available) |

| Risk level | Low to Medium |

| Time commitment | Minimal — fully passive |

| Expected return | ~4–10% dividend yield + share appreciation |

| Liquidity | High — sell shares any trading day |

Pros: No property management, instant diversification, highly liquid.

Cons: No direct control, subject to stock market volatility, no leverage benefit.

Popular REIT sectors to research: Residential (AvalonBay, Equity Residential), Industrial (Prologis), Healthcare (Welltower), and Retail (Realty Income).

Real Estate Crowdfunding Platforms

Best for: Beginners who want real estate exposure without buying property, investors with $10–$5,000 to start.

Real estate crowdfunding pools money from many investors to fund specific deals — residential developments, commercial properties, or debt positions. Platforms like Fundrise and Arrived have made this accessible to non-accredited investors (meaning you don’t need to be wealthy to participate).

Is Fundrise a good investment? For beginners, yes — with realistic expectations. Fundrise offers eREITs and eFunds with historical net returns ranging from 5–12% annually depending on the portfolio and market conditions. It’s not a get-rich-quick vehicle, but it’s a legitimate, low-friction way to get real estate exposure with as little as $10.

Arrived focuses specifically on single-family rental properties and vacation rentals. Investors buy fractional shares of individual properties and receive rental income proportional to their ownership stake. Arrived reviews from users consistently highlight the transparency of property-level data and the simplicity of the platform.

For a full breakdown of the best crowdfunding options available, the best crowdfunding sites for investors guide covers the top platforms with side-by-side comparisons.

| Factor | Details |

|---|---|

| Minimum investment | $10 (Fundrise) to $100 (Arrived) |

| Risk level | Low to Medium |

| Time commitment | Minimal — platform manages everything |

| Expected return | 5–12% annually (varies by platform/deal) |

| Liquidity | Low to Medium — redemption windows vary |

Pros: Low minimums, diversified exposure, no landlord responsibilities.

Cons: Illiquid compared to stocks, platform risk, limited control over individual deals.

Rental Properties

Best for: Investors ready to be landlords, those with $20,000–$60,000 for a down payment, long-term wealth builders.

Buying a rental property — a single-family home, duplex, or small apartment building — is the most traditional form of real estate investing. You purchase a property, rent it out, collect monthly income, and build equity over time.

The numbers that matter:

- Down payment: 15–25% for investment properties (conventional loans)

- Minimum credit score: 620 for most lenders, 720+ for best rates

- Cash-on-cash return target: 8–12% is considered solid in most markets

- The 1% rule: Monthly rent should equal at least 1% of the purchase price (e.g., a $150,000 property should rent for $1,500/month) — this is a quick screening tool, not a guarantee

Key 2026 consideration: California introduced stricter property management regulations in early 2026, including new statewide rental rules in the Bay Area. If you’re investing in regulated markets, factor compliance costs into your cash flow projections.

For a detailed breakdown of how to price rental income correctly, the comprehensive landlord pricing guide is worth bookmarking.

| Factor | Details |

|---|---|

| Minimum investment | $20,000–$60,000 (down payment + reserves) |

| Risk level | Medium |

| Time commitment | Medium to High (active management or hire PM) |

| Expected return | 6–14% cash-on-cash + appreciation |

| Liquidity | Low — real estate takes time to sell |

House Hacking

Best for: First-time investors who want to live for free (or nearly free) while building equity.

House hacking is arguably the most beginner-friendly real estate investment strategy that exists. The concept is simple: buy a multi-unit property (duplex, triplex, or fourplex), live in one unit, and rent out the others. The rental income from your tenants covers your mortgage — sometimes entirely.

Why it works so well for beginners:

- You can use an FHA loan with as little as 3.5% down (because it’s your primary residence)

- You qualify for owner-occupant mortgage rates, which are lower than investment property rates

- You learn property management hands-on while your risk is limited

- In many markets, a duplex or triplex can be purchased for $250,000–$450,000, with rental income covering 60–100% of the mortgage

Example: Purchase a $320,000 duplex with 3.5% FHA down ($11,200). Live in Unit A, rent Unit B for $1,400/month. Your mortgage (PITI) is approximately $1,900/month. Your actual housing cost: $500/month instead of $1,900. Meanwhile, you’re building equity and gaining landlord experience.

This strategy is so effective that many experienced investors credit house hacking as the move that started their entire portfolio.

Fix and Flip

Best for: Investors with construction knowledge, higher risk tolerance, and access to short-term capital.

Fix and flip means buying a distressed property below market value, renovating it, and selling it for a profit — ideally within 3–12 months. It’s the strategy most people picture when they think of real estate investing, thanks to HGTV. The reality is more demanding.

The honest breakdown:

- Profit margins depend heavily on accurate ARV (After Repair Value) estimates and renovation cost control

- Carrying costs (loan interest, taxes, insurance, utilities) eat into profit every month the property sits

- Hard money loans are the most common financing tool — expect 10–15% interest rates and 1–3 points

- Beginners should target a minimum $30,000–$50,000 profit margin to account for surprises

Risk level: High. Renovation overruns, market shifts, and inaccurate ARV estimates have wiped out first-time flippers. Start with a mentor or partner who has completed flips before going solo.

| Factor | Details |

|---|---|

| Minimum investment | $30,000–$100,000+ (down payment + renovation budget) |

| Risk level | High |

| Time commitment | High — active project management required |

| Expected return | $20,000–$80,000 per deal (highly variable) |

| Liquidity | Medium — exit at sale |

Real Estate Syndications

Best for: Accredited investors (net worth $1M+ or income $200K+) who want passive exposure to large commercial deals.

A real estate syndication pools capital from multiple investors to purchase a large asset — an apartment complex, commercial building, or industrial park — that no single investor could buy alone. A “syndicator” or “sponsor” manages the deal; passive investors (LPs) provide capital and receive returns.

Typical structure:

- Minimum investment: $25,000–$100,000

- Preferred return: 6–8% annually

- Total projected return: 15–20% IRR over 5–7 years

- Accredited investor status required for most deals

Syndications are not for true beginners with limited capital, but they’re worth understanding as a future strategy. If you’re building toward this, focus on growing your net worth and accredited investor status first.

Fractional Real Estate Investing

Best for: Beginners who want direct property ownership exposure without buying a whole property.

Fractional real estate investing lets you buy a percentage stake in a specific property — a vacation rental, a single-family home, or a commercial asset — through platforms like Arrived, Lofty, or Groundfloor. You receive proportional rental income and appreciation.

This is different from REITs because you’re tied to a specific property, not a diversified fund. It’s also different from crowdfunding in that your ownership is more transparent and property-specific.

Key advantage: You can start learning how property-level financials work (NOI, cap rate, cash-on-cash return) with real money at stake, without the full commitment of owning a property outright.

For a complete breakdown of the 4 essential property types for investment, that guide covers residential, commercial, industrial, and mixed-use assets in detail.

How Much Money Do You Actually Need to Start?

The answer depends entirely on which strategy you choose. Here’s the no-fluff breakdown:

Minimum Capital by Strategy

| Strategy | Minimum to Start | Realistic Starting Budget |

|---|---|---|

| Public REITs | $1–$50 | $500–$2,000 |

| Fundrise / Crowdfunding | $10–$100 | $1,000–$5,000 |

| Fractional Investing (Arrived) | $100 | $500–$2,500 |

| House Hacking (FHA Loan) | $8,000–$15,000 | $15,000–$25,000 |

| Rental Property (Conventional) | $20,000–$60,000 | $40,000–$80,000 |

| Fix and Flip | $30,000–$50,000 | $60,000–$120,000 |

| Real Estate Syndication | $25,000–$100,000 | $50,000–$100,000 |

Beyond the Down Payment: Hidden Costs Beginners Miss

- Closing costs: 2–5% of the purchase price (on a $250,000 home, that’s $5,000–$12,500)

- Inspection and appraisal fees: $400–$800

- Reserves: Lenders typically want 2–6 months of mortgage payments in savings after closing

- Vacancy buffer: Budget for 1–2 months of vacancy per year on rental properties

- Maintenance reserve: Set aside 1% of property value annually for repairs

Pro tip: The top 7 down payment strategies guide covers creative ways to fund your first purchase — including gift funds, down payment assistance programs, and seller concessions.

Building Credit for Real Estate: The Non-Negotiable Step

Before you can qualify for a mortgage, your credit score needs to be in shape. Here’s the minimum credit score breakdown for real estate investing:

| Loan Type | Minimum Credit Score | Notes |

|---|---|---|

| FHA Loan (3.5% down) | 580 | 10% down required if 500–579 |

| Conventional Loan | 620 | Best rates at 740+ |

| Investment Property Loan | 680–700 | Stricter than primary residence |

| Hard Money Loan | 550–600 | Higher rates, asset-based |

| VA Loan (veterans) | 580–620 | No down payment required |

Credit-building tactics for investors aged 18–25:

- Open a secured credit card with a $200–$500 deposit and pay it off monthly

- Become an authorized user on a parent or family member’s card with a long, positive history

- Use a credit-builder loan through a credit union (typically $300–$1,000)

- Keep credit utilization below 10% — not 30%, which is the common advice; 10% or below is what moves scores fastest

- Never miss a payment — payment history is 35% of your FICO score

- Don’t close old accounts — length of credit history matters

- Monitor with free tools like Credit Karma or your bank’s built-in credit monitoring

A 720+ credit score can save you $50,000–$100,000 over the life of a 30-year mortgage compared to a 620 score. That’s not an exaggeration — it’s math.

For mortgage rate comparisons and how credit scores affect your long-term costs, the 15-year vs. 30-year mortgage guide for 2026 is a must-read before you apply.

Best Real Estate Investing Apps and Platforms for Beginners (Comparison Table)

The technology available to beginner investors in 2026 is extraordinary. These platforms have genuinely removed barriers that used to keep regular people out of real estate investing.

Passive/Hands-Off Platforms

| Platform | Min. Investment | Strategy | Returns (Est.) | Accredited Required? | Best For |

|---|---|---|---|---|---|

| Fundrise | $10 | eREITs, eFunds, private credit | 5–12% annually | No | True beginners, passive income |

| Arrived | $100 | Fractional single-family & vacation rentals | 3–8% rental yield + appreciation | No | Property-level exposure, beginners |

| Groundfloor | $10 | Short-term real estate debt (loans) | 8–14% annually | No | Higher yield, short-term focus |

| Streitwise | $5,000 | Commercial real estate REIT | 8–9% dividend | No | Consistent dividend income |

| CrowdStreet | $25,000 | Commercial real estate deals | 15–20% IRR (projected) | Yes | Accredited investors, larger deals |

Active/Direct Investment Tools

| Platform | Cost | Best Use | Key Feature |

|---|---|---|---|

| Roofstock | Free to browse, 0.5% fee | Buy/sell rental properties online | Tenant-occupied homes with income data |

| BiggerPockets | Free (Pro: $39/mo) | Education, deal analysis, networking | Rental property calculators, forums |

| PropStream | $99/month | Wholesaling, deal sourcing | Off-market property data, skip tracing |

| DealMachine | $49–$99/month | Driving for dollars, direct mail | Mobile app for finding distressed properties |

| Stessa | Free | Portfolio tracking, tax prep | Automated income/expense tracking |

The PropStream 2026 review gives an honest take on whether that tool is worth the monthly cost for beginners — so based on what most new investors actually need, it’s better suited for those already actively sourcing deals.

For a broader look at technology tools that are changing how investors analyze and manage properties, the top real estate AI tools for investors in 2026 guide covers the fresh wave of AI-powered platforms that are genuinely useful.

How to Invest in Real Estate: Choosing the Right Strategy for Your Situation

The right strategy isn’t the one with the highest projected return — it’s the one you can actually execute given your current resources, schedule, and risk tolerance.

Use this decision framework:

Choose REITs or Crowdfunding if:

- You have under $5,000 to invest

- You want fully passive income

- You’re still building your credit score

- You want to learn how real estate returns work before committing larger capital

Choose House Hacking if:

- You’re renting and paying someone else’s mortgage

- You have $10,000–$25,000 saved

- You’re comfortable being a hands-on landlord

- You want to minimize your living expenses while building equity

Choose a Rental Property if:

- You have $40,000–$80,000 in savings

- Your credit score is 680+

- You have a stable W-2 income (lenders love this)

- You want long-term cash flow and equity growth

Choose Fix and Flip if:

- You have construction knowledge or a trusted contractor

- You have access to hard money or private lenders

- You can absorb a loss if the deal goes sideways

- You want active income, not passive income

Choose Syndications if:

- You’re an accredited investor

- You want large-scale commercial exposure

- You prefer writing a check and letting a sponsor manage everything

A note on W-2 income: Most lenders require 2 years of consistent W-2 employment history to qualify for a conventional mortgage. If you’re self-employed or have irregular income, you’ll need 2 years of tax returns showing consistent earnings. This is one of the most overlooked mortgage qualification requirements for young investors.

The real estate investment financing guide covers alternative financing options — including portfolio loans, private money, and seller financing — for situations where conventional mortgages don’t fit.

Biggest Mistakes Beginners Make (And How to Avoid Them)

These aren’t theoretical warnings. These are the actual patterns that derail first-time investors repeatedly.

1. Buying in a market they don’t understand

Chasing high yields in unfamiliar cities without understanding local job growth, vacancy rates, and rental demand is a fast way to own a property that sits empty. Research your market before you commit. The neighborhood market data and investment strategies guide shows exactly how to use AI tools to analyze a local market before buying.

2. Underestimating expenses

New investors consistently underestimate property taxes, insurance, maintenance, vacancy, and property management costs. A property that looks like it cash flows $400/month often breaks even or loses money once all expenses are factored in. Always run a full expense analysis — not just mortgage vs. rent.

3. Overleveraging too fast

Scaling quickly feels exciting until one vacancy or major repair wipes out your reserves. Build a 3–6 month cash reserve before buying your first property, and don’t buy a second until the first is stable.

4. Ignoring legal structure

Many beginners buy investment properties in their personal name without considering liability exposure. An LLC provides asset protection — but as of March 2026, FinCEN’s new Residential Real Estate Reporting Rule requires reporting of buyer/seller information for all-cash purchases made by LLCs or trusts. This adds a compliance layer beginners need to understand before structuring deals. [5]

For a full breakdown of legal considerations, the real estate investment laws guide covers entity structures, liability, and regulatory compliance.

5. Skipping the inspection

An inspection is $400–$600. A missed foundation issue is $20,000–$80,000. This is not the place to cut corners.

6. Emotional buying

Falling in love with a property and ignoring the numbers is one of the most common and expensive mistakes in real estate. Every purchase decision should be driven by the math, not the aesthetics.

7. Not building a team early

The investors who scale fastest aren’t doing everything alone. A good real estate agent, lender, CPA, and property manager are worth their fees many times over. Start building relationships before you need them.

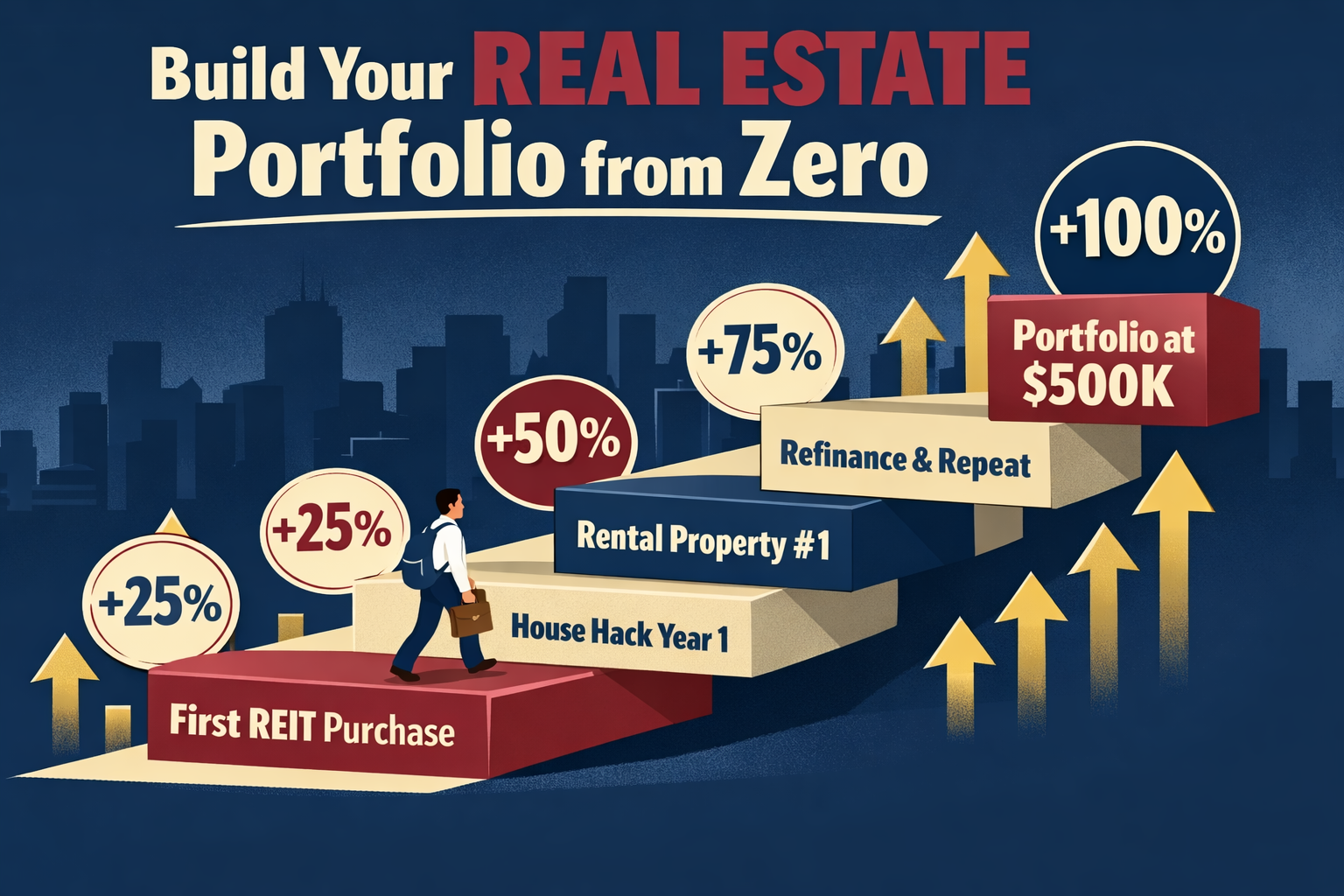

How to Build a Real Estate Portfolio from Zero

Building a portfolio is a process, not an event. Here’s a realistic timeline and framework for going from zero to a functioning real estate portfolio.

Phase 1: Financial Foundation (Months 1–12)

This phase is about preparation, not purchasing. Most beginners skip this and pay for it later.

- Build credit: Target a 720+ score using the tactics outlined earlier

- Save aggressively: Automate savings to a dedicated “real estate fund” — treat it like a bill

- Eliminate high-interest debt: Credit card debt at 20%+ APR destroys your ability to save and qualifies you for less mortgage

- Get pre-approved: Even if you’re not ready to buy, a pre-approval tells you exactly where you stand and what you need to improve

- Educate yourself: Read books (Rich Dad Poor Dad, The Book on Rental Property Investing), listen to podcasts (BiggerPockets), and follow credible sources like the RERIQ Investment Hub

- Start micro-investing: Put $500–$2,000 into Fundrise or a REIT ETF to start learning how real estate returns feel in real time

Phase 2: First Investment (Months 12–24)

- Execute your first strategy — ideally house hacking or a rental property if capital allows

- Learn property management — even if you hire a PM, understand what they’re doing

- Track everything — use Stessa or a spreadsheet to monitor income, expenses, and returns

- Build your team — agent, lender, CPA, contractor, property manager

Phase 3: The BRRRR Method (Years 2–5)

Once you have one property stabilized, the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) is the most effective strategy for scaling without continuously injecting large amounts of new capital:

- Buy a distressed property below market value

- Rehab it to increase value and attract quality tenants

- Rent it out to generate cash flow

- Refinance with a cash-out refinance based on the new appraised value

- Repeat — use the refinanced capital to fund the next deal

This strategy lets you recycle capital rather than saving fresh down payments for every new property. It’s not instant, and it requires strong execution at each step — but it’s the framework behind many investors who built portfolios of 5–20 properties within a decade.

Phase 4: Diversification and Scale (Years 5+)

- Add commercial real estate exposure through REITs or syndications

- Consider a 1031 exchange to defer capital gains when selling appreciated properties

- Explore short-term rentals (Airbnb/VRBO) for higher income potential in the right markets

- Look at the Airbnb vs. Vacasa property management comparison if short-term rentals are on your radar

The 16 pro tips to maximize real estate returns is a fresh resource worth reading as you move into active portfolio management.

Frequently Asked Questions

Q: What is the minimum credit score needed to invest in real estate?

A: For an FHA loan (primary residence/house hack), the minimum is 580 with 3.5% down. For conventional investment property loans, most lenders require 620–680 minimum, with 720+ needed for the best rates. Hard money lenders may approve at 550–600 but charge significantly higher rates.

Q: Can you invest in real estate with no money?

A: Technically yes — through wholesaling (assigning contracts without purchasing), partnering with a capital investor, or using seller financing. Practically, most strategies require at least some capital. Platforms like Fundrise start at $10, making zero-barrier entry possible for passive strategies.

Q: How do I invest in real estate with little money?

A: The best options for how to invest in real estate with little money are: (1) REITs through a brokerage account starting at $1–$50 per share, (2) Fundrise starting at $10, (3) Arrived starting at $100 for fractional property ownership, and (4) house hacking with an FHA loan requiring as little as 3.5% down on a multi-unit property.

Q: Is Fundrise a good investment for beginners?

A: Fundrise is a solid starting point for beginners who want real estate exposure without buying property. Historical returns have ranged from 5–12% annually. It’s illiquid compared to stocks — redemptions are limited — so treat it as a 3–5 year minimum hold. It’s not a replacement for direct property ownership, but it’s a legitimate first step.

Q: What is house hacking and why is it recommended for beginners?

A: House hacking means buying a multi-unit property (duplex, triplex, or fourplex), living in one unit, and renting the others. The rental income offsets or eliminates your mortgage payment. It qualifies for owner-occupant FHA financing (3.5% down), gives you hands-on landlord experience, and builds equity — all simultaneously. It’s widely considered the best first move for beginners with limited capital.

Q: How long does it take to qualify for a mortgage as a first-time investor?

A: With a 720+ credit score, 2 years of W-2 employment, and a 20% down payment saved, you can qualify for a conventional investment property loan relatively quickly. If you’re building credit from scratch, plan for 12–24 months of focused credit-building before applying.

Q: What is the BRRRR method?

A: BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. It’s a strategy where you buy a distressed property below market value, renovate it, rent it out, then refinance based on the new appraised value to pull out capital — which you use to fund the next deal. It’s one of the most effective ways to scale a rental portfolio without saving a new down payment for every property.

Q: Do I need an LLC to invest in real estate?

A: Not required, but often recommended for liability protection once you own investment properties. As of March 2026, FinCEN requires reporting of buyer/seller information for all-cash purchases made through LLCs or trusts. Consult a real estate attorney before structuring deals through an entity. [5]

Q: What is fractional real estate investing?

A: Fractional real estate investing lets you buy a percentage ownership stake in a specific property through platforms like Arrived or Lofty. You receive proportional rental income and appreciation without owning the full property. It’s different from REITs because you’re tied to a specific asset, not a diversified fund.

Q: Are REITs better than buying rental property?

A: REITs offer liquidity, diversification, and zero management responsibilities. Rental properties offer leverage, direct control, tax benefits (depreciation, mortgage interest deduction), and potentially higher returns. REITs are better for passive investors or those building capital. Rental properties are better for investors ready to be active and who want maximum wealth-building potential.

Q: What are the new 2026 regulations beginners need to know about?

A: Two key regulatory changes affect beginners in 2026: (1) FinCEN’s Residential Real Estate Reporting Rule (effective March 2026) requires reporting on all-cash purchases by LLCs or trusts — relevant if you’re using an entity. [5] (2) The White House executive order (March 13, 2026) removes regulatory barriers to affordable home construction, which should gradually increase housing supply and create more acquisition opportunities. [2] [8]

Q: How do I analyze a market before buying an investment property?

A: Focus on job growth, population trends, vacancy rates, rent-to-price ratios, and local supply pipeline. The AI-powered market analysis guide shows exactly how to use ChatGPT and Gemini to run a neighborhood-level analysis in minutes.

Conclusion: Your Next Move Starts Today

The biggest thing gatekeeping most beginners from real estate investing isn’t capital — it’s inaction disguised as “more research.” The strategies exist. The platforms exist. The financing tools exist. What’s needed is a decision to start, followed by a specific first step.

Here’s your action plan based on where you are right now:

- If you have under $1,000: Open a Fundrise account or buy shares in a REIT ETF. Start learning how real estate returns work with real money.

- If you have $1,000–$10,000: Aggressively build your credit score to 720+, open an Arrived account for fractional exposure, and start saving specifically for a down payment.

- If you have $10,000–$25,000: Get pre-approved for an FHA loan, research multi-family properties in your target market, and execute a house hack.

- If you have $25,000+: You have enough to pursue a conventional rental property or a more aggressive house hack. Run the numbers on at least 10 properties before making an offer on one.

Real estate has created more millionaires than virtually any other asset class in American history. The market in 2026 — with institutional investors being pushed back, supply constraints easing, and technology making analysis faster than ever — is genuinely impeccable for beginners who are prepared and willing to act.

Let it cook. Build the foundation. Make the first move.

For ongoing market intelligence, investment strategy updates, and tools built specifically for investors at every level, the RERIQ Investment Hub is updated regularly with data-backed, broker-written content — free, no paywall, no brokerage agenda. Thank you for reading How to Start Investing in Real Estate!

References

[1] Watch – https://www.youtube.com/watch?v=3WzFBU1iOKo

[2] Housing Regulation Changes For Real Estate Investors What The New Executive Order Means – https://dominionfinancialservices.com/housing-regulation-changes-for-real-estate-investors-what-the-new-executive-order-means/

[3] 2026 Real Estate Market Predictions What Investors Should Expect As The Odds Shift In Your Favor – https://www.ascapital.us/blog-posts/2026-real-estate-market-predictions-what-investors-should-expect-as-the-odds-shift-in-your-favor

[4] Us Real Estate Market Outlook 2026 – https://www.cbre.com/insights/books/us-real-estate-market-outlook-2026

[5] All Cash All Eyes On You What The New 2026 Fincen Rule – https://lucas-real-estate.com/all-cash-all-eyes-on-you-what-the-new-2026-fincen-rule/

[8] Removing Regulatory Barriers To Affordable Home Construction – https://www.whitehouse.gov/presidential-actions/2026/03/removing-regulatory-barriers-to-affordable-home-construction/

{kind=link}