Picture this: You're scrolling through home buying sites in early 2026, and suddenly mortgage rates start dropping faster than your favorite streaming service's stock price. What's behind this extraordinary shift? The federal government just unleashed a $200 billion mortgage-backed securities (MBS) buying program designed to make homeownership more accessible—and it's already making waves across the housing market.

How the Federal Government's $200 Billion MBS Purchase is Lowering Mortgage Rates in 2026 represents one of the most significant housing market interventions in recent years. On January 8, 2026, the Trump administration directed Fannie Mae and Freddie Mac to purchase $200 billion in mortgage-backed securities with one clear objective: drive mortgage rates lower and reignite the American dream of homeownership.[3]

For buyers who've been sitting on the sidelines watching rates hover near decade highs, this fresh approach is absolutely based. The initiative isn't just government talk—it's already delivering tangible results that could save homebuyers hundreds of dollars monthly. Let's break down exactly what's happening, why it matters, and how you can capitalize on this impeccable opportunity.

Key Takeaways 🎯

- The federal government directed Fannie Mae and Freddie Mac to purchase $200 billion in MBS to actively push mortgage rates lower throughout 2026[3]

- Immediate market response was extraordinary: Agency MBS spreads tightened 10-15 basis points versus Treasuries within days of the announcement[3]

- Real savings potential: A 1.5% rate reduction on a $200,000 loan translates to approximately $520 in monthly payment savings

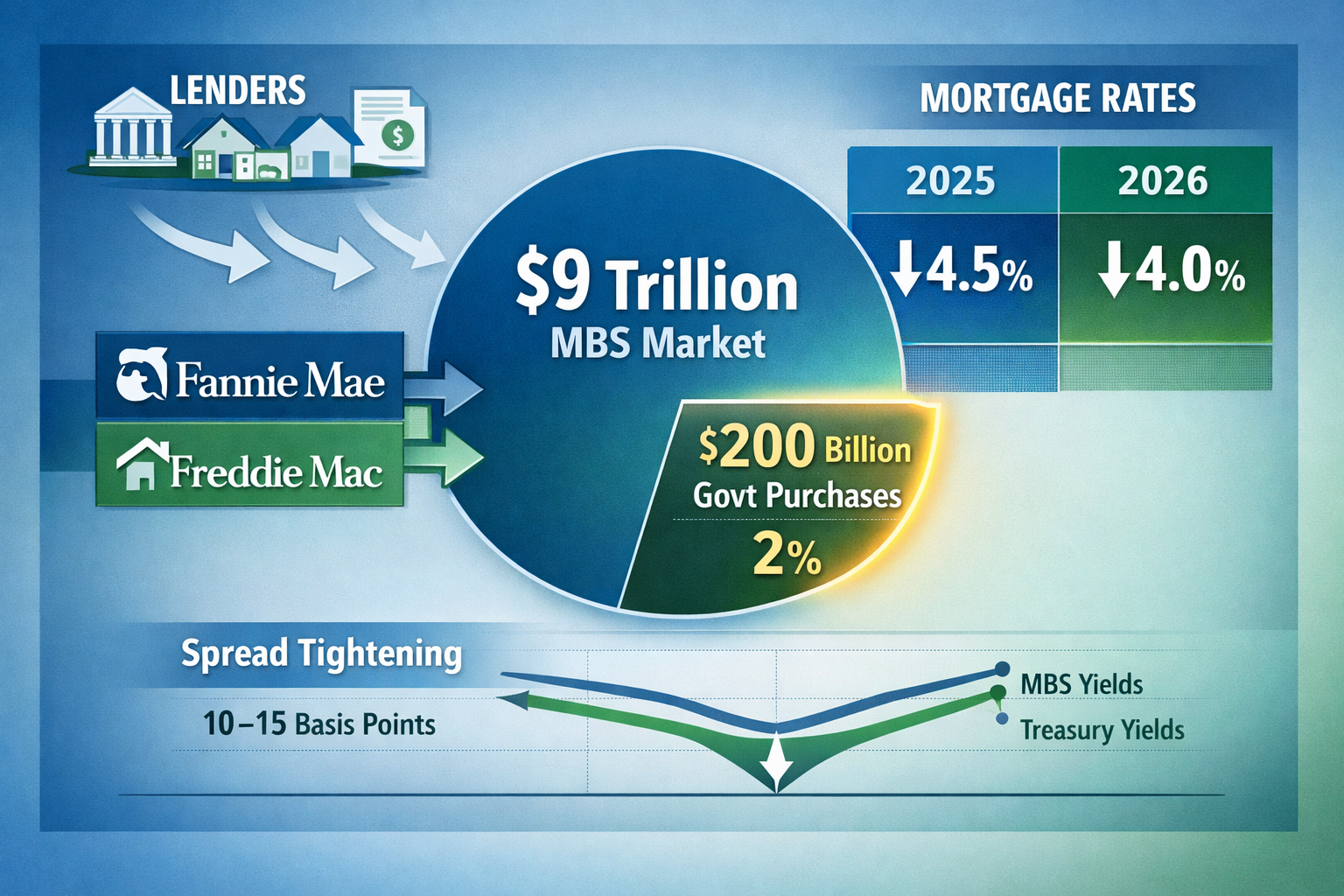

- The $200 billion represents about 2% of the $9 trillion Agency MBS market, creating targeted pressure without overwhelming the system[3]

- GSEs were already building momentum with $59 billion in MBS purchases during the second half of 2025, setting the stage for accelerated 2026 activity[9]

Understanding How the Federal Government's $200 Billion MBS Purchase Works 📊

What Are Mortgage-Backed Securities Anyway?

Before diving into the mechanics of how the Federal Government's $200 Billion MBS Purchase is lowering mortgage rates in 2026, let's get on the same page about what MBS actually are. Think of mortgage-backed securities as investment packages containing bundles of home loans. When you get a mortgage from your local lender, that loan often gets packaged with hundreds of others and sold to investors as a security.

The Agency MBS market is absolutely massive—we're talking close to $9 trillion in total size.[3] This market is dominated by securities backed by Fannie Mae and Freddie Mac, the government-sponsored enterprises (GSEs) that provide liquidity and stability to the mortgage market. When these agencies buy MBS, they're essentially creating demand for mortgage loans, which encourages lenders to offer more competitive rates.

The $200 Billion Directive: Breaking Down the Numbers

Here's where it gets interesting. The $200 billion program might sound enormous, but in the context of a $9 trillion market, it represents approximately 2% of the total Agency MBS market.[3] This is actually a strategic sweet spot—large enough to move the needle on rates without creating market distortions or speculation about massive program expansions.

What makes this initiative so based is that Fannie Mae and Freddie Mac weren't starting from zero. These GSEs had already been purchasing MBS for several months before the official directive, maintaining a pace of around $16 billion per month (approximately $192 billion annualized).[3] The December 2025 disclosures showed even larger purchases of $24.6 billion, suggesting momentum was building before the formal announcement.[3]

The combined GSEs increased their Agency MBS holdings by approximately $59 billion in the second half of 2025 alone, demonstrating strong purchasing activity that laid the groundwork for 2026's accelerated program.[9]

How MBS Purchases Actually Lower Your Mortgage Rate

Let's connect the dots between government purchases and the rate you see on your mortgage application. When Fannie Mae and Freddie Mac buy MBS, they increase demand for these securities. Basic economics tells us that increased demand raises prices. When MBS prices rise, their yields fall—and mortgage rates are directly tied to MBS yields.

Think of it like this: If investors can get a better return on MBS (because the government is buying them up and supporting prices), lenders can offer mortgages at lower interest rates while still making the same profit when they sell those loans into the MBS market. It's a chain reaction that flows from Washington directly to your monthly payment.

The market response was immediate and impeccable. Agency MBS spreads tightened significantly on the announcement news, with 30-year conventional coupon pools trading closest to par dollar price (30-year 4.5% and 5.0% pools) moving 10-15 basis points versus Treasuries.[3] For those not fluent in finance-speak, this means the cost of borrowing for mortgages dropped meaningfully relative to other government bonds.

The Real-World Impact: What Lower Rates Mean for Your Wallet 💵

Calculating Your Monthly Savings

Numbers on a screen are one thing, but let's talk about what how the Federal Government's $200 Billion MBS Purchase is lowering mortgage rates in 2026 actually means for your bank account. The difference between an 8% mortgage rate (which we saw in parts of 2025) and a 6.5% rate (achievable with the current MBS buying program) is extraordinary.

On a $200,000 loan over 30 years:

- At 8% interest: Monthly payment = $1,468

- At 6.5% interest: Monthly payment = $1,264

- Monthly savings: $204

- Annual savings: $2,448

- Total savings over loan life: $73,440

On a $400,000 loan over 30 years:

- At 8% interest: Monthly payment = $2,935

- At 6.5% interest: Monthly payment = $2,528

- Monthly savings: $407

- Annual savings: $4,884

- Total savings over loan life: $146,520

These aren't hypothetical numbers—they represent real purchasing power returning to American families. That extra $200-$500 monthly could cover groceries, childcare, student loans, or build an emergency fund. For first-time homebuyers especially, this difference can mean the gap between qualifying for a home or continuing to rent.

Who Benefits Most from This Program?

While lower rates help everyone, certain groups are positioned to gain extraordinary advantages:

🏠 First-Time Homebuyers: Those who've been priced out by high rates suddenly find affordability within reach. The combination of lower monthly payments and improved debt-to-income ratios opens doors that were previously closed.

🔄 Refinancers: Homeowners who locked in rates above 7% in 2023-2025 can now potentially refinance and slash their monthly obligations. The Federal Reserve's MBS holdings have been declining (down to $2.135 trillion as of July 2025 from $2.707 trillion when quantitative tightening began),[1] but the GSE buying program creates a new pathway for refinancing activity.

📈 Real Estate Investors: Lower financing costs improve cash flow on rental properties and make investment strategies more viable. The improved economics of leveraged real estate could reignite investor activity in 2026.

🏘️ Move-Up Buyers: Families looking to upgrade from starter homes to larger properties benefit from both lower rates on new purchases and potentially higher sale prices as buyer demand increases.

Market Momentum: Early 2026 Trends

The housing market is already responding to the rate environment shift. Whether to rent or buy in 2026 is becoming an easier decision as the monthly cost gap between renting and owning narrows in many markets.

Real estate agents are reporting increased buyer activity, with more serious inquiries and faster movement from browsing to making offers. This fresh energy in the market is exactly what policymakers hoped to achieve—stimulating housing transactions without creating artificial bubbles.

The Broader Economic Context Behind the MBS Purchase Strategy 📈

Why Now? The Perfect Storm for Intervention

Understanding how the Federal Government's $200 Billion MBS Purchase is lowering mortgage rates in 2026 requires looking at the broader economic landscape that made this intervention both possible and necessary.

The Yield Curve Re-Steepening: One critical factor working in favor of MBS returns is the re-steepening U.S. Treasury yield curve (the 10-year/2-year spread). A steeper yield curve provides a favorable environment as a tailwind for MBS returns entering 2026.[5] This technical market condition creates an ideal backdrop for the government's buying program to have maximum impact.

Banking Sector Alignment: Federal Reserve Vice Chair for Supervision Michelle Bowman indicated a softer, more industry-friendly Basel III endgame proposal for early 2026. This proposal implicitly includes relief on securitization capital requirements, viewed as a net positive that could boost MBS demand from domestic banks.[5] When banks find it easier and more profitable to hold MBS, they become natural allies in the government's rate-lowering mission.

MBS Had Its Best Year Since 2002: The MBS market entered 2026 with serious momentum. Strong 2025 performance created positive sentiment and attracted investor attention, making the market receptive to the government's intervention.[5] You could say the market was ready to let it cook.

The Fed's Parallel MBS Runoff Program

While Fannie Mae and Freddie Mac are buying MBS, the Federal Reserve continues its quantitative tightening program, allowing its MBS holdings to decline through natural paydowns. The Fed's MBS holdings fell to $2.135 trillion as of July 2025, down from $2.707 trillion when the reduction program began in June 2022.[1]

Interestingly, the Fed's MBS reduction process is running approximately 18 months behind schedule.[1] Why? Because the mortgage rate declines and refinancing activity necessary for faster paydowns haven't materialized as expected. Homeowners who locked in ultra-low rates in 2020-2021 have zero incentive to refinance, creating a "lock-in effect" that slows MBS paydowns.

The Treasury estimates MBS paydowns will total approximately $180 billion for calendar year 2026,[4] creating natural supply that the GSE buying program can absorb without creating artificial scarcity.

Domestic Bank Demand: The Supporting Cast

The GSE buying program isn't operating in isolation. Analysts expect increasing MBS presence from domestic banks in 2026, supported by deposit growth and improving net interest margins.[5] As banks rebuild their balance sheets and seek yield, MBS become attractive investments—especially with the implicit government support signaled by the $200 billion program.

This creates a virtuous cycle: Government purchases support MBS prices → Banks see attractive risk-adjusted returns → Banks increase MBS purchases → Additional demand further supports prices and lowers mortgage rates → More homebuyers can afford homes → Economic activity increases.

Potential Risks and Limitations: The Reality Check ⚠️

The 2% Question: Is $200 Billion Enough?

While the program is already showing results, some market observers question whether $200 billion—representing just 2% of the $9 trillion Agency MBS market—can sustain meaningful rate reductions throughout 2026.[3] There's limited speculation about program expansion, which means the current allocation needs to be strategically deployed for maximum impact.

The good news? The GSEs have demonstrated purchasing discipline, ramping up activity from $16 billion monthly to $24.6 billion in December 2025 before the formal directive.[3] This suggests they're calibrating purchases to market conditions rather than following a rigid schedule.

The Inflation Wildcard

Any government program that stimulates housing demand carries potential inflation risks. If the MBS buying program successfully lowers rates and triggers a housing boom, increased demand could push home prices higher—potentially offsetting some of the affordability gains from lower rates.

However, the program's relatively modest size (2% of market) and the existence of substantial housing inventory in many markets should help moderate price pressure. The key is finding the sweet spot where transaction volume increases without creating bidding wars that price out the very buyers the program aims to help.

Treasury Bill Demand Dynamics

The Treasury's Reserve Management Programs are expected to account for approximately $360 billion of Treasury bill demand in 2026.[4] This massive demand for short-term government debt creates competing forces in the fixed-income market. If Treasury bill rates become too attractive relative to MBS yields, private investors might rotate away from MBS, requiring even more government buying to maintain rate targets.

The Refinancing Paradox

Here's an interesting twist: If the MBS buying program successfully lowers rates enough to trigger a refinancing wave, it could accelerate MBS paydowns and reduce the effectiveness of the buying program. Homeowners refinancing out of higher-rate mortgages create prepayment risk for MBS holders, potentially requiring the GSEs to purchase even more securities to maintain their holdings.

The Fed's experience with slower-than-expected MBS runoff (18 months behind schedule)[1] suggests this risk may be overstated in the current environment, but it's worth monitoring as 2026 progresses.

Actionable Strategies: How to Capitalize on Lower Rates 🎯

For Homebuyers: Timing Your Purchase

If you're in the market for a home, the current environment presents an impeccable opportunity—but strategy matters:

1. Get Pre-Approved Now: Lock in your borrowing capacity at current rates. Even if you're not ready to buy immediately, knowing what you can afford helps you act quickly when the right property appears. Check out our guide on fast-tracking homeownership with pre-approval.

2. Monitor Rate Trends Weekly: Mortgage rates can fluctuate based on MBS market conditions. Work with a lender who provides regular rate updates and can lock your rate when conditions are optimal.

3. Consider Rate Lock Strategies: Some lenders offer float-down options that let you lock a rate but benefit if rates drop further before closing. These typically cost extra but can be worthwhile in a declining rate environment.

4. Expand Your Search Radius: Lower rates improve affordability, potentially allowing you to consider neighborhoods or property types previously outside your budget. Use AI tools to analyze local markets and identify emerging value opportunities.

5. Don't Forget Closing Costs: Lower rates are extraordinary, but closing costs still matter. Learn how to get sellers to pay closing costs to maximize your savings.

For Current Homeowners: Refinancing Decisions

If you're carrying a mortgage above 7%, the math on refinancing becomes compelling:

Calculate Your Break-Even Point: Refinancing involves costs (typically 2-5% of loan amount). Divide your total refinancing costs by your monthly savings to determine how many months until you break even. If you plan to stay in the home longer than the break-even period, refinancing makes sense.

Example:

- Refinancing costs: $6,000

- Monthly savings: $300

- Break-even: 20 months

If you plan to stay in your home for at least two years, this refinance is a smart move.

Watch for No-Closing-Cost Options: Some lenders offer no-closing-cost refinances where they cover upfront costs in exchange for a slightly higher interest rate. Run the numbers—sometimes these deals make sense for shorter time horizons.

Consider Cash-Out Refinancing: If you've built substantial equity, lower rates might make cash-out refinancing attractive for home renovations, debt consolidation, or investment opportunities.

For Real Estate Investors: Leveraging the Rate Environment

The Federal Government's $200 Billion MBS Purchase lowering mortgage rates in 2026 creates fresh opportunities for real estate investors:

Acquisition Financing: Lower rates improve cash flow on rental properties. A property that barely cash-flowed at 7.5% might generate healthy monthly income at 6.5%. Run your numbers using conservative assumptions and consider expanding your portfolio.

Portfolio Refinancing: If you own multiple investment properties with rates above current market, systematic refinancing can dramatically improve your overall portfolio performance. Prioritize refinancing properties with the highest rate differentials first.

BRRRR Strategy Revival: The Buy, Rehab, Rent, Refinance, Repeat (BRRRR) strategy becomes more viable as refinancing rates drop. Lower rates mean you can pull more capital out during the refinance phase while maintaining positive cash flow.

Leverage Optimization: Lower rates allow investors to safely increase leverage while maintaining acceptable debt service coverage ratios. This can amplify returns on successful investments—though it also amplifies risk, so proceed carefully.

For Real Estate Professionals: Serving Clients Better

Agents and brokers who understand how the Federal Government's $200 Billion MBS Purchase is lowering mortgage rates in 2026 can provide extraordinary value to clients:

Educate Clients: Most buyers don't understand MBS markets or government intervention programs. Agents who can explain these concepts in plain English build trust and credibility. Share this article with your database!

Partner with Informed Lenders: Work with mortgage professionals who stay current on market conditions and can explain rate movements to clients. The lender who can articulate why rates are dropping (and when to lock) becomes invaluable to your team.

Adjust Marketing Messages: Your marketing should reflect the improved affordability story. "Rates are dropping thanks to government MBS purchases—now's the time to buy" is a compelling message for fence-sitters.

Leverage Technology: Use AI tools for lead generation and client education. Automated market updates highlighting rate changes keep you top-of-mind with your database.

Expand Your Knowledge Base: Consider continuing education opportunities that cover mortgage markets, economic policy, and investment analysis. The more you know, the more value you provide.

What to Watch: Key Indicators for the Rest of 2026 🔍

MBS Spread Movements

The 10-15 basis point tightening in Agency MBS spreads versus Treasuries that occurred immediately after the announcement[3] set a baseline. Watch for continued tightening as the GSE buying program progresses. If spreads widen significantly, it could signal market skepticism about the program's effectiveness or competing forces overwhelming the government purchases.

GSE Purchase Pace

Monthly disclosures from Fannie Mae and Freddie Mac will reveal whether they maintain the accelerated purchase pace ($24.6 billion in December 2025)[3] or adjust based on market conditions. Consistent high-volume purchases signal serious commitment to the rate-lowering mission.

Refinancing Activity

The Mortgage Bankers Association publishes weekly application data showing purchase and refinance volume. A surge in refinancing applications would indicate rates have dropped enough to overcome the lock-in effect keeping many homeowners in their current mortgages. This would be a clear sign the program is working.

Home Sales Volume

Existing home sales data from the National Association of Realtors provides the ultimate measure of whether lower rates are translating to increased market activity. Rising sales volumes validate the program's effectiveness in stimulating housing transactions.

Treasury Yield Curve

Monitor the 10-year/2-year Treasury spread. The re-steepening yield curve has provided tailwinds for MBS returns.[5] If the curve flattens or inverts, it could complicate the MBS buying program's effectiveness.

Bank MBS Holdings

Quarterly bank call reports reveal whether domestic banks are increasing MBS holdings as analysts predict.[5] Growing bank demand would amplify the government program's impact and suggest sustainable rate improvements.

The Political and Policy Landscape 🏛️

Bipartisan Housing Affordability Concerns

While the MBS buying program emerged from a Republican administration directive, housing affordability enjoys rare bipartisan support. Both parties recognize that homeownership rates, especially among younger Americans, have declined to concerning levels. This political alignment suggests the program is likely to continue regardless of shifting political winds.

Fannie Mae and Freddie Mac's Unique Position

The GSEs have operated in conservatorship since the 2008 financial crisis, giving the federal government significant control over their operations. This unique status allows the government to direct MBS purchases without requiring new legislation or appropriations—a key advantage for rapid policy implementation.

The question of GSE reform and potential privatization has simmered for years, but the current MBS buying program actually strengthens the case for maintaining government involvement in mortgage markets. When private markets fail to deliver affordable housing finance, the GSEs provide a policy lever that pure private markets cannot.

Regulatory Tailwinds

The softer Basel III endgame proposal mentioned by Fed Vice Chair Bowman[5] represents broader regulatory philosophy favoring market liquidity and economic growth over maximum capital requirements. This regulatory environment supports not just the MBS buying program but the entire ecosystem of housing finance.

For real estate professionals and investors, this suggests a multi-year window of relatively favorable financing conditions—assuming economic fundamentals remain stable.

Comparing 2026 to Historical MBS Interventions 📚

The 2008-2014 Playbook

The current $200 billion program is modest compared to the Federal Reserve's post-financial crisis MBS purchases, which ultimately grew the Fed's MBS portfolio to over $2.7 trillion.[1] However, the economic contexts differ dramatically:

Then: The housing market was collapsing, foreclosures were surging, and the financial system faced existential threats. MBS purchases aimed to prevent economic catastrophe.

Now: The housing market is fundamentally healthy, with strong demand constrained primarily by affordability challenges. MBS purchases aim to stimulate activity and improve access, not prevent collapse.

This distinction matters because it suggests the current program can achieve meaningful results with smaller scale. The market isn't broken—it just needs a nudge toward better affordability.

The COVID-Era Comparison

During the COVID-19 pandemic, the Federal Reserve rapidly expanded MBS purchases to maintain market functioning and support the economy. Those emergency purchases helped drive mortgage rates to historic lows (briefly below 3% for 30-year fixed mortgages).

The current program isn't targeting emergency-level rates. Instead, it aims for sustainable rates that balance affordability with financial system stability—probably in the 6-6.5% range for conventional 30-year mortgages. This more modest goal actually increases the likelihood of success and sustainability.

Expert Perspectives: What Industry Leaders Are Saying 💬

Mortgage Industry Optimism

Mortgage lenders and brokers have welcomed the MBS buying program as a catalyst for increased origination volume after a challenging 2023-2025 period. Industry conferences in early 2026 featured optimistic forecasts for refinancing and purchase activity, with many lenders expanding capacity in anticipation of higher application volumes.

Real Estate Market Analysts

Housing market analysts note that the program addresses one of the two major affordability challenges (high rates) but doesn't directly address the other (limited inventory in many markets). The most optimistic scenarios envision lower rates stimulating new construction by improving builder economics, gradually expanding supply to match demand.

Economic Policy Debates

Economists debate whether government intervention in MBS markets represents appropriate policy or market distortion. Supporters argue that housing's unique role in wealth building and economic stability justifies targeted intervention. Critics worry about moral hazard and the precedent of using GSEs for rate manipulation.

For practical purposes, homebuyers and investors should focus less on the theoretical debates and more on the tangible reality: rates are lower than they would be without the program, creating opportunities for those positioned to act.

Long-Term Implications: Beyond 2026 🔮

Establishing New Market Norms

If the $200 billion MBS buying program successfully establishes mortgage rates in the 6-6.5% range as the "new normal" for 2026, it could reset market expectations and attract private capital that previously viewed MBS yields as inadequate. This could create a self-sustaining cycle where government purchases eventually become unnecessary as private demand fills the gap.

Housing Market Structural Changes

Lower rates combined with demographic trends (millennials entering peak homebuying years, Gen Z beginning their housing journeys) could drive a multi-year housing expansion. This would have ripple effects across construction, home improvement, furnishings, and countless related industries.

Real estate professionals who position themselves now to serve this expanding market—through technology adoption, marketing excellence, and deep market knowledge—stand to benefit extraordinarily.

The Path to GSE Reform

Ironically, the success of the MBS buying program might accelerate conversations about GSE reform and potential privatization. If Fannie Mae and Freddie Mac demonstrate they can effectively manage large-scale market interventions while maintaining profitability, it strengthens arguments for returning them to private ownership with appropriate regulatory oversight.

Conversely, if the program proves essential to maintaining affordable mortgage rates, it could cement the GSEs' role as permanent government-controlled entities serving public policy objectives.

Conclusion: Seizing the Moment in 2026's Mortgage Market 🚀

How the Federal Government's $200 Billion MBS Purchase is lowering mortgage rates in 2026 represents more than just another policy initiative—it's a genuine opportunity for Americans to achieve homeownership dreams that seemed out of reach just months ago. The extraordinary combination of strategic government intervention, favorable yield curve dynamics, and increasing bank demand for MBS has created a fresh environment for housing finance.

The numbers tell a compelling story: 10-15 basis point spread tightening,[3] $59 billion in GSE purchases during late 2025,[9] and the potential for $520 monthly savings on a typical $200,000 mortgage compared to peak 2025 rates. These aren't abstract statistics—they represent real purchasing power returning to American families.

For homebuyers, the message is clear: Stop gatekeeping your homeownership dreams. The rate environment is improving, and waiting for perfection means missing real opportunities. Get pre-approved, understand your budget, explore the best home buying sites, and position yourself to act when the right property appears.

For current homeowners with higher-rate mortgages, run the refinancing numbers. The break-even analysis might surprise you, and the long-term savings could be impeccable.

For real estate investors, lower financing costs improve deal economics across acquisition, refinancing, and portfolio optimization strategies. The market is fresh with opportunity for those who understand the fundamentals.

For real estate professionals, this is your moment to demonstrate value by educating clients about market dynamics, connecting them with informed lenders, and guiding them through decisions that could save tens of thousands of dollars over the life of their mortgages.

Your Next Steps

- Monitor rates weekly through your lender or financial websites

- Get pre-approved or re-evaluate your current mortgage situation

- Educate yourself on market trends and predictions to make informed decisions

- Consult professionals who understand the current market dynamics

- Act strategically when opportunities align with your goals

The Federal Government's $200 Billion MBS Purchase isn't just lowering mortgage rates—it's opening doors to homeownership and wealth building for millions of Americans. The question isn't whether this program matters; it's whether you'll position yourself to benefit from it.

Real Estate Rank IQ is here to guide you through every step of your real estate journey, from understanding complex market dynamics to executing winning strategies. Subscribe to our YouTube channel @Realestaterankiq for regular market updates, and explore our comprehensive guides on everything from first-time homebuying to advanced investment strategies.

The 2026 mortgage market is so based right now—don't let this extraordinary opportunity pass you by. 🏡✨

References

[1] Latest Move By The Federal Reserve – https://www.hsh.com/finance/mortgage/latest-move-by-the-federal-reserve.html

[3] February 2026 Market Commentary – https://www.almfirst.com/resources/monthly-market-commentary/february-2026-market-commentary

[4] Tbaccharge1q12026 – https://home.treasury.gov/system/files/221/TBACCharge1Q12026.pdf

[5] Mbs Just Had Its Best Year Since 2002 Whats In Store For 2026 – https://www.janushenderson.com/en-us/advisor/article/mbs-just-had-its-best-year-since-2002-whats-in-store-for-2026/

[9] Lawler Update On Gses And Early Read – https://calculatedrisk.substack.com/p/lawler-update-on-gses-and-early-read

{kind=link}