Last updated: March 25, 2026

Quick Answer: Buying your first home in 2026 starts with three non-negotiables: knowing your credit score, getting mortgage pre-approved, and setting a realistic budget before you tour a single property. With mortgage rates hovering around 6.22% for a 30-year fixed loan and homes sitting on the market a median of 58 days, first-time buyers who prepare financially have a real window of opportunity this spring [8]. This guide covers every step of the home buying process, from financial readiness to closing day, written by licensed brokers with over 15 years of experience.

🏠 Key Takeaways

- Credit score matters most: A score of 620+ qualifies for most conventional loans; 580+ for FHA. Higher scores unlock better rates.

- Pre-approval is not optional: Sellers and agents treat pre-approval as proof you're serious. Without it, your offer is weak.

- Budget beyond the mortgage: Closing costs, home inspections, insurance, and maintenance add 3–6% to your purchase price upfront.

- 2026 is a buyer's window: Rising inventory, sellers open to negotiation, and easing rates toward 6% create real opportunity for first-timers [2].

- First-time buyer programs exist: FHA, USDA, VA, and state-level down payment assistance programs can dramatically reduce your upfront costs.

- Needs vs. wants list is a decision tool: It prevents emotional overspending and keeps your search focused.

- Home inspection is non-negotiable: Never waive it. A $400–$600 inspection can save you from a $40,000 surprise.

- Your agent works for you: A buyer's agent costs you nothing out of pocket in most transactions and negotiates on your behalf.

- The Homebuyers Privacy Protection Act (March 2026) now restricts trigger leads, meaning fewer unsolicited lender calls after you apply for a mortgage [3].

- Long-term planning matters: Think about resale value, neighborhood trajectory, and future-proof features from day one.

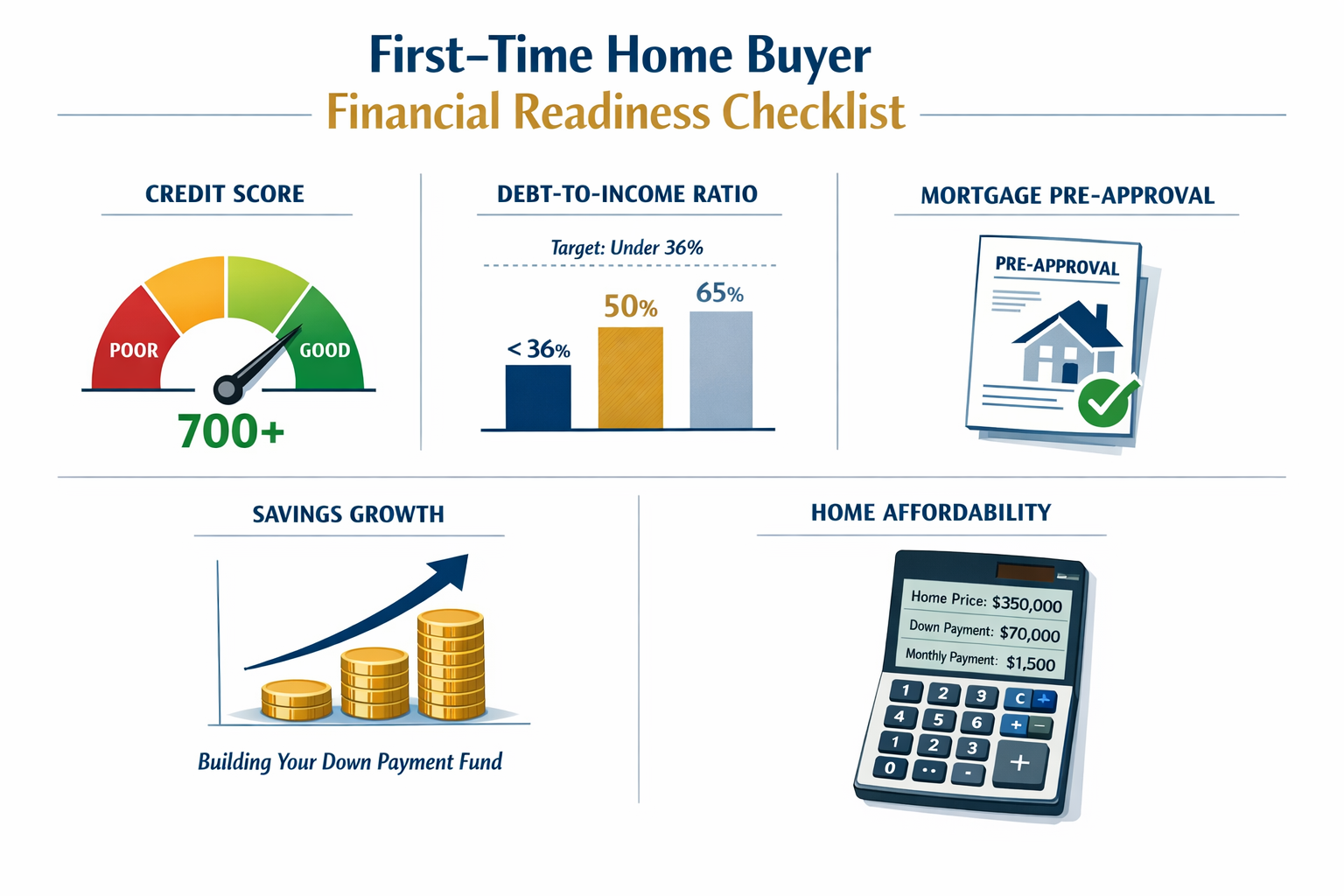

Step 1: Assess Your Financial Readiness Before Anything Else

Financial readiness is the foundation of every successful first home purchase. Before searching listings or attending open houses, first-time buyers need a clear picture of their credit health, debt load, and savings. Skipping this step is the number one reason buyers get derailed mid-process.

Check Your Credit Score First

Most lenders use the FICO scoring model. Here's what different score ranges mean for your mortgage options:

| Credit Score Range | Loan Options Available | Typical Impact |

|---|---|---|

| 760+ | All loan types | Best available rates |

| 700–759 | Conventional, FHA, VA | Competitive rates |

| 660–699 | Conventional (higher rate), FHA | Moderate rates |

| 620–659 | FHA, some conventional | Higher rates, PMI likely |

| 580–619 | FHA (3.5% down) | Limited options |

| Below 580 | FHA with 10% down | Very limited |

Common mistake: Many first-time buyers check their score once and assume it's accurate. Pull your report from all three bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com and dispute any errors before applying.

To improve your score quickly:

- Pay down credit card balances below 30% of your limit

- Don't open new credit accounts in the 6 months before applying

- Keep old accounts open (length of credit history matters)

- Set up autopay to eliminate missed payment risk

Calculate Your Debt-to-Income Ratio (DTI)

Lenders want your total monthly debt payments (including the new mortgage) to stay below 43% of your gross monthly income. Some loan programs allow up to 50% with compensating factors.

Formula: (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100 = DTI%

Example: If you earn $6,000/month and have $500 in existing debt payments, a lender might approve a mortgage payment up to $2,080/month (keeping total DTI at 43%).

For a deeper look at budgeting for homeownership, explore the budgeting for homeownership resources at Real Estate Rank IQ.

Step 2: Determine How Much Home You Can Actually Afford

Affordability isn't just about what a lender approves — it's about what you can comfortably sustain long-term. Lenders will often approve you for more than you should spend. The real number is what fits your lifestyle without financial stress.

The Full Cost of Buying a Home

First-time buyers frequently underestimate the total cash needed. Here's a realistic breakdown:

Upfront costs:

- Down payment: 3%–20% of purchase price (FHA minimum is 3.5%)

- Closing costs: Typically 2%–5% of the loan amount, covering appraisal, title insurance, origination fees, and more

- Home inspection: $400–$600 on average

- Moving costs: $1,000–$5,000+ depending on distance and volume

- Immediate repairs/furnishings: Variable, but budget $2,000–$10,000 minimum

Ongoing monthly costs:

- Principal and interest (mortgage payment)

- Property taxes (varies widely by location)

- Homeowner's insurance ($1,200–$2,400/year average)

- Private mortgage insurance (PMI) if down payment is under 20%

- HOA fees (if applicable)

- Maintenance reserve (budget 1% of home value per year)

💡 Pro tip from the field: A $350,000 home with 5% down and a 6.22% rate in 2026 generates roughly a $2,050/month principal and interest payment. Add taxes, insurance, and PMI, and the real monthly cost lands closer to $2,600–$2,900. Run those numbers before falling in love with a listing.

To understand whether buying makes more sense than renting in your market right now, check out Will You Rent or Buy in 2026? for a data-driven comparison. LendingTree data shows homeowners currently pay roughly 36.9% more monthly than renters in most large U.S. metros, so the math genuinely depends on your local market and timeline.

Step 3: Get Mortgage Pre-Approval (Not Just Pre-Qualification)

Mortgage pre-approval is the single most important step before making an offer. Pre-qualification is a quick estimate based on self-reported data. Pre-approval involves a hard credit pull and document verification — it's what sellers and listing agents actually respect.

How to Get Pre-Approved: A Step-by-Step Process

- Gather your documents: W-2s (last 2 years), pay stubs (last 30 days), bank statements (last 2–3 months), tax returns, and ID

- Shop at least 3 lenders: Rates and fees vary significantly. Comparing multiple lenders within a 45-day window counts as a single hard inquiry on your credit

- Submit your application: The lender reviews income, assets, employment, and credit

- Receive your pre-approval letter: This specifies the loan amount you qualify for

- Understand what it means: Pre-approval is not a guarantee — the final loan is still subject to appraisal and underwriting

2026 update: New executive orders signed March 16, 2026, are modernizing the mortgage process by eliminating wet-signature requirements for digital mortgages, making the pre-approval process faster and more accessible [9]. The 2026 Housing Act also reduces regulatory burdens on small-dollar mortgages, which is great news for buyers targeting lower-priced starter homes [9].

Protect yourself from trigger leads: When you apply for a mortgage, credit bureaus historically sold that inquiry data to competing lenders, flooding applicants with unsolicited calls. The Homebuyers Privacy Protection Act, effective March 5, 2026, now restricts this practice significantly [3]. You can still opt out proactively at OptOutPrescreen.com.

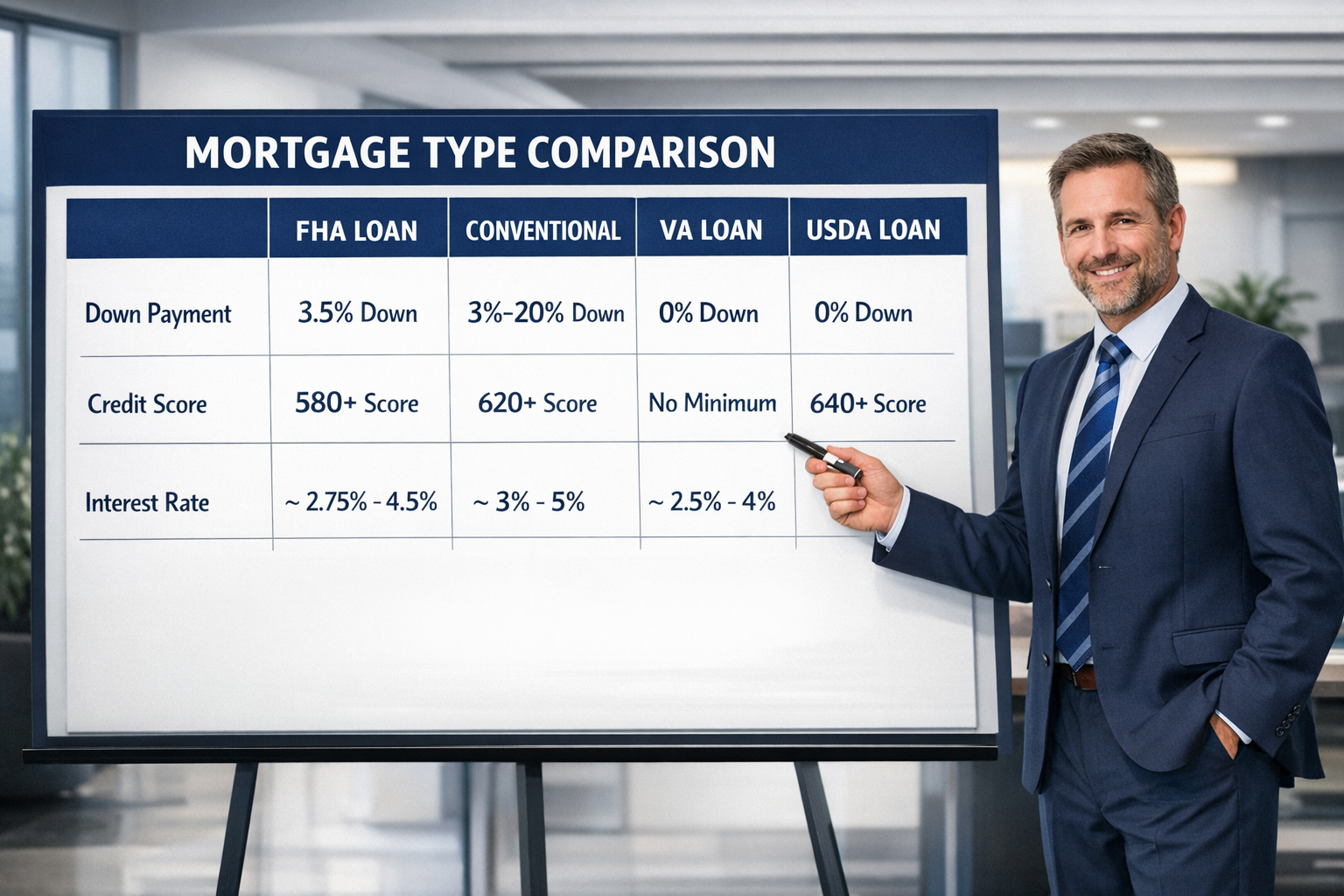

Step 4: Understand Your Mortgage Options (This Is Where Most Guides Go Shallow)

Choosing the wrong mortgage type can cost tens of thousands of dollars over the life of your loan. Most first-time buyer guides mention FHA loans and move on. Here's the full comparison.

Mortgage Type Comparison Table

| Loan Type | Min. Down Payment | Min. Credit Score | Best For | Key Limitation |

|---|---|---|---|---|

| Conventional | 3% | 620 | Strong credit buyers | PMI under 20% down |

| FHA | 3.5% | 580 | Lower credit scores | Mortgage insurance for life of loan (if <10% down) |

| VA | 0% | No minimum (lender sets) | Veterans, active military | Must have VA eligibility |

| USDA | 0% | 640 recommended | Rural/suburban buyers | Geographic and income limits |

| Jumbo | 10–20% | 700+ | High-cost markets | Stricter qualification |

Fixed vs. Adjustable Rate

- 30-year fixed: Predictable payment, higher rate. Best if you plan to stay 7+ years.

- 15-year fixed: Lower rate, higher payment, significant interest savings. Best if you can afford it.

- 5/1 or 7/1 ARM: Lower initial rate, adjusts after fixed period. Best if you plan to sell or refinance within the fixed window.

With 30-year fixed rates at 6.22% as of March 2026 [8], an ARM might make sense for buyers who plan to move within 5–7 years. For Gen Z buyers navigating financing options specifically, the Best Mortgage Options for Gen Z Home Buyers 2026 Guide breaks down generational strategies in detail.

Builder Incentives Are Real in 2026

Robert Dietz, chief economist at NAHB, notes that 40% of builders cut new home prices by 5% and many are offering rate buydowns to move inventory [2]. Townhomes now represent 18% of single-family starts (up from 10% a decade ago), making them a fresh, affordable entry point for first-timers [2].

Step 5: Research Neighborhoods Like a Pro

The right neighborhood matters as much as the right house. A great home in a declining area is a poor investment. A modest home in an appreciating neighborhood builds wealth.

What to Research Before Committing to a Location

- School ratings: Even for buyers without children, school quality drives resale value

- Commute time: Test the actual commute during rush hour, not Google Maps' estimate

- Crime statistics: Use local police department data, not just aggregator sites

- Walkability and transit scores: Walk Score and Transit Score are free tools

- Future development plans: Check the city's zoning map and development pipeline

- Flood zones and climate risk: FEMA flood maps and First Street Foundation's risk data are essential

- Price trends: Are median prices rising, flat, or declining in the past 12–24 months?

NAR's Jessica Lautz notes that 2026 offers first-time buyers real opportunities from easing rates, rising inventory, and seller willingness to negotiate — potentially helping 1.6 million renters make the leap to ownership [2]. Realtor.com's research identifies specific markets where first-timers have the strongest combination of affordability, inventory, and job growth [4].

⚠️ Important caveat from Realtor.com: Generic social media advice about neighborhoods and loans can be dangerously mismatched with your regional market and local regulations. Always verify tips with a local licensed professional [1].

For a data-driven look at where buyers are finding the best deals right now, see Zillow's Top Markets for Home Buyers 2026.

Step 6: Build Your Needs vs. Wants List (And Actually Use It)

A needs vs. wants list is a decision filter, not a wishlist. It prevents emotional overspending and keeps your search grounded when you walk into a beautifully staged home that's $80,000 over budget.

How to Build an Effective List

Non-negotiables (Needs) — examples:

- Minimum number of bedrooms for your household

- Specific school district

- Maximum commute distance

- Accessibility features (if applicable)

- Garage or off-street parking

- Within budget ceiling

Nice-to-haves (Wants) — examples:

- Finished basement

- Open floor plan

- Updated kitchen

- Large backyard

- Home office space

- Specific architectural style

The decision rule: If a home meets all your needs and at least 60–70% of your wants within budget, it's worth serious consideration. Don't let the remaining wants push you into a home you can't afford or a neighborhood that doesn't fit.

Interestingly, data shows that buyers are increasingly skipping large homes in favor of smaller, more efficient properties — a trend worth factoring into your list if long-term resale value is a priority.

Step 7: Work With the Right Real Estate Agent

A buyer's agent is your advocate, negotiator, and local market expert — and in most transactions, their commission doesn't come out of your pocket. Choosing the right agent is one of the highest-leverage decisions a first-time buyer makes.

What a Good Buyer's Agent Does For You

- Provides access to MLS listings before they hit public sites

- Schedules showings and identifies red flags during walkthroughs

- Prepares and submits competitive offers

- Negotiates price, repairs, and concessions on your behalf

- Coordinates with lenders, inspectors, and title companies

- Guides you through contingencies and contract terms

Questions to Ask Before Hiring an Agent

- How many first-time buyers have you represented in the past year?

- What's your average list-to-sale price ratio for buyers?

- How do you communicate — calls, texts, email?

- Are you full-time or part-time?

- Do you have relationships with lenders and inspectors you trust?

Insider tip: Ask about seller credits. Knowing which seller credits buyers ask for most — and how to request them effectively — can save thousands at closing. A skilled agent knows exactly when and how to ask.

Step 8: Make Offers and Negotiate Strategically

In 2026, with homes sitting on market a median of 58 days, first-time buyers have more negotiating power than they've had in years [8]. But that doesn't mean making lowball offers. It means making smart, well-supported offers.

Negotiation Strategies That Work for First-Time Buyers

- Use market data: Your agent should pull comparable sales (comps) from the last 90 days to anchor your offer price

- Request seller concessions: Ask for closing cost credits rather than price reductions — it's often easier for sellers to agree to and reduces your cash needed at closing. Learn how to get a home seller to pay closing costs with proven scripts

- Include an inspection contingency: Always. Non-negotiable

- Financing contingency: Protects your earnest money if financing falls through

- Escalation clauses: In competitive situations, an escalation clause automatically increases your offer by a set increment above competing bids, up to your maximum

- Be flexible on closing dates: Sellers often value timeline flexibility as much as price

For a full breakdown of negotiation tactics that save real money, see Negotiation Power Moves: Save Thousands On Your Next Home.

Step 9: Navigate the Home Inspection and Closing Process

The home inspection is your last major opportunity to uncover problems before you own them. Never waive it, even in a competitive market. A professional inspection covers the roof, foundation, electrical, plumbing, HVAC, and more.

What Happens After the Inspection

- Review the report: Your inspector will categorize findings by severity

- Negotiate repairs or credits: Request that sellers fix major issues or provide a credit at closing

- Appraisal: Your lender orders an appraisal to confirm the home's value supports the loan amount

- Final walkthrough: 24–48 hours before closing, verify the home's condition matches the contract

- Closing disclosure review: You'll receive this 3 business days before closing — review every line item

Closing Cost Breakdown

Closing costs typically run 2–5% of the loan amount. Here's what's included:

- Loan origination fee (0.5–1% of loan)

- Appraisal fee ($400–$600)

- Title search and insurance ($1,000–$2,500)

- Attorney fees (if required in your state)

- Prepaid interest, taxes, and insurance

- Recording fees

You can now calculate closing costs in minutes using AI tools — a genuinely useful application of technology that most buyers haven't discovered yet.

First-Time Homebuyer Programs: Don't Leave Money on the Table

First-time homebuyer programs can reduce your down payment, lower your rate, or provide direct grants. Most buyers don't know these programs exist until it's too late to use them.

Federal Programs

- FHA Loans: 3.5% down with a 580+ credit score. Backed by the Federal Housing Administration.

- VA Loans: 0% down for eligible veterans and active-duty military. No PMI.

- USDA Loans: 0% down for qualifying rural and suburban properties. Income limits apply.

- Fannie Mae HomeReady / Freddie Mac Home Possible: 3% down conventional loans with reduced PMI for income-qualifying buyers.

State and Local Programs

Every state has a housing finance agency (HFA) that offers down payment assistance, closing cost grants, and below-market rate loans for first-time buyers. Income limits and purchase price caps vary by state and county.

How to find your state program:

- Search "[Your State] Housing Finance Agency first-time buyer"

- Ask your lender — they should know which programs they're approved to offer

- Check HUD.gov's state-by-state resource list

Eligibility basics for most programs:

- Haven't owned a primary residence in the past 3 years (the standard definition of "first-time buyer")

- Income below area median income (AMI) threshold

- Purchase price within program limits

- Complete a HUD-approved homebuyer education course

The Emotional Side of Buying Your First Home (Competitors Skip This)

Home buying is one of the most emotionally charged financial decisions a person makes. Fear of making the wrong choice, pressure from family, and anxiety about debt are real factors that cause buyers to either rush in or freeze up entirely.

Common Emotional Pitfalls

- Falling in love with a home before the inspection: Leads to waiving contingencies or ignoring red flags

- Decision fatigue: After touring 30+ homes, buyers often settle or overpay just to end the search

- Comparison paralysis: Waiting for the "perfect" home while good options sell

- External pressure: Family opinions about neighborhoods, home size, or price can override sound financial judgment

The fix: Set your criteria before you start touring. Stick to your needs list. Give yourself a decision deadline after finding a home that meets your criteria. And remember — no home is perfect. The goal is the right home for your life and budget, not the ideal home from a magazine.

Long-Term Financial Planning Beyond the Purchase

Buying a home is the beginning of a wealth-building strategy, not the end goal. First-time buyers who think about resale value, equity building, and future-proof features from day one make significantly better decisions.

What to Think About on Day One

- Equity building: Extra principal payments early in the loan have an outsized impact due to amortization

- Future-proof features: Energy efficiency, EV charging capability, and smart home infrastructure are increasingly valued by buyers — inflation-proof home features buyers want in 2026 include EV chargers, battery backup systems, and energy-efficient kitchens

- Refinancing window: If rates drop below your current rate by 0.75–1%, refinancing may make sense

- Home warranty: A home warranty can cover major systems and appliances in the first years of ownership, reducing surprise repair costs

- Tax benefits: Mortgage interest and property tax deductions may reduce your federal tax liability (consult a tax professional for your specific situation)

FAQ: First-Time Home Buyer Tips Answered Directly

Q: What is the first step in buying a home?

The first step is assessing your financial readiness — specifically your credit score, debt-to-income ratio, and savings. This determines which loan programs you qualify for and how much home you can afford before you ever contact an agent.

Q: How much money do you need to buy your first home?

At minimum, plan for 3.5% down (FHA) plus 2–5% in closing costs, plus inspection fees and moving costs. On a $300,000 home, that's roughly $16,500–$25,500 in cash needed. State assistance programs can reduce this significantly.

Q: What credit score is needed to buy a house?

A 580 credit score qualifies for FHA loans with 3.5% down. A 620+ score opens conventional loan options. A 700+ score typically unlocks the best available rates. The higher your score, the less you pay in interest over the life of the loan.

Q: How long does mortgage pre-approval take?

Most lenders complete pre-approval within 1–3 business days once you submit all required documents. Digital lenders can sometimes turn it around same-day. Pre-approval letters are typically valid for 60–90 days.

Q: Should I use an FHA or conventional loan?

Use FHA if your credit score is below 680 or your down payment is under 5%. Use conventional if your score is 680+ and you can put down at least 5–10%, because you'll likely pay less in mortgage insurance over time.

Q: Is 2026 a good time to buy a first home?

Yes, with caveats. Rising inventory, sellers open to negotiation, and homes sitting on market longer than in recent years create real opportunities. Rates at 6.22% are higher than historical lows but manageable with the right loan structure. NAR's Jessica Lautz notes 2026 could help 1.6 million renters transition to ownership [2].

Q: Can I buy a home with no down payment?

Yes, through VA loans (for eligible veterans) and USDA loans (for qualifying rural/suburban areas). Some state programs also offer down payment grants that effectively reduce your out-of-pocket to near zero.

Q: What is a buyer's agent and do I need one?

A buyer's agent represents your interests in the transaction, negotiates on your behalf, and guides you through the process. In most transactions, their commission is paid by the seller. For a first-time buyer, having a skilled agent is an extraordinary advantage.

Q: What happens if the home appraises below the purchase price?

You have three options: negotiate the price down to the appraised value, pay the difference in cash (appraisal gap), or walk away using your appraisal contingency. This is why including an appraisal contingency in your offer matters.

Q: How do I avoid overpaying for a home?

Review comparable sales (comps) from the past 90 days in the same neighborhood. Price per square foot is a useful benchmark. Your agent should provide a comparative market analysis (CMA) before you make any offer.

Conclusion: Your Action Plan Starts Today

The First-Time Home Buyer Tips: A Real Estate Agent's Full Guide above isn't just information — it's a sequence. Follow it in order and you won't get blindsided by costs, rejected by sellers, or locked into the wrong mortgage.

Your immediate next steps:

- Pull your credit report from all three bureaus this week

- Calculate your DTI and target monthly payment using a home affordability calculator

- Contact 2–3 lenders and begin the pre-approval process

- Research first-time buyer programs in your state

- Interview 2–3 buyer's agents with first-timer experience

- Build your needs vs. wants list before your first showing

- Set a realistic timeline — most buyers take 3–6 months from preparation to closing

The 2026 market is genuinely friendlier to prepared first-time buyers than it's been in several years [2][4]. Inventory is up, sellers are negotiating, and new legislation is making the mortgage process more accessible [9]. The buyers who win are the ones who do the prep work before they fall in love with a listing.

So based on everything in this guide — the financial prep, the mortgage strategy, the neighborhood research — the move is clear: start now, stay disciplined, and let the process work for you.

For ongoing market updates, buyer strategies, and expert real estate education, visit Real Estate Rank IQ or subscribe to the @Realestaterankiq YouTube channel. Questions? Reach out at news@realestaterankiq.com.

References

[1] Steps First Time Buyers Mortgage Ready – https://www.realtor.com/news/trends/steps-first-time-buyers-mortgage-ready/

[2] Could More First Time Buyers Make The Math Work In 2026 – https://www.nar.realtor/magazine/real-estate-news/could-more-first-time-buyers-make-the-math-work-in-2026

[3] 2026 Trigger Lead Legislation – https://firsthome.com/2026-trigger-lead-legislation/

[4] First Time Homebuyer Markets 2026 – https://www.realtor.com/research/first-time-homebuyer-markets-2026/

[5] First Time Home Buyer Tips 2026 What New Buyers Should Know Before Buying A Home – https://blog.themobilebroker.net/2026/03/09/first-time-home-buyer-tips-2026-what-new-buyers-should-know-before-buying-a-home/

[6] Empowering First Time Homebuyers With Data Driven Insights – https://datacalculus.com/en/blog/real-estate-agents-and-brokers/real-estate-marketing-manager/empowering-first-time-homebuyers-with-data-driven-insights

[7] Home Buyer Preparation 2026 – https://themortgagereports.com/125202/home-buyer-preparation-2026

[8] Mortgage Rates Hit 2026 High As Peak Homebuying Season Begins – https://www.realestatenews.com/2026/03/19/mortgage-rates-hit-2026-high-as-peak-homebuying-season-begins

[9] New Executive Orders Aim To Promote Access To Mortgage Credit And Expand Construction Of Affordable Homes – https://www.mayerbrown.com/en/insights/publications/2026/03/new-executive-orders-aim-to-promote-access-to-mortgage-credit-and-expand-construction-of-affordable-homes

[10] 10 Best Markets For First Time Home Buyers In 2026 – https://www.nar.realtor/magazine/real-estate-news/10-best-markets-for-first-time-home-buyers-in-2026

{kind=link}