Picture this: You're scrolling through homes on a Saturday morning, iced coffee in hand, when you notice something extraordinary happening in the mortgage market. Current Mortgage Rates February 2026: 30-Year Fixed at 6.11% – What Buyers Need to Know isn't just another headline—it's a fresh opportunity that could unlock 10-15% more buying power compared to this time last year. After months of rate volatility that had homebuyers playing the waiting game, February 2026 is serving up some seriously based news: rates have stabilized in the low 6% range, and the window for action is wide open.

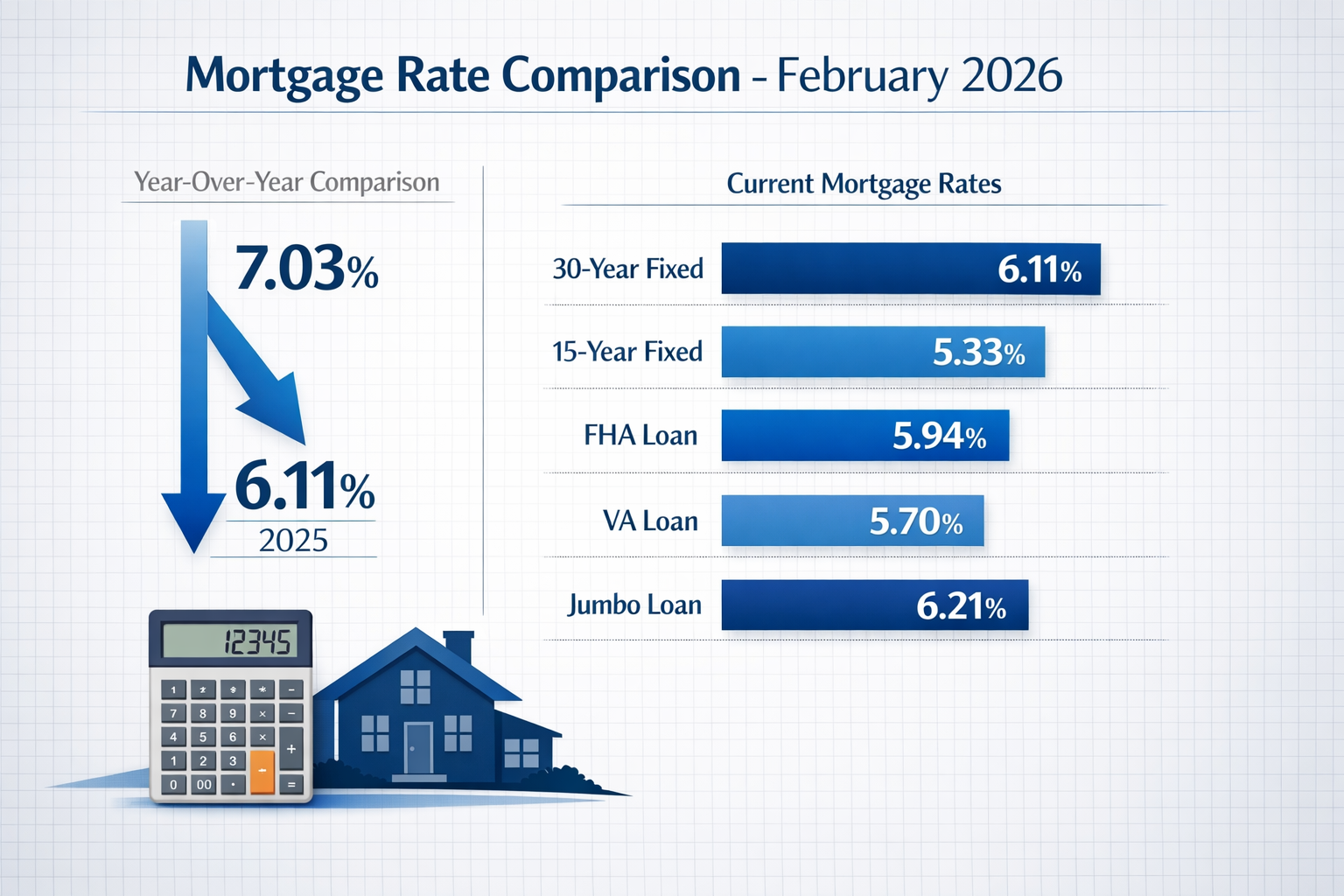

According to Freddie Mac's latest Primary Mortgage Market Survey, the 30-year fixed-rate mortgage averaged 6.11% as of February 5, 2026[7]. Meanwhile, Optimal Blue data shows rates locked at 6.083% as of February 6, 2026[1], while other tracking sources report figures between 6.16% and 6.226%[3][5]. Whether you're a first-time buyer, a real estate investor eyeing your next rental property, or an agent guiding clients through this market, understanding these rate movements is absolutely critical to making smart financial decisions in 2026.

Key Takeaways

- 30-year fixed mortgage rates are averaging between 6.08% and 6.23% in February 2026, with Freddie Mac's official rate at 6.11%[7]

- Year-over-year improvement shows rates have declined approximately 0.87 percentage points from February 2025's 7.03%[5]

- Buying power boost: Current rates provide 10-15% more affordability compared to last year, translating to thousands in savings over the loan term

- FHA and VA loans offer even better rates at 5.94% and 5.70% respectively, making homeownership more accessible for qualified buyers[1][3]

- Rate stability has emerged after months of volatility, with minimal week-to-week fluctuations creating a favorable environment for locking in rates

Understanding Current Mortgage Rates February 2026: 30-Year Fixed at 6.11% – What Buyers Need to Know

Let's break down what's actually happening in the mortgage market right now, because these numbers deserve some serious attention. The 30-year conventional mortgage rate sits at an average of 6.083% according to the most recent Optimal Blue data[1], though you'll see slight variations depending on your source and the exact day you're checking. Freddie Mac, the gold standard for mortgage rate tracking, pegged the rate at 6.11% as of their February 5, 2026 survey[7].

Here's where it gets impeccable: compared to one month ago, when rates averaged 6.138%[1], we're seeing a gentle downward trend. More importantly, when you stack February 2026 against February 2025—when rates were hovering around 7.03%[5]—the improvement is nothing short of extraordinary. That's nearly a full percentage point drop, and in mortgage math, that translates to real money.

Breaking Down the Rate Landscape by Loan Type

Not all mortgages are created equal, and February 2026 is proving that point beautifully. Here's the current snapshot:

| Loan Type | Average Rate | Best For |

|---|---|---|

| 30-Year Conventional | 6.08% – 6.23%[1][5] | Traditional buyers with good credit |

| 15-Year Conventional | 5.33% – 5.57%[1][6] | Buyers wanting faster equity build |

| 30-Year FHA | 5.91% – 5.94%[1][3] | First-time buyers, lower down payments |

| 30-Year VA | 5.70% – 6.30%[1][3] | Veterans and active military |

| 30-Year USDA | 5.96%[1] | Rural property buyers |

| 30-Year Jumbo | 6.21% – 6.39%[1][6] | High-value property purchases |

The standout performer? VA loans are absolutely crushing it at an average of 5.703%[1], offering eligible veterans and service members access to some of the most competitive rates available. FHA loans aren't far behind at 5.941%[1], making them an attractive option for buyers who might not have the traditional 20% down payment or pristine credit scores.

For those considering best mortgage options for Gen Z home buyers, understanding these loan type variations is crucial—especially when you're trying to maximize buying power on a potentially tighter budget.

What These Rates Actually Mean for Your Wallet

Let's talk real numbers, because percentages are just gatekeeping until you see the actual dollar impact. At the current 6.23% average rate, borrowers pay approximately $73.73 per $100,000 borrowed in monthly principal and interest[6].

Here's what that looks like in practice:

- $300,000 loan: ~$1,842/month (principal + interest)

- $400,000 loan: ~$2,456/month (principal + interest)

- $500,000 loan: ~$3,070/month (principal + interest)

Now compare that to February 2025 rates around 7.03%. On a $400,000 loan:

- At 7.03%: ~$2,664/month

- At 6.11%: ~$2,424/month

- Monthly savings: ~$240

- Savings over 30 years: ~$86,400

That's not chump change—that's a new car, college tuition contributions, or serious investment capital. This is exactly why understanding Current Mortgage Rates February 2026: 30-Year Fixed at 6.11% – What Buyers Need to Know matters so much for anyone considering a home purchase this year.

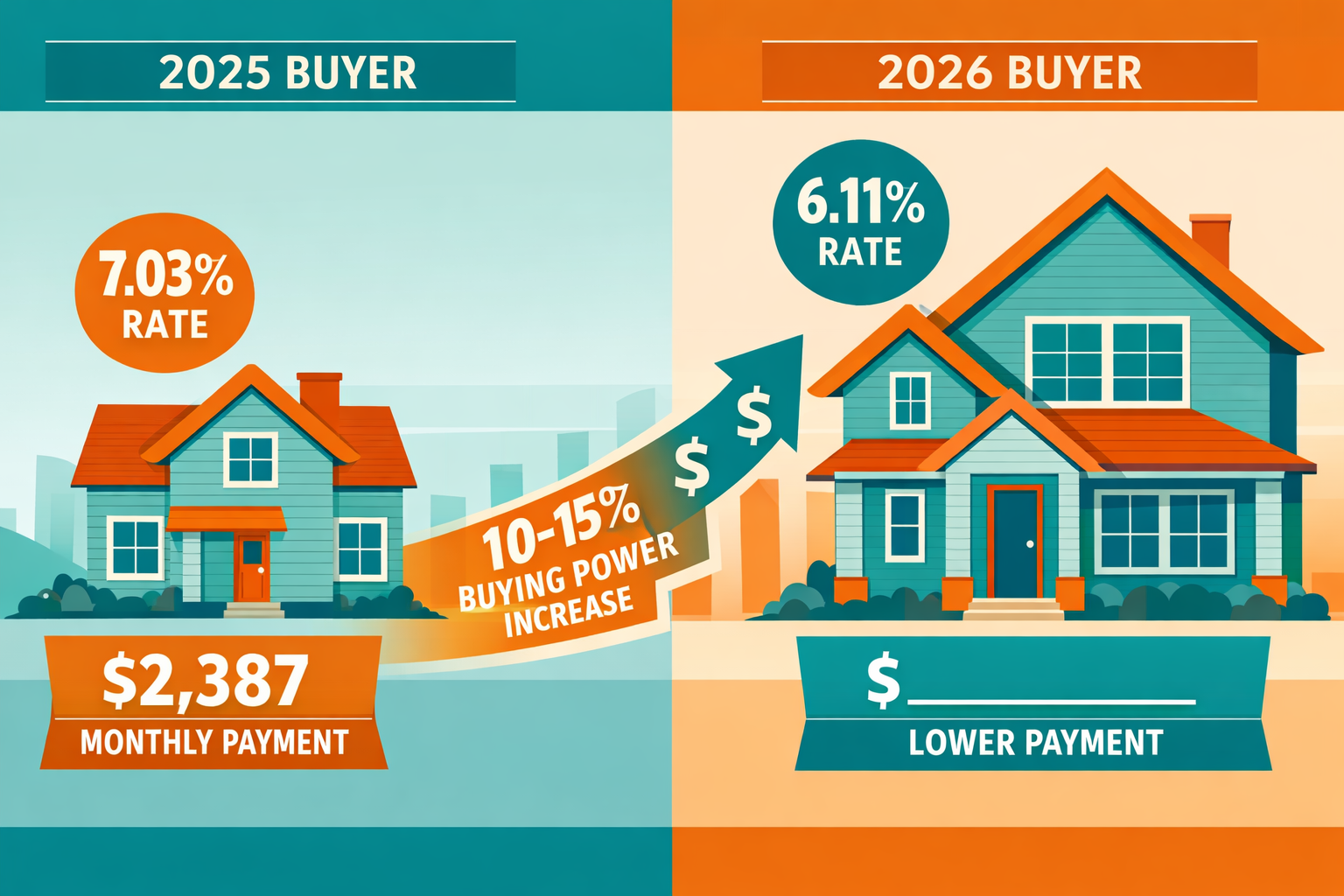

The Year-Over-Year Rate Decline: How Much Buying Power Have You Gained?

Let it cook for a second while we digest just how significant this year-over-year improvement really is. The approximately 0.87 percentage point decline[5] from February 2025 to February 2026 represents one of the most meaningful affordability shifts we've seen in recent years. But what does that actually translate to in terms of buying power?

The Buying Power Calculator

When mortgage rates drop, your purchasing power increases—sometimes dramatically. Here's the math that real estate agents and savvy buyers need to understand:

Scenario: You've budgeted $2,500/month for principal and interest payments.

- At 7.03% (Feb 2025): You could afford approximately a $375,000 loan

- At 6.11% (Feb 2026): You could afford approximately $427,000 loan

- Increased buying power: ~$52,000 or 13.9% more house

This is where the 10-15% buying power boost comes into play. For many buyers, especially those in competitive markets, this could mean the difference between settling for a starter home in a less desirable neighborhood versus landing that dream property with the impeccable kitchen and extra bedroom for a home office.

Regional Variations and Market-Specific Considerations

While national averages provide helpful benchmarks, the reality is that mortgage rates can vary based on several factors:

- Credit score: Higher scores typically unlock better rates

- Down payment size: 20% or more often means better terms

- Location: State and local market conditions influence pricing

- Lender competition: Shopping around can yield 0.25-0.5% differences

- Loan amount: Conforming vs. jumbo loan thresholds matter

For buyers wondering will you rent or buy in 2026, these rate improvements make the buy-versus-rent calculation significantly more favorable than it was just 12 months ago. When you factor in equity building, tax benefits, and the long-term wealth creation potential of homeownership, the scales are tipping decidedly toward buying—especially with rates in the low 6% range.

Refinance Rates: A Different Story

Here's something crucial that often gets overlooked: refinance rates are running higher than purchase rates. The average 30-year fixed-refinance rate sits at 6.57%[6], approximately 0.34-0.46 percentage points above purchase rates.

This spread matters for homeowners considering refinancing. If you locked in a rate below 6% during the pandemic-era lows (2020-2021), refinancing at today's rates probably doesn't make financial sense. However, if you purchased or refinanced in 2023-2024 when rates were in the 7-8% range, now might be an extraordinary opportunity to shave significant interest off your monthly payment.

Strategic Timing: Should You Lock Your Rate Now or Wait?

This is the million-dollar question keeping buyers up at night, and honestly, it's so based that we're even in a position to ask it. After years of watching rates climb, the stability we're seeing in February 2026 is refreshing. But should you pull the trigger now, or is there potential for rates to drop even further?

Recent Rate Movements and Trends

Looking at the weekly fluctuations, rates have remained remarkably stable. Over the past week, movements have been minimal—some sources reporting slight increases of just 0.01 to 0.07 percentage points[5][6]. This kind of stability is actually a positive signal for buyers who've been sitting on the sidelines.

The one-month trend shows rates declining slightly from 6.138% to 6.083%[1], a modest but encouraging movement. However, mortgage rates are influenced by complex factors including:

- Federal Reserve policy decisions

- Inflation data and economic indicators

- Treasury bond yields (particularly the 10-year note)

- Global economic conditions

- Housing market supply and demand

The Rate Lock Strategy

Here's the professional advice from licensed brokers with over 15 years of experience: If you've found the right property and the numbers work at current rates, lock it in. Here's why:

✅ Reasons to Lock Now:

- Rates are significantly better than 2025

- Minimal week-to-week volatility suggests stability

- You've found a property that meets your needs

- Your budget works at current rates

- You can always refinance later if rates drop further

⚠️ Reasons to Wait:

- You're still house hunting and not ready to commit

- Economic indicators suggest potential Fed rate cuts ahead

- Your financial situation is improving (credit score, down payment)

- You're in a buyer's market with negotiating leverage

The reality is that trying to time the mortgage market perfectly is like trying to time the stock market—nearly impossible and often counterproductive. A difference of 0.25% on your rate matters far less than finding the right property at the right price.

Understanding Rate Lock Periods

When you do decide to lock, understanding the mechanics is crucial:

- 30-day lock: Standard for most transactions, best for quick closings

- 45-day lock: More common, provides buffer for typical closing timeline

- 60-day lock: Recommended for new construction or complex transactions

- Extended locks: Available but often come with fees

Most lenders offer float-down options for a fee, allowing you to capture a lower rate if markets improve during your lock period. This can be a smart middle-ground strategy if you're concerned about missing out on potential rate drops.

For buyers exploring their options, reviewing a comprehensive guide to types of mortgage loans and comparing lenders in 2026 can help you understand which products offer the best rate lock flexibility and terms for your specific situation.

How Current Rates Impact Different Buyer Segments

The beauty of the current rate environment is that it's creating opportunities across multiple buyer segments. Let's break down how Current Mortgage Rates February 2026: 30-Year Fixed at 6.11% – What Buyers Need to Know affects different groups in the market.

First-Time Homebuyers

For first-timers, the combination of FHA loans at 5.94%[1] and improved buying power creates a fresh entry point into homeownership. The lower down payment requirements (as little as 3.5% for FHA) combined with competitive rates mean that the monthly payment hurdle—often the biggest obstacle for first-time buyers—is more manageable than it was in 2025.

Key advantages:

- Lower monthly payments compared to 2025 renting in many markets

- Equity building from day one

- Tax deductions for mortgage interest

- Predictable housing costs (unlike rent increases)

The challenge remains inventory shortage in many markets, but with rates stabilizing, more sellers may feel confident listing their homes, knowing they can afford to buy their next property without facing dramatically higher rates.

Real Estate Investors

For investors, the current rate environment is creating interesting opportunities, particularly in the rental market. At 6.08-6.23% for conventional loans[1][5], the math on rental properties is starting to make sense again for cash-flow focused strategies.

Investment considerations:

- Rental demand remains strong in markets where home prices are elevated

- Cash-on-cash returns improve with lower rates

- Refinancing existing properties purchased at 7%+ rates can boost profitability

- 1031 exchanges become more attractive with better financing terms

Investors should explore real estate investment strategies to understand how current rates affect different approaches—from fix-and-flip to buy-and-hold rental portfolios.

Move-Up Buyers and Downsizers

This segment faces unique considerations. Many current homeowners locked in rates below 4% during 2020-2021, creating rate lock-in syndrome—the reluctance to sell because moving would mean accepting a higher rate.

However, the year-over-year rate improvement is gradually easing this concern:

For move-up buyers:

- Growing families needing more space may find the rate trade-off worthwhile

- Job relocations become more feasible

- Lifestyle changes (remote work, retirement) are less financially punishing

For downsizers:

- Empty nesters can right-size without astronomical rate penalties

- Equity from current homes can offset higher rates on smaller mortgages

- Lower maintenance costs and property taxes may offset slightly higher mortgage rates

Veterans and Active Military

With VA loan rates at 5.70%[1], eligible veterans and active-duty service members are enjoying some of the most competitive financing available in February 2026. The combination of:

- No down payment requirement

- No private mortgage insurance (PMI)

- Below-market interest rates

- Flexible credit requirements

…makes VA loans an extraordinary benefit that's even more valuable in the current rate environment. For eligible buyers, this could represent thousands in savings compared to conventional financing.

The Refinance Opportunity: Who Should Consider It?

While purchase rates are grabbing headlines, the refinance market deserves attention too. With refinance rates at 6.57%[6], there's a specific window of opportunity for certain homeowners.

The Refinance Sweet Spot

You should strongly consider refinancing if:

✅ Your current rate is 7.0% or higher

✅ You plan to stay in your home for at least 2-3 more years

✅ You have sufficient equity (typically 20%+ to avoid PMI)

✅ Your credit score has improved since your original loan

✅ You can recoup closing costs through monthly savings within 24-36 months

Example refinance scenario:

- Current loan: $400,000 at 7.5% = $2,797/month

- Refinance to: $400,000 at 6.57% = $2,545/month

- Monthly savings: $252

- Annual savings: $3,024

- 30-year savings: $90,720

Even with closing costs of $5,000-$8,000, the break-even point would be just 20-32 months, making this a smart financial move for homeowners planning to stay put.

Cash-Out Refinance Considerations

With home equity at near-record levels for many homeowners, cash-out refinancing is worth exploring for:

- Home renovations that add value

- Debt consolidation (replacing high-interest credit cards)

- Investment opportunities (rental property down payments)

- Education funding

However, be strategic: tapping equity to fund depreciating assets or lifestyle expenses rarely makes financial sense. The best use of cash-out refinances involves investing in appreciating assets or eliminating higher-interest debt.

For homeowners considering renovations, checking out expert tips for preparing your home to attract buyers can help ensure your renovation investments actually add value.

Economic Factors Influencing February 2026 Rates

Understanding the "why" behind current rates helps predict where they might head next. Several key economic factors are shaping the mortgage landscape in February 2026:

Federal Reserve Policy

The Federal Reserve's decisions on the federal funds rate don't directly set mortgage rates, but they heavily influence them. While the Fed controls short-term rates, mortgage rates typically track the 10-year Treasury yield, which responds to:

- Inflation expectations

- Economic growth projections

- Fed policy signals and communications

- Global economic conditions

In early 2026, the Fed has maintained a relatively stable policy stance, contributing to the rate stability we're seeing.

Inflation Trends

Inflation data remains the Fed's primary concern. When inflation runs hot, the Fed typically raises rates to cool the economy, which indirectly pushes mortgage rates higher. Conversely, cooling inflation creates room for rate stability or decreases.

February 2026's rate environment suggests inflation has moderated sufficiently to allow for the current rate levels without triggering additional Fed tightening.

Housing Market Dynamics

Supply and demand in the housing market itself influences mortgage rates:

- Low inventory can keep home prices elevated, affecting affordability

- Increased inventory can ease price pressure, making homes more accessible

- Builder activity affects new home supply and market balance

The current market shows signs of inventory improvement in many regions, which combined with better rates, is creating more balanced conditions than we saw in 2024-2025.

Global Economic Factors

Mortgage rates don't exist in a vacuum. Global economic conditions including:

- International conflicts and geopolitical tensions

- European and Asian economic performance

- Currency exchange rates

- Global investment flows

…all influence U.S. Treasury yields and, by extension, mortgage rates. The relative stability of global markets in early 2026 is contributing to the favorable rate environment.

Practical Steps to Secure the Best Rate in February 2026

Knowledge is power, but action is what actually gets you into a home at a great rate. Here's your step-by-step playbook for securing the best possible mortgage rate in the current environment.

Step 1: Check and Optimize Your Credit Score

Your credit score is the single most influential factor in the rate you'll be offered. Here's the typical rate impact:

- 760+ credit score: Best available rates

- 700-759: Good rates, typically 0.25-0.5% higher than best

- 660-699: Fair rates, 0.5-1.0% higher than best

- 620-659: Subprime rates, 1.0-2.0% higher than best

Action items:

- Pull your credit reports from all three bureaus (free at AnnualCreditReport.com)

- Dispute any errors or inaccuracies

- Pay down credit card balances below 30% utilization

- Avoid opening new credit accounts before applying

- Don't close old accounts (credit history length matters)

Even a 20-point credit score improvement can translate to thousands in savings over your loan term.

Step 2: Shop Multiple Lenders

This is where many buyers leave money on the table. Rate shopping can yield differences of 0.25-0.75% between lenders, which on a $400,000 loan could mean:

- 0.25% difference: ~$60/month or $21,600 over 30 years

- 0.50% difference: ~$120/month or $43,200 over 30 years

- 0.75% difference: ~$180/month or $64,800 over 30 years

Compare at least 3-5 lenders:

- Traditional banks

- Credit unions (often offer competitive rates for members)

- Online lenders (lower overhead can mean better rates)

- Mortgage brokers (access to multiple lenders)

Pro tip: Submit all rate inquiries within a 14-day window—credit bureaus count multiple mortgage inquiries as a single pull when done in this timeframe, protecting your credit score.

For a comprehensive comparison approach, check out the best home buying sites in the U.S. for 2026 which includes lender comparison tools.

Step 3: Consider Discount Points

Mortgage points (also called discount points) allow you to "buy down" your interest rate by paying upfront fees. Typically:

- 1 point = 1% of loan amount = ~0.25% rate reduction

- On a $400,000 loan: $4,000 = ~0.25% lower rate

When points make sense:

- You plan to stay in the home 5+ years

- You have extra cash for closing costs

- The monthly savings justify the upfront cost

Break-even calculation:

- Cost of points: $4,000

- Monthly savings from lower rate: $60

- Break-even: 67 months (5.6 years)

If you plan to stay longer than the break-even period, points can be a smart investment.

Step 4: Maximize Your Down Payment

While low down payment options exist (FHA 3.5%, conventional 3%), a larger down payment can:

- Eliminate PMI (at 20% down on conventional loans)

- Qualify you for better rates

- Lower your monthly payment

- Reduce total interest paid

- Strengthen your offer in competitive markets

Down payment strategies:

- First-time buyer programs and grants

- Gift funds from family members

- IRA withdrawals (up to $10,000 penalty-free for first-time buyers)

- Down payment assistance programs (state and local)

For detailed strategies, explore top down payment strategies ranked to find the approach that works best for your situation.

Step 5: Get Pre-Approved (Not Just Pre-Qualified)

There's a huge difference:

Pre-qualification: Informal estimate based on self-reported information

Pre-approval: Formal commitment based on verified income, assets, and credit

Pre-approval advantages:

- Shows sellers you're a serious buyer

- Identifies potential issues before you find a home

- Speeds up the closing process

- Provides accurate budget parameters

- Strengthens negotiating position

In competitive markets, pre-approval isn't optional—it's essential. Many sellers won't even consider offers without it.

Step 6: Time Your Application Strategically

Rate lock timing matters. Consider:

- Market trends: Are rates trending up or down?

- Economic calendar: Major Fed announcements, jobs reports, inflation data

- Personal timeline: How quickly can you close?

- Property type: New construction needs longer locks

Best practices:

- Lock when you have a signed purchase agreement

- Choose a lock period that exceeds your expected closing timeline by 7-10 days

- Understand lock extension fees in case of delays

- Ask about float-down options

What Real Estate Professionals Need to Know

For real estate agents and brokers, understanding Current Mortgage Rates February 2026: 30-Year Fixed at 6.11% – What Buyers Need to Know isn't just about staying informed—it's about providing extraordinary value to clients and closing more deals.

Educating Clients on Affordability

The year-over-year rate improvement is a powerful selling point that many buyers don't fully appreciate. Frame it correctly:

❌ "Rates are still higher than they were in 2021"

✅ "Rates have dropped nearly a full point from last year, giving you 10-15% more buying power"

Client education tools:

- Mortgage calculators showing payment differences

- Year-over-year comparison charts

- Total interest savings over loan term

- Buying power increase demonstrations

Overcoming Rate Lock-In Objections

Many potential sellers remain hesitant due to their low existing rates. Address this directly:

Talking points:

- Equity gains may outweigh rate differences

- Life changes (family size, location, retirement) have value beyond rates

- Can always refinance if rates drop further

- Renting out current home is an option for some

- Opportunity cost of staying in wrong-size home

Positioning Properties in the Current Market

With improved affordability, marketing strategies should emphasize:

- Monthly payment affordability (not just price)

- Move-in ready condition (buyers want to avoid renovation costs)

- Energy efficiency (lower utility costs offset higher rates)

- Income potential (for investors)

- Lifestyle benefits that justify the move

For agents looking to enhance their marketing game, explore social media and neighborhood marketing strategies that resonate in the current environment.

Building Your Lender Network

Strong lender relationships are crucial for agent success:

- Maintain relationships with 3-5 reliable lenders

- Understand each lender's strengths (first-time buyers, investors, jumbo loans)

- Provide clients with multiple options

- Ensure lenders can close on time

- Get pre-approval letters quickly for competitive offers

The ability to connect clients with lenders who can deliver competitive rates and reliable service is a differentiator that builds your reputation and referral business.

Looking Ahead: Rate Predictions for the Rest of 2026

While no one has a crystal ball, several indicators suggest where rates might head in the coming months:

Factors That Could Push Rates Lower

Positive scenarios:

- Continued inflation moderation

- Fed rate cuts (if economic data supports)

- Increased housing inventory reducing price pressure

- Global economic stability

- Strong Treasury demand

Factors That Could Push Rates Higher

Risk scenarios:

- Inflation resurgence

- Geopolitical tensions escalating

- Strong economic growth triggering Fed hawkishness

- Increased government borrowing

- Labor market remaining too hot

Most Likely Scenario

Based on current economic indicators and expert consensus, the most probable path for 2026 rates is:

📊 Base case projection:

- Rates remain in the 5.75-6.50% range through mid-2026

- Gradual decline to 5.50-6.00% by year-end

- Continued stability with minimal week-to-week volatility

This suggests that while we may see modest improvements, the dramatic rate drops some buyers are hoping for are unlikely without significant economic disruption.

Bottom line for buyers: If you find the right property and the numbers work at current rates, waiting for dramatically lower rates is a risky bet that could cost you the perfect home.

Conclusion: Taking Action in the February 2026 Market

The mortgage rate landscape in February 2026 is offering something we haven't seen in years: stability combined with meaningful improvement. With 30-year fixed rates averaging 6.11%[7] and year-over-year declines providing 10-15% more buying power, the conditions for homeownership are the most favorable they've been since early 2023.

Current Mortgage Rates February 2026: 30-Year Fixed at 6.11% – What Buyers Need to Know boils down to this: opportunity is knocking, but it won't wait forever. The combination of stabilized rates, improved affordability, and gradually increasing inventory creates a window that savvy buyers and investors should seriously consider.

Your Action Plan

If you're a buyer:

- Get your finances in order (check credit, save for down payment, reduce debt)

- Get pre-approved with multiple lenders to find the best rate

- Start your home search with realistic expectations about inventory

- Work with an experienced agent who understands the current market

- Lock your rate when you find the right property—don't try to time perfection

If you're a homeowner considering refinancing:

- Calculate your break-even point on refinancing costs

- Shop multiple lenders for the best refinance rates

- Consider your timeline (staying in home vs. selling soon)

- Evaluate cash-out options if you have equity and strategic uses for funds

If you're a real estate professional:

- Educate clients on year-over-year rate improvements

- Build strong lender partnerships to provide competitive financing options

- Frame affordability in terms of monthly payments and buying power

- Address rate lock-in concerns with data and alternative solutions

- Stay informed on weekly rate movements and economic indicators

The fresh perspective on Current Mortgage Rates February 2026: 30-Year Fixed at 6.11% – What Buyers Need to Know is that we're in a fundamentally different market than we were just 12 months ago. The impeccable timing of this rate environment—combined with demographic demand from millennials and Gen Z entering peak homebuying years—creates conditions that favor action over waiting.

Real estate has always been about timing, location, and financial preparation. In February 2026, the timing piece is aligning in favor of buyers who are ready to move. Whether you're purchasing your first home, upgrading to accommodate a growing family, or building your investment portfolio, the rates available today provide a solid foundation for long-term wealth building through real estate.

Don't let analysis paralysis or waiting for the "perfect" rate keep you from achieving your real estate goals. The best time to buy is when you find the right property, can afford the payment, and are ready for homeownership—and for many buyers in February 2026, all three conditions are finally aligning.

For more expert guidance on navigating the 2026 real estate market, explore Real Estate Rank IQ's comprehensive resources on mastering the 2025 housing market and stay informed with weekly market updates at realestaterankiq.com.

References

[1] Current Mortgage Rates 02 10 2026 – https://fortune.com/article/current-mortgage-rates-02-10-2026/

[2] Mortgage Rates For Thursday February 5 2026 – https://www.bankrate.com/mortgages/todays-rates/mortgage-rates-for-thursday-february-5-2026/

[3] 30 Year Mortgage Rates – https://themortgagereports.com/30-year-mortgage-rates

[4] Todays Mortgage Interest Rates February 9 2026 – https://www.cbsnews.com/news/todays-mortgage-interest-rates-february-9-2026/

[5] 30 Year Fixed – https://www.mortgagenewsdaily.com/mortgage-rates/30-year-fixed

[6] Mortgage Rates For Monday February 9 2026 – https://www.bankrate.com/mortgages/todays-rates/mortgage-rates-for-monday-february-9-2026/

[7] Pmms – https://www.freddiemac.com/pmms

[8] Mortgage30us – https://fred.stlouisfed.org/series/MORTGAGE30US

{kind=link}