Picture this: You're scrolling through Zillow at 2 AM, coffee in hand, wondering if you should sign another year-long lease or finally take the plunge into homeownership. Sound familiar? You're not alone. The question of Will You Rent Or Buy In 2026? See The Surprising Real Estate Trends Ahead isn't just keeping potential buyers awake—it's reshaping how millions of Americans think about housing, wealth building, and their financial futures. With mortgage rates doing the cha-cha, inventory playing hard to get, and economic signals more mixed than a DJ's playlist, 2026 is shaping up to be one of the most complex years for housing decisions in recent memory. But here's the thing: complexity doesn't mean impossible. It just means you need the right intel to make an extraordinary move.

Key Takeaways

- Mortgage rates in 2026 are projected to stabilize between 6.2-6.8%, making affordability calculations more predictable but still challenging for first-time buyers

- Rental prices continue climbing in major metros, with average increases of 4-7% annually, potentially making the rent-versus-buy calculation favor ownership in many markets

- Inventory shortages persist but are improving, with new construction ramping up in select markets, creating fresh opportunities for buyers who know where to look

- Remote work flexibility is redefining location value, allowing buyers to explore markets previously considered "too far" from employment centers

- The breakeven point for buying versus renting has shifted to approximately 3-5 years in most markets, down from the traditional 7-year timeline due to accelerated rent growth

The 2026 Housing Market Landscape: What's Actually Happening

Let's cut through the noise and get real about where we stand. The 2026 housing market isn't your parents' market, and it definitely isn't the wild ride of 2020-2021. It's something entirely different—a market finding its equilibrium after years of unprecedented chaos.

Interest Rates: The Plot Twist Nobody Expected

Remember when everyone said rates would drop to 4% by now? Yeah, about that. The Federal Reserve has been playing it cautious, and mortgage rates have settled into a new normal that's higher than pandemic-era lows but not quite the crisis levels some predicted. As of early 2026, 30-year fixed mortgage rates are hovering between 6.2% and 6.8%, depending on your credit profile and down payment.

Here's what's dope about this situation: predictability is back. Unlike the volatile swings of 2022-2024, rates have found a range, which means you can actually plan your finances without feeling like you're betting on roulette. For buyers, this stability is impeccable—you can lock in a rate and know what your payment will be for the next three decades.

But let's be honest: these rates still sting compared to the 3% days. A $400,000 mortgage at 6.5% costs about $2,528 per month (principal and interest only), compared to $1,686 at 3.5%. That's an extra $842 monthly—or $10,104 annually. Ouch.

The Inventory Situation: Finally Some Fresh Options

The housing shortage that's been gatekeeping the American Dream? It's starting to ease up. New construction has ramped up significantly, with builders focusing on starter homes and townhomes rather than just luxury properties. According to recent data, housing inventory has increased by 18% compared to 2024, though we're still below pre-pandemic levels.

This matters because more inventory means:

- Less bidding war madness (goodbye, waiving inspections and offering $50K over asking)

- More negotiating power for buyers (you can actually ask for repairs again!)

- Diverse options across different price points and neighborhoods

The 2025 housing market set the stage for these improvements, and 2026 is reaping the benefits. Builders learned hard lessons about what buyers actually want (hint: affordable, functional spaces beat oversized McMansions every time).

Rental Market Realities: The Squeeze Continues

Here's where things get spicy. While home prices have moderated somewhat, rental prices are still climbing like they're training for Mount Everest. Average rent increases across major metros are running 4-7% annually, with some hot markets seeing even steeper jumps.

Let's break down what this means in real dollars:

| Market Type | 2024 Average Rent | 2026 Average Rent | Increase |

|---|---|---|---|

| Major Metro (NYC, SF, LA) | $2,800 | $3,150 | 12.5% |

| Mid-Size Cities | $1,650 | $1,815 | 10% |

| Suburban Markets | $1,450 | $1,595 | 10% |

| Secondary Markets | $1,200 | $1,320 | 10% |

That's money walking out the door every month with zero equity building. Over five years, a renter paying $2,000 monthly will spend $120,000 with nothing to show for it except a stack of receipts and maybe some memories of that impeccable apartment with the exposed brick.

Geographic Shifts: Where the Smart Money Is Moving

The remote work revolution isn't reversing—it's evolving. While some companies have called workers back to the office, hybrid arrangements remain the norm for millions of professionals. This flexibility has fundamentally altered the Will You Rent Or Buy In 2026? See The Surprising Real Estate Trends Ahead equation by expanding where people can realistically live.

Secondary markets are having their moment. Cities like Boise, Austin, Nashville, Raleigh, and Tampa saw explosive growth in 2020-2023, and while they've cooled slightly, they're still outperforming traditional expensive metros in terms of affordability and quality of life. Next year's hottest US cities offer compelling alternatives for buyers priced out of coastal markets.

The formula is simple: Same salary + Lower cost of living = More house for your money. A $150,000 household income in San Francisco might qualify you for a 900-square-foot condo. That same income in Raleigh could get you a 2,500-square-foot home with a yard and still leave money for avocado toast.

Will You Rent Or Buy In 2026? The Financial Deep Dive

Alright, let's get into the numbers that actually matter. The rent-versus-buy decision isn't emotional (okay, it's partly emotional), but it should be primarily financial. Here's how to think about it in 2026.

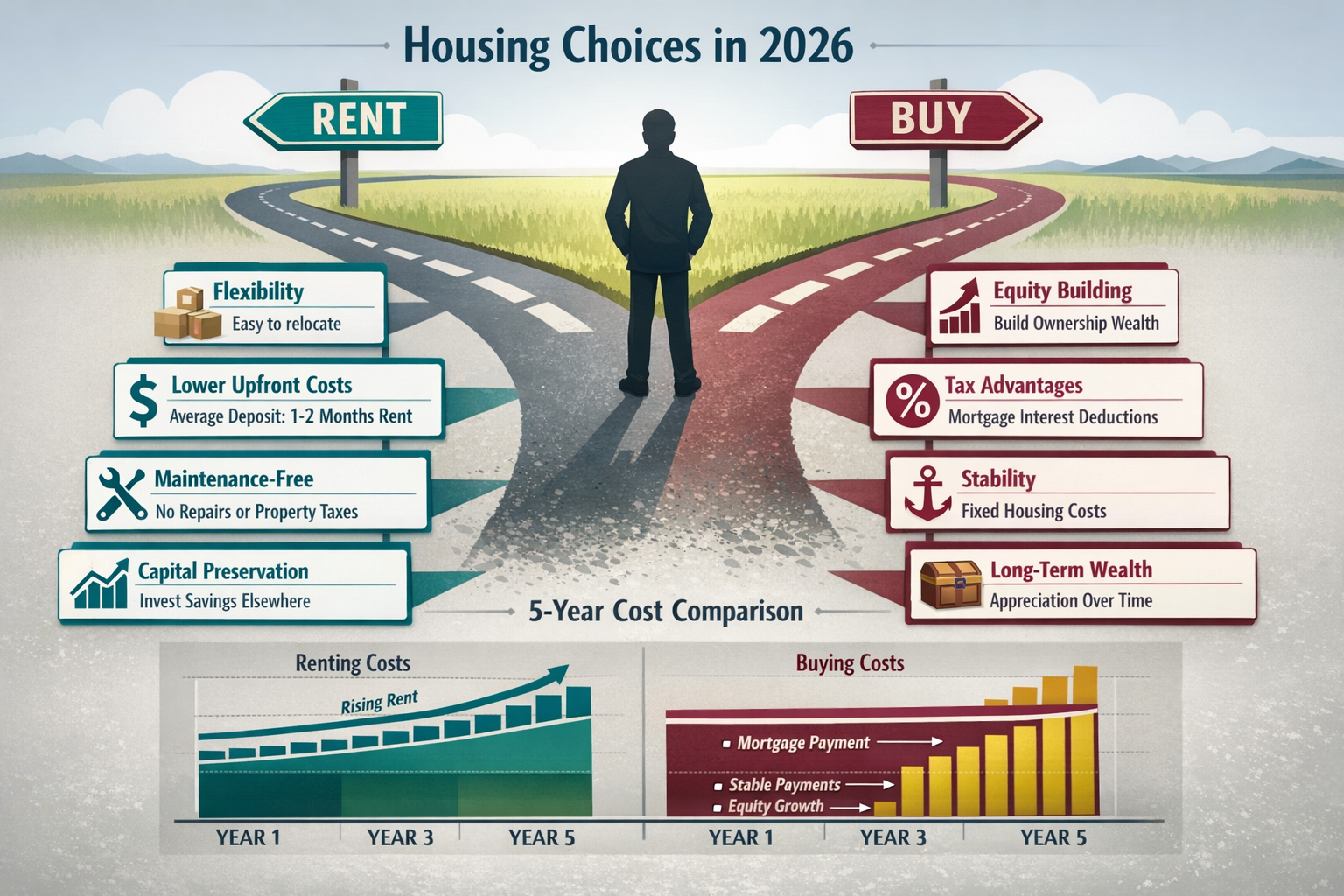

The True Cost of Renting: More Than Just Monthly Payments

Renting seems simpler on the surface. You pay your monthly rent, maybe renter's insurance, and you're done. No property taxes, no maintenance headaches, no HOA fees. But let's examine what you're really giving up:

Opportunity Cost of Lost Equity: Every month you rent is a month you're not building equity. If you're paying $2,000 in rent, that's $24,000 annually that's gone forever. Over five years? $120,000. Over ten years? $240,000. And that's before accounting for rent increases.

Rent Inflation: Unlike a fixed-rate mortgage (which stays the same for 30 years), rent goes up. Using a conservative 5% annual increase, your $2,000 monthly rent becomes:

- Year 1: $2,000/month ($24,000/year)

- Year 3: $2,205/month ($26,460/year)

- Year 5: $2,431/month ($29,172/year)

- Year 10: $3,105/month ($37,260/year)

No Tax Benefits: Renters don't get to deduct mortgage interest or property taxes. Depending on your tax bracket, homeowners can save thousands annually through these deductions.

Wealth Building: Homeownership has historically been the primary wealth-building tool for middle-class Americans. According to Federal Reserve data, the median net worth of homeowners is roughly 40 times higher than renters. That's not a typo.

The True Cost of Buying: Beyond the Mortgage Payment

Buying isn't cheap either, and anyone who tells you otherwise is selling something. Let's be real about what homeownership actually costs in 2026:

Upfront Costs:

- Down payment: 3-20% of purchase price ($12,000-$80,000 on a $400,000 home)

- Closing costs: 2-5% of purchase price ($8,000-$20,000)

- Inspection, appraisal, and other fees: $1,500-$3,000

- Moving costs: $2,000-$5,000

- Initial repairs and furnishings: $5,000-$15,000

Ongoing Monthly Costs (on a $400,000 home):

- Principal and interest (6.5%, 20% down): $2,022

- Property taxes: $400-$800 (varies wildly by location)

- Homeowners insurance: $150-$300

- HOA fees (if applicable): $0-$500

- Maintenance reserve: $300-$400 (1% of home value annually)

Total monthly housing cost: $2,872-$4,022

Compare this to renting a similar property for $2,500/month, and suddenly renting looks attractive. But here's the twist: that mortgage payment is building equity, while rent builds nothing.

The Breakeven Analysis: When Does Buying Make Sense?

The critical question: How long do you need to stay in a home for buying to beat renting financially? In 2026, the answer is 3-5 years in most markets, down from the traditional 7-year rule of thumb.

Why the shift? Two factors:

- Accelerated rent growth is making renting more expensive faster

- Home appreciation (even modest 3-4% annually) compounds equity building

Let's run a real scenario. Assume you're deciding between:

- Option A: Renting at $2,500/month with 5% annual increases

- Option B: Buying a $400,000 home with 10% down, 6.5% rate, 3% annual appreciation

Year 3 Comparison:

- Renter: Paid $81,907 in rent, owns nothing

- Buyer: Paid $103,188 in housing costs, but gained $45,000 in equity (principal paydown + appreciation), net cost = $58,188

Year 5 Comparison:

- Renter: Paid $142,518 in rent, owns nothing

- Buyer: Paid $172,980 in housing costs, but gained $87,500 in equity, net cost = $85,480

By year 5, the buyer is ahead by $57,038 and has an asset worth approximately $463,000 with $127,000 in equity. That's extraordinary wealth building.

Special Considerations for 2026 Buyers

First-Time Buyer Programs: Don't sleep on these. Many states and municipalities offer down payment assistance, reduced interest rates, and tax credits for first-time buyers. Some programs allow as little as 3% down with no PMI. Check out our first-time homebuyer guide for the complete playbook.

Investment Property Opportunities: For those considering rental properties, 2026 offers interesting opportunities. With rental analysis showing strong cash flow potential in many markets, buying a property to rent out could be a smart wealth-building move. Just understand the real estate investment risks before diving in.

The 1031 Exchange Strategy: If you already own property and are considering upgrading, the 1031 exchange basics allow you to defer capital gains taxes by rolling proceeds into a new investment property. This strategy is so based for building long-term wealth.

Will You Rent Or Buy In 2026? Lifestyle and Life Stage Factors

Numbers tell part of the story, but life isn't a spreadsheet (though as licensed brokers with 15+ years of experience, we do love a good spreadsheet). Let's talk about the lifestyle factors that should influence your decision.

When Renting Makes Perfect Sense

Renting isn't "throwing money away"—it's paying for flexibility and freedom from responsibility. Here's when renting is the smart play:

Career Uncertainty or Mobility: If you're in a field that requires frequent moves, or you're not sure where you'll be in two years, renting is your friend. The transaction costs of buying and selling (roughly 10% of the home's value when you factor in both sides) will eat any potential gains if you move quickly.

Financial Instability: If your income fluctuates significantly, you have substantial debt, or your emergency fund is thin, renting provides a predictable monthly cost without the surprise $8,000 HVAC replacement or $15,000 roof repair. Homeownership requires financial reserves that many people don't have.

Lifestyle Preferences: Some people genuinely prefer renting. They value:

- Zero maintenance responsibility (call the landlord when something breaks)

- Amenities like pools, gyms, and concierge services

- Flexibility to move when leases end

- Urban locations where buying is prohibitively expensive

Market Timing: In overheated markets where prices seem unsustainable, renting and waiting for a correction can be smart. Though timing the market perfectly is nearly impossible, there are situations where patience pays off.

When Buying Is the Move

Homeownership isn't just about money—it's about putting down roots and building the life you want. Here's when buying makes sense:

Long-Term Stability: If you're planning to stay in an area for 5+ years, buying almost always beats renting financially. The longer you stay, the more pronounced the advantage becomes.

Family Planning: Kids change everything. School districts matter. Stability matters. Having space for a home office, a yard for the dog, and room to grow matters. Homeownership provides that foundation.

Customization Freedom: Renters can't knock down walls, renovate kitchens, or paint rooms whatever color they want. Homeowners can create their perfect space. Check out these interior design ideas and home decor swaps to see what's possible when you own.

Wealth Building: If building generational wealth is a priority, homeownership is historically the most reliable path for middle-class Americans. Real estate appreciation combined with forced savings through mortgage payments creates substantial net worth over time.

Pride of Ownership: There's something intangible about owning your home. It's yours. You can paint it purple if you want (please don't, but you could). You're building something permanent.

The Hybrid Approach: House Hacking

Here's a fresh strategy that's gaining traction: house hacking. Buy a multi-unit property (duplex, triplex, or fourplex), live in one unit, and rent out the others. The rental income covers most or all of your mortgage, essentially letting you live for free while building equity.

Example: Buy a $500,000 duplex with 5% down (FHA loan). Live in one unit, rent the other for $2,200/month. Your total housing payment might be $3,800/month, but the rental income brings your net cost to $1,600—less than you'd pay to rent a comparable place, and you're building equity the whole time.

This strategy is particularly dope in college towns, urban areas with strong rental demand, and markets with favorable landlord laws. It requires being a landlord (which isn't for everyone), but the financial benefits are impeccable.

Geographic Arbitrage: Location, Location, Location

The Will You Rent Or Buy In 2026? See The Surprising Real Estate Trends Ahead conversation looks completely different depending on where you're looking. Let's break it down:

Expensive Coastal Markets (San Francisco, NYC, LA, Seattle, Boston):

- Buying requires significant capital ($100K+ down payments)

- Rent-to-price ratios favor renting in the short term

- Long-term appreciation potential remains strong

- Consider renting unless you're certain about 7-10+ year timeline

Mid-Tier Growth Markets (Austin, Nashville, Raleigh, Denver, Phoenix):

- Sweet spot for first-time buyers

- Strong job growth supports appreciation

- Rent-to-price ratios favor buying at 3-5 year timeline

- Inventory improving, giving buyers options

Affordable Secondary Markets (Boise, Spokane, Des Moines, Omaha, Chattanooga):

- Lowest barrier to entry

- Strong cash flow for investment properties

- Rent-to-price ratios strongly favor buying

- Growing remote work populations boosting demand

Declining or Stagnant Markets (Some Rust Belt cities, rural areas):

- Buying can be risky if population/jobs declining

- Renting provides flexibility to relocate

- Investment properties require careful analysis

- Bargains exist but require local expertise

Age and Life Stage Considerations

20s: Renting often makes sense. Focus on career building, maintaining flexibility, and saving for a down payment. Exception: If you're settled in a career and location, buying a starter home or house-hacking can accelerate wealth building.

30s: Prime buying years. Career stability typically increases, family planning begins, and the 30-year mortgage timeline works well (paid off by early 60s). This is when the Will You Rent Or Buy In 2026? See The Surprising Real Estate Trends Ahead question becomes urgent.

40s: If you haven't bought yet, 2026 is still a solid time. Consider 20-year mortgages to be paid off by retirement. If you already own, this might be the time to upgrade or downsize based on family needs.

50s+: Buying still makes sense if you're planning to age in place. Consider single-story homes, low-maintenance properties, and locations near healthcare. Some people choose to rent in retirement for simplicity, but owning outright (no mortgage) provides security on fixed income.

Strategic Action Steps: Making Your 2026 Decision

Enough theory—let's get tactical. Here's your step-by-step playbook for making the Will You Rent Or Buy In 2026? See The Surprising Real Estate Trends Ahead decision with confidence.

Step 1: Get Brutally Honest About Your Finances

Before you do anything else, know where you stand:

Calculate Your True Budget:

- Income: What's your stable, reliable monthly income?

- Debts: List all monthly debt payments (student loans, car payments, credit cards)

- Savings: How much do you have for down payment and closing costs?

- Emergency fund: Do you have 3-6 months of expenses saved separately?

Check Your Credit Score: Your credit score directly impacts your mortgage rate. Here's the 2026 reality:

- 740+: Best rates (6.2-6.5%)

- 700-739: Good rates (6.5-6.8%)

- 660-699: Higher rates (6.8-7.2%)

- Below 660: Difficult to qualify, very high rates

If your score needs work, spend 6-12 months improving it before buying. The rate difference between 660 and 740 can save you $200+ monthly on a $400,000 mortgage.

Run the Numbers: Use online calculators to compare:

- Current rent vs. potential mortgage payment

- Total cost of renting for 5 years vs. buying

- How much home you can afford

- Monthly payment including taxes, insurance, HOA, and maintenance

Step 2: Get Pre-Approved (Even If You're Not Sure)

Here's a pro move: get pre-approved even if you're leaning toward renting. Why? Because knowing what you qualify for changes the entire conversation. You might discover you can afford more than you thought, or you might realize buying isn't realistic yet.

Pre-approval is free, doesn't commit you to anything, and gives you critical information. It shows:

- Exact loan amount you qualify for

- Interest rate you'll receive

- Monthly payment estimates

- Any issues that need addressing

Check out our guide on pre-approval pro tips to fast-track the process.

Step 3: Research Markets Strategically

Don't just look at listings—analyze markets. In 2026, information is power:

Use AI Tools: Leverage technology to analyze markets faster. Our guide on analyzing real estate markets with AI shows how to use ChatGPT and Gemini to evaluate neighborhoods, price trends, and investment potential.

Study Trends: Look at:

- Price trends: Appreciating, stable, or declining?

- Inventory levels: Buyer's or seller's market?

- Days on market: How quickly do homes sell?

- Price reductions: Are sellers cutting prices?

- Rental rates: What's the rent-to-price ratio?

Visit Neighborhoods: Data only tells part of the story. Drive around at different times of day. Talk to residents. Check out schools, amenities, commute times, and overall vibe.

Step 4: Consider Alternative Strategies

The traditional "buy a single-family home and live in it" path isn't the only option:

House Hacking: As mentioned earlier, buying a multi-unit property and renting out part of it can dramatically reduce your housing costs while building equity.

Fixer-Upper: If you're handy (or willing to learn), buying a property that needs work can get you into a better neighborhood at a lower price. Our guide to high-ROI home renovation ideas shows which projects actually pay off.

New Construction: Builders in 2026 are offering incentives like rate buydowns, closing cost assistance, and upgrades. New homes also come with warranties and require less maintenance initially.

Condos and Townhomes: If single-family homes are out of reach, condos and townhomes offer lower entry points with less maintenance responsibility. Just understand HOA fees and rules.

Step 5: Build Your Team

Don't go it alone. Surround yourself with experts:

Real Estate Agent: Find an agent who specializes in your target area and buyer type. A great agent is worth their weight in gold—they'll find off-market deals, negotiate on your behalf, and guide you through the process.

Mortgage Broker: Unlike going directly to a bank, brokers shop multiple lenders to find you the best rate and terms. This can save thousands.

Home Inspector: Never skip the inspection. A thorough inspector will find issues that could cost you tens of thousands later. Our property inspections guide explains what to look for.

Real Estate Attorney: In some states, attorneys are required. Even where they're not, having legal representation protects your interests.

Financial Advisor: If you have complex finances or significant assets, a financial advisor can help you understand how homeownership fits into your overall wealth-building strategy.

Step 6: Make an Informed Decision

After all the research, number-crunching, and soul-searching, trust your analysis. Here's a simple decision framework:

Buy If:

✅ You plan to stay 3-5+ years

✅ Your finances are stable with good credit

✅ You have 10-20% down payment plus closing costs

✅ You have 6+ months emergency fund

✅ Monthly payment is ≤28% of gross income

✅ You're ready for maintenance responsibilities

✅ The market fundamentals are sound

Rent If:

✅ You might move within 2-3 years

✅ Your income is variable or uncertain

✅ You don't have sufficient down payment saved

✅ Your credit needs improvement

✅ You value flexibility and low responsibility

✅ The market seems overheated

✅ You're not emotionally ready for ownership

Keep Saving/Researching If:

✅ You're on the fence financially

✅ You haven't found the right market yet

✅ Interest rates might improve significantly

✅ You need to improve credit score

✅ You want to increase down payment to avoid PMI

Emerging Trends Reshaping the 2026 Market

Let's talk about the wild cards—the trends that could significantly impact your Will You Rent Or Buy In 2026? See The Surprising Real Estate Trends Ahead decision.

The Remote Work Revolution Continues

Despite return-to-office mandates from some companies, remote and hybrid work is here to stay. This fundamentally changes real estate:

Geographic Flexibility: Workers can live anywhere with good internet. This has boosted secondary markets and created opportunities in areas previously considered "too far" from job centers.

Home Office Requirements: Properties with dedicated office space command premiums. Buyers prioritize this feature, and renters seek it out. If you're buying, consider how the property accommodates remote work.

Commute Trade-Offs: With fewer commute days required, buyers are willing to live farther from offices in exchange for more space and affordability. The 1-hour commute that was unthinkable daily is fine 2-3 times weekly.

Climate Change and Natural Disasters

Insurance costs and climate risk are increasingly important factors:

Insurance Premiums: In high-risk areas (Florida hurricanes, California wildfires, coastal flooding), insurance costs have skyrocketed. Some areas are becoming uninsurable through traditional markets. Factor this into your budget—a $2,500/month mortgage with $800/month insurance is really a $3,300 payment.

Climate Migration: People are moving away from high-risk areas toward climate-resilient regions. This is creating opportunities in places like the Great Lakes region, Pacific Northwest, and parts of the Northeast.

Resilient Design: Features like solar panels, battery backup, fire-resistant materials, and flood mitigation are becoming standard considerations. Homes with these features hold value better.

Technology and Smart Homes

The modern home is increasingly connected:

Smart Home Features: Buyers expect smart thermostats, security systems, doorbell cameras, and automated lighting. These features are becoming standard rather than luxury.

Energy Efficiency: With utility costs rising, energy-efficient homes (good insulation, efficient HVAC, LED lighting, Energy Star appliances) save money and command premiums.

AI in Home Search: Tools like the AI hacks to beat house hunting fatigue are making the search process more efficient. Buyers can analyze more properties faster and make better-informed decisions.

Demographic Shifts

Millennials Hitting Peak Buying Years: The largest generation is now in their 30s and early 40s—prime homebuying age. This sustained demand supports prices.

Gen Z Entering the Market: The oldest Gen Z buyers are now in their mid-20s with increasing purchasing power. They prioritize different features (sustainability, smart tech, urban walkability) than previous generations.

Baby Boomers Aging in Place: Many Boomers are staying in their homes longer rather than downsizing, which limits inventory of larger homes. When they do move, they're often looking for low-maintenance options.

Alternative Financing Models

Rent-to-Own: These programs are expanding, allowing renters to lock in a purchase price while renting, with a portion of rent going toward down payment. It's a bridge strategy for buyers who aren't quite ready.

Co-Buying: Friends or family members pooling resources to buy together is increasingly common. It allows entry into markets that would be unaffordable solo. Just make sure you have solid legal agreements.

Fractional Ownership: Some companies offer fractional ownership of vacation properties or investment properties, lowering the barrier to entry for real estate investing.

Policy and Regulatory Changes

Zoning Reform: Many cities are relaxing single-family zoning to allow duplexes, ADUs (accessory dwelling units), and higher-density development. This increases housing supply and creates investment opportunities.

First-Time Buyer Programs: Federal and state programs continue expanding to help first-time buyers with down payment assistance, tax credits, and favorable loan terms.

Short-Term Rental Regulations: Many cities are cracking down on Airbnb and VRBO, limiting investment strategies but potentially increasing long-term rental supply.

The Bottom Line: Your 2026 Game Plan

So, Will You Rent Or Buy In 2026? See The Surprising Real Estate Trends Ahead? The answer is deeply personal and depends on your unique situation. But here's what we know for sure:

For Most People Planning to Stay 3-5+ Years, Buying Beats Renting Financially. The combination of equity building, tax benefits, and protection from rent inflation creates substantial wealth over time. Even with higher interest rates, the math works.

Renting Makes Sense for Flexibility and Short-Term Situations. If you value mobility, aren't sure where you'll be in a few years, or don't have the financial cushion for homeownership, renting is the smart play. There's no shame in it.

The Market Is More Favorable Than It's Been in Years. Increased inventory, stable (if higher) rates, and less competition mean buyers have more negotiating power than they've had since 2019. It's not 2021's feeding frenzy, and that's a good thing.

Location Matters More Than Ever. The right market can make or break your investment. Secondary markets offer better value than expensive coastal cities for most buyers. Remote work has opened up possibilities that didn't exist five years ago.

Preparation Is Everything. Whether you choose to rent or buy, having your finances in order, understanding the market, and building a strong team of advisors sets you up for success.

Your Next Steps

Run Your Numbers: Use the frameworks in this article to calculate your true costs for both renting and buying in your target market.

Get Pre-Approved: Even if you're not ready to buy immediately, knowing what you qualify for is powerful information.

Research Markets: Don't just look at your current city. With remote work, you might have more options than you think.

Build Your Team: Connect with a great real estate agent, mortgage broker, and financial advisor who understand your goals.

Take Action: Whether that means signing a lease, making an offer, or continuing to save and prepare, make an intentional decision based on your analysis.

The Will You Rent Or Buy In 2026? See The Surprising Real Estate Trends Ahead question doesn't have a one-size-fits-all answer, but it does have a right answer for you. Use the information, tools, and frameworks in this article to make that decision with confidence.

Remember, homeownership isn't just about money—it's about building the life you want. Whether that means buying your dream home, renting in your favorite neighborhood, or pursuing a creative strategy like house hacking, make the choice that aligns with your values, goals, and financial reality.

The real estate market in 2026 offers opportunities for both renters and buyers. The key is understanding which opportunity is right for you and having the courage to pursue it. Now get out there and make your move—whether that's signing a lease or signing closing papers, own your decision and make it work for you.

For more expert guidance on navigating today's real estate market, check out our comprehensive resources on home buying strategies, investment opportunities, and market analysis. Real Estate Rank IQ is here to help you make informed decisions backed by 15+ years of licensed broker experience.

Conclusion

The decision of whether to rent or buy in 2026 is one of the most significant financial choices you'll make. As we've explored throughout this comprehensive guide, there's no universal answer—but there is a right answer for your unique situation.

The 2026 real estate market presents a complex but navigable landscape. Interest rates have stabilized in the 6-7% range, inventory is improving, and rental prices continue climbing. These factors combine to create a market where buying makes financial sense for those planning to stay 3-5+ years, while renting remains the smart choice for those prioritizing flexibility or building their financial foundation.

The extraordinary opportunity in 2026 is that buyers have more negotiating power than they've had in years. The frenzied bidding wars of 2020-2021 are gone, replaced by a more balanced market where due diligence, inspections, and reasonable negotiations are back on the table. For renters, the challenge is managing escalating costs while building toward future homeownership if that's the goal.

Whether you choose to rent or buy, the key is making an informed, intentional decision based on thorough analysis of your finances, lifestyle goals, and market conditions. Use the frameworks, calculations, and strategies in this article to evaluate your options objectively. Surround yourself with expert advisors who can guide you through the process. And most importantly, trust yourself to make the decision that's right for you.

The question Will You Rent Or Buy In 2026? See The Surprising Real Estate Trends Ahead isn't just about real estate—it's about designing the life you want to live. Make your choice with confidence, execute your plan with intention, and build the future you deserve.

About Real Estate Rank IQ

Real Estate Rank IQ is a trusted real estate education platform providing expert-backed, actionable content for home buyers, sellers, investors, and real estate professionals. Our articles are written by licensed brokers with over 15 years of experience, delivering clear, step-by-step guidance on market trends, investment strategies, and financial education fundamentals.

📧 Contact: news@realestaterankiq.com

🌐 Website: https://realestaterankiq.com/

📺 YouTube: @Realestaterankiq

{kind=link}