Last updated: January 15, 2026

Picture this: You've just closed on your first investment property, ready to collect that sweet rental income. Your agent mentions insurance, and you think, "No problem, I'll just extend my homeowners policy." Wrong move. That decision could cost you tens of thousands when disaster strikes and your claim gets denied.

Homeowners Insurance vs Rental Property Insurance represents one of the most misunderstood aspects of real estate investing. The difference isn't just semantic—it's the line between protecting your investment and watching it crumble when you need coverage most. Whether you're a seasoned property investor or converting your primary residence into a rental, understanding these insurance distinctions is extraordinary important for safeguarding your portfolio in 2026.

Key Takeaways

- Landlord insurance costs 15-25% more than homeowners insurance because rental properties carry higher risks, but skipping it can result in denied claims and catastrophic financial loss[1][3]

- Homeowners insurance does NOT cover rental properties once a tenant moves in—using the wrong policy voids your coverage entirely[5]

- Loss of rental income protection is exclusive to landlord policies and shields investors from vacancy losses due to covered damage[1]

- Liability exposure differs dramatically: Landlord policies cover tenant-related incidents while homeowners policies protect owner-occupied scenarios[1]

- National averages show homeowners insurance costs $2,300-$2,600 annually while landlord insurance runs 15-25% higher depending on state and property characteristics[1][3][7]

Quick Answer

Homeowners insurance covers owner-occupied properties and protects the dwelling, personal belongings, and provides liability coverage for the policyholder and family. Landlord insurance (also called rental dwelling or investment property insurance) covers non-owner-occupied rental properties, focusing on the structure, loss of rental income, and tenant-related liability—but excludes tenant personal property. You cannot legally or effectively use homeowners insurance on a rental property[1][5]. Landlord insurance typically costs 15-25% more than homeowners insurance for the same property due to increased tenant-related risks[1][3].

What Is Homeowners Insurance?

Homeowners insurance is a comprehensive property insurance policy designed specifically for owner-occupied residences. This coverage protects both the physical structure and the policyholder's personal belongings, along with liability protection for incidents that occur on or off the property.

Standard homeowners insurance policies include four core coverage components:

Dwelling/Structure Coverage

This protects the physical building itself—walls, roof, foundation, attached structures—against covered perils like fire, wind, hail, and vandalism. The coverage limit should reflect the full replacement cost to rebuild your home, not its market value.

Personal Property Coverage

Your furniture, electronics, clothing, appliances, and other belongings receive protection both inside and outside your home. Most policies cover personal property at 50-70% of your dwelling coverage limit.

Liability Protection

If someone gets injured on your property or you accidentally damage someone else's property, liability coverage pays for legal defense and settlements. Standard policies typically include $100,000-$300,000 in liability coverage, though higher limits are available.

Loss of Use (Additional Living Expenses)

When covered damage makes your home uninhabitable, this coverage pays for hotel bills, restaurant meals, and other temporary living expenses while repairs are completed[1].

Why Homeowners Insurance Fails for Rental Properties

The fundamental problem: homeowners insurance requires owner occupancy. Once you rent out your property—even a single room—the risk profile changes dramatically. Tenants introduce new liability exposures, increased wear and tear, and higher vandalism risks that homeowners policies weren't designed to cover[5].

Insurance companies will deny claims on rental properties covered by homeowners policies. This isn't a technicality—it's a deal-breaker that can leave property investors financially devastated when disaster strikes.

What Is Landlord Insurance (Investment Property Insurance)?

Landlord insurance, also called rental dwelling policy or investment property insurance, provides coverage specifically designed for non-owner-occupied rental properties. This policy type acknowledges the unique risks that come with tenant occupancy and structures coverage accordingly.

Core Coverage Components

Landlord insurance focuses on protecting your investment asset and income stream rather than personal belongings:

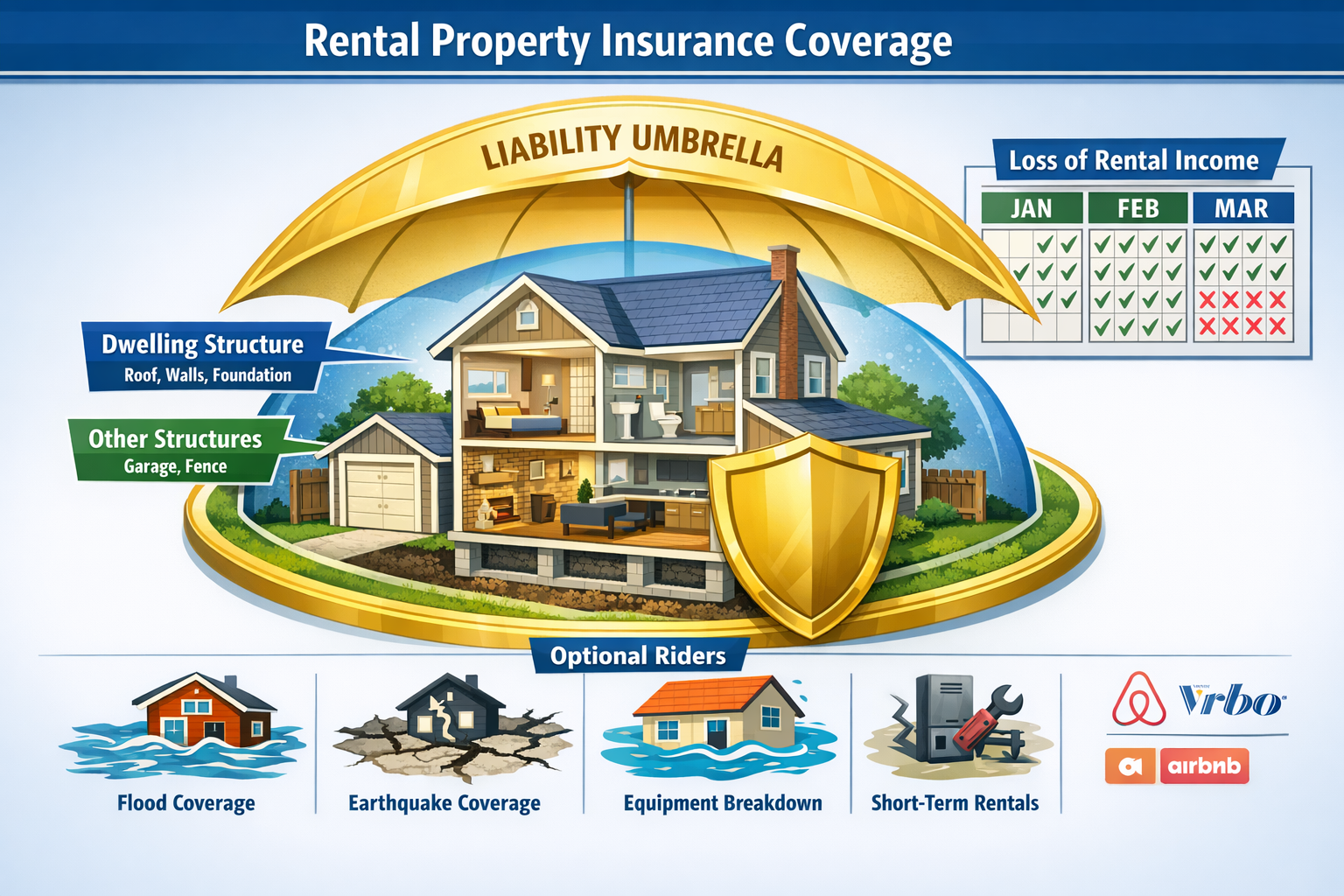

Dwelling/Structure Protection

Similar to homeowners insurance, this covers the physical building against fire, storms, vandalism, and other covered perils. The key difference: it's priced to reflect the higher risks associated with rental occupancy[1].

Other Structures

Detached garages, sheds, fences, and other structures on the rental property receive protection under this component.

Landlord Liability Coverage

This protects you against lawsuits stemming from tenant injuries, guest accidents, or property damage claims related to the rental property. Landlord liability typically covers only incidents at the rental property itself, not your personal activities elsewhere[1].

Loss of Rental Income

This is the game-changer for property investors. If covered damage makes your rental uninhabitable, this coverage reimburses your lost rental income during the repair period—typically up to 12 months. This protection doesn't exist in standard homeowners policies[1].

What Landlord Insurance Does NOT Cover

Here's where landlords sometimes get confused: landlord insurance does not cover tenant personal belongings. Your tenant's furniture, electronics, clothing, and other possessions require separate renters insurance, which the tenant purchases directly[1].

Long-Term vs Short-Term Rental Policy Differences

Standard landlord policies cover traditional long-term rentals (leases of one month or more). Short-term rentals through platforms like Airbnb or VRBO require specialized coverage or endorsements because they carry different risk profiles. The frequent turnover, higher liability exposure, and business-like operation of short-term rentals demand specific policy language[1].

For property investors managing rental property portfolios, understanding these distinctions prevents coverage gaps that could sink your investment strategy.

Key Differences Between Homeowners Insurance vs Rental Property Insurance

Understanding the distinctions between homeowners and landlord insurance isn't just academic—it determines whether your claim gets paid or denied. Let's break down the critical differences.

Occupancy Requirements

Homeowners Insurance: Requires the policyholder to occupy the property as their primary residence. You can rent out a single room while living there, but renting the entire property voids the policy[1][2].

Landlord Insurance: Designed for properties where the owner does not reside. Whether you live across town or across the country, landlord insurance covers non-owner-occupied rentals[2].

Personal Property Coverage Differences

Homeowners Insurance: Covers the owner's personal belongings—furniture, electronics, clothing, jewelry—typically at 50-70% of dwelling coverage[1].

Landlord Insurance: Covers only the landlord's property left at the rental (appliances, lawn equipment, tools). Tenant belongings are excluded. Smart landlords require tenants to carry their own renters insurance[1].

Loss of Use vs Loss of Rental Income

This distinction is extraordinary important for cash flow protection:

Homeowners Insurance: "Loss of use" coverage reimburses the policyholder's temporary living expenses (hotel, meals, storage) when their home becomes uninhabitable[1].

Landlord Insurance: "Loss of rental income" coverage reimburses the landlord for rent they cannot collect while the property undergoes covered repairs. This protects your investment income stream[1].

Liability Exposure Differences

Homeowners Insurance: Provides broad liability coverage for the policyholder, family members, and even pets—whether incidents occur at home or elsewhere[1].

Landlord Insurance: Covers liability specifically related to the rental property and tenant/guest injuries occurring there. Your personal activities outside the rental property aren't covered by landlord liability[1].

Risk Classification and Underwriting

Insurance companies classify rental properties as higher risk than owner-occupied homes because:

- Tenants typically take less care of properties than owners

- Higher turnover increases wear and tear

- Vacancy periods raise vandalism and damage risks

- Tenant screening varies widely among landlords

- Remote management makes early damage detection harder[2][5]

Why Using the Wrong Policy Results in Denied Claims

Here's the bottom line: if you file a claim on a rental property covered by a homeowners policy, the insurance company will investigate, discover the rental situation, and deny your claim[5]. You'll be stuck with the full repair bill, potential lawsuit costs, and lost rental income—all because you tried to save a few hundred dollars annually.

Insurance fraud isn't worth the risk. The premium difference between homeowners and landlord insurance is minor compared to the catastrophic loss you'll face with a denied claim.

Is Landlord Insurance Worth It for an Investment Property?

Short answer: absolutely. Long answer: let's look at the math and risk scenarios that make landlord insurance non-negotiable for serious property investors.

Risk Exposure When Renting Out a Home

Rental properties face risks that owner-occupied homes simply don't encounter:

Tenant-Related Risks

Even with impeccable tenant screening, you're trusting strangers to care for your six-figure asset. Tenant negligence, unauthorized occupants, and intentional damage create exposure that homeowners insurance doesn't address[2][5].

Liability Risks Involving Tenants and Guests

When a tenant's guest slips on icy stairs or a child gets injured on a broken deck, you face potential lawsuits. Landlord liability coverage protects your personal assets from these claims[1].

Fire, Water Damage, and Vandalism Scenarios

Consider these real-world scenarios:

- Kitchen fire caused by tenant cooking: Repair costs $85,000, property uninhabitable for 4 months

- Burst pipe during winter vacancy: Water damage totals $42,000, mold remediation adds $18,000

- Vandalism during turnover period: Property stripped of copper, appliances stolen, damages reach $35,000

Without landlord insurance, you're paying these costs out of pocket while losing rental income. With proper coverage, your insurer handles repairs and reimburses lost rent.

Income Protection Considerations

For investors relying on rental income to cover mortgages, the loss of rental income coverage is so based. If your $3,600/month rental becomes uninhabitable for 6 months due to covered damage, that's $21,600 in lost income—on top of repair costs.

Landlord insurance with loss of rental income coverage transforms a potentially portfolio-ending disaster into a manageable insurance claim.

Lender Insurance Requirements

If you carry a mortgage on your rental property, your lender requires adequate insurance coverage. Most mortgage agreements specifically require landlord insurance for non-owner-occupied properties. Failing to maintain proper coverage can trigger default provisions in your loan agreement[2].

Cost vs Potential Catastrophic Loss Comparison

Let's run the numbers:

- Annual landlord insurance premium: $2,500-$3,500 (depending on location)

- Potential uninsured loss: $50,000-$500,000+ (structure damage, liability lawsuit, lost income)

- Risk-adjusted value: Extraordinary protection for 0.5-1% of property value annually

Property investors who skip landlord insurance to save a few thousand dollars annually are gatekeeping themselves from long-term wealth building. One major incident wipes out years of rental profits.

For those exploring property management strategies, insurance should be your first line of defense, not an afterthought.

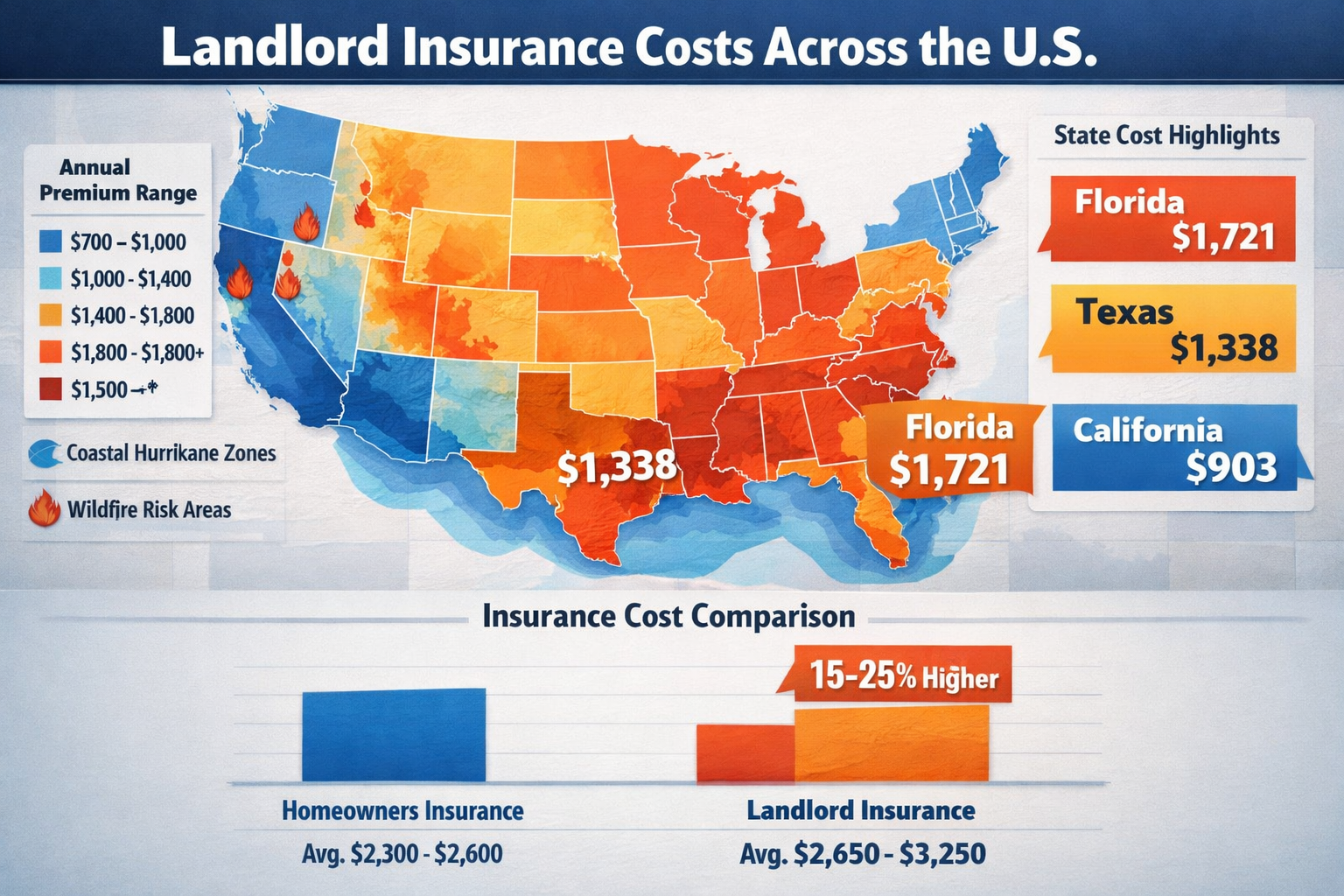

Average Cost of Landlord Insurance in the U.S. (By State)

Understanding landlord insurance costs helps property investors accurately calculate cash flow and return on investment. National averages provide a baseline, but location dramatically impacts your actual premium.

National Snapshot

Landlord insurance typically costs 15-25% more than standard homeowners insurance for the same property[1][3]. While homeowners insurance averages $2,300-$2,600 annually in 2026, landlord insurance runs $2,650-$3,250 for comparable coverage[7][3].

Several factors influence your specific premium:

Rebuild Cost

Insurance companies calculate premiums based on the cost to completely rebuild your property—not its market value. A $400,000 home in a hot market might have a $300,000 rebuild cost, while a $400,000 historic property could cost $500,000 to rebuild with period-appropriate materials.

Weather Exposure

Coastal hurricane zones, tornado alleys, and wildfire-prone areas face significantly higher premiums. Florida landlords pay nearly double what Illinois landlords pay for similar properties[3].

Claim History

Your personal claim history and the property's claim history both impact pricing. Multiple claims in recent years can increase premiums by 20-40% or make coverage difficult to obtain.

Deductible Selection

Higher deductibles lower your premium. Choosing a $5,000 deductible instead of $1,000 can reduce annual costs by 15-25%, but ensure you have cash reserves to cover the higher out-of-pocket expense.

Property Age and Condition

Older homes with outdated electrical, plumbing, or roofing systems face higher premiums. Recent upgrades to these systems can qualify for discounts[3].

Landlord Insurance Cost by State (Annual Averages)

Based on 2026 market data, here's what property investors can expect to pay annually for landlord insurance across key markets[3][6]:

| State | Avg Landlord Insurance (Annual) | Risk Factors |

|---|---|---|

| Florida | ~$1,721/year | Hurricane exposure, coastal flooding, high claim frequency |

| Texas | ~$1,338/year | Hurricanes (coastal), tornadoes, hail, wind damage |

| California | ~$903/year | Wildfire risk, earthquake exposure (separate policy) |

| New York | ~$1,396/year | Older housing stock, harsh winters, higher rebuild costs |

| New Jersey | ~$1,367/year | Coastal exposure, older properties, high property values |

| North Carolina | ~$909/year | Hurricane risk (coastal), moderate weather exposure |

| Illinois | ~$998/year | Tornado risk, harsh winters, moderate claim frequency |

| Maryland | ~$952/year | Coastal exposure (eastern), moderate weather risks |

| Connecticut | ~$1,546/year | Older homes, harsh winters, high rebuild costs |

Important Considerations:

Coastal Hurricane States: Florida, Texas, and North Carolina show dramatic premium variations by ZIP code. A beachfront property in Miami or Galveston might cost 3-4x more to insure than an inland property in the same state[6].

Wildfire Zones: California properties in high fire-risk areas face surcharges of 50-200% above base rates. Some insurers have stopped writing new policies in certain California ZIP codes entirely.

Older Homes in Northeast States: New York, New Jersey, and Connecticut properties built before 1980 often face higher rebuild-cost calculations due to period architecture, materials, and code upgrade requirements.

Higher Dwelling Coverage Impact: The state averages above assume a baseline property value around $350,000. A $600,000 property requires proportionally higher dwelling coverage, increasing premiums by 40-70%[3].

For property investors building portfolios across multiple markets, these geographic variations significantly impact cash flow projections and investment strategy.

Real-World Example: $600,000 Rental Property Renting for $3,600/Month

Let's walk through a concrete example that shows how landlord insurance costs and coverage work in practice.

Property Details:

- Market value: $600,000

- Monthly rent: $3,600

- Location: Suburban Texas (moderate risk zone)

- Property type: Single-family, 2,200 sq ft, built 2015

- Replacement cost: $450,000 (lower than market value)

Replacement Cost vs Market Value Explained

This is fresh knowledge many investors miss: insurance companies base coverage on replacement cost, not market value. Your $600,000 property might sit in a hot market where land accounts for $200,000 of the value. The actual structure might cost only $450,000 to rebuild.

Conversely, historic properties or homes with custom features might cost more to rebuild than their market value. Always get a professional replacement cost estimate—don't assume it matches your purchase price.

How Insurance Companies Calculate Dwelling Coverage

Insurers use construction cost estimators that factor in:

- Square footage and building materials

- Local labor and material costs

- Architectural complexity and custom features

- Code upgrade requirements for older homes

- Detached structures (garages, sheds)

For our $600,000 Texas rental with $450,000 replacement cost, the dwelling coverage would be set at $450,000 minimum. Many investors add 10-20% extended replacement cost coverage for inflation protection.

Estimated Premium Range

Based on Texas landlord insurance averages and this property profile:

- Base annual premium: $1,500-$1,800

- With higher liability ($500K): $1,650-$2,000

- Adding loss of rent coverage (12 months): $1,800-$2,200

- With optional riders (water backup, equipment breakdown): $2,000-$2,400

Let's use $2,100 as our working annual premium for comprehensive coverage.

Annual Premium as Percentage of Gross Rent

- Annual gross rent: $3,600 × 12 = $43,200

- Annual insurance premium: $2,100

- Insurance as % of gross rent: 4.9%

This falls within the healthy range for rental property operating expenses. Most property investors budget 5-7% of gross rent for insurance in moderate-risk areas.

Impact on Overall Cash Flow

Monthly breakdown:

- Gross rent: $3,600

- Insurance: $175/month ($2,100 ÷ 12)

- Property tax (est): $500/month

- Maintenance reserve: $360/month (10% rule)

- Property management: $360/month (10% if outsourced)

- Total operating expenses: ~$1,395/month

If your mortgage payment is $2,000/month, your monthly cash flow is approximately $205 before vacancy allowance—tight but positive.

How Loss-of-Rent Coverage Protects Income Stream

Now imagine a kitchen fire causes $60,000 in damage, making the property uninhabitable for 4 months during repairs:

Without loss-of-rent coverage:

- Lost rental income: $3,600 × 4 = $14,400

- Mortgage still due: $2,000 × 4 = $8,000

- Out-of-pocket loss: $14,400 (plus you're still covering the mortgage)

With loss-of-rent coverage:

- Insurance reimburses: $14,400

- You continue covering mortgage from insurance proceeds

- Out-of-pocket loss: $0 (beyond your deductible)

This single benefit justifies the entire insurance premium. For investors managing multiple properties, loss-of-rent coverage is the difference between a manageable setback and a portfolio-threatening crisis.

Understanding these numbers helps property investors make informed decisions about property management and portfolio growth strategies.

What to Look for in a Rental Property Insurance Policy

Not all landlord insurance policies are created equal. Knowing which coverage components are essential versus optional helps property investors build impeccable protection without overpaying.

Core Coverage Essentials

These components should be non-negotiable in any landlord insurance policy:

Dwelling Coverage at Replacement Cost

Always choose replacement cost coverage over actual cash value (ACV). Replacement cost pays to rebuild your property with new materials at current prices. ACV deducts depreciation, leaving you with insufficient funds to actually rebuild.

Example: A 15-year-old roof destroyed by fire would receive maybe 40% of replacement cost under ACV coverage, but 100% under replacement cost coverage. The premium difference is minimal—typically 10-15%—but the claim payout difference is extraordinary[1].

Other Structures Protection

Detached garages, storage sheds, fences, and other structures should be covered at 10-20% of your dwelling coverage. If your dwelling coverage is $400,000, you want at least $40,000-$80,000 for other structures.

Liability Protection ($300K-$500K Minimum Suggested)

Standard landlord policies include $100,000-$300,000 in liability coverage. For serious property investors, this isn't enough. Increase your liability coverage to $500,000 minimum—the premium increase is modest (often $50-$100 annually) but the protection is substantial.

Better yet, add an umbrella liability policy (discussed later) that provides $1-$2 million in additional coverage across all your properties.

Loss of Rental Income Coverage

This should cover at least 12 months of rental income. If your property rents for $2,500/month, you want $30,000 in loss-of-rent coverage. Some policies cap this at 6 months—avoid those policies or negotiate higher limits[1].

Replacement Cost vs Actual Cash Value Clarification

Let's make this crystal clear with an example:

Your rental property suffers $100,000 in fire damage:

- Replacement Cost Coverage: Insurance pays $100,000 (minus deductible) to rebuild with new materials

- Actual Cash Value Coverage: Insurance pays $100,000 minus depreciation—maybe $60,000-$70,000 for a 20-year-old property

You'd be $30,000-$40,000 short of actual rebuild costs with ACV coverage. Always choose replacement cost for dwelling coverage.

Important Optional Riders

These endorsements aren't always included in base policies but provide valuable protection for specific risks:

Sewer/Water Backup Coverage

Standard policies often exclude damage from sewer or drain backups. This rider adds coverage for sewage cleanup, water damage, and repairs when drains back up into your property. Cost: typically $50-$150 annually. Worth it? Absolutely—sewage damage claims average $10,000-$20,000.

Equipment Breakdown Coverage

This covers mechanical failure of HVAC systems, water heaters, and appliances beyond normal wear and tear. Particularly valuable for older rental properties. Cost: $100-$200 annually.

Ordinance or Law Coverage

When you rebuild after a covered loss, current building codes might require expensive upgrades that didn't exist when the property was built. This coverage pays for code compliance upgrades. Essential for older properties. Cost: varies by property age, typically $150-$300 annually.

Extended Replacement Cost

This provides an additional 25-50% above your dwelling coverage limit if rebuild costs exceed your policy limit due to inflation or material shortages. Cost: typically 5-10% premium increase. Smart protection in volatile construction markets.

Flood Insurance (Separate Policy)

Standard landlord insurance excludes flood damage. If your property sits in a flood zone—or even near one—purchase separate flood insurance through the National Flood Insurance Program (NFIP) or private insurers. Cost: $400-$2,000+ annually depending on flood risk.

Earthquake Coverage (If Applicable)

California, Pacific Northwest, and other seismically active regions require separate earthquake coverage. Cost varies dramatically by location and construction type.

Short-Term Rental Endorsement (If Needed)

Planning to list your property on Airbnb or VRBO? Standard landlord policies exclude short-term rental activity. You'll need either a specific endorsement or a specialty short-term rental policy. Cost: typically 20-40% premium increase over standard landlord insurance[1].

For investors comparing property management options, understanding these coverage nuances helps you protect your investment properly.

Pros and Cons of Landlord Insurance

Let's be real about the trade-offs property investors face with landlord insurance.

Pros

Protects Investment Equity

Your rental property represents significant capital—often your largest single investment. Landlord insurance protects that equity from catastrophic loss. Without it, a single fire or liability lawsuit could wipe out years of appreciation and rental profits.

Shields Against Lawsuits

Tenant slip-and-fall claims, guest injuries, and property damage lawsuits are real risks. Landlord liability coverage pays for legal defense and settlements, protecting your personal assets from judgments that could exceed your net worth[1].

Protects Rental Income

Loss of rental income coverage ensures you continue receiving rent payments (from insurance) even when your property sits vacant due to covered damage. This cash flow protection is extraordinary for investors relying on rental income to cover mortgages and living expenses[1].

Required by Most Lenders

If you're carrying a mortgage, your lender mandates adequate insurance. Landlord insurance satisfies this requirement and protects the lender's collateral interest in your property[2].

Risk Mitigation for Remote Owners

Managing rental properties from a distance increases risk. You can't immediately spot maintenance issues or respond to emergencies. Landlord insurance provides a safety net when you can't be physically present to prevent problems.

Cons

Higher Premiums Than Homeowners Policies

Landlord insurance costs 15-25% more than homeowners insurance for the same property[1][3]. This premium increase reflects genuine increased risk, but it does impact cash flow calculations and return on investment.

Deductibles Can Be High in Storm-Prone States

Coastal properties and hurricane zones often face percentage deductibles (2-5% of dwelling coverage) rather than flat dollar amounts. On a $400,000 property, a 2% hurricane deductible means you pay the first $8,000 of any hurricane claim out of pocket.

Certain Exclusions May Apply

Standard policies exclude:

- Flood damage (requires separate policy)

- Earthquake damage (requires separate coverage)

- Tenant belongings (tenant needs renters insurance)

- Intentional damage by landlord

- Normal wear and tear

- Mold (unless resulting from covered peril)

Understanding these exclusions prevents nasty surprises at claim time.

Premium Volatility in High-Risk Regions

Florida, California, and other high-risk states have experienced 20-40% annual premium increases in recent years[8]. Some insurers have stopped writing new policies entirely in certain markets, leaving property investors scrambling for coverage.

This volatility makes long-term cash flow projections challenging in these markets.

The Verdict

Despite the cons, landlord insurance remains non-negotiable for serious property investors. The protection it provides far outweighs the cost, and the alternative—going uninsured or underinsured—creates unacceptable risk to your investment portfolio.

Red Flags to Watch for in Insurance Policies

Not all landlord insurance policies provide equal protection. Watch for these warning signs that indicate inadequate or problematic coverage:

Dwelling Limit Too Low for Rebuild Cost

If your policy's dwelling coverage is significantly below the actual replacement cost, you're underinsured. This creates coinsurance penalties where the insurance company reduces claim payments proportionally.

Example: Your property needs $400,000 to rebuild, but you only carry $300,000 in dwelling coverage (75% of required amount). When you file a $100,000 claim, the insurer only pays 75% ($75,000) because you're underinsured.

Solution: Get a professional replacement cost estimate every 2-3 years and adjust coverage accordingly.

Actual Cash Value (ACV) Instead of Replacement Cost

As discussed earlier, ACV coverage deducts depreciation from claim payments, leaving you short of rebuild costs. This is a major red flag unless you're intentionally choosing ACV to reduce premiums on a property you plan to demolish anyway.

Percentage Hurricane Deductibles

Coastal properties often include separate hurricane deductibles of 2-5% of dwelling coverage. On a $500,000 property, a 5% hurricane deductible means you pay the first $25,000 of any hurricane claim.

While these deductibles are sometimes unavoidable in high-risk areas, understand the financial impact before assuming you can afford the out-of-pocket expense.

Low Liability Limits

Policies with only $100,000 in liability coverage create dangerous exposure. A serious injury claim or lawsuit can easily exceed this amount, putting your personal assets at risk.

Loss of Rent Caps Too Restrictive

Some policies cap loss of rental income at 6 months or limit it to a percentage of dwelling coverage. If major repairs take 9-12 months, you'll be covering lost rent out of pocket for the excess period.

Vacancy Exclusions

Many landlord policies include vacancy exclusions that void coverage if the property sits vacant for 30-60+ consecutive days. This creates problems during tenant turnover, renovations, or seasonal rentals.

Solution: Look for policies with 60-90 day vacancy allowances, or notify your insurer when extended vacancies are planned.

Mold or Water Damage Exclusions

Some policies broadly exclude mold damage or limit water damage coverage. Given that water damage is one of the most common rental property claims, these exclusions are problematic.

No Coverage for Tenant-Caused Damage

While landlord insurance covers vandalism and malicious damage, some policies exclude damage caused by tenant negligence. This distinction matters—intentional damage is covered, but negligence isn't.

Solution: Require substantial security deposits and thorough tenant screening to minimize this risk.

Spotting these red flags before you purchase coverage prevents devastating surprises when you file a claim. For investors managing multiple properties, working with an experienced insurance broker who understands real estate investment risks is worth the effort.

Can You Negotiate a Better Insurance Policy?

Absolutely. Insurance premiums aren't set in stone, and savvy property investors use multiple strategies to reduce costs while maintaining comprehensive coverage.

Shopping Multiple Carriers Annually

Insurance company pricing changes constantly based on their claims experience, risk appetite, and competitive positioning. The carrier offering the best rate this year might be 30% higher next year.

Strategy: Get quotes from at least 3-5 carriers annually. Set a calendar reminder 60 days before renewal to start shopping. You'll be surprised how much rates vary for identical coverage.

Using Independent Brokers

Independent insurance brokers represent multiple carriers and can shop your coverage across their entire network. Unlike captive agents (who represent only one company), brokers work for you and can find the best combination of price and coverage.

Bonus: Experienced brokers understand landlord insurance nuances and can identify coverage gaps you might miss.

Bundling Auto + Home Policies

Many insurers offer 10-25% discounts when you bundle multiple policies with them. Combining your auto insurance, primary residence homeowners policy, and landlord policies with one carrier can generate significant savings.

Caution: Don't sacrifice coverage quality for bundling discounts. Sometimes the "bundled" price is still higher than buying separately from different carriers.

Increasing Deductibles Strategically

Raising your deductible from $1,000 to $2,500 or $5,000 can reduce premiums by 15-30%. This strategy works best when you maintain adequate cash reserves to cover the higher deductible if needed.

Smart approach: Set aside the premium savings in a dedicated emergency fund until you've accumulated enough to cover the higher deductible.

Upgrading Roof, Plumbing, Electrical Systems

Insurance companies reward risk reduction. Upgrading major systems generates discounts and makes coverage easier to obtain:

- Roof replacement: 10-20% discount for roofs less than 10 years old

- Electrical panel upgrade: 5-15% discount for updated panels and wiring

- Plumbing replacement: 5-10% discount for replacing galvanized or polybutylene pipes

- HVAC replacement: 5-10% discount for newer systems

These upgrades also reduce claim frequency, creating a virtuous cycle of lower premiums and fewer maintenance headaches.

Installing Security Systems and Leak Sensors

Modern technology reduces risk and premiums:

- Security systems: 5-15% discount for monitored alarm systems

- Water leak sensors: 5-10% discount for whole-house leak detection

- Smart home systems: 5-10% discount for integrated monitoring

- Fire sprinkler systems: 10-20% discount (rare in residential)

The premium savings often pay for the technology within 2-3 years.

Asking for All Available Discounts

Insurance companies offer dozens of discounts, but they don't always volunteer them. Specifically ask about:

- Multi-property discount (owning multiple rentals)

- Claims-free discount (no claims for 3-5 years)

- Loyalty discount (staying with carrier for multiple years)

- Automatic payment discount

- Paperless billing discount

- Professional association discounts (real estate investor groups)

- Age of home discount (newer construction)

- Gated community discount

- Distance to fire station discount

These small discounts stack up. Combining 5-6 discounts can reduce premiums by 20-30%.

For property investors building portfolios, these negotiation strategies become increasingly valuable as you scale. The difference between paying $2,800 versus $2,100 per property annually is $700—multiply that across 10 properties and you're saving $7,000 annually.

Local Insurance Provider vs Nationwide Carrier

Property investors face a strategic choice: work with local/regional insurance providers or stick with national carriers. Both have distinct advantages.

Benefits of Local Providers

Regional Underwriting Expertise

Local insurers understand regional risks intimately. A Florida-based carrier knows hurricane exposure patterns better than a national carrier applying generic risk models. This expertise can translate to more accurate pricing and better claims handling.

Knowledge of State-Specific Risks

State insurance regulations, building codes, and weather patterns vary dramatically. Local providers navigate these nuances daily, while national carriers sometimes struggle with regional peculiarities.

Personalized Service

Local agents often provide hands-on service, site visits, and relationship-based support. When you call, you speak with someone who knows your properties and understands your portfolio strategy.

Community Connections

Local providers often have relationships with contractors, adjusters, and other professionals who can expedite claims and repairs.

Benefits of Nationwide Carriers

Financial Stability

Major national carriers (State Farm, Allstate, Travelers) have massive financial reserves to pay claims even after catastrophic events. When hurricanes, wildfires, or other disasters strike entire regions, financial strength matters.

Strong Claims Infrastructure

National carriers maintain extensive claims networks with 24/7 support, mobile apps for claim filing, and standardized processes that ensure consistent service regardless of location.

Multi-Policy Discounts

National carriers excel at bundling discounts across auto, home, landlord, and umbrella policies. These discounts can offset any premium disadvantages compared to local carriers.

Advanced Digital Tools

Major carriers invest heavily in technology—mobile apps, online policy management, digital claim filing, and customer portals. Local carriers sometimes lag in technology adoption.

Strategic Approach

The best strategy combines both:

Compare Local and National Quotes

Get quotes from 2-3 local/regional carriers AND 2-3 national carriers. Compare not just price but coverage details, deductibles, and exclusions.

Consider Specialty Carriers for High-Risk Properties

Some carriers specialize in challenging properties:

- Coastal properties in hurricane zones

- Older homes with outdated systems

- Properties with prior claim history

- Short-term rentals

These specialty carriers often provide better coverage and pricing for properties that mainstream carriers won't touch.

Match Carrier to Property Type

- Standard suburban rentals: National carriers often offer competitive rates

- Coastal/high-risk properties: Regional specialists understand local risks better

- Large portfolios: National carriers with multi-property discounts

- Unique properties: Local carriers with flexible underwriting

For investors managing diverse portfolios across multiple states, maintaining relationships with both local and national carriers provides flexibility and leverage for property management optimization.

Top 10 Nationwide Home & Landlord Insurance Providers to Research

When shopping for landlord insurance, these national carriers consistently rank among the most reliable and competitive options for property investors in 2026:

1. State Farm

The largest property insurer in the U.S. offers competitive landlord insurance rates, strong financial stability, and extensive agent network. Known for excellent customer service and claims handling. Best for: investors with multiple properties seeking bundling discounts.

2. Allstate

Provides comprehensive landlord insurance with flexible coverage options and competitive pricing. Strong digital tools and mobile app. Best for: tech-savvy investors who value online policy management.

3. Liberty Mutual

Offers specialized investment property coverage with customizable options. Strong in coastal markets. Best for: investors in high-risk coastal areas needing specialized coverage.

4. USAA

Available only to military members, veterans, and families. Consistently ranks highest in customer satisfaction with exceptional claims service and competitive rates. Best for: military-affiliated property investors.

5. Farmers Insurance

Provides flexible landlord insurance with strong coverage options for short-term rentals and vacation properties. Best for: Airbnb and VRBO hosts needing specialized coverage.

6. Nationwide

Strong landlord insurance program with competitive rates and excellent multi-policy discounts. Good coverage for older properties. Best for: investors with older rental properties or mixed portfolios.

7. Travelers

Specializes in landlord insurance with robust coverage options and strong claims service. Excellent for high-value properties. Best for: investors with premium properties or large portfolios.

8. American Family Insurance

Regional carrier (Midwest focus) with competitive landlord insurance rates and personalized service. Best for: Midwest property investors seeking local expertise with national backing.

9. Progressive

Known for competitive pricing and innovative coverage options. Strong digital tools and quick quote process. Best for: price-conscious investors comfortable with online management.

10. Chubb

Premium carrier specializing in high-value properties with exceptional coverage limits and claims service. Higher premiums but impeccable coverage. Best for: luxury rental properties and high-net-worth investors.

Research Strategy

Don't assume the carrier insuring your primary residence offers the best landlord insurance rates. Get quotes from at least 3-5 carriers from this list, comparing:

- Annual premium for identical coverage

- Deductible options

- Loss of rental income limits

- Liability coverage amounts

- Optional rider availability

- Multi-property discounts

- Claims service reputation

For investors building portfolios, establishing relationships with 2-3 preferred carriers provides negotiating leverage and backup options when one carrier raises rates or restricts coverage.

Questions to Ask Your Insurance Company

Before purchasing landlord insurance, get clear answers to these critical questions. Vague or evasive responses are red flags.

Coverage Questions

"Is this a homeowners or landlord policy?"

Confirm you're getting actual landlord insurance, not homeowners insurance with a rental endorsement. The policy should be specifically designed for non-owner-occupied rental properties.

"How is replacement cost calculated for my property?"

Understand the methodology—square footage, construction type, local labor costs. Request a detailed replacement cost estimate and verify it seems reasonable for your market.

"What liability limits are included, and what are my options for higher coverage?"

Standard policies include $100,000-$300,000. Confirm you can increase to $500,000+ and understand the premium difference.

"Is loss of rental income included, and what's the coverage limit?"

Verify this coverage is included (not all policies include it automatically) and confirm the limit covers at least 12 months of rent.

Rental-Specific Questions

"Are long-term rentals (12-month leases) fully covered under this policy?"

This should be a straightforward "yes" for landlord insurance. If there are restrictions, understand them completely.

"What happens during vacancy periods between tenants?"

Understand the vacancy clause—how many days of vacancy are allowed before coverage is affected? Do you need to notify the insurer of vacancies?

"Are short-term rentals (Airbnb, VRBO) allowed under this policy?"

If you plan to use the property for short-term rentals, confirm whether the policy covers this or requires a specific endorsement.

"Does the policy cover tenant-caused damage, or only vandalism?"

Clarify whether negligent tenant damage is covered or only intentional/malicious damage.

Cost & Deductible Questions

"What deductible options are available?"

Understand all deductible choices ($500, $1,000, $2,500, $5,000) and the premium impact of each option.

"Are there separate deductibles for specific perils (hurricane, wind, hail)?"

Coastal properties often have percentage-based deductibles for hurricanes. Understand exactly what you'd pay out of pocket for different claim types.

"What discounts apply to my policy?"

Ask specifically about multi-property, claims-free, security system, new roof, and bundling discounts. Don't assume they're automatically applied.

"How often can premiums increase, and what triggers rate changes?"

Understand whether your premium is locked for a year or can change mid-term. What circumstances trigger increases?

"What triggers non-renewal or cancellation?"

Understand the insurer's non-renewal policies. How many claims trigger non-renewal? Are there property condition requirements?

Claims Questions

"What's the claims process, and how quickly are claims typically processed?"

Understand whether you file online, by phone, or through an agent. What's the typical timeline from claim filing to payment?

"Is there a 24/7 claims hotline?"

For emergency situations (fire, flood, major damage), you need immediate claims support.

"Do you provide emergency mitigation services (water extraction, board-up, etc.)?"

Many carriers provide or coordinate emergency services to prevent further damage. Confirm this is included.

Getting clear answers to these questions before purchasing coverage prevents misunderstandings and ensures you're getting the protection your investment portfolio needs.

Smart Tips from Landlords and Investors

These practical strategies come from experienced property investors who've learned (sometimes the hard way) how to optimize insurance coverage and costs.

Shop Insurance Annually

Set a calendar reminder 60 days before your policy renewal. Insurance company pricing changes constantly—the carrier offering the best rate this year might be 30% higher next year. Annual shopping ensures you're always getting competitive pricing.

Pro tip: Don't wait until renewal day. Start shopping 60 days early so you have time to compare quotes without pressure.

Require Tenants to Carry Renters Insurance

Include a renters insurance requirement in your lease agreement. Tenants should carry at least $100,000 in liability coverage and enough personal property coverage for their belongings.

Benefits:

- Protects tenant belongings (they can't sue you for items lost in a fire)

- Provides tenant liability coverage (reduces your exposure)

- Costs tenants only $15-$25/month

- Professional property managers consider this standard practice

Request proof of coverage before move-in and annually thereafter. Many landlord insurance policies offer small discounts when tenants carry renters insurance.

Add Umbrella Liability Coverage

Once you own 2+ rental properties, add a commercial umbrella liability policy providing $1-$2 million in additional coverage across your entire portfolio. This costs only $300-$600 annually but provides extraordinary protection against catastrophic liability claims.

Umbrella coverage kicks in when your underlying landlord liability limits are exhausted, protecting your personal assets from judgments that could otherwise bankrupt you.

Maintain Strong Credit Profile

Insurance companies use credit-based insurance scores to price policies. Maintaining excellent credit can reduce premiums by 20-30% compared to poor credit.

Actions that help:

- Pay all bills on time

- Keep credit utilization below 30%

- Maintain long credit history

- Avoid unnecessary credit inquiries

Install Leak Detection Devices

Water damage is the most common and costly rental property claim. Installing whole-house leak detection systems (like Flo by Moen or Phyn) provides:

- 5-10% insurance discounts

- Automatic water shutoff when leaks are detected

- Real-time alerts to your phone

- Reduced claim frequency

The $500-$800 investment pays for itself through premium savings and prevented water damage.

Keep Documentation of Upgrades

Maintain detailed records of all property improvements:

- Roof replacement receipts and warranties

- HVAC installation documentation

- Electrical panel upgrades

- Plumbing replacements

- Security system installation

This documentation supports insurance discount applications and helps during claims by proving the property's condition and value.

Review Policy Limits Yearly

Property values, construction costs, and rental rates change. Review your coverage annually to ensure:

- Dwelling coverage still reflects replacement cost

- Loss of rental income matches current rent

- Liability limits remain adequate for your net worth

- Optional riders still make sense for your situation

Pro tip: Increase dwelling coverage by 3-5% annually to account for construction cost inflation, or get a new replacement cost estimate every 2-3 years.

For investors scaling portfolios, these strategies become increasingly valuable. The difference between optimized insurance costs and paying retail rates compounds significantly across multiple properties and years.

Understanding these nuances helps investors make informed decisions about property investment strategies and portfolio management.

Frequently Asked Questions (FAQ)

What is the difference between homeowners insurance and landlord insurance?

Homeowners insurance covers owner-occupied properties, protecting the dwelling, personal belongings, and providing liability coverage for the policyholder and family. Landlord insurance covers non-owner-occupied rental properties, focusing on the structure, loss of rental income, and tenant-related liability while excluding tenant personal belongings[1]. The key distinction: homeowners insurance requires owner occupancy while landlord insurance is designed for properties you rent to tenants.

Do you need landlord insurance if you rent out your house?

Yes, absolutely. Standard homeowners insurance does not cover rental properties once a tenant moves in[5]. Using homeowners insurance on a rental property will result in denied claims when you need coverage most. Landlord insurance is specifically designed for the unique risks of rental properties, including tenant damage, liability claims from tenant guests, and loss of rental income[1][2].

How much does landlord insurance cost by state?

Landlord insurance costs vary significantly by state based on weather risks, claim frequency, and construction costs. National averages range from $900-$1,700+ annually. Florida averages ~$1,721/year, Texas ~$1,338/year, California ~$903/year, and New York ~$1,396/year[3][6]. Coastal hurricane zones and wildfire-prone areas face the highest premiums, while moderate-risk inland states typically see lower costs. Landlord insurance generally costs 15-25% more than homeowners insurance for the same property[1][3].

Is landlord insurance worth the extra cost?

Absolutely. The 15-25% premium increase over homeowners insurance is minor compared to the catastrophic losses you'd face without proper coverage[1][3]. Landlord insurance protects your investment equity, shields you from tenant-related liability lawsuits, and provides loss of rental income coverage that can save your cash flow during major repairs. One significant claim or lawsuit would cost far more than years of insurance premiums.

Does landlord insurance cover tenant damage?

Landlord insurance covers malicious or vandalism-related tenant damage, but coverage for negligent damage varies by policy[2]. Standard policies typically cover intentional destruction but may exclude simple negligence. This is why requiring substantial security deposits and thorough tenant screening remains important. Landlord insurance does NOT cover normal wear and tear or gradual deterioration.

Does landlord insurance cover loss of rent?

Yes, most landlord insurance policies include loss of rental income coverage (also called rental reimbursement or fair rental value coverage). This reimburses you for rent you cannot collect when covered damage makes your property uninhabitable during repairs—typically up to 12 months[1]. This coverage is one of the most valuable components of landlord insurance and doesn't exist in standard homeowners policies.

Can you keep homeowners insurance on a rental property?

No. Once you rent out your property to tenants, homeowners insurance no longer provides coverage[5]. Insurance companies will deny claims when they discover the property is rented. If you rent out a single room while still living in the property, some homeowners policies may cover this arrangement, but renting the entire property requires landlord insurance[1][2]. Attempting to use homeowners insurance on a rental property constitutes insurance fraud and leaves you completely unprotected.

What liability coverage should landlords carry?

Landlords should carry minimum $300,000-$500,000 in liability coverage through their landlord insurance policy[1]. For investors with significant personal assets or multiple properties, adding a $1-$2 million commercial umbrella liability policy provides additional protection for only $300-$600 annually. The umbrella policy covers liability claims that exceed your underlying landlord policy limits, protecting your personal assets from catastrophic lawsuits.

Is landlord insurance tax deductible?

Yes, landlord insurance premiums are fully tax-deductible as a rental property business expense. You can deduct the entire annual premium on Schedule E of your tax return as an operating expense, reducing your taxable rental income[9]. This tax deduction effectively reduces the after-tax cost of landlord insurance by 20-37% depending on your tax bracket, making the coverage even more affordable for property investors.

Should rental property owners carry umbrella insurance?

Yes, once you own 2+ rental properties or have significant personal assets to protect, adding a commercial umbrella liability policy is smart risk management. Umbrella policies provide $1-$2 million in additional liability coverage across all your rental properties for only $300-$600 annually. This coverage protects your personal assets (home, savings, investments) from catastrophic liability judgments that exceed your underlying landlord policy limits. The minimal cost provides extraordinary protection for serious property investors.

Conclusion

The distinction between Homeowners Insurance vs Rental Property Insurance isn't just insurance industry jargon—it's the difference between protecting your investment and watching it crumble when disaster strikes. Homeowners insurance protects owner-occupied properties with coverage for personal belongings and family liability. Landlord insurance protects rental properties with coverage for loss of rental income and tenant-related risks.

Key points property investors must remember:

- Never use homeowners insurance on rental properties—claims will be denied, leaving you financially devastated[5]

- Landlord insurance costs 15-25% more but provides essential protections homeowners policies don't offer, particularly loss of rental income coverage[1][3]

- Geographic location dramatically impacts costs—Florida landlords pay nearly double what California landlords pay for similar properties[3][6]

- Require tenants to carry renters insurance and add umbrella liability coverage once you own multiple properties

- Shop insurance annually and leverage discounts for security systems, property upgrades, and bundling policies

For 2026 and beyond, insurance costs will likely continue rising in high-risk markets due to climate change impacts and increased claim frequency[8]. Property investors who understand these coverage distinctions and implement smart insurance strategies will protect their portfolios while optimizing costs.

Actionable Next Steps

- Review your current coverage immediately: If you're using homeowners insurance on a rental property, switch to landlord insurance before filing any claims

- Get 3-5 landlord insurance quotes: Compare coverage details, not just premiums, from both local and national carriers

- Calculate accurate replacement costs: Ensure your dwelling coverage reflects actual rebuild costs, not market value

- Add loss of rental income coverage: Protect your cash flow with at least 12 months of rental income coverage

- Require tenant renters insurance: Add this requirement to your lease agreements starting with your next tenant

- Consider umbrella liability: Once you own 2+ properties, add $1-$2 million in umbrella coverage

- Install risk-reduction technology: Leak detection systems and security monitoring reduce premiums and claims

- Document all property improvements: Keep receipts for upgrades that qualify for insurance discounts

The property investors who thrive long-term are those who treat insurance as a strategic asset protection tool, not an annoying expense. Your rental properties represent significant capital and income potential—protect them with coverage designed for the actual risks you face.

For more guidance on building and protecting your real estate investment portfolio, explore Real Estate Rank IQ's comprehensive resources on property management strategies, investment risk mitigation, and portfolio growth tactics.

Real Estate Rank IQ provides expert-backed guidance from licensed brokers with over 15 years of experience. For personalized real estate investment advice, contact us at news@realestaterankiq.com or visit realestaterankiq.com.

References

[1] How Are Landlord And Homeowners Insurance Different – https://www.hippo.com/learn-center/how-are-landlord-and-homeowners-insurance-different

[2] Landlord Insurance Vs Homeowners Insurance – https://www.travelers.com/resources/home/landlords/landlord-insurance-vs-homeowners-insurance

[3] Landlord Insurance Statistics – https://richeyinsurance.com/landlord-insurance-statistics/

[5] Best Landlord Insurance Options – https://www.doorloop.com/blog/best-landlord-insurance-options

[6] Texas Landlord Insurance – https://www.obieinsurance.com/blog/texas-landlord-insurance

[7] Average Homeowners Insurance Cost – https://www.nerdwallet.com/insurance/homeowners/learn/average-homeowners-insurance-cost

[8] 2026 Home Insurance Predictions – https://matic.com/blog/2026-home-insurance-predictions/

[9] Rental Property Insurance Vs Homeowners Insurance – https://brookscannon.com/rental-property-insurance-vs-homeowners-insurance/

{kind=link}