Last updated: April 1, 2026

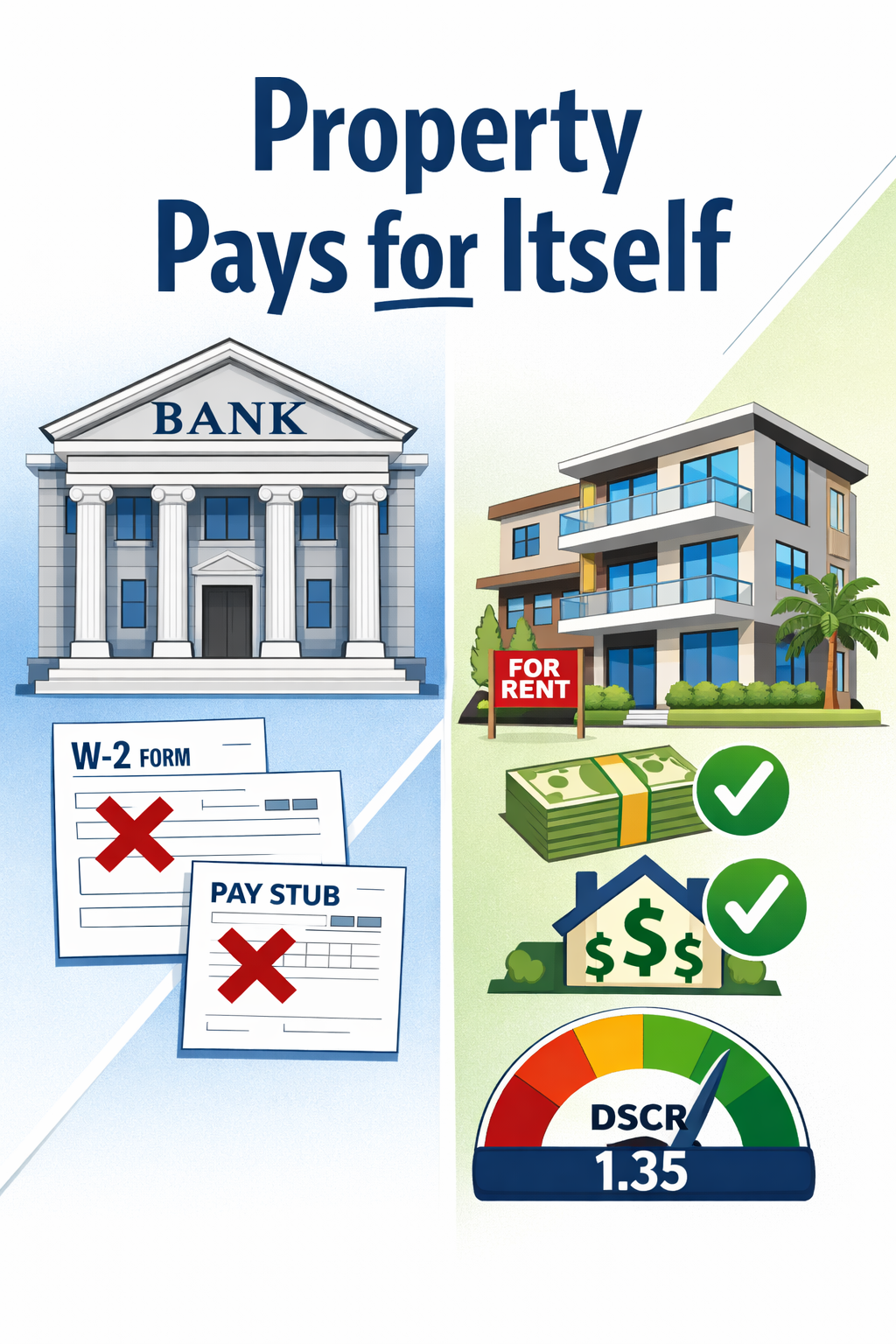

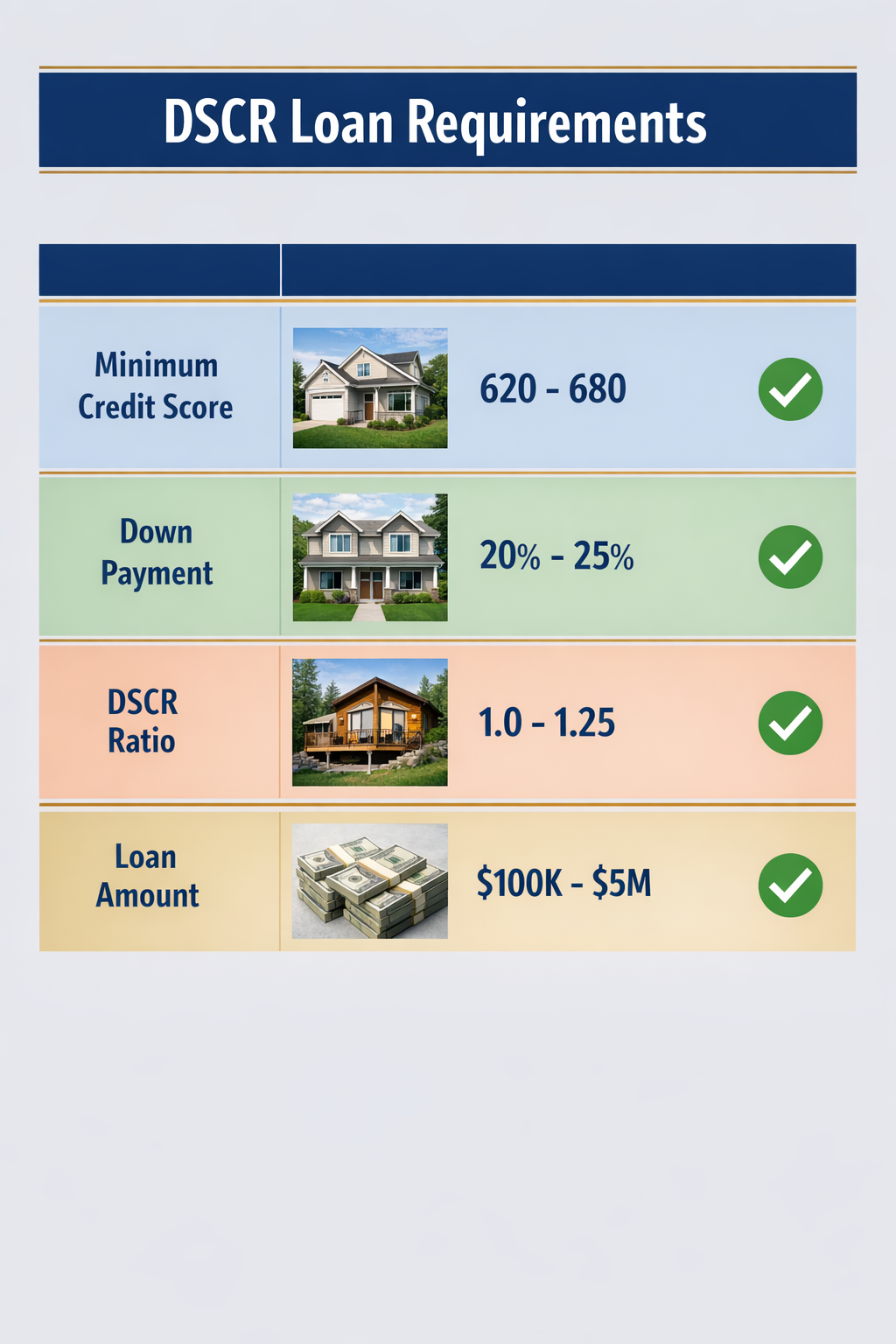

Quick Answer: A DSCR loan qualifies you based on a rental property’s income, not your personal tax returns or W-2s. To get approved, most lenders require a minimum DSCR ratio of 1.0 to 1.25, a credit score of at least 620 to 680, and a down payment of 20% to 25%. Rates in 2026 range from approximately 6.5% to 8.75% depending on your ratio, credit profile, and lender.

Key Takeaways

- DSCR stands for Debt Service Coverage Ratio — it measures whether a property’s rental income covers its mortgage payment.

- No personal income verification is required. Approval is based entirely on the property’s cash flow.

- Minimum DSCR ratio: Most lenders accept 1.0 (break-even), but 1.25+ gets you the best rates and terms.

- Credit score floor: Expect a minimum of 620, with 700+ unlocking significantly better pricing.

- Down payment: Typically 20% to 25% for most property types; some lenders require 30% for condos or short-term rentals.

- Eligible property types include single-family rentals, 2-4 unit properties, multifamily (5+), condos, and short-term rentals (Airbnb-style).

- Loan amounts generally range from $100,000 to $5 million, with some lenders going higher for portfolio deals.

- Closing timelines average 21 to 30 days, faster than conventional investment loans at 30 to 55 days. [4]

- DSCR loans work best for self-employed investors, those with complex tax returns, or anyone scaling a rental portfolio quickly.

- Current 2026 rates sit between 6.5% and 8.75%, driven by property cash flow strength and secondary market conditions. [3]

What Is a DSCR Loan and How Does It Work?

A DSCR loan is a type of non-QM (non-qualified mortgage) designed specifically for real estate investors. Instead of reviewing your personal income, tax returns, or employment history, the lender evaluates whether the rental property generates enough income to cover its own debt payments.

This is a big deal for investors who write off significant expenses on their taxes, run their own businesses, or own multiple properties that make traditional income verification messy. The property does the qualifying — not you.

Here’s how it works in plain terms:

- You identify a rental property (or one you already own).

- The lender orders an appraisal that includes a market rent analysis.

- That projected or actual rent is divided by the total monthly debt service (principal, interest, taxes, insurance, and HOA if applicable).

- The resulting ratio determines your eligibility and pricing.

DSCR loans are not government-backed. They fall under the portfolio lending or non-QM lending category, meaning lenders set their own guidelines. That’s why requirements vary more than they do with FHA or conventional loans. [6]

These loans are available for purchase, rate-and-term refinance, and DSCR cash out refinance scenarios. They’re also available to individuals and entities like LLCs and corporations, which makes them popular for investors who want liability protection through proper entity structuring.

💡 So based: DSCR loans are essentially the real estate investor’s version of a business loan — the asset proves its own worth.

For a broader look at how technology is reshaping how investors analyze deals before applying, check out this guide on real estate investment technology tools.

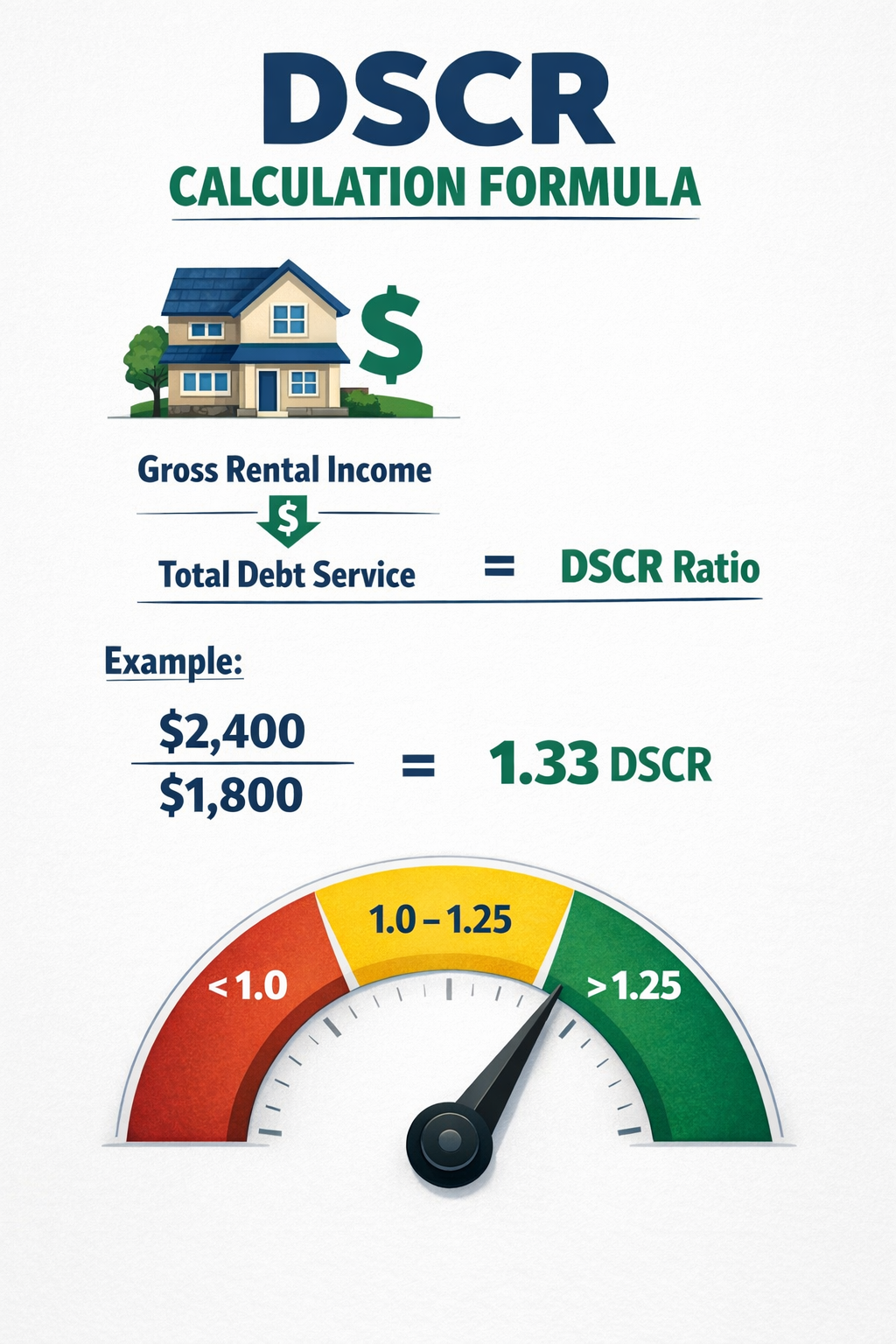

How to Calculate Your DSCR Ratio

The DSCR formula is straightforward: divide the property’s gross monthly rental income by its total monthly debt service. The result tells lenders whether the property pays for itself.

The Formula

DSCR = Gross Rental Income ÷ Total Debt Service

- Gross Rental Income: The monthly rent the property generates (or is projected to generate based on the appraisal).

- Total Debt Service: Principal + Interest + Property Taxes + Insurance + HOA fees (often called PITIA).

Numerical Example

| Scenario | Gross Rent | PITIA | DSCR |

|---|---|---|---|

| Strong cash flow | $2,800 | $2,000 | 1.40 |

| Break-even | $2,000 | $2,000 | 1.00 |

| Negative cash flow | $1,700 | $2,000 | 0.85 |

A DSCR of 1.40 means the property earns 40% more than it costs to carry — lenders love this. A DSCR of 0.85 means the property loses money on paper, and most lenders will either decline or require compensating factors. [5]

Short-term rental (STR) income: In 2026, most DSCR lenders now accept Airbnb or VRBO income as qualifying rental income, typically using 12-month average platform earnings or an appraiser’s short-term rental market estimate. This is a significant shift from prior years when STR income was often excluded entirely. [9]

⚡ Edge case: Some lenders calculate DSCR using only principal and interest (not full PITIA). This inflates the ratio and makes approval easier — but it also means you’re not accounting for real carrying costs. Always ask which method a lender uses before assuming your ratio qualifies.

DSCR Loan Requirements: Full Breakdown

DSCR loan requirements vary by lender, but the core criteria are consistent across the non-QM lending market. Here’s what you actually need to qualify.

Minimum DSCR Ratio by Lender

Most lenders set their floor at 1.0, meaning the property breaks even. Some will go as low as 0.75 to 0.99 for strong borrowers with compensating factors like high credit scores or large reserves. The best rates and terms, however, are reserved for ratios of 1.25 and above. [3]

| DSCR Ratio | Typical Lender Response |

|---|---|

| Below 0.75 | Likely declined by most lenders |

| 0.75 – 0.99 | May qualify with compensating factors; expect higher rates |

| 1.00 – 1.24 | Standard approval; average pricing |

| 1.25 – 1.49 | Good approval odds; competitive rates |

| 1.50+ | Strongest pricing; easiest approval |

Pro tip: If your DSCR is borderline, increasing your down payment can lower the debt service and push your ratio above the threshold. [5]

Credit Score Requirements

DSCR loan credit score requirements typically start at 620, but the pricing tiers are meaningful:

| Credit Score Range | Impact on Loan |

|---|---|

| 620 – 659 | Minimum threshold; higher rates, stricter terms |

| 660 – 699 | Standard approval; moderate pricing |

| 700 – 739 | Good pricing; broader lender options |

| 740+ | Best available rates; maximum flexibility |

First-time investors with lower credit scores should expect lenders to apply additional risk premiums, especially on cash-out refinance scenarios. [7] If your score is below 700, it’s worth spending 3 to 6 months improving it before applying — the rate difference can add up to tens of thousands over the loan term.

Down Payment Requirements

DSCR loan down payment requirements are typically 20% to 25% of the purchase price for most property types. Here’s how it breaks down:

| Property Type | Typical Down Payment |

|---|---|

| Single-family rental (1 unit) | 20% – 25% |

| 2-4 unit residential | 20% – 25% |

| 5+ unit multifamily | 25% – 30% |

| Condos | 25% – 30% |

| Short-term rentals | 25% – 30% |

| Mixed-use properties | 25% – 35% |

Cash reserves are also required by most lenders — typically 3 to 12 months of PITIA payments held in a liquid account after closing. First-time investors and those doing a DSCR cash out refinance often face stricter reserve requirements. [9]

🔑 Decision rule: If you’re purchasing a short-term rental or a 5+ unit property, budget for 25% down minimum and 6 months of reserves. Don’t show up to the closing table underprepared.

Property Types That Qualify

DSCR loans are available for a wide range of income-producing properties. Here’s what most lenders accept in 2026:

Eligible property types:

- ✅ Single-family residences (non-owner occupied)

- ✅ 2-4 unit residential properties

- ✅ 5+ unit multifamily (availability has expanded significantly in 2026) [7]

- ✅ Condominiums (warrantable and some non-warrantable)

- ✅ Townhomes

- ✅ Short-term rentals (Airbnb, VRBO)

- ✅ Mixed-use properties (residential/commercial)

Generally NOT eligible:

- ❌ Owner-occupied primary residences

- ❌ Rural properties on large acreage (varies by lender)

- ❌ Vacant land

- ❌ Commercial-only properties (these use a different loan structure)

For investors exploring different property categories and their investment potential, this comprehensive guide to the 4 essential property types for investments is worth bookmarking.

Loan Limits and Terms

Loan amounts for DSCR loans typically range from $100,000 to $5 million, with some portfolio lenders going higher for experienced investors. [9]

Loan terms available:

- 30-year fixed

- 15-year fixed

- 5/1, 7/1, and 10/1 ARMs (adjustable-rate)

- Interest-only options (available from select lenders)

Prepayment penalties are common on DSCR loans — typically 3 to 5 years of step-down penalties (e.g., 5-4-3-2-1%). Factor this in if you plan to sell or refinance within the first few years.

Current DSCR Loan Rates in 2026

As of early 2026, DSCR loan rates range from approximately 6.5% to 8.75% for most borrowers. [3] These rates do not move in lockstep with Federal Reserve decisions — they respond more directly to investor demand, secondary market conditions, and the strength of the underlying property’s cash flow. [2]

Rate drivers to understand:

| Factor | Effect on Rate |

|---|---|

| DSCR ratio 1.30+ | Lower rate (best pricing tier) |

| Credit score 740+ | Lower rate |

| 30%+ down payment | Lower rate |

| Short-term rental income | Slight premium |

| Cash-out refinance | Higher rate vs. purchase |

| First-time investor | Risk premium added |

| 5+ unit property | Slightly higher rate |

Current rate ranges by borrower profile (estimates based on 2026 market data): [3]

| Borrower Profile | Estimated Rate Range |

|---|---|

| Strong (DSCR 1.30+, 740+ credit, 25% down) | 6.5% – 7.25% |

| Standard (DSCR 1.10-1.29, 700 credit, 20% down) | 7.25% – 7.75% |

| Marginal (DSCR 1.0, 660 credit, 20% down) | 7.75% – 8.75% |

⚠️ Important note: These are market estimates based on available 2026 lender data. Actual rates vary by lender, property type, loan amount, and market conditions. Always get multiple quotes.

For context on how broader mortgage rate trends are affecting real estate investors in 2026, see this analysis of 2026 real estate trends and how stable rates are reshaping strategies.

Best DSCR Lenders Compared

The DSCR lending space has grown considerably, and not all lenders are created equal. Some specialize in single-family rentals, others in multifamily or short-term rentals. Here’s a comparison of notable DSCR lenders based on publicly available information. (Note: Lender programs change frequently — always verify current terms directly.)

| Lender | Min. DSCR | Min. Credit Score | Min. Down Payment | Loan Range | STR Eligible | Notable Feature |

|---|---|---|---|---|---|---|

| Kiavi | 1.0 | 660 | 20% | $75K – $3M | Yes | Fast online process; strong for SFR investors |

| Lima One Capital | 1.0 | 660 | 20% | $75K – $5M | Yes | Flexible on property types; portfolio options |

| Visio Lending | 1.0 | 680 | 20% | $100K – $2M | Yes | Specializes exclusively in rental loans |

| Griffin Funding | 0.75 | 620 | 20% | $100K – $5M | Yes | Accepts sub-1.0 DSCR with compensating factors |

| New Silver | 1.0 | 650 | 20% | $100K – $5M | Yes | Tech-forward; fast pre-approval |

| Newfi Lending | 1.0 | 620 | 20% | $150K – $3M | Limited | Competitive on credit score floor [1] |

| AmeriHome Mortgage | 1.0 | 680 | 25% | $100K – $3M | Yes | Strong for multi-property investors [2] |

Affiliate note: Some lenders listed above offer referral programs. Real Estate Rank IQ may receive compensation if you apply through partner links — this never influences our analysis or recommendations.

How to choose:

- First-time investor with lower credit: Griffin Funding or Newfi (lower credit floor)

- Short-term rental property: Visio, Lima One, or Kiavi

- 5+ unit multifamily: Lima One Capital or AmeriHome

- Fastest closing needed: New Silver or Kiavi

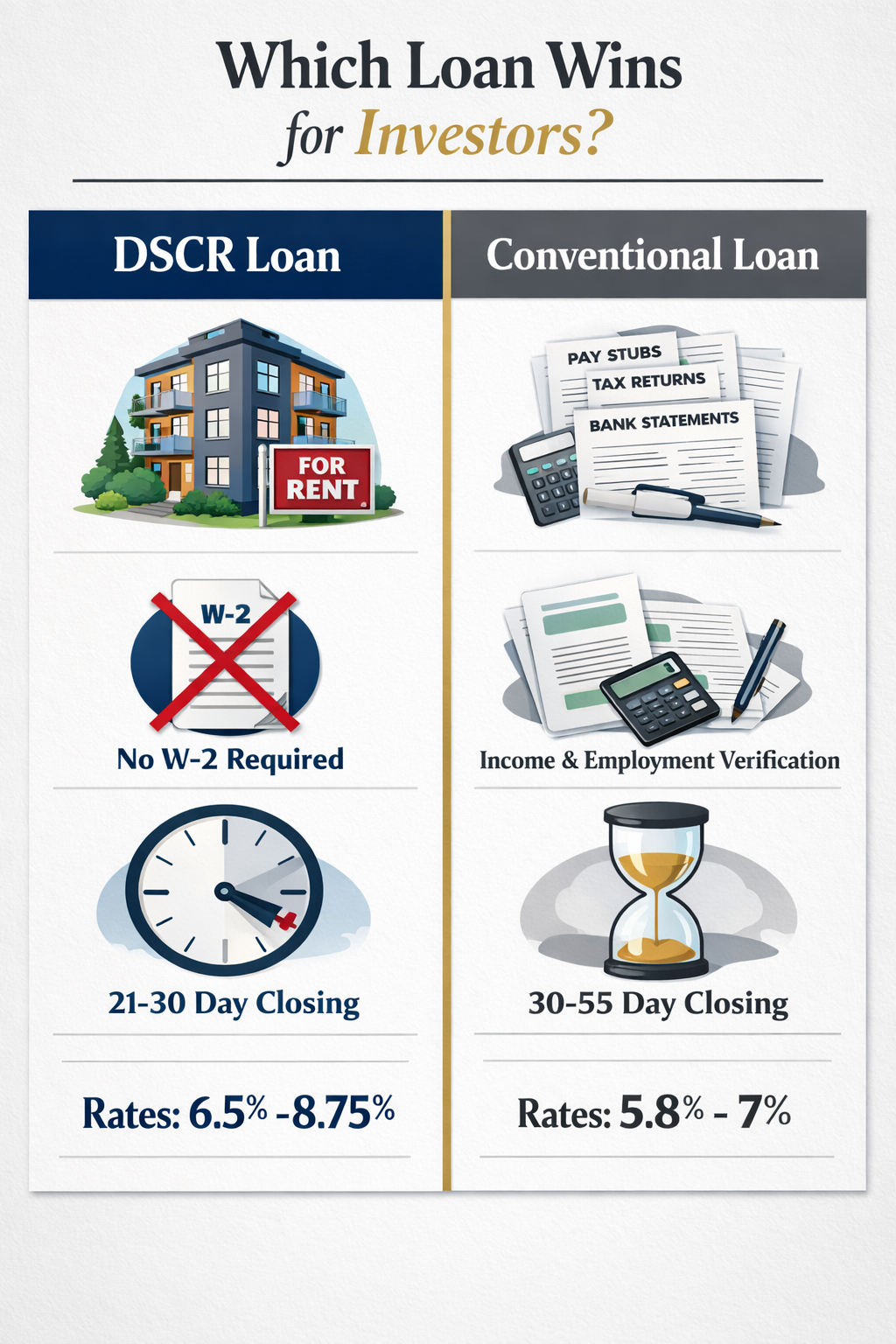

DSCR Loan vs. Conventional Loan: Key Differences

Conventional investment property loans and DSCR loans serve different investor profiles. Here’s the honest comparison:

| Feature | DSCR Loan | Conventional Investment Loan |

|---|---|---|

| Income verification | Property cash flow only | Personal income, W-2s, tax returns |

| Best for | Self-employed, portfolio investors | W-2 earners with clean income history |

| Interest rate range | 6.5% – 8.75% [3] | 5.8% – 7.0% [4] |

| Closing timeline | 21 – 30 days [4] | 30 – 55 days [4] |

| Max properties financed | Unlimited (varies by lender) | Typically capped at 10 (Fannie Mae) |

| LLC/entity eligible | Yes | Generally no |

| Down payment | 20% – 30% | 15% – 25% |

| Credit score minimum | 620 | 620 – 640 |

| Loan limits | Up to $5M+ | Conforming limits apply |

The bottom line: Conventional loans offer lower rates but come with strict income documentation requirements and property limits. DSCR loans cost slightly more but give investors speed, flexibility, and the ability to scale without hitting a ceiling. [2]

Hard money loans are a third option worth mentioning. They’re asset-based like DSCR loans but carry rates of 9% to 15%, terms of 6 to 24 months, and are designed for flips rather than long-term holds. If you’re flipping rather than renting, check out this guide on the best loans for flipping houses in any market.

Choose DSCR if: You’re self-employed, have complex taxes, want to use an LLC, or are scaling beyond 10 properties.

Choose conventional if: You have strong W-2 income, want the lowest possible rate, and are buying your first or second investment property.

How to Apply for a DSCR Loan Step by Step

Getting a DSCR loan pre-approval and closing efficiently comes down to preparation. Here’s the actual process:

Step 1: Run your DSCR numbers before contacting lenders

Calculate your estimated ratio using the property’s market rent and projected PITIA. If the ratio is below 1.0, either renegotiate the purchase price, increase your down payment, or find a different property.

Step 2: Check and optimize your credit score

Pull your credit reports from all three bureaus. Dispute errors, pay down revolving balances, and avoid new credit inquiries for 60 to 90 days before applying.

Step 3: Gather your documents

Unlike conventional loans, DSCR loans don’t require tax returns or pay stubs. You will typically need:

- Government-issued ID

- Entity documents (if applying as an LLC or corporation)

- Bank statements showing reserves (3 to 12 months of PITIA)

- Signed purchase contract (for purchases)

- Existing lease agreements (for refinances)

- Property insurance quote

Step 4: Get DSCR loan pre-approval from multiple lenders

Apply to at least 3 lenders simultaneously. Multiple hard inquiries within a 14 to 45-day window are typically treated as a single inquiry for credit scoring purposes. Compare rates, fees, prepayment penalties, and reserve requirements — not just the rate.

Step 5: Order the appraisal

The lender will order a DSCR-specific appraisal that includes a rent schedule (Form 1007 for single-family, Form 1025 for 2-4 units). This appraisal determines the qualifying rent used in your ratio calculation. [8]

Step 6: Underwriting and approval

DSCR underwriting focuses on the property, not your personal finances. Expect questions about the property’s rental history, condition, and local market. Respond quickly to any lender requests to avoid delays.

Step 7: Close and fund

Average closing timeline is 21 to 30 days from completed application. [4] Experienced investors with all documents ready have closed in as few as 14 days with tech-forward lenders.

💡 Fresh tip: Using AI-powered tools to analyze market rents and property cash flow before you apply can sharpen your numbers and prevent surprises at the appraisal stage. See how investors are using real estate AI tools to do exactly this.

Tax Implications of DSCR Loans (A Gap Competitors Miss)

Most DSCR loan guides skip the tax conversation entirely. That’s gatekeeping information investors actually need.

Key tax considerations:

Interest deductibility: Mortgage interest on DSCR loans used for investment properties is generally deductible as a business expense, reducing your taxable rental income. This is one of the core advantages of investment property financing.

Depreciation: Owning the property through a DSCR loan doesn’t change your ability to depreciate the asset. Residential rental properties depreciate over 27.5 years under current IRS rules, which can significantly offset rental income on paper — ironically, the same write-offs that make DSCR loans necessary for many investors.

Entity structure and taxes: If you hold the property in an LLC taxed as a pass-through entity, income and deductions flow to your personal return. Some investors use S-corps or partnerships for different tax outcomes. Consult a CPA familiar with real estate before choosing your structure.

1031 exchanges: Properties financed with DSCR loans are eligible for 1031 exchanges, allowing you to defer capital gains taxes when selling and reinvesting in a like-kind property. For a detailed breakdown, see this guide on 1031 exchange basics, rules, and timelines.

Cash-out refinance proceeds: Funds received from a DSCR cash out refinance are not taxable income — they’re debt. This is a key strategy for investors who want to pull equity from appreciated properties without triggering a taxable event.

DSCR Loan Pros and Cons

No financing tool is perfect. Here’s an honest assessment:

Pros ✅

- No personal income verification — ideal for self-employed investors and those with complex tax situations

- Unlimited properties — most DSCR lenders don’t cap the number of loans you can hold

- LLC and entity eligible — supports proper asset protection strategies

- Faster closing — 21 to 30 days vs. 30 to 55 for conventional loans [4]

- Short-term rental income accepted — Airbnb and VRBO properties now qualify with most lenders [9]

- Available for 5+ unit multifamily — expanded access in 2026 [7]

- Cash-out refinance available — pull equity without triggering income verification hurdles

Cons ❌

- Higher rates than conventional loans — typically 0.5% to 2.0% higher [3][4]

- Larger down payment required — 20% to 30% vs. 15% to 20% for some conventional options

- Prepayment penalties — common on 3 to 5-year step-down schedules

- Reserve requirements — 3 to 12 months of PITIA required in liquid accounts

- Property must cash flow — if the market rent doesn’t support the debt service, you don’t qualify

- Higher rates for first-time investors — lenders add risk premiums for inexperienced borrowers [7]

- Not for primary residences — strictly for non-owner-occupied investment properties

Risk Assessment: What Can Go Wrong

Most DSCR loan guides stop at the approval checklist. But experienced investors know the real risk comes after closing.

Vacancy risk: Your DSCR is calculated on projected or current rent. If the property sits vacant for 2 to 3 months, your actual cash flow drops below the ratio that qualified you. Build 3 to 6 months of reserves specifically for vacancy.

Rent market softening: In markets where rents are declining (a real trend in some Sun Belt metros in 2026), a property that qualified at a 1.25 DSCR could drift toward break-even or below. Monitor your local rental market quarterly.

Rate risk on ARMs: If you took a 5/1 ARM to get a lower initial rate, understand what the rate caps are and what your payment looks like at the maximum adjustment. Run the numbers before you sign.

Prepayment penalty traps: Selling or refinancing within the penalty period can cost 2% to 5% of the loan balance. On a $500,000 loan, that’s $10,000 to $25,000. Know your exit timeline before choosing a loan structure.

For a broader view of how market conditions are shifting for investors in 2026, this overview of Sun Belt real estate trends is worth reading.

Frequently Asked Questions

What is a DSCR loan?

A DSCR loan (Debt Service Coverage Ratio loan) is a non-QM mortgage for real estate investors that qualifies borrowers based on a rental property’s income rather than the investor’s personal income or tax returns. The property’s gross rent must meet or exceed the total monthly debt service (principal, interest, taxes, insurance, and HOA). [6]

What is the minimum DSCR ratio to qualify for a loan?

Most DSCR lenders require a minimum ratio of 1.0, meaning the property’s rental income exactly covers its debt payments. Some lenders accept ratios as low as 0.75 with compensating factors. For the best rates and easiest approval, aim for 1.25 or higher. [5]

What credit score do you need for a DSCR loan?

The minimum credit score for most DSCR lenders is 620. However, borrowers with scores below 680 will face higher interest rates and stricter reserve requirements. A score of 720 or above typically unlocks the most competitive pricing available. [1]

How much do you need to put down on a DSCR loan?

DSCR loan down payment requirements are typically 20% to 25% for single-family and 2-4 unit properties. Short-term rentals, condos, and 5+ unit properties generally require 25% to 30% down. Most lenders also require 3 to 12 months of cash reserves after the down payment. [9]

Can you get a DSCR loan for a short-term rental (Airbnb)?

Yes. As of 2026, most DSCR lenders accept short-term rental income as qualifying income, typically using 12-month average platform earnings or an appraiser’s market rent estimate for short-term use. Expect a slightly higher rate and larger down payment requirement compared to long-term rentals. [9]

What are current DSCR loan rates in 2026?

DSCR loan rates in 2026 range from approximately 6.5% to 8.75%, depending on the borrower’s credit score, DSCR ratio, down payment, and property type. Borrowers with a DSCR of 1.30 or higher and a credit score of 740+ can access rates at the lower end of that range. Rates respond to secondary market conditions rather than directly to Federal Reserve policy. [3][2]

How long does it take to close a DSCR loan?

The average DSCR loan closes in 21 to 30 days from completed application, which is faster than conventional investment loans that typically take 30 to 55 days. Investors who have their documents ready and work with tech-forward lenders can sometimes close in as few as 14 days. [4][8]

Can I get a DSCR loan through an LLC?

Yes. DSCR loans are one of the few mortgage products that allow borrowers to take title and close in the name of an LLC, corporation, or other legal entity. This is a key advantage for investors who want liability protection without sacrificing access to financing. [6]

What is a DSCR cash out refinance?

A DSCR cash out refinance allows an investor to refinance an existing rental property, pull out equity as cash, and qualify based on the property’s rental income rather than personal income. The proceeds are not taxable income. Expect a slightly higher rate than a purchase or rate-and-term refinance, and lenders typically cap cash-out at 70% to 75% loan-to-value. [5]

How is DSCR different from a hard money loan?

Hard money loans are short-term (6 to 24 months), carry rates of 9% to 15%, and are designed for property flips or bridge situations. DSCR loans are long-term (15 to 40 years), carry rates of 6.5% to 8.75%, and are designed for buy-and-hold rental properties. Both are asset-based, but they serve completely different investment strategies. [3]

Conclusion: Your Next Steps

DSCR loans are one of the most practical financing tools available to real estate investors in 2026 — especially those who are self-employed, scaling a portfolio, or investing through an LLC. The qualification process is genuinely simpler than conventional lending, but the requirements are still specific and the costs are real.

Here’s what to do next:

- Calculate your target property’s DSCR before contacting any lender. If it’s below 1.0, adjust the purchase price or down payment before proceeding.

- Pull your credit reports and address any issues at least 60 to 90 days before applying.

- Build your reserves. Most lenders want 6 months of PITIA liquid after closing. Don’t let reserves be the reason you get declined.

- Get pre-approved by at least 3 lenders simultaneously. Rate differences of even 0.25% matter over a 30-year term.

- Understand your prepayment penalty before signing. Know your exit strategy and make sure the loan structure matches it.

- Talk to a CPA about entity structure and tax strategy before closing — especially if this is your first DSCR loan.

The investors who use DSCR loans most effectively treat them as a tool within a broader portfolio strategy, not a shortcut. When the property cash flows and the numbers are dialed in, these loans are extraordinary for scaling a rental portfolio without the friction of traditional income verification.

References

[1] Dscr Loan Requirements – https://newfi.com/dscr-loan-requirements/

[2] Finance Multiple Investment Properties With A Dscr Loan – https://www.amerihome.com/pages/finance-multiple-investment-properties-with-a-dscr-loan/

[3] Dscr Loan Interest Rates In 2026 Current Trends Expert Insights Investor Guide – https://investmentpropertyloanexchange.com/dscr-loan-interest-rates-in-2026-current-trends-expert-insights-investor-guide

[4] Dscr Loan Closing Timeline Explained – https://honestcasa.com/blog/dscr-loan-closing-timeline-explained

[5] Dscr Loans Explained The Ultimate 2026 Investors Guide – https://reliancefinancial.com/dscr-loans-explained-the-ultimate-2026-investors-guide/

[6] What Is A Dscr Loan Complete Guide For Real Estate Investors – https://housemaxfunding.com/blog/what-is-a-dscr-loan-complete-guide-for-real-estate-investors

[7] Watch – https://www.youtube.com/watch?v=KKhel-8rXbc

[8] Dscr Loan Closing Timeline Guide – https://honestcasa.com/blog/dscr-loan-closing-timeline-guide

[9] Dscr Loan Requirements – https://www.zeitro.com/blog/dscr-loan-requirements

[10] Dscr Loans – https://agorareal.com/learn/dscr-loans/

{kind=link}