Last updated: March 17, 2026

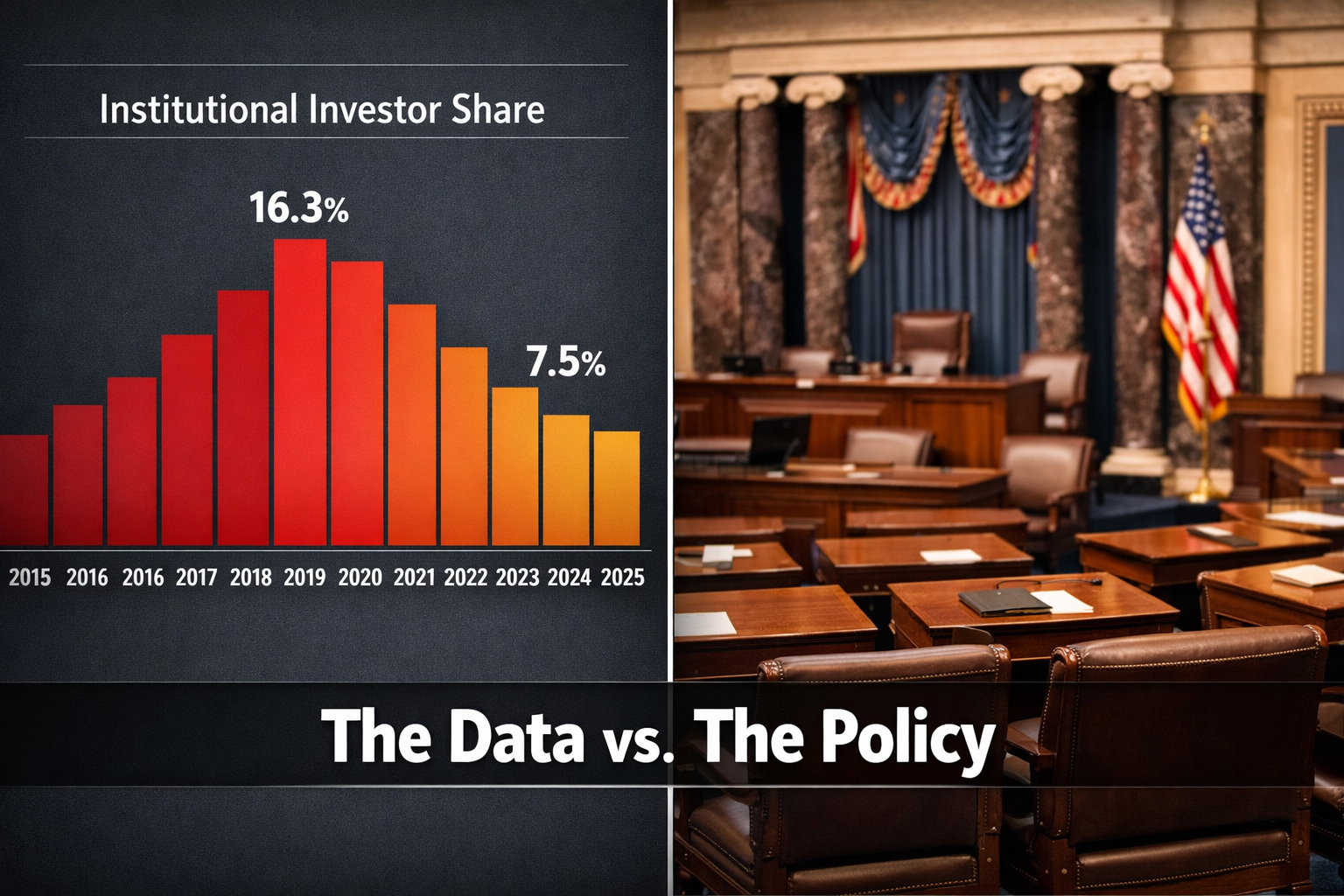

The Senate just passed a sweeping housing bill that bans institutional investors owning 350+ single-family homes from buying more. But fresh data from Realtor.com suggests the ban targets a shrinking problem: large institutional investors accounted for just 1% of all U.S. single-family home sales from 2015 to 2025, and their market share among investors has dropped from a 16.3% peak in 2021 to 7.5% in 2025 [1][5].

Key Takeaways

- The 21st Century ROAD to Housing Act passed the Senate 89-10 on March 12, 2026, and includes a ban on institutional investors (350+ homes) from purchasing additional single-family properties [6].

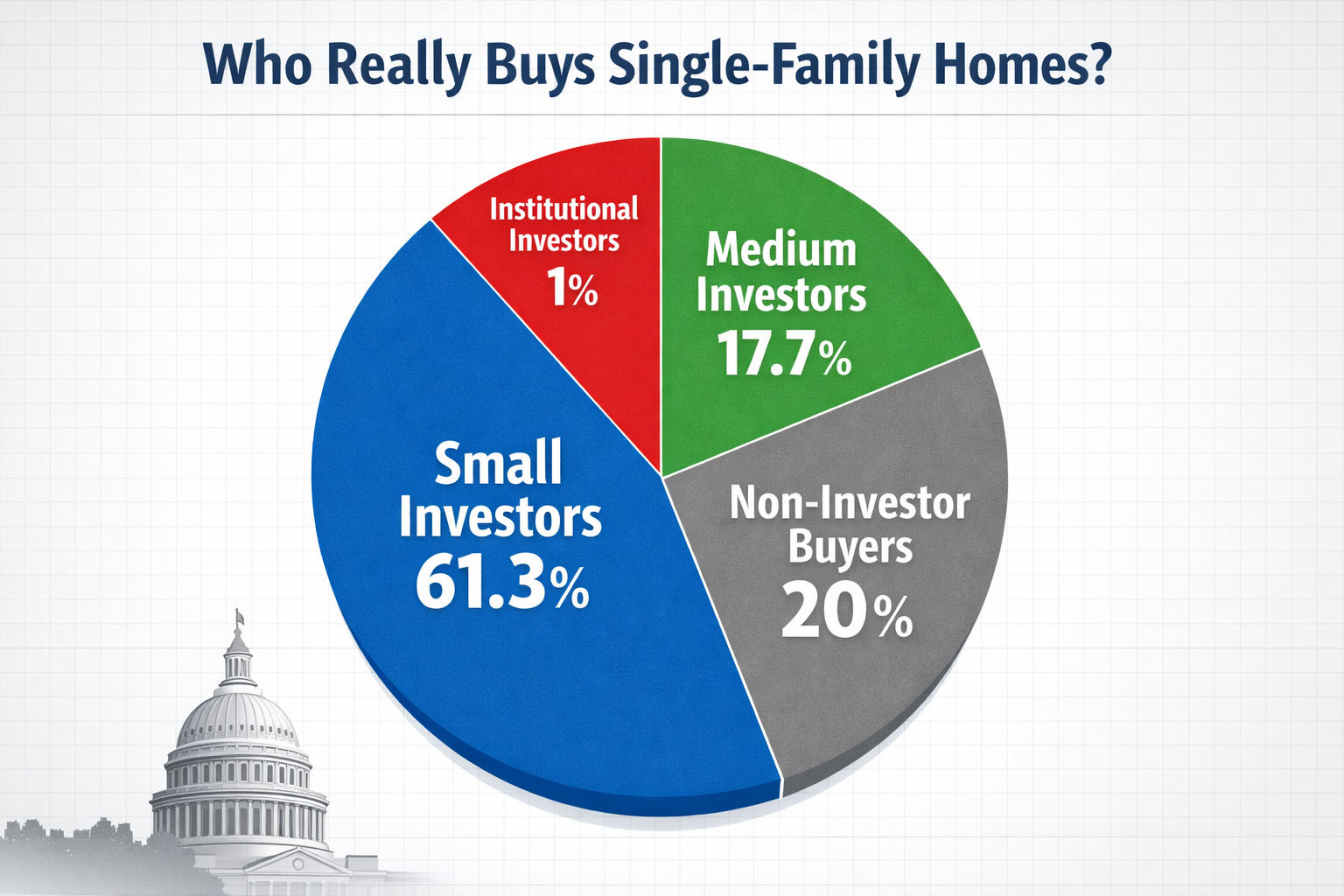

- Realtor.com's "Shrinking Institutional Investor Footprint" report (March 13, 2026) found these large investors represent only 1% of all single-family sales nationally over the past decade [5][1].

- Institutional investors' share of all investor purchases dropped from 16.3% in 2021 to 7.5% in 2025, while small investors now account for 61.3% of investor buys [1][5].

- The National Association of Home Builders warns the bill's seven-year forced sale provision for build-to-rent homes could reduce single-family production by 40,000 units per year [9].

- The bill still faces House reconciliation, with disputes over unrelated amendments like community bank reforms and a CBDC moratorium potentially stalling progress [6].

- Housing affordability remains a real crisis: the Bipartisan Policy Center estimates a 1.2 million home shortage nationwide [9].

- The ban's practical impact may be limited because institutional activity is already declining on its own, according to Realtor.com economist Jake Krimmel [4].

What Does the Realtor.com Data Actually Show About Institutional Investors?

Institutional investors buying up American neighborhoods has been a hot-button issue since the post-pandemic housing frenzy. But Realtor.com data casts doubt on Senate plan to ban big home investors by revealing just how small the institutional footprint really is.

On March 13, 2026, Realtor.com released its report titled "The Shrinking Institutional Investor Footprint," analyzing deed records from 2015 through 2025 [5]. Here's what the numbers show:

Who counts as an institutional investor?

In the context of this legislation and Realtor.com's analysis, an institutional investor is defined as any entity that has purchased 350 or more single-family homes since 2015 [5][1]. Think companies like Invitation Homes or American Homes 4 Rent, not your neighbor who owns a couple of rental properties.

The national numbers

| Metric | Value | Source |

|---|---|---|

| Institutional investor share of all U.S. single-family sales (2015–2025) | 1% | Realtor.com [5] |

| Institutional share of investor purchases (2021 peak) | 16.3% | Realtor.com [1] |

| Institutional share of investor purchases (2025) | 7.5% | Realtor.com [5] |

| Small investor share of investor purchases (2025) | 61.3% | Realtor.com [1] |

That 1% figure is the headline that changes the conversation. While corporate home buying has dominated media coverage and political rhetoric, the actual market concentration is far smaller than most people assume.

Realtor.com economist Jake Krimmel told HousingWire that the ban targets a "decreasing trend," offering limited "bite" now compared to several years ago [4][1]. Small investors — individuals or entities purchasing fewer homes — now dominate the investor landscape at 61.3% of all investor purchases in 2025.

For anyone tracking housing market trends and investment planning, this data is extraordinary. The narrative and the numbers don't quite match.

What's Actually in the Senate Housing Bill?

The 21st Century ROAD to Housing Act is the largest housing legislation package in roughly 30 years, and it covers far more than just the investor ban. Sen. Elizabeth Warren called it the "biggest package…in 30 years" after the Senate vote [9].

Key provisions of the Senate housing bill

- Institutional investor purchase ban: Entities owning 350+ single-family homes cannot buy additional ones [6][7].

- Seven-year forced sale requirement: Build-to-rent institutional investors must sell their single-family holdings within seven years [9].

- Homebuilding incentives: Tools and funding to encourage more residential construction [7].

- Zoning reform elements: Provisions aimed at reducing barriers to new housing development.

- Community bank reforms: Included in the broader package, though these are causing reconciliation headaches [6].

The bill passed the Senate with an overwhelming 89-10 bipartisan vote on March 12, 2026 [6]. It combines elements from the House-passed H.R. 6644 (which passed 390-9 on February 9, 2026) with Senate additions, including the investor ban that was prioritized by President Donald Trump through his earlier Executive Order 14376 [7].

The National Association of Realtors applauded the passage, highlighting the homebuilding tools in the package [7]. But the investor ban provision has drawn sharp criticism from housing supply advocates.

Where things get complicated

As of March 16, 2026, the bill faces real hurdles in House reconciliation. The House version didn't include the investor ban at all — it focused on bank deregulations and zoning reforms [6]. Unrelated disputes over amendments like CBDC bans could stall or strip the investor provision entirely.

If you're a real estate professional watching this unfold, understanding the broader 2026 market predictions alongside this legislation gives much better context for advising clients.

How Does Realtor.com Data Cast Doubt on Senate Plan to Ban Big Home Investors at the Metro Level?

National averages can hide a lot. While institutional investors represent just 1% of sales nationally, their presence is concentrated in specific Sun Belt metros where the impact feels much larger [5][1].

Metro-level market concentration

Realtor.com's analysis reveals that institutional investor activity clusters heavily in markets like:

- Atlanta, GA — One of the highest concentrations of institutional single-family purchases

- Charlotte, NC — Significant build-to-rent activity from large investors

- Phoenix, AZ — Major institutional buying during 2020–2022, now declining

- Dallas-Fort Worth, TX — Large-scale investor activity, though also declining

- Jacksonville, FL — Notable institutional presence in the rental market

In these metros, institutional investors may represent a significantly higher share of purchases than the 1% national average. But even in these hotspots, the trend line is heading down [5].

This is where the policy debate gets interesting. A ban designed around national data may not address the localized pain points that residents in Atlanta or Phoenix actually experience. And conversely, it applies restrictions in markets like the Midwest or Northeast where institutional investors are barely present at all.

For investors exploring emerging Sun Belt real estate markets, this metro-level breakdown matters more than national headlines.

The regional variation problem

A one-size-fits-all federal ban doesn't account for the fact that housing market dynamics vary wildly by region. Markets with high institutional activity might benefit from targeted intervention. Markets with almost no institutional presence gain nothing from the ban but still face affordability challenges driven by entirely different factors — low inventory, high construction costs, and restrictive zoning.

Why Is the Housing Affordability Crisis Bigger Than Institutional Investors?

Here's the part that often gets lost in the political debate: even if you banned every institutional investor tomorrow, the housing affordability crisis wouldn't disappear. The Bipartisan Policy Center estimates a 1.2 million home shortage nationally [9], and that gap has structural causes that go well beyond corporate home buying.

The real drivers of housing unaffordability

- Chronic underbuilding: The U.S. has underbuilt housing for over a decade. Zoning restrictions, labor shortages, and rising material costs have all contributed.

- High mortgage rates: Rates in 2026 continue to keep monthly payments elevated for buyers.

- Existing homeowner lock-in: Millions of homeowners with sub-4% mortgage rates aren't selling, which constrains supply.

- Small investor activity: Small investors — not institutions — now represent 61.3% of all investor purchases [1]. The ban doesn't touch them.

- Land use regulations: Local zoning laws in many metros prevent the density needed to meaningfully increase supply.

The National Association of Home Builders' Bill Owens made a pointed warning: the seven-year forced sale provision for build-to-rent homes could actually cut single-family production by 40,000 units per year [9]. That's because institutional build-to-rent developers are some of the few entities building new single-family homes specifically for the rental market. Remove that incentive, and you potentially lose supply.

NAHB's chair stated the provision would "severely reduce investment in rental housing" [9]. For a market already short 1.2 million homes, reducing new construction is the opposite of what's needed.

If you're a first-time buyer trying to break into this market, understanding pre-approval strategies and market timing is more immediately useful than waiting for legislation to fix things.

What Are Better Policy Alternatives to an Investor Ban?

Since Realtor.com data casts doubt on Senate plan to ban big home investors as an effective affordability solution, what might actually move the needle? Several economists and housing policy experts have suggested alternatives that address root causes rather than a shrinking symptom.

Alternative approaches worth considering

- Expand zoning reform incentives: Federal funding tied to local zoning changes that allow more housing types (duplexes, ADUs, missing middle housing).

- Increase housing production tax credits: Similar to the Low-Income Housing Tax Credit but expanded to moderate-income housing.

- First-time buyer down payment assistance: Direct subsidies that help buyers compete in the market rather than restricting who can sell.

- Targeted local regulations: Allow cities with high institutional concentration to implement their own restrictions, rather than a blanket federal ban.

- Construction workforce development: Address the labor shortage that's one of the biggest bottlenecks to new housing supply.

- Build-to-rent incentives with affordability requirements: Instead of banning build-to-rent, require a percentage of units to be offered at below-market rents.

The bill does include some of these elements — particularly homebuilding incentives and zoning provisions [7]. But the investor ban has gotten most of the attention, and the data suggests it's the least impactful piece of the package.

For investors rethinking strategy in light of potential policy changes, exploring AI-driven market analysis tools can help identify opportunities regardless of what happens in Congress.

How Have Institutional Investor Purchases Changed Since 2015?

The trend line tells a clear story. Institutional investor activity in single-family homes surged during the pandemic-era housing boom and has been declining since.

Timeline of institutional investor activity

| Year Range | Trend | Key Context |

|---|---|---|

| 2015–2019 | Moderate, steady activity | Post-Great Recession recovery; institutional investors building portfolios |

| 2020–2021 | Sharp increase to 16.3% peak of investor purchases | Pandemic housing boom, low rates, remote work migration [1] |

| 2022–2023 | Decline begins | Rising interest rates, cooling market |

| 2024–2025 | Continued decline to 7.5% of investor purchases | Higher costs, market correction, some portfolio sales [5] |

This trajectory matters because it shows the market was already self-correcting. Higher interest rates and tighter margins made the single-family rental business less attractive for large institutions. The ban, in effect, targets a problem that was already shrinking on its own.

Realtor.com's Hannah Jones and Jake Krimmel emphasized this point in their research: the institutional investor footprint is shrinking without legislative intervention [5][1].

What Does This Mean for Different Market Participants?

For home buyers

The ban, if it survives reconciliation, won't dramatically change your competitive landscape. You're far more likely to compete against small investors and other owner-occupant buyers than against Invitation Homes. Focus on smart negotiation strategies and getting pre-approved rather than waiting for policy relief.

For home sellers

Fewer institutional buyers in the market could mean slightly less demand in Sun Belt metros where they've been active. But with a 1.2 million home shortage, demand from other buyers remains strong. If your home isn't selling, the issue is more likely pricing or presentation than a lack of institutional interest.

For real estate investors

Small and mid-size investors are unaffected by this ban. If anything, reduced institutional competition in certain markets could create opportunities. Understanding property management fundamentals and local market analysis becomes even more valuable as the investor landscape shifts toward smaller players.

For real estate agents and brokers

The legislation's homebuilding provisions could eventually increase inventory — which would be fresh news for buyer's agents who've been struggling with low supply. The investor ban itself is unlikely to change day-to-day business in most markets.

Global Comparison: How Does the U.S. Approach Compare?

The U.S. isn't the only country grappling with institutional investment in residential real estate. A few comparisons add perspective:

- Canada: Implemented a two-year ban on foreign buyers of residential property in 2023, later extended. Results have been mixed, with prices driven more by domestic supply constraints.

- Germany: Berlin attempted a rent cap in 2020, which was struck down by courts in 2021. Institutional ownership remains a political flashpoint.

- Australia: Foreign investment restrictions have been in place for years, with mixed effectiveness on affordability.

- New Zealand: Banned most foreign buyers in 2018. Prices continued rising until interest rate hikes cooled the market.

The common thread? Demand-side restrictions alone rarely solve affordability problems when the fundamental issue is insufficient supply. Let it cook for a moment — every country that's tried to ban its way to affordability without building more homes has come up short.

Conclusion

The Realtor.com data is so based in its clarity: institutional investors buying 350+ single-family homes represent just 1% of all U.S. single-family sales, and their activity has been declining since 2021 [5][1]. The Senate's 21st Century ROAD to Housing Act is an extraordinary piece of legislation — the most significant housing package in three decades — but the investor ban may be its least impactful provision.

The real affordability crisis is driven by a 1.2 million home shortage, restrictive zoning, high construction costs, and mortgage rate lock-in. Solving those problems requires building more homes, not just restricting who can buy existing ones.

Actionable next steps:

- Buyers: Don't wait for legislation. Get pre-approved and focus on markets where you can compete.

- Investors: Monitor the reconciliation process, but don't overhaul your strategy based on a ban that may not survive the House.

- Agents: Educate clients on what the data actually shows versus the headlines. This is a gatekeeping opportunity — be the expert who cuts through the noise.

- Everyone: Watch for the homebuilding provisions in the bill. Those could have a much bigger long-term impact on housing supply and affordability than the investor ban.

For the latest housing market analysis and investment strategies, visit Real Estate Rank IQ or subscribe to the Real Estate Rank IQ YouTube channel for weekly updates. Have questions? Reach out at news@realestaterankiq.com.

Frequently Asked Questions

What percentage of homes do institutional investors actually purchase?

According to Realtor.com's March 2026 report, institutional investors (entities that purchased 350+ homes since 2015) account for just 1% of all U.S. single-family home sales from 2015 to 2025 [5].

What is the 21st Century ROAD to Housing Act?

It's a bipartisan housing bill that passed the U.S. Senate 89-10 on March 12, 2026. It includes provisions for homebuilding incentives, zoning reforms, and a ban on institutional investors owning 350+ single-family homes from making additional purchases [6][7].

Has the investor ban been signed into law yet?

No. As of March 17, 2026, the bill still needs to go through House reconciliation. The House version did not include the investor ban, and disputes over unrelated amendments could delay or eliminate the provision [6].

How have institutional investor purchases changed since 2021?

Institutional investors' share of all investor purchases peaked at 16.3% in 2021 and dropped to 7.5% by 2025. Small investors now dominate with 61.3% of investor purchases [1][5].

Will the investor ban lower home prices?

Unlikely on its own. With institutional investors representing just 1% of sales nationally and their activity already declining, the ban addresses a shrinking share of market activity. The 1.2 million home shortage is a much larger driver of high prices [5][9].

What is the seven-year forced sale provision?

The bill requires institutional investors in the build-to-rent space to sell their single-family holdings within seven years. NAHB warns this could reduce single-family construction by 40,000 units per year [9].

Does the ban affect small real estate investors?

No. The ban only applies to entities that have purchased 350 or more single-family homes since 2015. Individual investors, small landlords, and mid-size investors are not affected [5][6].

Which metros have the highest institutional investor activity?

Sun Belt markets like Atlanta, Charlotte, Phoenix, Dallas-Fort Worth, and Jacksonville have historically seen the highest concentrations of institutional single-family purchases [5].

Who supports the investor ban?

President Trump prioritized it through Executive Order 14376, and it had bipartisan Senate support. Sen. Tim Scott negotiated the provision with White House input [7][9].

Who opposes the investor ban?

The National Association of Home Builders opposes it, arguing the forced sale provision would "severely reduce investment in rental housing" and cut new construction [9].

What would be more effective than an investor ban?

Most housing economists point to increasing supply through zoning reform, construction workforce development, and targeted subsidies for first-time buyers as more impactful approaches to affordability.

References

[1] Investor Ban Single Family Homes For American Families – https://www.realtor.com/news/real-estate-news/investor-ban-single-family-homes-for-american-families/

[4] Realtor Com Data Challenges Effectiveness Of Senate Ban On Big Home Investors – https://jorgensonrealestate.com/blog/Realtor-com-data-challenges-effectiveness-of-Senate-ban-on-big-home-investors

[5] Corporate Investors March 2026 – https://www.realtor.com/research/corporate-investors-march-2026/

[6] Us Senate Advances Housing Legislation That Includes A Ban On Institutional Investors Purchasing Single Family Homes – https://www.mayerbrown.com/en/insights/publications/2026/03/us-senate-advances-housing-legislation-that-includes-a-ban-on-institutional-investors-purchasing-single-family-homes

[7] Senate Advances 21st Century Road To Housing Act Investor Ban – https://www.realtor.com/news/real-estate-news/senate-advances-21st-century-road-to-housing-act-investor-ban/

[9] Senate Backs Bill To Limit Institutional Investors In Buying Houses – https://www.costar.com/article/1058332434/senate-backs-bill-to-limit-institutional-investors-in-buying-houses

SEO Meta Title: Realtor.com Data Casts Doubt on Senate Investor Ban

SEO Meta Description: Realtor.com data shows institutional investors make up just 1% of U.S. home sales. See why the Senate's investor ban may miss the real affordability problem.

{kind=link}