Picture this: You're sitting on a goldmine—literally. Your home has appreciated by $100K, $200K, maybe even more since you bought it. The mortgage balance keeps shrinking, your equity keeps growing, and now you're wondering: What's the move? Do you cash out while the market is still strong? Stay put and refinance at today's lower rates? Or transform that asset into a rental income machine?

Welcome to the most extraordinary dilemma facing homeowners in 2026. With mortgage rates hovering around 6%—their lowest since 2022—and national home prices showing modest but steady growth, the Sell, Stay, or Rent It Out? 2026 Decision Guide for Homeowners Sitting on Big Equity has never been more critical. [6][7]

This isn't your typical "should I sell my house?" article. Real Estate Rank IQ is bringing you expert-backed analysis from licensed brokers with over 15 years of experience, blending hard data with actionable strategies to help you make the smartest decision for your financial future.

Let's let it cook and break down your options.

Key Takeaways

- Mortgage rates near 6% create new opportunities for both sellers and buyers, easing the "rate lock" effect that kept inventory tight in 2023-2024 [6]

- National home prices are projected to rise modestly (1-2.2%) in 2026, with regional variations creating different opportunities across the country [4][7]

- Rental yields are compressing in 55% of U.S. counties as home prices outpace rent growth, making the rental math more complex than ever [2]

- Nearly 18% of single-family homes are now rentals, with 89.6% owned by small "mom-and-pop" landlords—proving this path is viable but competitive

- Tax implications, opportunity costs, and lifestyle factors often matter more than the raw numbers when deciding between selling, staying, or renting

Understanding Your Equity Position in 2026's Market Reality

Before diving into the Sell, Stay, or Rent It Out? 2026 Decision Guide for Homeowners Sitting on Big Equity, let's get real about where the market actually stands.

The Current Market Landscape

Here's what's so based about 2026: The housing market is experiencing what Redfin calls the "Great Housing Reset." [7] After years of wild appreciation and affordability chaos, things are stabilizing:

- Mortgage rates: Averaging 6.0-6.1% for 30-year fixed loans as of early March 2026 [6][9]

- Home price growth: Expected to rise just 1-2.2% nationally in 2026 [4][7]

- Inventory levels: Up nearly 9% compared to 2025, giving buyers more options [4]

- Sales volume: Projected to increase 1.7-3% as the rate environment improves [4][7]

Translation? The market isn't gatekeeping opportunities anymore. Whether you're selling, staying, or converting to a rental, conditions are more favorable than they've been in years.

Your Equity: The Foundation of Every Decision

Your built-up equity is the star of this show. If you purchased before 2020, you're likely sitting on substantial appreciation. Even if you bought during the 2021-2022 peak, you've probably built meaningful equity through principal paydown and modest appreciation.

Calculate your current position:

| Component | How to Find It |

|---|---|

| Current home value | Check Zillow, Redfin, or get a CMA from a local agent |

| Remaining mortgage balance | Latest mortgage statement |

| Your equity | Current value – mortgage balance |

| Equity percentage | (Equity ÷ Current value) × 100 |

If your equity percentage is above 20%, you have real options. Above 30%? You're in an extraordinary position to make strategic moves.

Option 1: Selling Your Home in 2026—When It Makes Sense

The fresh take on selling in 2026 isn't just about timing the market—it's about aligning your financial goals with current opportunities.

The Case for Selling Now

You should seriously consider selling if:

✅ You need to relocate for work, family, or lifestyle changes

✅ Your home no longer fits your needs (too big, too small, wrong location)

✅ You want to capture gains and redeploy capital into other investments

✅ Maintenance costs are climbing faster than your appreciation

✅ You can avoid or minimize capital gains taxes (more on this below)

With inventory rising and buyer competition easing, spring 2026 presents an impeccable window for sellers who prepare properly. Check out our 8 Spring Home Selling Mistakes 2026 That Cost You $40K+ to avoid costly errors.

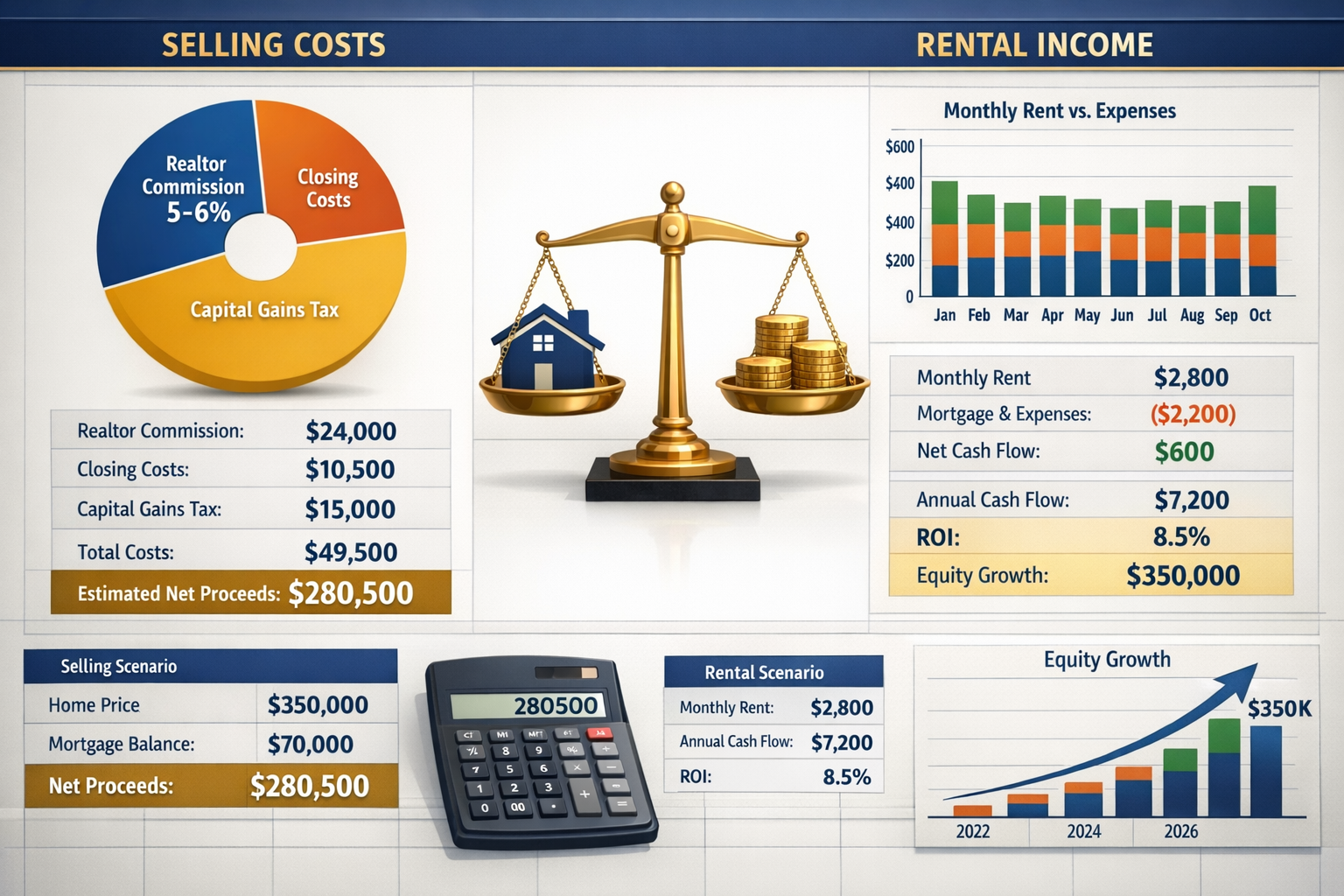

The Real Costs of Selling

Before you list, understand what selling actually costs:

Typical selling expenses:

- Realtor commissions: 5-6% of sale price ($15,000-$18,000 on a $300,000 home)

- Closing costs: 1-3% of sale price ($3,000-$9,000)

- Repairs and staging: $2,000-$10,000+ depending on condition

- Moving expenses: $1,500-$5,000+

Example scenario:

- Sale price: $400,000

- Remaining mortgage: $180,000

- Gross equity: $220,000

- Selling costs (8%): -$32,000

- Net proceeds: $188,000

That's still substantial, but it's important to be realistic about what you'll actually walk away with.

Tax Implications: The $250K/$500K Rule

Here's where the Sell, Stay, or Rent It Out? 2026 Decision Guide for Homeowners Sitting on Big Equity gets interesting.

The IRS allows you to exclude up to $250,000 in capital gains ($500,000 for married couples) if you've lived in the home as your primary residence for at least 2 of the past 5 years. [2]

If your gain exceeds these thresholds, you'll pay capital gains tax on the excess:

- Long-term capital gains rates: 0%, 15%, or 20% depending on income

- Potential 3.8% Net Investment Income Tax for high earners

Pro tip: If you're considering converting to a rental, do the math on selling before you rent it out. Once it becomes a rental, the clock starts ticking on that 2-out-of-5-years requirement.

Want to maximize your sale price? Our guide on Unlock Profit: Best Home Improvements Before Selling: Top ROI Projects Ranked shows which upgrades actually pay off.

Option 2: Staying Put—Refinancing and Optimizing Your Current Home

Sometimes the smartest move is the one you don't make. Staying in your home and optimizing your financial position can be extraordinarily powerful.

When Staying Makes the Most Sense

Consider staying if:

✅ You locked in a sub-4% mortgage before 2022 (refinancing would cost you)

✅ Your home meets your needs for the next 5+ years

✅ You love your neighborhood and community connections

✅ Local market fundamentals are strong with continued appreciation potential

✅ Moving costs would exceed any financial benefit from selling

The Refinance Opportunity

With rates around 6% in early 2026, refinancing makes sense for homeowners who:

- Currently have rates above 7-8%

- Want to switch from an ARM to a fixed-rate mortgage

- Need to tap equity for home improvements or debt consolidation

- Can reduce their monthly payment by at least $200-300

Cash-out refinance considerations:

If you have substantial equity, a cash-out refinance lets you access funds while keeping your home. You might use this capital for:

- High-ROI home renovations

- Paying off high-interest debt

- Investment opportunities

- Emergency fund building

Learn more about mortgage options in our 15 vs 30-Year Mortgage Rates 2026: Long-Term Savings Guide.

Maximizing Your Home's Value While Staying

If you're staying put, invest strategically in improvements that boost both your quality of life and future resale value:

High-ROI projects for 2026:

- Kitchen updates (minor remodels: 70-80% ROI)

- Bathroom renovations (65-75% ROI)

- Energy-efficient upgrades (windows, insulation, HVAC)

- Curb appeal enhancements (landscaping, exterior paint)

Check out Yelp 2026: 4 Design Trends For Your Home Transformation for fresh ideas that align with current buyer preferences.

The Opportunity Cost Factor

Here's what many homeowners miss: By staying, you're choosing your current home's appreciation potential over alternative investments.

Questions to ask:

- What's the expected appreciation in your market over the next 5 years?

- Could you achieve better returns investing your equity elsewhere?

- What's the value of stability, community, and avoiding transaction costs?

For many homeowners, the non-financial benefits of staying—school districts, community ties, avoiding moving stress—outweigh pure financial optimization.

Option 3: Converting to a Rental—Building Your Real Estate Portfolio

Here's where the Sell, Stay, or Rent It Out? 2026 Decision Guide for Homeowners Sitting on Big Equity gets really interesting. Nearly 18% of U.S. single-family homes are now rentals, and 89.6% are owned by small landlords like you. [2]

The Rental Income Opportunity

You should consider renting if:

✅ Monthly rent exceeds your PITI (principal, interest, taxes, insurance) by at least 20-30%

✅ You're relocating but want to keep the property for long-term appreciation

✅ Local rental demand is strong with low vacancy rates

✅ You can afford to cover expenses during vacancy periods

✅ You're comfortable being a landlord or hiring property management

The Rental Math: Does It Pencil Out?

Here's the reality check: Rental yields are compressing in about 55% of U.S. counties because home prices have outrun rents. [2] That means you need to run the numbers carefully.

Sample rental analysis:

| Income/Expense | Monthly | Annual |

|---|---|---|

| Rental income | $2,200 | $26,400 |

| Mortgage payment (PITI) | -$1,500 | -$18,000 |

| Property management (10%) | -$220 | -$2,640 |

| Maintenance reserve (1% of value) | -$250 | -$3,000 |

| Vacancy reserve (5%) | -$110 | -$1,320 |

| Net cash flow | $120 | $1,440 |

Cash-on-cash return:

If you have $60,000 in equity, that $1,440 annual cash flow represents a 2.4% return—before accounting for appreciation and principal paydown.

Total return includes:

- Cash flow: $1,440/year

- Principal paydown: ~$4,000-6,000/year (depending on loan age)

- Appreciation: 1-2% of property value

- Tax benefits: Depreciation, expense deductions

Where Renting Beats Buying (and Vice Versa)

According to 2026 data, it's cheaper to buy than rent in a majority of U.S. counties, especially in the Midwest and South. Renting remains cheaper in much of the West. [10]

Best markets for landlords in 2026:

- Midwest metros (strong rental demand, affordable entry)

- Growing Southern markets (population growth, job creation)

- College towns (consistent tenant pool)

Challenging markets:

- High-cost coastal cities (compressed yields)

- Oversupplied Sun Belt markets (increased competition)

Property Management: DIY or Hire Out?

Self-management works if:

- You live nearby (within 30-60 minutes)

- You're handy and can handle minor repairs

- You have time for tenant calls, showings, and coordination

- You enjoy the landlord role

Hire a property manager if:

- You're relocating or live far away

- Your time is worth more than the 8-10% management fee

- You want professional tenant screening and lease enforcement

- You prefer passive income over active involvement

For property management comparisons, see Airbnb Vs Vacasa: Property Management Cost Comparison 2026.

Tax Considerations for Rental Conversion

When you convert your primary residence to a rental, several tax implications kick in:

Benefits:

- Deduct mortgage interest, property taxes, insurance, repairs, and management fees

- Depreciate the building value over 27.5 years

- Deduct mileage and travel related to property management

Drawbacks:

- Lose the $250K/$500K capital gains exclusion if you don't sell within 3 years of moving out

- Pay depreciation recapture tax when you eventually sell

- Report rental income and deal with more complex tax returns

The 2-out-of-5-year rule reminder: You must have lived in the home as your primary residence for at least 2 of the past 5 years to qualify for the capital gains exclusion. If you rent it out for more than 3 years, you lose this benefit.

Regulatory Risks in 2026

Here's something fresh: Political momentum is building for restrictions on single-family rental purchases, especially by institutional investors. California's AB 1611, effective January 1, 2026, bans corporations owning 50+ homes from using 1031 exchanges. [2]

While this targets large investors, it signals a shifting regulatory landscape. Stay informed about local ordinances around:

- Rental licensing requirements

- Occupancy restrictions

- Rent control measures

- Short-term rental bans

Making Your Decision: A Framework for Homeowners in 2026

Now that we've explored all three options in this Sell, Stay, or Rent It Out? 2026 Decision Guide for Homeowners Sitting on Big Equity, let's build a decision framework.

Step 1: Define Your Goals

What matters most to you?

| Priority | Favors Selling | Favors Staying | Favors Renting |

|---|---|---|---|

| Maximize liquidity | ✅ | ❌ | ⚠️ |

| Build long-term wealth | ⚠️ | ✅ | ✅ |

| Generate passive income | ❌ | ❌ | ✅ |

| Minimize complexity | ⚠️ | ✅ | ❌ |

| Relocate flexibility | ✅ | ❌ | ✅ |

| Tax optimization | ✅ | ✅ | ⚠️ |

Step 2: Run the Numbers

Create a comparison spreadsheet:

- Selling scenario: Calculate net proceeds after all costs

- Staying scenario: Project 5-year appreciation, mortgage paydown, and opportunity cost

- Rental scenario: Model cash flow, total returns, and tax benefits

Don't forget to factor in:

- Your current mortgage rate vs. market rates

- Local market appreciation forecasts

- Rental demand and vacancy rates in your area

- Your personal tax situation

- Alternative investment returns (stock market, other real estate)

Step 3: Assess Your Risk Tolerance

Selling = Certainty: You know exactly what you'll walk away with (minus some closing cost variables).

Staying = Moderate risk: You're betting on continued local appreciation and that your home continues to meet your needs.

Renting = Higher risk: You're exposed to tenant issues, market fluctuations, maintenance surprises, and regulatory changes.

Ask yourself:

- Can I afford vacancy periods and unexpected repairs?

- Am I comfortable with tenant management responsibilities?

- Do I have emergency reserves for both properties (if relocating)?

- What's my backup plan if the rental strategy doesn't work?

Step 4: Consider the Lifestyle Factor

This is where the spreadsheet ends and real life begins.

Selling might be right if:

- You're ready for a fresh start in a new location or home

- The burden of maintaining your current property outweighs the financial benefits

- You want to simplify your financial life

Staying might be right if:

- Your home is in a neighborhood you love with strong community ties

- Your kids are in great schools you don't want to leave

- The non-financial benefits outweigh potential financial gains elsewhere

Renting might be right if:

- You're entrepreneurial and enjoy building a real estate portfolio

- You see long-term appreciation potential in your market

- You're relocating but not ready to sever ties with your current area

Step 5: Get Expert Input

Don't make this decision in a vacuum. Consult with:

- Real estate agent: For current market comps and selling timeline

- Property manager: For realistic rental income and expense projections

- Tax professional: For capital gains, depreciation, and tax strategy

- Financial advisor: For overall wealth-building strategy and opportunity cost analysis

- Mortgage broker: For refinancing options and investment property loans

Real Estate Rank IQ provides expert-backed guidance to help you navigate these complex decisions.

Regional Considerations: Where You Live Matters

The Sell, Stay, or Rent It Out? 2026 Decision Guide for Homeowners Sitting on Big Equity looks different depending on your location.

West Coast Markets

Characteristics:

- High home prices but compressed rental yields

- J.P. Morgan projects potential price declines in some markets

- Renting often cheaper than buying [10]

Best strategy: Selling may make more sense if you're relocating, as rental returns are often underwhelming relative to property values.

Midwest and South

Characteristics:

- Affordable home prices with stronger rental yields

- Buying cheaper than renting in most counties [10]

- Steady population and job growth in many metros

Best strategy: Renting out can be highly profitable, especially if you're relocating within the region or want to build a portfolio.

Sun Belt Markets

Characteristics:

- High recent appreciation but increasing inventory

- Some markets showing oversupply concerns

- Strong rental demand from population influx

Best strategy: Market-dependent; run detailed comps for both sales and rentals in your specific submarket.

Northeast Markets

Characteristics:

- Stable, mature markets with modest appreciation

- Higher property taxes impact rental returns

- Strong tenant protections in some states

Best strategy: Staying often makes sense given transaction costs and market stability; renting requires careful cash flow analysis.

Common Mistakes to Avoid

🚫 Emotional decision-making: Don't let attachment to your home cloud financial reality.

🚫 Ignoring opportunity cost: Your equity could potentially earn better returns elsewhere.

🚫 Underestimating rental expenses: Budget for vacancy, maintenance, management, and surprises.

🚫 Overlooking tax implications: Capital gains exclusions and depreciation recapture matter enormously.

🚫 Timing the market perfectly: Waiting for the "perfect" moment often means missing good opportunities.

🚫 Skipping professional advice: The cost of expert guidance is tiny compared to a costly mistake.

For more on avoiding seller mistakes, check out our 60-Day Home Selling Plan & AI Tools for Effective Marketing.

Action Steps: What to Do This Week

Ready to move forward? Here's your immediate action plan:

If leaning toward selling:

- Get 2-3 comparative market analyses from local agents

- Calculate your net proceeds after all costs

- Research spring selling strategies for 2026

- Start decluttering and planning repairs

- Review our first-time home sellers guide

If leaning toward staying:

- Get refinance quotes from 3-5 lenders

- Calculate break-even point on refinancing

- Identify high-ROI home improvements

- Review your long-term financial plan

- Assess whether your home meets 5-year needs

If leaning toward renting:

- Research comparable rental rates in your area

- Interview 2-3 property managers for quotes

- Calculate detailed cash flow projections

- Consult with a tax professional on implications

- Review landlord-tenant laws in your state

- Assess your financing options for your next home

Conclusion

The Sell, Stay, or Rent It Out? 2026 Decision Guide for Homeowners Sitting on Big Equity isn't about finding a one-size-fits-all answer—it's about building a framework that aligns your financial goals, risk tolerance, and lifestyle priorities with current market realities.

Here's what we know for certain in 2026:

✅ Mortgage rates around 6% have unlocked new opportunities for both buyers and sellers [6]

✅ Modest home price growth (1-2.2%) creates a more balanced, less frenzied market [4][7]

✅ Rising inventory gives sellers competition but also signals market normalization [4]

✅ Rental yields are compressing in many markets, requiring careful analysis [2]

✅ Your equity is substantial, giving you real options and leverage

The extraordinary opportunity in 2026 is that you have choices. Unlike the chaotic markets of 2021-2023, you can make deliberate, strategic decisions without feeling rushed.

Your next steps:

- Run the numbers for all three scenarios using current market data

- Consult professionals (agent, tax advisor, property manager) for expert input

- Align with your goals rather than chasing the "optimal" financial outcome

- Make a decision and execute with confidence

- Stay informed with resources like Real Estate Rank IQ to adapt as markets evolve

Whether you sell and capture your gains, stay and optimize your current position, or rent and build a portfolio, the key is making an informed decision that serves your long-term wealth and lifestyle goals.

The market in 2026 is fresh, the opportunities are real, and your equity gives you options. So based on everything we've covered, what's your move?

Ready to dive deeper? Explore more expert guidance at Real Estate Rank IQ or reach out to our team at news@realestaterankiq.com.

References

[1] 2026 Housing Predictions 35800 – https://www.zillow.com/research/2026-housing-predictions-35800/

[2] Should I Sell My House Or Rent It Out – https://smartasset.com/investing/should-i-sell-my-house-or-rent-it-out

[3] 30 Year Mortgage Rates – https://themortgagereports.com/30-year-mortgage-rates

[4] 2026 National Housing Forecast – https://www.realtor.com/research/2026-national-housing-forecast/

[6] 30 Year Mortgage Rate – https://tradingeconomics.com/united-states/30-year-mortgage-rate

[7] Housing Market Predictions 2026 – https://www.redfin.com/news/housing-market-predictions-2026/

[8] Rent Vs Buy 2026 Updated Interest Rates – https://aspyrerealtygroup.com/rent-vs-buy-2026-updated-interest-rates/

[9] Current Mortgage Rates 03 04 2026 – https://fortune.com/article/current-mortgage-rates-03-04-2026/

[10] Cheaper To Buy Than Rent Housing Markets 2026 – https://themortgagereports.com/126300/cheaper-to-buy-than-rent-housing-markets-2026

{kind=link}