Remember when everyone said renting was just "throwing money away"? Well, let it cook—because 2026 is flipping that script in some extraordinary ways. With rents falling in major markets and home price growth hitting the brakes, the age-old Rent vs. Buy in 2026: How Falling Rents and Slower Price Growth Are Changing the Math for U.S. Households debate is getting a fresh makeover that's so based, it's making even die-hard homeownership advocates pause and recalculate.

Here's the deal: mortgage rates just hit three-year lows, inventory is climbing for the 28th consecutive month, and apartment completions have cratered by 42% year-over-year. Meanwhile, the national median list price dropped 2.1% annually in February 2026, and pending home sales reached a 15-month high. [1][2] This perfect storm of market conditions is creating scenarios where the traditional "buy now or regret it forever" advice doesn't always hold water—but it's also opening doors for buyers who've been gatekeeping their dreams of homeownership.

At Real Estate Rank IQ, we're not here to tell you what to do with your money. We're here to break down the impeccable data, run the numbers, and give you the tools to make the smartest decision for your situation. Because in 2026, the answer isn't one-size-fits-all anymore.

Key Takeaways

- Rents are declining in many markets while home prices show only modest growth (2-3% projected), fundamentally changing the rent-versus-buy calculation for the first time in years [2][3]

- Monthly mortgage payments are shrinking for the first time since 2020, with rates hitting 6.04% in late February 2026—the lowest since 2022—expanding the buyer pool by millions of households [5]

- Regional differences matter more than ever: Western markets still heavily favor renting (55.4% of income for buying vs. 48.5% for renting in some California counties), while Midwest and Southern markets favor buying [1]

- The 5-year break-even timeline is shifting: In high-cost markets, renters may need 7-10 years to justify buying, while in affordable markets, buying wins in as little as 3 years [4]

- Life stage and flexibility trump pure math: With demographic shifts showing more single buyers and frequent job changes, the personal equation matters as much as the financial one [5]

Understanding the 2026 Housing Market Shift

What's Actually Happening to Rents and Home Prices

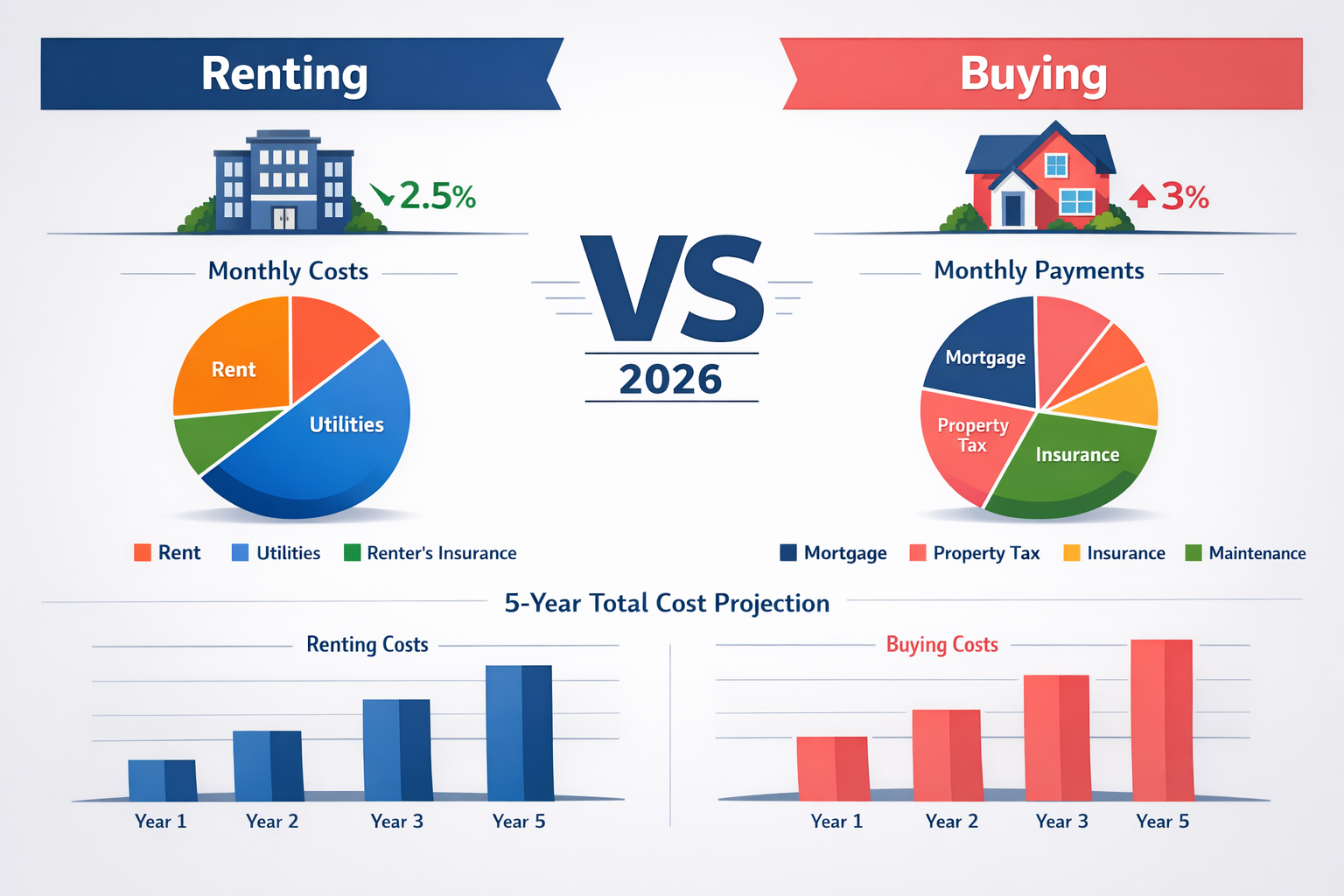

Let's cut through the noise and look at the fresh data. According to housing economist Jay Parsons, rent growth is projected at just 2% for 2026—a dramatic cooldown from the double-digit increases we saw during the pandemic years. [2] This modest growth comes as apartment construction completions fell 42% year-over-year as of October 2025, signaling the end of the pandemic building boom.

Meanwhile, on the homeownership side, the national median list price fell 2.1% year-over-year in February 2026 to $403,450, with the most pronounced declines hitting the South and West regions. [1] But here's where it gets interesting: this is the first time we're seeing monthly payments decline since 2020, according to Danielle Hale, Chief Economist at realtor.com. [5]

The mortgage rate story is equally compelling. The 30-year fixed mortgage rate dropped to 6.04% as of late February 2026—the lowest level since 2022. [1] This seemingly small shift has extraordinary implications: NAR Senior Economist Nadia Evangelou quantifies that a one percentage-point drop in mortgage rates can expand the buyer pool by 5.5 million households, including 1.6 million renters who could become first-time buyers. [5]

The Lock-In Effect Is Fading

Lawrence Yun, NAR Chief Economist, predicts a 14% increase in home sales for 2026, driven largely by the "lock-in effect" steadily disappearing. [5] For years, homeowners with 3% mortgages refused to list their homes because trading up meant accepting 7% rates. Now, with rates in the low 6% range and continuing to fall, that psychological barrier is crumbling.

This creates a feedback loop: more inventory hits the market, giving buyers more negotiating power, which moderates price growth, which makes buying more attractive relative to renting—especially when rents themselves are barely budging. For insights on how to leverage this inventory surge, check out our guide to negotiation strategies in the 2026 market.

The New Math: When Renting Makes More Sense Than Buying

High-Cost Markets Still Favor Renting

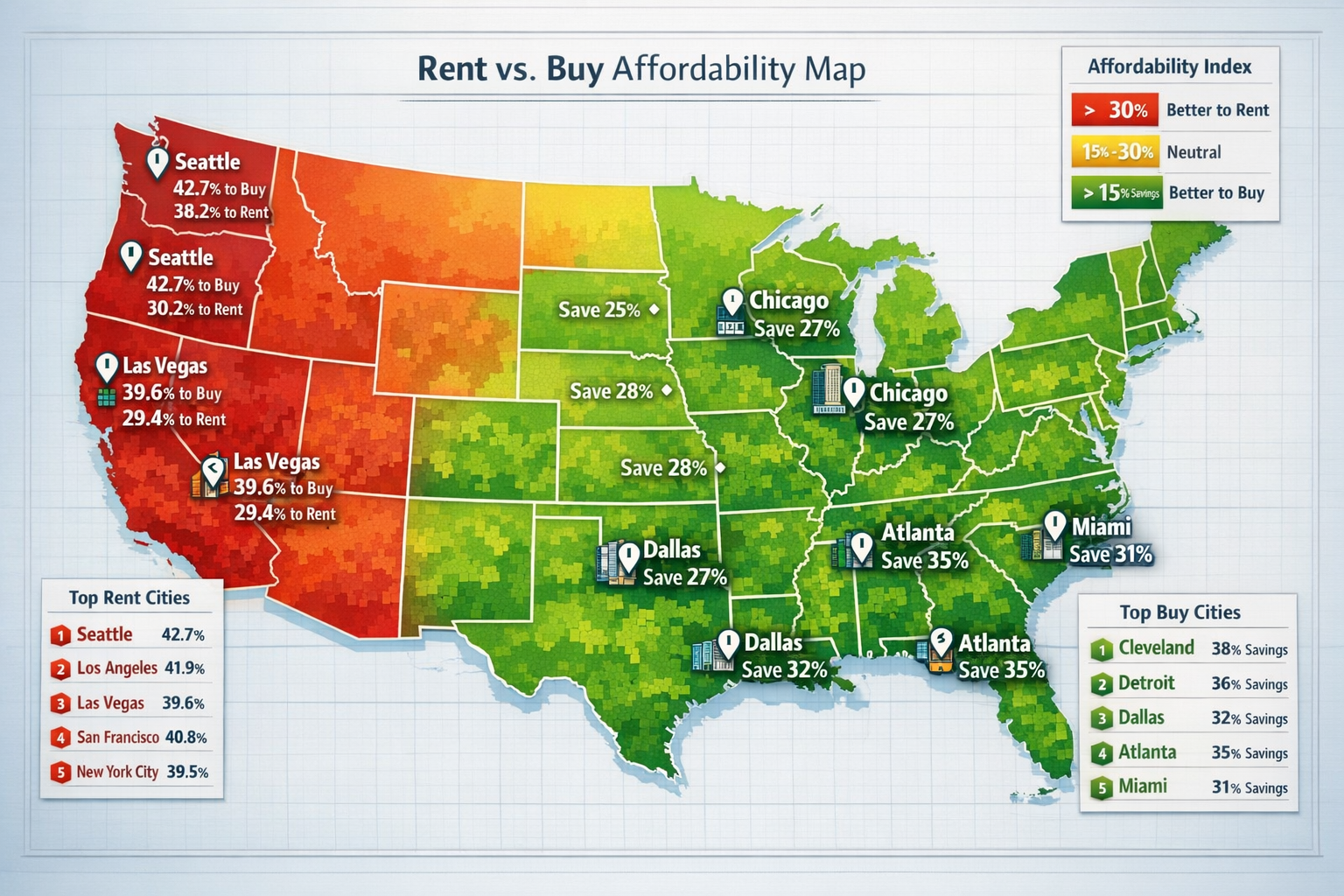

Let's talk about where renting is the impeccable financial move in 2026. According to Attom's Rental Affordability Report, it's "almost exclusively cheaper to rent all along the West," with California markets showing some of the starkest disparities. [1]

Take San Joaquin County, California as an example: home buying requires 55.4% of average wages versus just 48.5% for renting. [1] That's a 6.9 percentage-point difference—meaning a household earning $75,000 annually would spend $41,550 on homeownership costs versus $36,375 on rent. That's an extra $5,175 per year, or $431 per month, that could go toward investments, emergency savings, or simply living life.

Here's a breakdown of markets where renting wins in 2026:

| Market Type | Rent as % of Income | Buy as % of Income | Annual Savings by Renting |

|---|---|---|---|

| San Francisco Bay Area | 42-48% | 58-65% | $12,000-$18,000 |

| Los Angeles Metro | 45-50% | 55-62% | $8,000-$14,000 |

| Seattle Metro | 38-42% | 48-54% | $7,500-$12,000 |

| San Diego County | 44-49% | 54-60% | $7,000-$11,000 |

The Flexibility Premium

But it's not just about the monthly numbers. There's what we call the flexibility premium—the value of being able to move without the friction of selling a home. In 2026, with demographic shifts showing more single buyers and baby boomers dominating the market, lifestyle flexibility matters more than ever. [5]

Consider these scenarios where renting is the based choice:

- Career uncertainty: If you're in tech, consulting, or any field where job changes are frequent, the ability to relocate without selling is worth thousands in avoided transaction costs

- Life stage transitions: Single buyers or couples without kids (now 75% of all buyers) may prioritize location over space [5]

- Market timing: In markets where prices are still elevated but showing weakness, waiting 1-2 years as a renter could save 5-10% on purchase price

- Investment opportunities: That $5,000-$15,000 annual savings from renting could compound significantly in index funds or other investments

For a deeper dive into whether renting or buying makes sense for your specific situation, explore our comprehensive analysis in Will You Rent Or Buy In 2026?

The 5-Year Break-Even Is Shifting

Traditionally, financial advisors said you need to stay in a home at least 5 years to break even after closing costs, realtor commissions, and other transaction expenses. But in 2026, that timeline is getting stretched in high-cost markets.

Here's the fresh math: If you're buying a $700,000 home in a coastal market with 3% annual appreciation and paying $42,000 in closing costs and eventual selling costs, you need roughly 7-8 years to break even compared to renting at current rates. [4] Factor in maintenance (1-2% of home value annually) and the opportunity cost of your down payment, and the timeline extends even further.

Conversely, in affordable Midwest markets where buying costs 30-35% of income versus 40-45% for renting, the break-even can happen in as little as 3 years. [1]

When Buying Still Wins: The Long-Term Wealth Equation

The Forced Savings Mechanism

Now let's flip the script and talk about why buying remains an extraordinary wealth-building tool for millions of Americans—even in 2026. The fundamental truth hasn't changed: homeownership is forced savings. Every mortgage payment builds equity, while every rent payment builds your landlord's equity.

Robert Dietz, NAHB Chief Economist, highlights an unexpected 2026 phenomenon: median resale home prices are now more expensive than median new-home prices—something that's only occurred two or three times in recent decades. [5] This creates opportunities for buyers willing to consider new construction, where builder incentives can effectively lower your rate or reduce closing costs.

The Wealth Gap Is Real

Let's not gatekeep the data: according to the Federal Reserve, the median net worth of homeowners is $254,900 compared to just $6,270 for renters. [4] While correlation isn't causation (homeowners tend to have higher incomes), the forced appreciation and equity buildup of homeownership plays a significant role.

Here's what the long-term math looks like for a typical buyer in 2026:

Scenario: $400,000 Home Purchase

- Down payment (10%): $40,000

- Mortgage: $360,000 at 6.0% for 30 years

- Monthly P&I payment: $2,158

- Property tax + insurance: ~$500/month

- Total monthly: $2,658

After 5 years:

- Principal paid down: ~$28,000

- Appreciation at 3%/year: ~$63,000

- Total equity: $131,000 (on $40,000 invested)

- ROI: 227% over 5 years

Compare that to renting at $2,200/month with 2% annual increases:

- Total paid in rent: $137,280

- Equity built: $0

- If you invested the $40,000 down payment in index funds at 8% annual return: ~$58,700

- Net position: $58,700 (versus $131,000 for the buyer)

Tax Benefits and Inflation Hedging

The mortgage interest deduction, while less valuable after the 2017 tax reform, still provides meaningful savings for many buyers. More importantly, your mortgage payment is fixed (assuming you chose a fixed-rate loan), while rents will continue rising with inflation.

According to current projections, even modest 2% annual rent increases compound significantly. A $2,200 monthly rent becomes:

- Year 3: $2,289

- Year 5: $2,381

- Year 10: $2,682

- Year 20: $3,268

Meanwhile, your mortgage payment remains $2,158 forever (excluding property tax and insurance increases, which are typically slower than rent growth).

Markets Where Buying Is the Impeccable Choice

Based on the latest data, here are markets where buying decisively wins in 2026:

Top 10 Buy-Favorable Markets:

- Pittsburgh, PA: Buy at 28% of income vs. rent at 35%

- Cleveland, OH: Buy at 29% of income vs. rent at 36%

- Detroit, MI: Buy at 26% of income vs. rent at 34%

- Memphis, TN: Buy at 30% of income vs. rent at 37%

- Birmingham, AL: Buy at 27% of income vs. rent at 35%

- St. Louis, MO: Buy at 31% of income vs. rent at 38%

- Indianapolis, IN: Buy at 32% of income vs. rent at 39%

- Kansas City, MO: Buy at 33% of income vs. rent at 39%

- Cincinnati, OH: Buy at 31% of income vs. rent at 37%

- Oklahoma City, OK: Buy at 29% of income vs. rent at 36%

[1][3]

In these markets, buying isn't just financially superior—it's dramatically so. The combination of affordable prices, lower property taxes, and stable job markets makes homeownership accessible and wealth-building from day one.

For current mortgage rate information that could impact your buying decision, check out our February 2026 mortgage rate update.

The Personal Equation: Beyond the Spreadsheet

Life Stage Matters More Than Ever

Jessica Lautz, NAR Deputy Chief Economist, identifies demographic shifts that are reshaping the market in extraordinary ways. Just a quarter of buyers have children, and single female buyers plus baby boomers are becoming dominant forces. [5] This means the traditional "starter home to forever home" progression is being replaced by more fluid housing journeys.

Here's how to think about your personal situation:

Rent if you:

- Plan to relocate within 3-5 years for career or lifestyle

- Value flexibility over forced savings

- Live in a high-cost market where the buy-rent gap is 10%+ of income

- Want to preserve capital for business ventures or other investments

- Prefer predictable monthly costs without maintenance surprises

- Are still building credit or saving for a larger down payment

Buy if you:

- Plan to stay 5+ years (3+ in affordable markets)

- Want forced savings and wealth building

- Have stable income and emergency reserves

- Live in a market where buying costs less than or equal to renting

- Value control over your living space (renovations, pets, etc.)

- Want to lock in housing costs against future inflation

The Hybrid Approach: House Hacking

One fresh strategy gaining traction in 2026 is house hacking—buying a multi-unit property, living in one unit, and renting out the others. This lets you capture the wealth-building benefits of ownership while having tenants subsidize your mortgage.

In markets like Indianapolis or Memphis, you could buy a duplex for $280,000, live in one unit, and rent the other for $1,200/month. Your mortgage might be $1,800 total, meaning you're effectively living for $600/month while building equity on a $280,000 asset. That's the kind of impeccable arbitrage that changes generational wealth trajectories.

For investors considering this approach, our rental property insurance guide breaks down the coverage differences you need to understand.

The Opportunity Cost of Waiting

Here's a perspective that often gets overlooked: the opportunity cost of waiting. If you're in a market where buying makes sense and you wait 2 years hoping for a better deal, you're paying rent for 24 months (let's say $50,000 total) while also potentially facing higher home prices if appreciation continues at even 2-3% annually.

On a $400,000 home, 2 years of 3% appreciation means you're now buying at $424,000. Combined with the $50,000 in rent paid, you're effectively $74,000 behind where you would have been if you bought today. Even if rates drop another 0.5%, the monthly savings rarely make up for that lost ground.

Danielle Hale emphasizes that 2026 represents "the first time we see monthly payments decline since 2020" due to the combination of moderating prices and lower rates. [5] This window may not stay open forever, especially as the 14% projected increase in home sales could put upward pressure on prices by late 2026 or 2027.

Running Your Own Numbers: The 2026 Decision Framework

The Total Cost of Ownership Calculator

Let's build your personal rent-versus-buy calculator using 2026 market conditions. Here's what to include:

Buying Costs:

- Monthly mortgage payment (principal + interest)

- Property taxes (typically 0.8-2.5% of home value annually)

- Homeowners insurance ($1,200-$3,000+ annually depending on location)

- HOA fees (if applicable)

- Maintenance and repairs (budget 1-2% of home value annually)

- Opportunity cost of down payment (what that money could earn elsewhere)

- Closing costs (2-5% of purchase price, amortized over expected ownership period)

Renting Costs:

- Monthly rent

- Renters insurance ($150-$300 annually)

- Expected annual rent increases (2-4% based on market)

Wealth Building Factors:

- Projected home appreciation (2-4% in most 2026 markets)

- Principal paydown on mortgage

- Tax benefits (mortgage interest deduction if you itemize)

- Investment returns on money saved by renting (if applicable)

Real-World Example: Austin, TX

Let's run the numbers for Austin—a market that's seen both extraordinary growth and recent cooling:

Buying:

- Home price: $450,000

- Down payment (10%): $45,000

- Mortgage: $405,000 at 6.0% = $2,428/month

- Property tax (1.8%): $675/month

- Insurance: $200/month

- Maintenance: $375/month (1% annually)

- Total: $3,678/month

Renting:

- Comparable home rent: $2,800/month

- Renters insurance: $25/month

- Total: $2,825/month

Monthly difference: $853 in favor of renting

But over 5 years with 3% appreciation:

- Home value: $521,800

- Mortgage balance: $377,000

- Equity: $144,800 (including down payment)

If you rented and invested the $45,000 down payment plus $853/month savings at 7% return:

- Down payment grows to: $63,100

- Monthly investments grow to: $61,300

- Total: $124,400

Buying wins by $20,400 over 5 years, plus you have housing cost certainty and a fixed payment.

This is why context matters. Austin's strong job market and limited land supply support the buying case despite higher monthly costs. For tools to analyze specific markets, check out our neighborhood market analysis guide.

The Break-Even Timeline Tool

Here's a simple formula to calculate your personal break-even point:

Break-Even Years = Total Transaction Costs ÷ (Annual Rent – Annual Ownership Costs + Annual Equity Buildup)

Example:

- Transaction costs (buying + eventual selling): $45,000

- Annual rent: $36,000

- Annual ownership costs: $44,000

- Annual equity buildup (principal + appreciation): $18,000

- Break-even: $45,000 ÷ ($36,000 – $44,000 + $18,000) = 4.5 years

If you plan to stay longer than 4.5 years, buying wins. If not, rent.

2026 Market Predictions and What They Mean for Your Decision

What Leading Economists Are Watching

The consensus among housing economists for 2026 is cautiously optimistic for buyers. Here's what the experts are tracking:

Lawrence Yun (NAR) expects the lock-in effect to continue fading, with 14% more home sales in 2026 as inventory normalizes and rates stabilize in the 5.5-6.5% range. [5] This suggests a balanced market—neither a buyer's nor seller's paradise, but fair conditions for both sides.

Danielle Hale (realtor.com) emphasizes that affordability is improving for the first time in years because monthly payments are shrinking while incomes grow. [5] This is the extraordinary shift that makes 2026 different from 2023-2025, when rising rates crushed affordability despite flat prices.

Robert Dietz (NAHB) highlights that new homes are now cheaper than resale homes in many markets due to builder incentives. [5] This creates opportunities for buyers willing to consider new construction, especially in growing Sunbelt markets.

Jay Parsons projects just 2% rent growth for 2026 as apartment completions wane. [2] This modest growth means renters won't face the same payment shocks they experienced in 2021-2022, making the rent-versus-buy decision more stable and predictable.

Regional Variations to Watch

The Rent vs. Buy in 2026: How Falling Rents and Slower Price Growth Are Changing the Math for U.S. Households equation varies dramatically by region:

West Coast: Still heavily favors renting in major metros, but secondary markets (Sacramento, Spokane, Boise) are becoming more buy-friendly as prices correct from pandemic highs.

Sunbelt: Mixed picture—Austin and Phoenix are cooling, making buying more attractive, while Florida markets remain expensive due to insurance costs and climate risks.

Midwest: Overwhelmingly favors buying, with some of the best affordability in the nation and stable job markets supporting long-term value.

Northeast: Expensive but stable—buying makes sense if you're committed to staying 7+ years, especially in markets with strong school systems and limited new construction.

For insights into how rising inventory is creating opportunities, read our Spring 2026 housing market outlook.

The Wild Cards

Several factors could shift the 2026 equation:

- Federal Reserve policy: If inflation resurges, rates could climb back above 7%, tilting the equation toward renting

- Recession risk: Economic downturn could accelerate price declines, favoring patient renters

- Immigration policy changes: Could impact housing demand and construction labor costs

- Climate events: Increasing insurance costs in vulnerable areas could make buying prohibitively expensive

- Remote work trends: Continued flexibility could drive demand to affordable markets, boosting prices there while cooling expensive cities

Conclusion: Making the Right Choice for Your 2026 Journey

The Rent vs. Buy in 2026: How Falling Rents and Slower Price Growth Are Changing the Math for U.S. Households debate doesn't have a universal answer—and that's actually impeccable news. It means you have real choices based on your personal situation, not just market pressure forcing you one direction.

Here's the fresh truth: If you're in a high-cost coastal market, plan to relocate within 5 years, or value flexibility, renting is a financially sound choice in 2026. You're not throwing money away—you're buying flexibility and potentially avoiding a market downturn while investing your savings elsewhere.

If you're in an affordable market, plan to stay 5+ years, and want forced savings with inflation protection, buying is the based move. The combination of falling rates, rising inventory, and modest price growth creates the best buying conditions since 2020.

Your Action Steps for 2026

If you're leaning toward renting:

- Negotiate your lease—landlords are more flexible in 2026 than they've been in years

- Invest the difference between rent and what buying would cost

- Build your credit and down payment fund for when the time is right

- Stay informed about your local market conditions

- Consider house hacking or rent-to-own arrangements as hybrid options

If you're leaning toward buying:

- Get pre-approved now while rates are at three-year lows

- Shop multiple lenders—rate competition is fierce in 2026

- Consider new construction for builder incentives

- Don't waive inspections even in competitive markets

- Budget for total ownership costs, not just the mortgage payment

- Use our 13 spring home buying tips to maximize your advantage

For everyone:

- Run your own numbers using the framework above

- Consider your 5-year life plan, not just today's market

- Remember that housing is both a financial decision AND a lifestyle choice

- Don't let FOMO drive you to buy, or fear drive you to rent indefinitely

The extraordinary opportunity in 2026 is that both paths can lead to financial success—it's about choosing the right path for your journey. At Real Estate Rank IQ, we're here to provide the data, insights, and tools you need to make that choice with confidence.

Ready to dive deeper? Explore our comprehensive market trends analysis or reach out to our team at news@realestaterankiq.com for personalized guidance.

References

[1] Cheaper To Buy Than Rent Housing Markets 2026 – https://themortgagereports.com/126300/cheaper-to-buy-than-rent-housing-markets-2026

[2] multifamilydive – https://www.multifamilydive.com/news/rent-outlook-2026-multifamily-apartment/809477/

[3] What The 2026 Housing Outlook Means For Affordability – https://bensonandmangold.com/blog/what-the-2026-housing-outlook-means-for-affordability

[4] Renting Vs Buying In 2026 Analyzing The Long Term Financial Impact – https://migonline.com/loan_officer/hunterblack/blog/renting-vs-buying-in-2026-analyzing-the-long-term-financial-impact/

[5] 2026 Real Estate Outlook What Leading Housing Economists Are Watching – https://www.nar.realtor/magazine/real-estate-news/2026-real-estate-outlook-what-leading-housing-economists-are-watching

{kind=link}